1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Metrology Instrument?

The projected CAGR is approximately 6%.

Semiconductor Metrology Instrument

Semiconductor Metrology InstrumentSemiconductor Metrology Instrument by Type (Autoloading, Manual Loading, World Semiconductor Metrology Instrument Production ), by Application (Material, Metallurgy, Biology, Medicine, Semiconductor, Others, World Semiconductor Metrology Instrument Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The semiconductor industry's relentless pursuit of miniaturization and enhanced performance fuels significant growth in the semiconductor metrology instrument market. Driven by the increasing complexity of semiconductor fabrication processes and the demand for higher accuracy in chip manufacturing, this market is projected to experience robust expansion. The 6% CAGR suggests a steady, consistent growth trajectory, indicating a healthy demand for advanced metrology tools across diverse semiconductor applications. Major drivers include the rising adoption of advanced node technologies (e.g., 5nm and 3nm), the increasing need for real-time process control and quality assurance, and the growing demand for high-volume manufacturing. Key trends shaping the market include the development of innovative measurement techniques, such as atomic force microscopy and optical metrology, and the integration of artificial intelligence and machine learning for enhanced data analysis and process optimization. While challenges exist, such as high equipment costs and the complexity of integrating new technologies into existing manufacturing lines, the overall market outlook remains positive, fueled by continuous technological advancements and the ever-increasing demand for sophisticated semiconductor devices in various industries.

