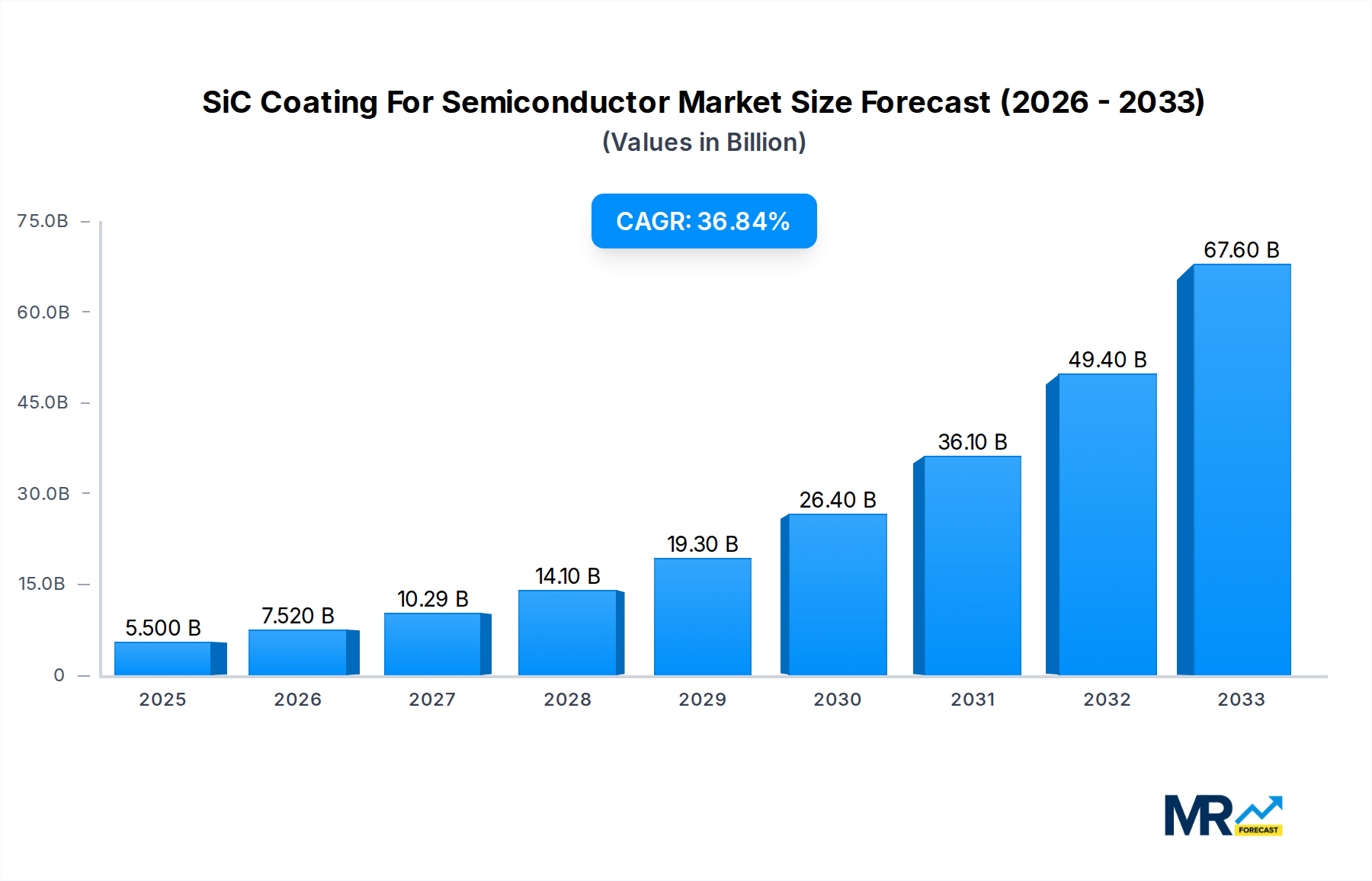

1. What is the projected Compound Annual Growth Rate (CAGR) of the SiC Coating For Semiconductor?

The projected CAGR is approximately 34.6%.

