1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicon-28?

The projected CAGR is approximately 10.9%.

Silicon-28

Silicon-28Silicon-28 by Purity (Purity: 3N, Purity: 4N, Purity: >4N), by Application (Quantum Computing, Semiconductor Research & Development, Advanced Semiconductor Manufacturing, Metrology & Standards, Photonics & Silicon Photonics, Photovoltaic Cells, Others), by Distribution Channel (Direct Sales, Distributors and Wholesalers), by End User (Quantum Computing Companies, Semiconductor Manufacturers, Research Institutes & Universities, National Laboratories, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

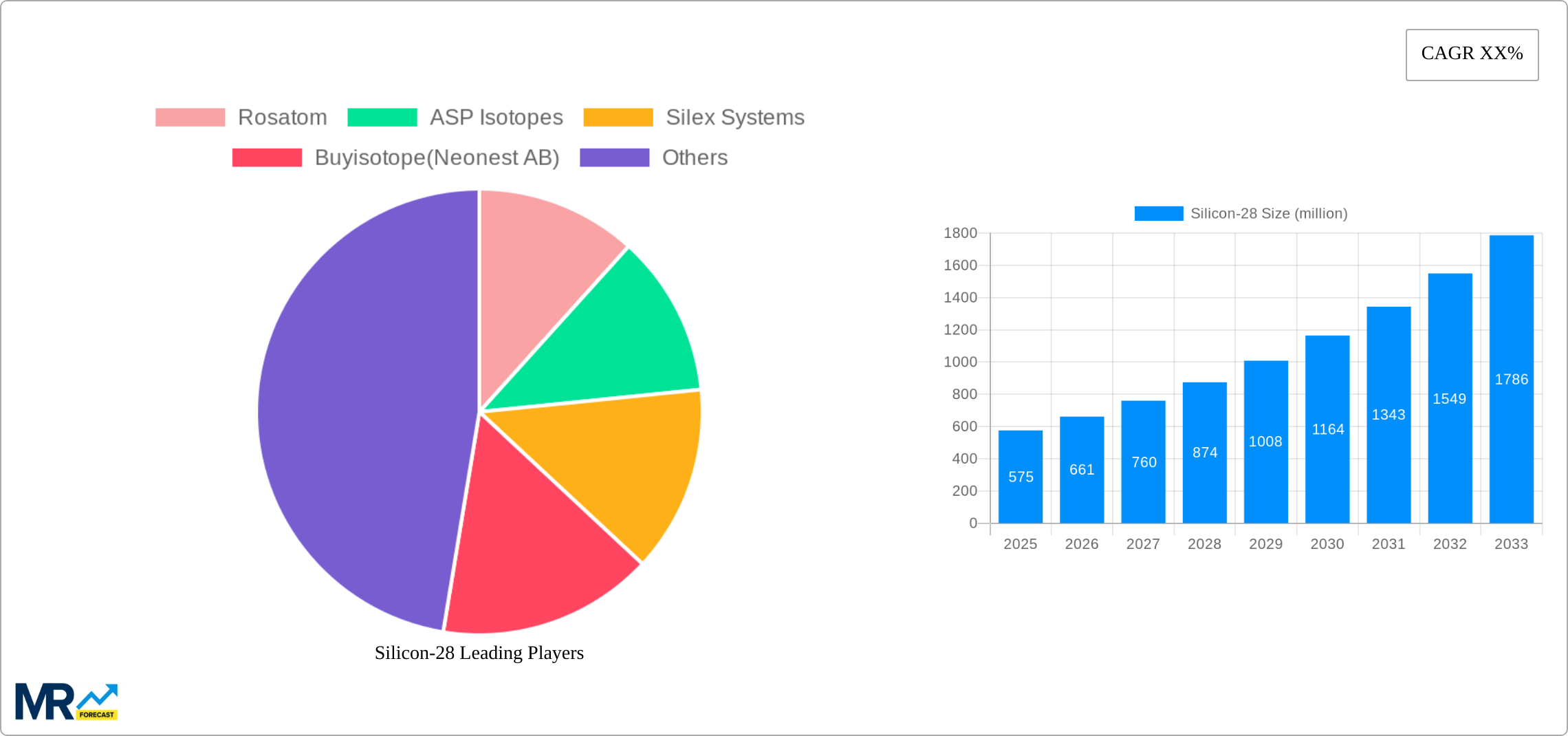

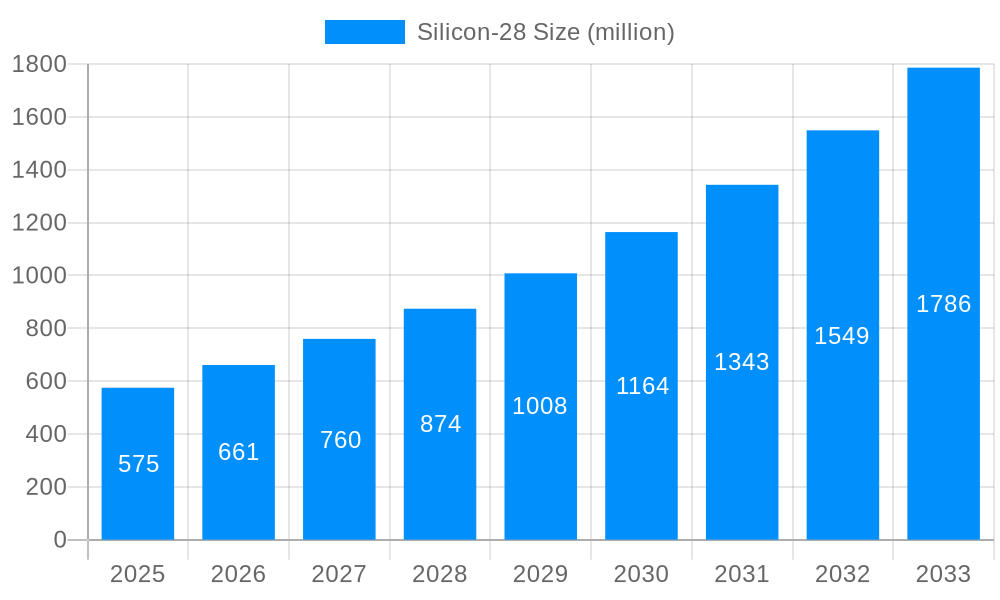

The Global Silicon-28 Market is poised for substantial expansion, with its valuation projected to reach significant figures by the end of the forecast period, commencing from 2025 to 2033. As of 2024, the market's estimated size stands at $76.97 million. This growth trajectory is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 10.9%, reflecting an accelerating demand for isotopically enriched silicon in critical high-technology applications. The primary impetus stems from the burgeoning requirements within quantum computing, advanced semiconductor manufacturing, and precision metrology, areas where the unique isotopic purity of Silicon-28 is indispensable.

The demand for Silicon-28 is intrinsically linked to advancements in quantum information science. As research and development intensify globally, the imperative for spin-qubit architectures utilizing highly purified silicon substrates becomes more pronounced, directly fueling the expansion of the Silicon-28 Market. Concurrently, the evolving landscape of advanced semiconductor manufacturing demands materials with unprecedented purity to mitigate defects and enhance device performance at sub-nanometer scales. The High-Purity Silicon Market, while broader, increasingly seeks isotopically enriched variants to meet these exacting specifications. Furthermore, the precise atomic weight and crystalline perfection offered by Silicon-28 are critical for establishing fundamental physical constants and developing next-generation metrological standards, including the redefinition of the kilogram, thus creating a niche yet high-value segment.