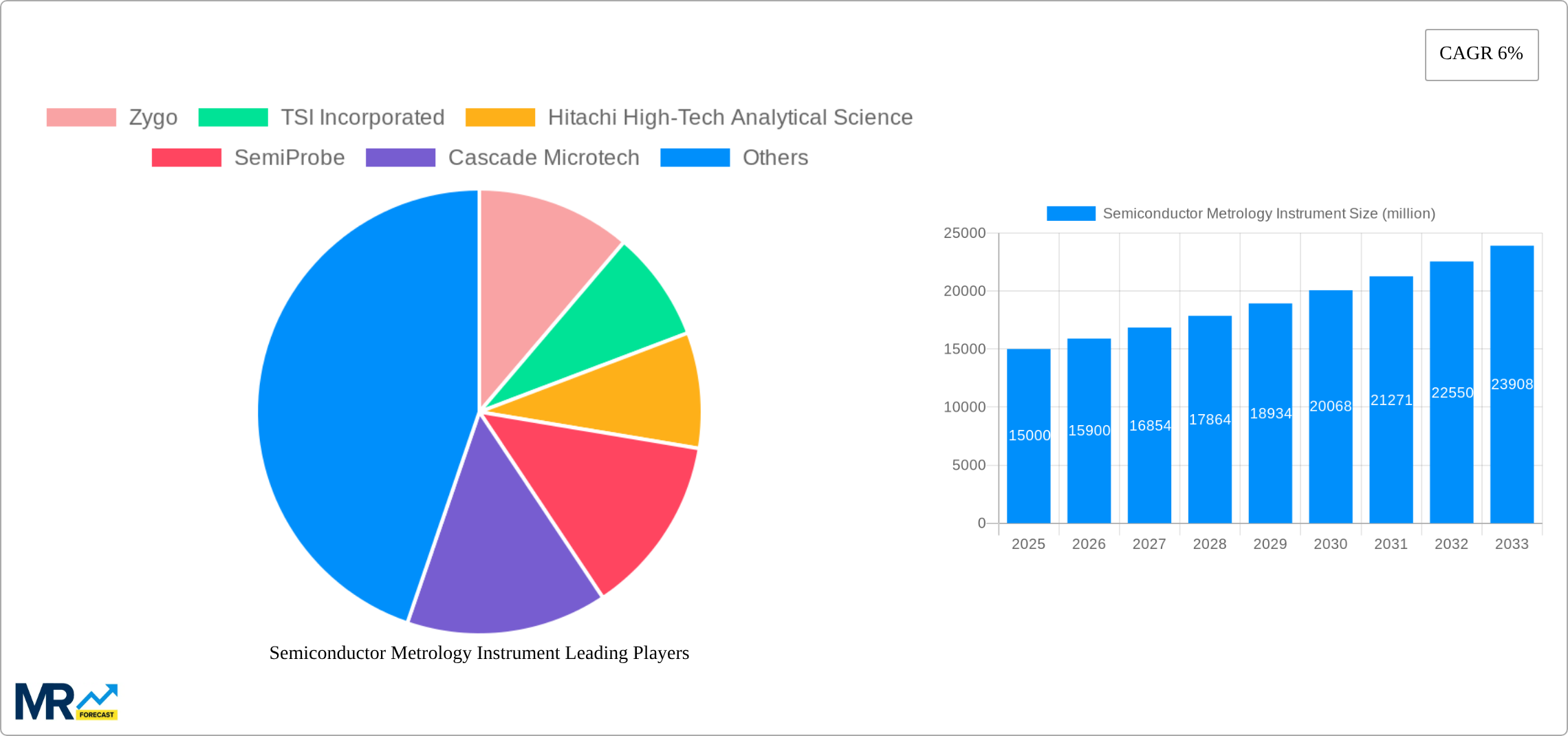

The competitive landscape is marked by a diverse range of players, including established industry giants like Bruker, Nikon Metrology, and Keyence, alongside specialized companies like Zygo and KLA (implied by the presence of competitors in similar spaces). These companies are actively engaged in research and development, striving to provide cutting-edge solutions to meet the evolving needs of semiconductor manufacturers. The regional distribution likely mirrors the global semiconductor manufacturing hubs, with North America, Asia-Pacific (particularly Taiwan, South Korea, and China), and Europe holding substantial market shares. The forecast period of 2025-2033 indicates a promising future for the industry, with continued growth anticipated as the semiconductor sector expands across various applications, from consumer electronics and automotive to high-performance computing and artificial intelligence. Strategic partnerships, mergers, and acquisitions are anticipated to further shape the market dynamics in the coming years.