SiC Coating For Semiconductor

SiC Coating For SemiconductorSiC Coating For Semiconductor by Type (CVD & PVD, Thermal Spray, World SiC Coating For Semiconductor Production ), by Application (Rapid Thermal Process Components, Plasma Etch Components, Susceptors and Dummy Wafer, LED Wafer Carriers & Cover Plates, Others, World SiC Coating For Semiconductor Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The SiC coating for semiconductor market is experiencing robust growth, driven by the increasing demand for high-power, high-frequency, and high-temperature electronic devices. The semiconductor industry's continuous pursuit of miniaturization and enhanced performance necessitates advanced materials like silicon carbide (SiC), which offers superior electrical and thermal properties compared to traditional silicon. SiC coatings further enhance these properties, providing protection against oxidation, corrosion, and contamination, thus extending the lifespan and improving the reliability of semiconductor components. This market is segmented by coating type (e.g., CVD, PVD), application (power electronics, RF devices, sensors), and region. The leading players are strategically investing in R&D to develop innovative SiC coating technologies and expand their manufacturing capabilities to meet the growing market demand. A conservative estimate suggests a market size of approximately $1.5 billion in 2025, projecting a Compound Annual Growth Rate (CAGR) of 15% from 2025 to 2033, driven by the proliferation of electric vehicles, renewable energy infrastructure, and 5G communication technologies. This growth is further fueled by government initiatives promoting the adoption of energy-efficient technologies and advancements in semiconductor manufacturing processes.

The competitive landscape is characterized by both established players and emerging companies. Key players are focusing on strategic collaborations and acquisitions to broaden their product portfolios and strengthen their market presence. While the market faces challenges such as the high cost of SiC substrates and the complexity of the coating process, these are being mitigated through ongoing technological advancements and economies of scale. The geographic distribution of the market is expected to remain relatively balanced across North America, Europe, and Asia-Pacific, with Asia-Pacific experiencing faster growth due to significant investments in semiconductor manufacturing and the burgeoning electronics industry. Future growth hinges on continuing innovations in SiC coating techniques, which will improve efficiency, reduce costs, and broaden the applications of SiC-based semiconductors.

The SiC coating for semiconductor market is experiencing robust growth, driven by the increasing demand for high-power, high-frequency, and high-temperature applications in the electronics industry. The global market size, estimated at USD XX million in 2025, is projected to reach USD YY million by 2033, exhibiting a remarkable CAGR of Z%. This significant expansion reflects the critical role SiC coatings play in enhancing the performance and reliability of semiconductor devices. The historical period (2019-2024) witnessed steady growth, laying a strong foundation for the anticipated surge in the forecast period (2025-2033). Key market insights reveal a strong preference for advanced coating techniques that offer superior adhesion, uniformity, and thermal stability. The demand for SiC coatings is particularly high in power electronics, where the need for efficient energy conversion and reduced power losses is paramount. Furthermore, the automotive and renewable energy sectors are major contributors to this market expansion, fuelled by the electrification of vehicles and the widespread adoption of solar and wind power technologies. The increasing adoption of 5G networks and the growth of data centers also contribute significantly to the rising demand for advanced semiconductor devices that leverage SiC coatings for improved performance. This trend is expected to continue, with ongoing research and development efforts focused on improving the quality, efficiency, and cost-effectiveness of SiC coating processes. The market is characterized by intense competition among leading players, each striving to enhance their product offerings and expand their market share through strategic partnerships, acquisitions, and technological advancements.

Several key factors are propelling the growth of the SiC coating for semiconductor market. The rising demand for energy-efficient power electronics is a primary driver, as SiC-coated semiconductors offer superior performance compared to traditional silicon-based devices. These coatings significantly improve the efficiency of power conversion, leading to reduced energy consumption and lower operating costs – highly desirable in applications like electric vehicles and renewable energy systems. The increasing adoption of high-frequency applications, such as 5G wireless communication and high-speed data transmission, further necessitates the use of SiC coatings, as they enable the operation of devices at higher frequencies without significant power losses. Moreover, advancements in SiC coating technologies, leading to improved coating quality, durability, and cost-effectiveness, are accelerating market adoption. The ongoing miniaturization of semiconductor devices also plays a significant role, as SiC coatings are essential for protecting these delicate components from damage and ensuring reliable performance. Finally, stringent government regulations aimed at reducing carbon emissions and promoting energy efficiency are indirectly driving the demand for SiC-coated semiconductors, as they offer a pathway toward more sustainable and environmentally friendly technologies.

