1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicon-Based Microdisplay Chips?

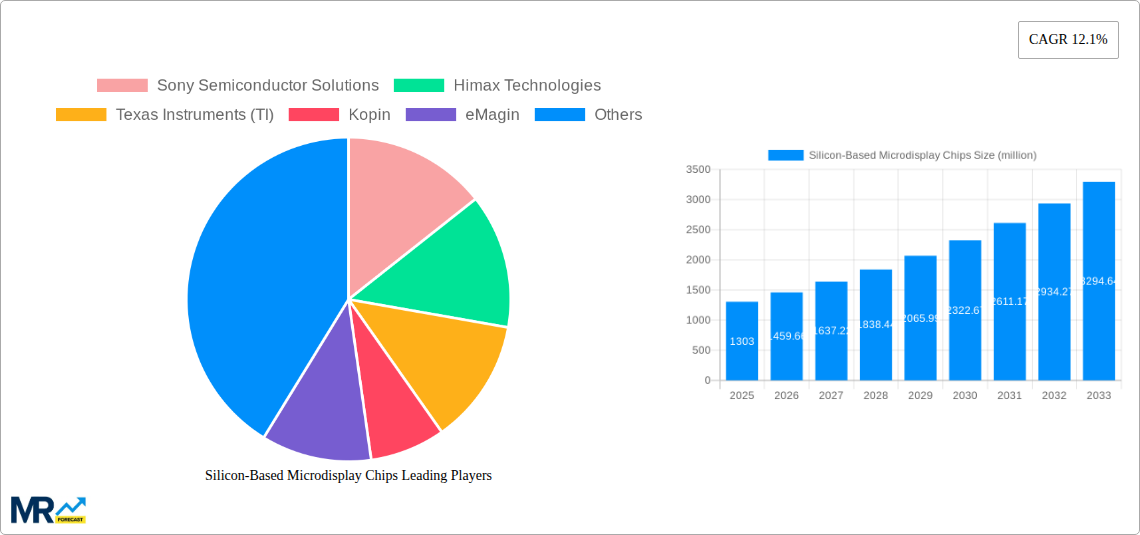

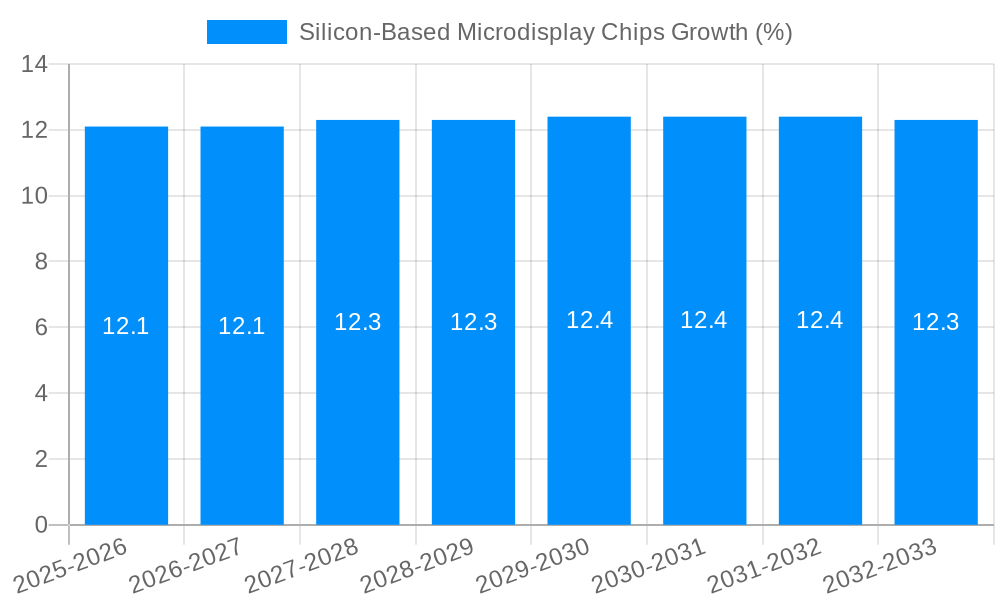

The projected CAGR is approximately 12.1%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Silicon-Based Microdisplay Chips