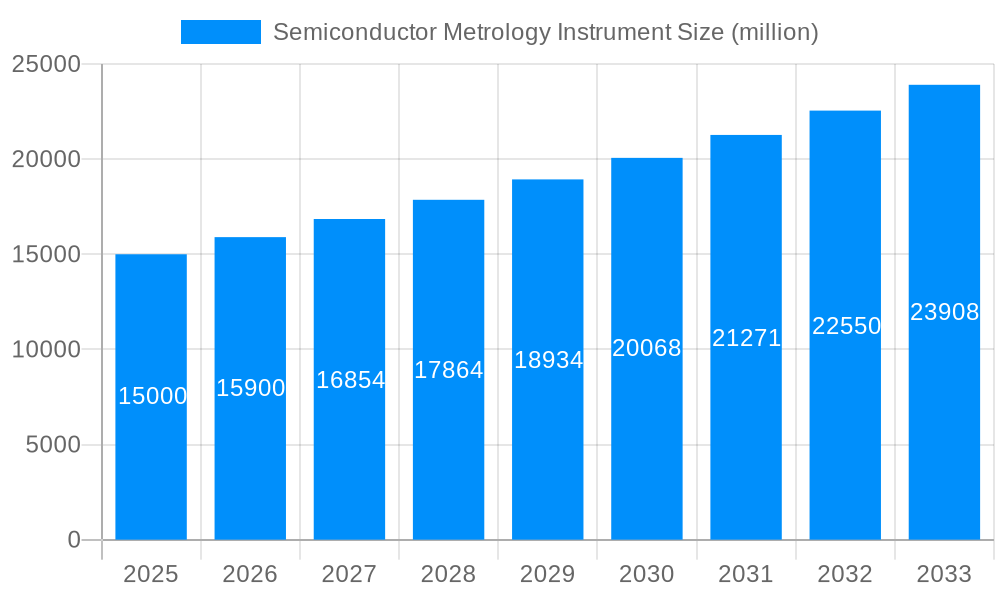

The global semiconductor metrology instrument market is experiencing robust growth, projected to reach several billion USD by 2033. The study period (2019-2033), with a base year of 2025 and a forecast period spanning 2025-2033, reveals a compelling upward trajectory. This expansion is fueled by the unrelenting demand for advanced semiconductor devices across diverse applications, including 5G infrastructure, high-performance computing (HPC), artificial intelligence (AI), and the Internet of Things (IoT). The increasing complexity of semiconductor manufacturing processes necessitates precise and highly sensitive metrology instruments to ensure quality control and yield optimization. Miniaturization trends in semiconductor technology, with features shrinking to the nanoscale, further amplify the need for advanced metrology solutions capable of accurate measurement and analysis at these incredibly fine levels. Consequently, the market is witnessing a surge in demand for advanced techniques like atomic force microscopy (AFM), optical metrology, and electron microscopy, driving innovation and pushing technological boundaries. The historical period (2019-2024) showcases a steady climb, providing a firm foundation for the projected exponential growth in the coming years. The estimated market value in 2025 represents a significant milestone, showcasing the industry’s maturity and potential for future expansion. This growth is further amplified by substantial investments from key players in research and development, focused on enhancing accuracy, speed, and automation in metrology processes. The ongoing trend toward automation and data analytics in semiconductor fabrication is also shaping the demand for instruments that seamlessly integrate into sophisticated manufacturing ecosystems. In short, the market is characterized by a dynamic interplay of technological advancements, increasing demand driven by the electronics industry, and a concerted effort by manufacturers to provide more efficient and precise measurement solutions.

Several factors are synergistically driving the growth of the semiconductor metrology instrument market. The relentless miniaturization of semiconductor devices is a primary driver, demanding increasingly sophisticated metrology tools capable of resolving features at the nanoscale. The need for higher process yields and improved product quality in semiconductor manufacturing necessitates precise and reliable measurement techniques. The rise of advanced semiconductor nodes, requiring extremely accurate process control, is another significant factor. Furthermore, the expanding applications of semiconductors across various industries, such as automotive, healthcare, and consumer electronics, fuel demand for high-volume, high-quality production, further driving the adoption of advanced metrology instruments. Stringent quality control standards and regulations in the semiconductor industry necessitate the use of precise and reliable metrology equipment. Government initiatives and funding for research and development in advanced semiconductor technologies also contribute to market growth. Additionally, the increasing adoption of automation and data analytics in semiconductor manufacturing facilities is driving the demand for integrated metrology solutions that seamlessly integrate into existing workflows. Finally, ongoing technological innovations in metrology techniques and instrument design are creating more advanced and efficient solutions, thus propelling market expansion.

Despite its robust growth trajectory, the semiconductor metrology instrument market faces several challenges. The high cost of advanced metrology instruments can be a significant barrier to entry for smaller companies and research institutions. The complexity of operating and maintaining these instruments also presents a challenge, requiring specialized training and expertise. The need for continuous calibration and maintenance to ensure accuracy and reliability adds to the operational costs. Furthermore, the rapid pace of technological advancements in the semiconductor industry necessitates frequent upgrades and replacements of metrology equipment, placing financial strain on companies. Competition among established players and the emergence of new technologies can lead to price pressure and reduced profit margins. The market is also subject to cyclical fluctuations in the semiconductor industry, potentially impacting demand for metrology instruments during periods of economic downturn. Finally, the integration of new metrology instruments into existing manufacturing processes can be complex and time-consuming, hindering rapid adoption. Overcoming these challenges requires strategic planning, investments in research and development, and effective partnerships across the semiconductor ecosystem.