Despite the strong growth prospects, the SiC coating for semiconductor market faces certain challenges. The high cost of SiC substrates and the complexity of the coating processes can make the overall production cost significantly higher compared to traditional silicon-based devices. This can hinder wider adoption, especially in price-sensitive applications. The development of robust and reliable coating techniques that ensure high adhesion, uniformity, and long-term stability remains a significant technical challenge. Any imperfections in the coating can lead to device failure, demanding stringent quality control measures throughout the manufacturing process. Furthermore, the availability of skilled workforce possessing expertise in SiC coating techniques presents a bottleneck. This skill gap necessitates substantial investments in training and development programs to ensure a sufficient supply of qualified personnel. Finally, the limited scalability of current SiC coating processes poses a challenge to meet the increasing global demand. Addressing these challenges requires concerted efforts from manufacturers, research institutions, and government agencies to foster technological innovation, improve process efficiency, and reduce production costs.

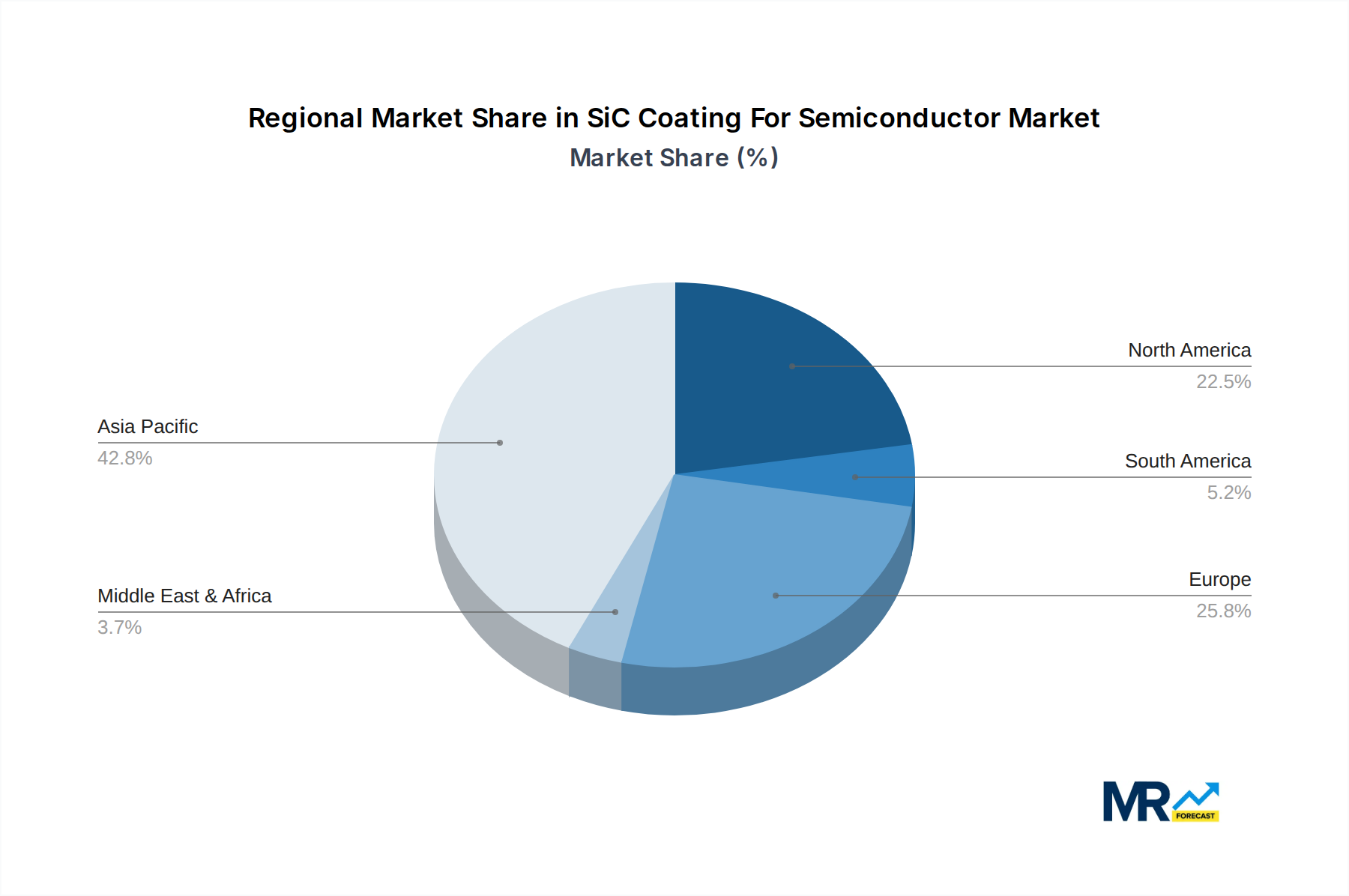

North America: This region is expected to maintain a leading position due to its strong semiconductor industry, substantial investments in research and development, and early adoption of advanced technologies. The presence of major semiconductor manufacturers and a supportive regulatory environment further contribute to market dominance.

Asia-Pacific: Rapid industrialization and significant growth in the electronics sector are driving significant demand for SiC coatings in this region. China, Japan, South Korea, and Taiwan are expected to witness robust growth, fueled by substantial investments in renewable energy, electric vehicles, and advanced electronics manufacturing.

Europe: Europe is projected to show steady growth, driven by increasing adoption of SiC-based power electronics in automotive and industrial applications. Government initiatives focused on promoting energy efficiency and reducing carbon emissions also contribute to market expansion.

Segments: The power electronics segment is projected to dominate due to the high demand for energy-efficient power conversion solutions in electric vehicles, renewable energy systems, and industrial automation. Furthermore, the increasing adoption of 5G and data centers will further stimulate growth within this segment.