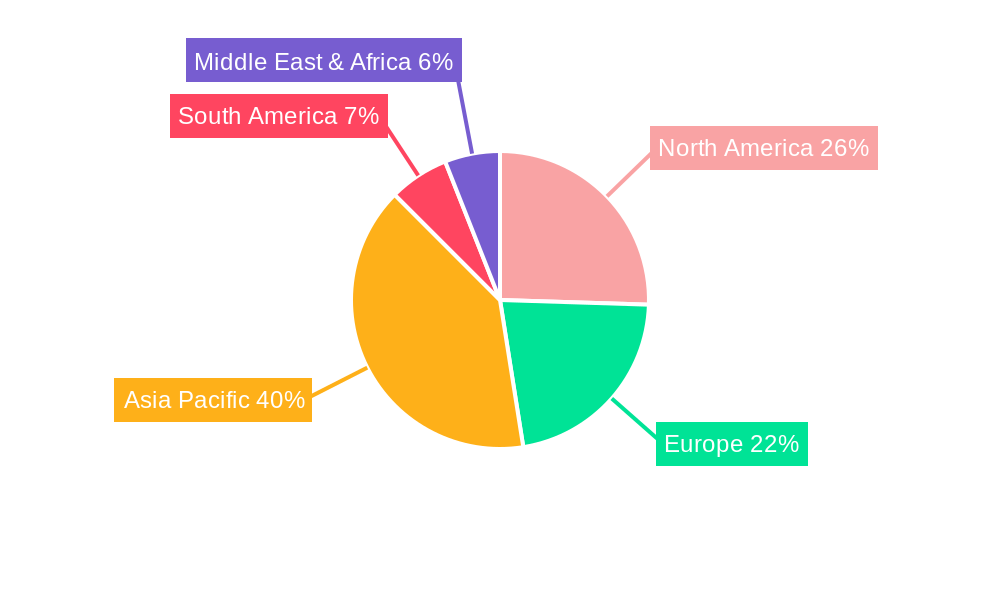

Silicon-Based Microdisplay ChipsSilicon-Based Microdisplay Chips by Application (VR/AR, Micro-Projector, Wearable Devices, Medical Devices, Other), by Type (LCoS, OLED, DLP), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Silicon-Based Microdisplay Chips market is experiencing robust growth, projected to reach approximately USD 1303 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 12.1% expected to drive it through 2033. This significant expansion is fueled by the burgeoning demand across various high-growth sectors, most notably Virtual Reality (VR) and Augmented Reality (AR) devices, where immersive visual experiences are paramount. The miniaturization trend in consumer electronics further propels this market, enabling the development of increasingly sophisticated micro-projectors for mobile devices and pico-projectors, as well as highly integrated wearable devices like smart glasses and advanced fitness trackers. The medical sector also presents a substantial opportunity, with silicon-based microdisplays finding applications in surgical visualization, diagnostic tools, and head-mounted displays for medical professionals, enhancing precision and accessibility. Emerging applications in automotive heads-up displays (HUDs) and advanced imaging systems are also poised to contribute to sustained market expansion.

The market's dynamism is further shaped by key technological advancements and evolving consumer preferences. LCoS (Liquid Crystal on Silicon) and OLED (Organic Light-Emitting Diode) technologies continue to dominate, offering high resolution, excellent contrast ratios, and energy efficiency, crucial for battery-powered portable devices. While DLP (Digital Light Processing) also holds a significant share, particularly in projection applications, the focus on wafer-level optics and integrated functionalities is a prevailing trend. Major industry players such as Sony Semiconductor Solutions, Himax Technologies, and Texas Instruments are at the forefront of innovation, investing heavily in research and development to enhance brightness, reduce power consumption, and improve the overall performance of these microdisplay chips. Despite the immense growth potential, challenges such as high manufacturing costs for certain advanced technologies and the need for greater standardization across different applications could temper the pace of adoption in some segments. However, the relentless pursuit of more compact, power-efficient, and high-performance visual solutions ensures a bright future for silicon-based microdisplay chips across a diverse range of industries.