Macroeconomic tailwinds include sustained global investments in R&D infrastructure for future technologies, national initiatives in quantum supremacy, and growing strategic importance of domestic semiconductor supply chains. The Isotope Separation Market is a crucial upstream contributor, with technological advancements in enrichment processes directly influencing the availability and cost of Silicon-28. Innovations in techniques like laser isotope separation and gas centrifugation are key to scaling production efficiently. The overall outlook for the Silicon-28 Market is exceptionally positive, driven by its foundational role in enabling breakthroughs across multiple scientific and industrial frontiers, positioning it as a cornerstone within the broader Advanced Materials Market and Specialty Chemicals Market ecosystems. Its specialized applications ensure a premium valuation and sustained growth, despite the inherent complexities and costs associated with its production and purification. The indispensable nature of Silicon-28 for future technological paradigms cements its long-term growth prospects.

The Purity segment stands as the most critical and revenue-defining component within the Silicon-28 Market, driving value based on the degree of isotopic enrichment. While the data delineates purity levels into Purity: 3N, Purity: 4N, and Purity: >4N, it is the highest purity segment, specifically Purity: >4N (e.g., 99.99% or higher isotopic enrichment), that commands the largest revenue share and dictates the technological frontier. This segment's dominance is directly attributable to its indispensability in the most demanding applications, particularly in quantum computing and advanced semiconductor research. For instance, the coherence times of silicon spin qubits, a fundamental metric for quantum computer performance, are significantly extended in substrates with extremely low concentrations of non-zero nuclear spin isotopes, primarily Silicon-29. Achieving Purity: >4N for Silicon-28 minimizes quantum decoherence, enabling robust qubit operation and contributing substantially to the Quantum Computing Market.