In summary, while North America maintains a strong foothold due to its established technology and industry base, the Asia-Pacific region's rapid growth in electronics manufacturing and renewable energy deployment is positioning it for significant market share gains in the coming years. The power electronics segment's sustained demand, underpinned by global trends in energy efficiency and technological advancements, ensures its continued dominance across all regions.

The SiC coating for semiconductor industry is experiencing significant growth driven by several converging factors. The increasing demand for high-power, high-frequency devices in electric vehicles, renewable energy systems, and 5G infrastructure necessitates the superior performance offered by SiC-coated semiconductors. Further advancements in coating techniques are continuously improving efficiency, reliability, and cost-effectiveness, making SiC coatings increasingly attractive for wider adoption. Stringent government regulations promoting energy efficiency and sustainability also propel market expansion by incentivizing the use of energy-efficient technologies like SiC-coated semiconductors. This confluence of factors creates a highly favorable environment for substantial growth in the coming years.

This comprehensive report offers a detailed analysis of the SiC coating for semiconductor market, encompassing market size estimations, growth forecasts, key market trends, driving factors, challenges, competitive landscape, and significant industry developments. It provides valuable insights for industry stakeholders, including manufacturers, suppliers, investors, and researchers, enabling informed decision-making and strategic planning in this rapidly evolving market. The report's in-depth analysis of regional markets and key segments offers a granular understanding of market dynamics, helping to identify potential opportunities and assess market risks. Furthermore, the report highlights the key players and their strategies, providing a comprehensive overview of the competitive landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 34.6% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 34.6%.

Key companies in the market include Tokai Carbon, SGL Group, Morgan Advanced Materials, Ferrotec, CoorsTek, AGC, SKC Solmics, Mersen, Toyo Tanso, NTST, MINTEQ International, Heraeus, Bay Carbon, ACME, Xycarb, Ningbo VET Energy Technology, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "SiC Coating For Semiconductor," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the SiC Coating For Semiconductor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.