This comprehensive report offers an in-depth analysis of the global Silicon-Based Microdisplay Chips market, providing critical insights and future projections for stakeholders. Spanning the Study Period of 2019-2033, with a keen focus on the Base Year of 2025 and an Estimated Year also of 2025, this report leverages the Forecast Period of 2025-2033 to map out the trajectory of this dynamic industry. The Historical Period of 2019-2024 has been meticulously examined to establish current market trends and provide a foundation for future estimations. The market is expected to witness robust growth, with the global silicon-based microdisplay chips market size projected to reach USD 15 million by 2025, and further expand to USD 25 million by the end of the forecast period.

The silicon-based microdisplay chips market is currently experiencing a paradigm shift, driven by an insatiable demand for miniaturization, enhanced visual fidelity, and power efficiency across a multitude of applications. XXX highlights that the market's expansion is intricately linked to the burgeoning adoption of augmented reality (AR) and virtual reality (VR) headsets, which represent a significant segment contributing to the projected market valuation. The increasing sophistication of AR/VR applications, from gaming and entertainment to industrial training and remote collaboration, necessitates higher resolution, wider field of view, and lower latency microdisplays, areas where silicon-based technologies excel. Furthermore, the proliferation of wearable devices, including smart glasses and heads-up displays (HUDs) in automotive applications, is another key driver, demanding compact, low-power, and bright display solutions. The report delves into the nuanced trends within different microdisplay types, such as Liquid Crystal on Silicon (LCoS), Organic Light-Emitting Diode (OLED), and Digital Light Processing (DLP), analyzing their respective market shares and growth prospects. For instance, the LCoS segment, known for its high resolution and contrast ratio, is expected to maintain a strong presence, particularly in professional and medical imaging applications. Meanwhile, OLED microdisplays are gaining traction due to their superior brightness, color saturation, and fast response times, making them ideal for premium AR/VR experiences. DLP technology continues to carve out its niche, especially in micro-projector applications where its robustness and brightness are advantageous. The report also scrutinizes the evolving technological landscape, including advancements in fabrication processes, pixel density, and optical efficiency, which are crucial for meeting the ever-increasing performance demands. The competitive intensity within the industry, coupled with continuous innovation, is creating a fertile ground for market expansion. The global market size, which stood at an estimated USD 12 million in 2024, is projected to witness a compound annual growth rate (CAGR) of approximately 5% during the forecast period. The report also examines the impact of emerging technologies, such as micro-LEDs, on the silicon-based microdisplay landscape, assessing their potential to disrupt or complement existing solutions. The integration of artificial intelligence (AI) and machine learning (ML) into microdisplay control systems is also an emerging trend, promising more intelligent and adaptive visual experiences.

The surge in demand for silicon-based microdisplay chips is underpinned by several powerful driving forces. Foremost among these is the rapid expansion of the virtual and augmented reality (VR/AR) market. As VR/AR headsets transition from niche consumer devices to mainstream entertainment and enterprise tools, the need for high-resolution, low-latency, and power-efficient microdisplays becomes paramount. Silicon-based technologies, with their inherent advantages in miniaturization and integration capabilities, are ideally suited to meet these stringent requirements. This surge in VR/AR adoption alone is estimated to contribute USD 8 million to the market by 2025. Secondly, the increasing integration of wearable devices across various sectors is a significant propellant. Smart glasses, advanced fitness trackers, and heads-up displays (HUDs) in automotive applications are all increasingly incorporating microdisplay technology. These devices demand compact form factors, minimal power consumption, and clear, vibrant visuals, all of which silicon-based microdisplays deliver effectively. The medical device segment, particularly for surgical visualization and diagnostic tools, is also showcasing robust growth, driven by the need for precise and detailed imaging, adding an estimated USD 3 million to the market by 2025. The ongoing technological advancements in semiconductor manufacturing, enabling higher pixel densities and improved optical performance, directly translate into more sophisticated and appealing microdisplay solutions. This innovation cycle, where improved chip technology fuels better display performance, creates a virtuous loop of demand. Finally, the growing demand for compact and efficient projection systems, including pico projectors for mobile devices and specialized industrial applications, further bolsters the market. These systems rely on the miniaturization and high brightness capabilities offered by silicon-based microdisplays like DLP. The combined effect of these factors is creating a robust and expanding market for silicon-based microdisplay chips, projected to reach USD 15 million by 2025.