The rationale for this segment's dominance lies in the direct correlation between isotopic purity and performance metrics in next-generation devices. In Advanced Semiconductor Manufacturing Market applications, while traditional silicon wafers suffice for many processes, specialized nodes requiring atomic-scale precision for features or doping profiles can benefit from isotopically pure substrates to reduce scattering centers and enhance carrier mobility. Although the primary drivers for 4N silicon purity (99.99%) or higher are currently niche, they represent the highest value-per-unit sales. For metrology and standards applications, such as the redefinition of the kilogram through Avogadro's constant, Silicon-28 crystals of extraordinary purity (99.999% and beyond) are absolutely essential for realizing atomic-scale precision.

Key players in this specialized segment, such as Orano Group, ASP Isotopes, and Urenco, are at the forefront of developing and refining isotope separation technologies, which are capital-intensive and require advanced expertise. Silex Systems, for example, is innovating with laser-based enrichment techniques to achieve these ultra-high purities more efficiently. American Elements also supplies various purity grades, catering to both research and initial commercial deployment. The market share within the Purity: >4N segment is highly consolidated, given the technical barriers to entry and the specialized infrastructure required for isotopic enrichment. These companies are not merely suppliers but strategic partners to research institutions and advanced technology developers. The trend indicates a sustained increase in demand for higher purity grades as quantum technologies mature and advanced semiconductor design continues to push material limits, further solidifying the Purity: >4N segment's preeminence within the Silicon-28 Market. The need for precise material specifications in the Silicon Photonics Market also emphasizes the importance of consistent, high-purity silicon substrates, although typically not to the isotopic purity levels required for quantum computing.

The Silicon-28 Market's growth is predominantly propelled by several high-impact strategic drivers, concurrently navigating inherent market constraints. A primary driver is the accelerating development in the Quantum Computing Market. Quantum coherence, crucial for stable qubit operation, is significantly enhanced in isotopically pure Silicon-28 substrates by minimizing nuclear spin-induced decoherence. Global investments in quantum technologies, estimated to exceed $30 billion by 2030 across public and private sectors, directly translate into increased demand for high-purity Silicon-28. Major research initiatives and commercial ventures are actively seeking reliable sources of this material to advance their quantum hardware roadmaps.

Another significant driver is the continuous innovation in the Advanced Semiconductor Manufacturing Market. While not as universally pervasive as in quantum computing, specialized applications within advanced logic, memory, and high-frequency devices are exploring the benefits of isotopically enriched silicon to improve device performance, reduce defect rates, and enhance thermal conductivity. The pursuit of smaller feature sizes and more complex 3D architectures necessitates materials with predictable atomic properties, creating a growing niche for Silicon-28. The increasing sophistication of Semiconductor Manufacturing Equipment Market further enables the integration and processing of such advanced materials.

Conversely, the Silicon-28 Market faces substantial constraints, primarily centered on production cost and limited supply infrastructure. The process of isotope separation is exceptionally complex and energy-intensive, requiring specialized technologies such as gas centrifuges or laser isotope separation (LIS). This results in a high manufacturing cost per unit, which restricts broader adoption to only the most value-added applications. Current global production capacity for high-purity Silicon-28 remains relatively limited, with only a handful of entities possessing the requisite expertise and facilities. This limited supply, coupled with geopolitical considerations for critical materials, creates supply chain vulnerabilities and potentially volatile pricing. Furthermore, the specialized knowledge and substantial capital expenditure required for developing and operating isotope enrichment facilities act as significant barriers to entry for new market participants, leading to a highly concentrated supply side. These constraints, while challenging, also underpin the premium pricing and strategic value of the Silicon-28 Market.

The competitive landscape of the Silicon-28 Market is characterized by a specialized group of players focused on high-purity material production and isotope enrichment services. These entities often leverage proprietary technologies to achieve the stringent isotopic purity levels required by advanced applications.

The Silicon-28 Market has been subject to several strategic advancements and milestones, reflecting its critical role in emerging technologies. These developments typically involve technological breakthroughs in enrichment, strategic collaborations, and increased investment in associated end-use applications.

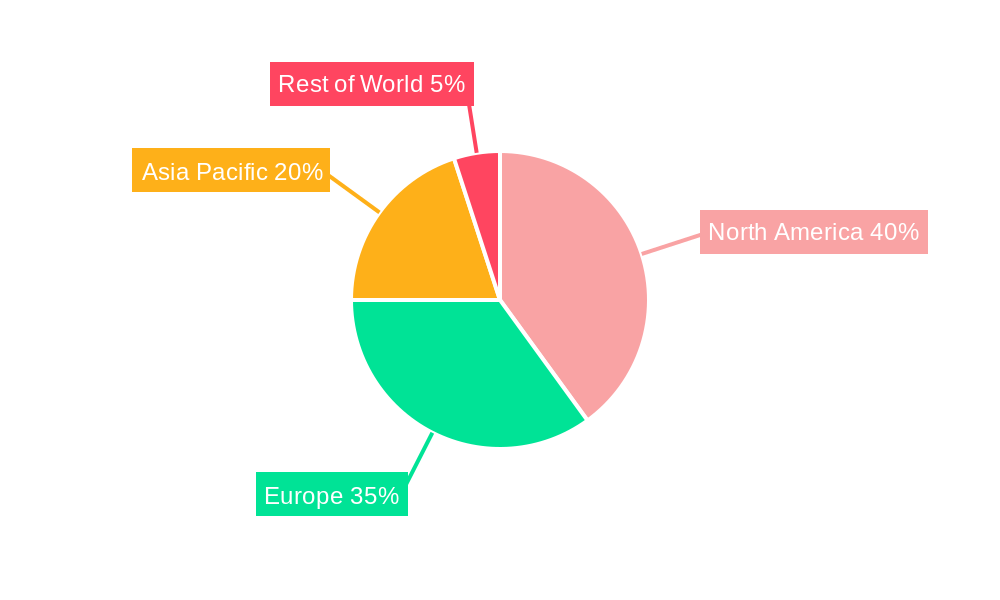

The Silicon-28 Market exhibits distinct regional dynamics driven by varying levels of research funding, semiconductor manufacturing capabilities, and quantum technology initiatives. Globally, North America and Europe currently represent the largest revenue shares due to their advanced R&D infrastructure and significant investments in quantum computing and precision metrology.

North America holds a substantial share of the Silicon-28 Market, projected to maintain a strong CAGR driven primarily by robust governmental funding for quantum information science and a high concentration of leading research universities and technology companies. The United States, in particular, is a hub for Quantum Computing Market development, demanding high-purity Silicon-28 for qubit fabrication. Canada also contributes significantly, especially in materials science research. The presence of numerous national laboratories and defense-related research further solidifies this region's leadership.

Europe commands another significant portion of the market, with countries like the UK, Germany, and France investing heavily in quantum technologies and advanced physics research. This region is a leader in metrology standards, where Silicon-28 is crucial for atomic weight determination and fundamental constant research. The European Union's Horizon Europe program, with its substantial funding for advanced materials and quantum technologies, acts as a primary demand driver. The regional CAGR is expected to be competitive, fueled by a collaborative research environment.

Asia Pacific is anticipated to be the fastest-growing region in the Silicon-28 Market, albeit from a smaller base. This growth is predominantly driven by massive investments in semiconductor manufacturing (especially in China, South Korea, and Taiwan) and emerging quantum computing initiatives in Japan and India. While the primary demand for Silicon-28 in Asia Pacific is currently skewed towards Advanced Semiconductor Manufacturing Market research and high-end Photovoltaic Cells Market applications, the burgeoning quantum computing sector promises significant future acceleration. China's ambitious long-term plans in quantum technologies position it as a critical growth engine.

Middle East & Africa and South America currently hold smaller shares of the Silicon-28 Market. Demand in these regions is primarily limited to academic research and nascent industrial applications, with growth contingent on developing indigenous advanced technology sectors and increasing collaboration with global research hubs. While the absolute market size here is comparatively modest, specific government-backed initiatives in scientific research could spur future localized demand.

The Silicon-28 Market's future is intrinsically linked to advancements in material science and quantum engineering, with several disruptive technologies shaping its trajectory. The first key innovation area is Advanced Isotope Separation Techniques. Traditional methods like gas centrifugation are highly energy-intensive and costly. Emerging techniques, particularly laser isotope separation (LIS) technologies, such as those pioneered by Silex Systems, promise significantly lower production costs and higher throughput. These innovations could drastically improve the supply elasticity of Silicon-28, making it more accessible for broader commercial applications beyond niche research. Adoption timelines for next-generation LIS facilities are projected within the next 5-7 years, with R&D investments remaining high as governments and private entities seek to secure domestic supply chains for critical quantum materials. This threatens incumbent business models heavily reliant on established, often less efficient, separation processes.