Despite the promising growth trajectory, the silicon-based microdisplay chips market faces several significant challenges and restraints. One of the primary hurdles is the high cost of manufacturing and R&D. The intricate fabrication processes involved in producing high-resolution, low-defect microdisplays require substantial capital investment in specialized foundries and equipment. This can lead to higher unit costs, particularly for niche applications or smaller production volumes, potentially limiting adoption in price-sensitive segments. The initial setup for a state-of-the-art microdisplay fabrication facility can easily exceed USD 50 million. Another significant challenge is achieving true immersion and comfort in VR/AR applications. While microdisplays are becoming more advanced, issues such as motion sickness, field of view limitations, and the weight of headsets still need to be addressed through further integration with optics and system design. This requires a holistic approach beyond just the chip itself. Furthermore, power consumption remains a critical concern, especially for battery-powered wearable devices. While silicon-based technologies are generally power-efficient, pushing for higher brightness and resolution often comes with increased power demands, necessitating ongoing optimization and innovation in power management techniques. The development of energy-efficient display drivers and backplanes is crucial. Competition from emerging display technologies, such as micro-LEDs, poses a potential threat. While silicon-based microdisplays currently dominate many segments, micro-LEDs offer advantages in terms of brightness, contrast, and pixel density, and their increasing maturity could lead to market share erosion in certain applications. The scalability of production for ultra-high-resolution displays can also be a bottleneck, particularly for demanding professional applications requiring extremely fine pixel pitches and minimal uniformity variations. Finally, standardization across different application segments and device manufacturers can be slow, leading to fragmentation and potential interoperability issues, which can hinder widespread adoption and market growth.

The silicon-based microdisplay chips market is poised for dominance by specific regions and segments, driven by concentrated innovation, strong end-user demand, and supportive industrial ecosystems.

Dominating Regions/Countries:

Dominating Segments:

The interplay of these regional strengths and segment demands will shape the future landscape of the silicon-based microdisplay chips market, with the Asia Pacific region's manufacturing prowess and the VR/AR and OLED segments' rapid advancement at its core.

The silicon-based microdisplay chips industry is propelled by several key growth catalysts. The relentless advancement in semiconductor technology, enabling higher resolutions and greater pixel densities, is a fundamental driver. Furthermore, the expanding adoption of Virtual Reality (VR) and Augmented Reality (AR) devices across consumer and enterprise sectors is creating unprecedented demand. The increasing use of wearable technology, from smart glasses to heads-up displays, also contributes significantly. Finally, ongoing innovation in optical design and integration with advanced optics is unlocking new application possibilities and enhancing user experiences, further fueling market expansion.

This comprehensive report offers an exhaustive examination of the silicon-based microdisplay chips market, encompassing market dynamics, technological advancements, and future projections. It delves into the intricate details of market segmentation by application and type, providing granular insights into the performance of VR/AR, micro-projectors, wearable devices, medical devices, and other niche applications. Similarly, the analysis of LCoS, OLED, and DLP technologies sheds light on their respective market positions and growth potentials. The report critically assesses the driving forces, such as the burgeoning VR/AR sector and the increasing adoption of wearable devices, which are injecting significant momentum into the market. Simultaneously, it highlights the prevailing challenges and restraints, including high manufacturing costs and the need for further technological refinement, which could impact market expansion. Through extensive research and analysis, this report provides stakeholders with the essential intelligence to navigate this dynamic industry, understand its future trajectory, and capitalize on emerging opportunities within the global silicon-based microdisplay chips landscape.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 12.1% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12.1%.

Key companies in the market include Sony Semiconductor Solutions, Himax Technologies, Texas Instruments (TI), Kopin, eMagin, OmniVision, HOLOEYE Photonics, Microoled, AUO, Visionox, BOE Technology, Hongshi Intelligence Tech, VIEWTRIX Technology, Nanjing SmartVision Electronics.

The market segments include Application, Type.

The market size is estimated to be USD 1303 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Silicon-Based Microdisplay Chips," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Silicon-Based Microdisplay Chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.