The second critical innovation involves Novel Crystal Growth and Wafer Fabrication Methods. Producing large, defect-free single crystals of isotopically pure Silicon-28 is a significant technical challenge. Researchers are exploring advanced Czochralski and Float-Zone growth techniques adapted for enriched silicon melts, aiming to minimize impurities and crystal defects that can degrade device performance. Furthermore, innovations in wafering and surface preparation for these delicate materials are crucial. These advancements are vital for transitioning Silicon-28 from laboratory samples to industrial-scale substrates for the Advanced Semiconductor Manufacturing Market and Silicon Photonics Market. R&D in this area is heavily funded by semiconductor giants and national research institutes, with adoption expected within 3-5 years for specialized applications. These innovations reinforce incumbent material suppliers who can adapt but present a barrier to those with less advanced processing capabilities.

A third disruptive area is the Integration of Silicon-28 with Quantum Information Science Architectures. Beyond basic spin qubits, Silicon-28 is being explored as a platform for hybrid quantum systems, including integration with superconducting qubits, topological qubits, or even quantum dots within advanced Photovoltaic Cells Market structures. Innovations here focus on achieving robust quantum entanglement and error correction within a silicon-based framework, pushing the boundaries of material requirements. The High-Purity Silicon Market will increasingly cater to these demands. Adoption timelines are longer, perhaps 7-10 years, as these are still foundational research areas. R&D investments are concentrated in government-funded programs and venture-backed quantum startups, profoundly reinforcing the high-value niche of Silicon-28 while potentially disrupting traditional silicon manufacturing paradigms.

The Silicon-28 Market, while niche, has seen targeted investment and funding activity, largely driven by its indispensable role in the rapidly advancing fields of quantum computing and high-end semiconductor research. Over the past 2-3 years, capital flows have predominantly focused on upstream enrichment technologies and downstream application development.

Venture Capital and Strategic Investments: There has been a notable surge in venture funding for startups operating in the Quantum Computing Market, many of which explicitly highlight their reliance on isotopically pure silicon. For instance, companies developing silicon spin qubit architectures have attracted substantial Series A and B funding rounds, collectively totaling hundreds of millions of dollars globally. These investments indirectly fuel the Silicon-28 Market by creating a guaranteed future demand for the material. Furthermore, strategic investments have been made into companies specializing in Isotope Separation Market technologies, particularly those pursuing laser-based enrichment methods. These investments are aimed at de-risking supply chains and potentially reducing the cost of high-purity Silicon-28.

Government Funding and Research Grants: National governments, recognizing the strategic importance of quantum technologies, have allocated significant funds to research institutes and universities. Programs like the U.S. National Quantum Initiative, the European Quantum Flagship, and similar initiatives in China and Japan, include substantial grants for materials science research specifically targeting enriched silicon substrates. These grants, often multi-year and multi-million dollar commitments, ensure sustained R&D activity and demand for Silicon-28 for foundational research.

Mergers & Acquisitions (M&A): While large-scale M&A activity directly involving pure-play Silicon-28 producers has been limited due to the market's specialized nature and consolidated supplier base, there have been strategic acquisitions or partnerships by larger Advanced Materials Market and Specialty Chemicals Market firms into companies with advanced isotope handling or purification capabilities. These moves are typically aimed at vertical integration or diversifying product portfolios to capture emerging high-value markets. For example, a major industrial gas company might acquire a small firm with expertise in cryogenic isotope separation.

Sub-Segments Attracting Capital: The most capital-intensive sub-segments are those directly involved in quantum computing hardware development and advanced metrology standards. Investments here are driven by the extremely high purity requirements and the potential for groundbreaking technological leaps. There is also increasing interest in funding research for Silicon Photonics Market applications where high-purity silicon can offer performance advantages, particularly in optical loss reduction. The overarching theme is securing access to and improving the cost-effectiveness of this critical advanced material for future technological leadership.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 10.9%.

Key companies in the market include Orano Group, ASP Isotopes, American Elements, Silex Systems, Urenco, Others.

The market segments include Purity, Application, Distribution Channel, End User.

The market size is estimated to be USD 76.97 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Silicon-28," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Silicon-28, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.