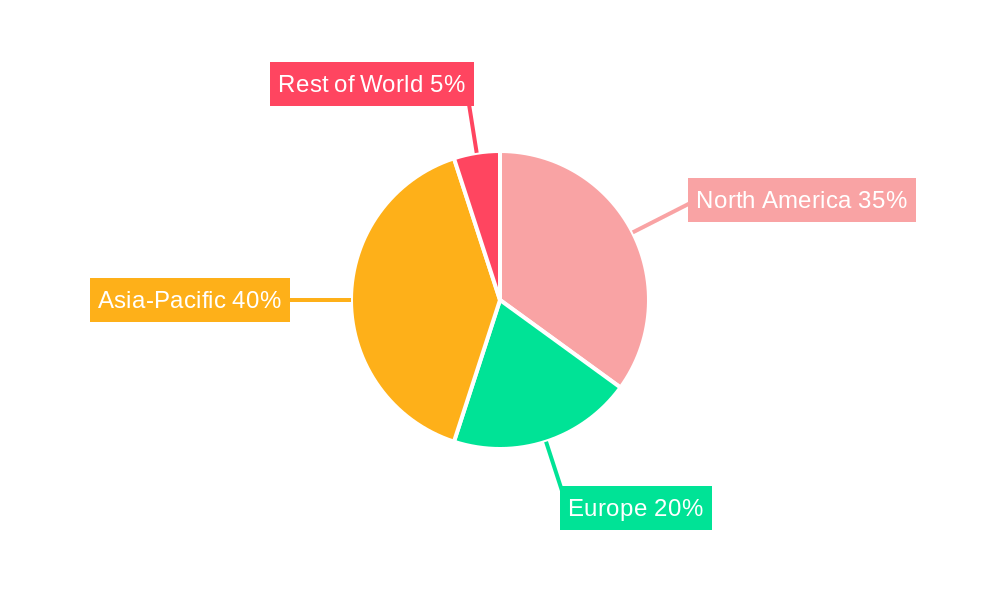

The semiconductor metrology instrument market is geographically diverse, but certain regions and segments exhibit stronger growth than others.

Asia-Pacific: This region is expected to dominate the market due to the concentration of major semiconductor manufacturers and a rapidly expanding electronics industry. Countries like China, South Korea, Taiwan, and Japan are significant contributors to this growth, driven by massive investments in semiconductor fabrication facilities and a continuous push for technological advancements. This region's significant contribution to global semiconductor production directly translates to high demand for advanced metrology solutions. The increasing adoption of advanced technologies, such as 5G and AI, within the Asia-Pacific region is accelerating this demand further.

North America: While holding a substantial market share, North America’s growth is projected to be relatively moderate compared to Asia-Pacific. However, the presence of major technology companies and strong R&D capabilities ensures a steady demand for high-end metrology instruments. The region remains a crucial hub for innovation and technology development within the semiconductor industry, particularly concerning cutting-edge metrology techniques and instrument design.

Europe: While possessing a sizable market presence, Europe's growth is relatively slower compared to other regions. However, it remains significant, driven by the presence of key semiconductor manufacturers and research institutions. The European market shows steady growth, although it lags behind the rapid expansion seen in Asia.

Dominant Segments:

Optical Metrology: This segment is poised for significant growth due to its high accuracy, non-destructive nature, and suitability for various applications in semiconductor manufacturing.

Electron Microscopy: This segment is also projected to experience strong growth, driven by the need for high-resolution imaging and analysis in advanced semiconductor manufacturing processes.

AFM (Atomic Force Microscopy): With its capacity for nanoscale analysis, AFM is seeing increasing demand, particularly for characterization at the atomic level.

In summary, while the Asia-Pacific region is forecast to lead in overall market size due to its high concentration of semiconductor manufacturing, the demand for advanced metrology solutions is prevalent across all regions, driven by continuous technological advancements and the need for higher-quality, high-yield production in the semiconductor industry. The specific segment dominating will fluctuate based on technological breakthroughs and the industry's immediate process control needs.

Several factors are catalyzing the growth of the semiconductor metrology instrument industry. The increasing demand for smaller, faster, and more energy-efficient semiconductor devices is driving the need for more precise and sophisticated metrology tools. Simultaneously, the rise of advanced semiconductor nodes necessitates higher accuracy and resolution in metrology instruments. The growing adoption of automation in semiconductor manufacturing plants enhances the integration of metrology systems into production lines, boosting efficiency and productivity. Furthermore, the need for faster and more efficient quality control processes is increasing the adoption of automated metrology solutions. Finally, government investments and initiatives promoting the advancement of semiconductor technology are fostering innovation and growth within the metrology sector.

This report provides a comprehensive analysis of the semiconductor metrology instrument market, covering market size, growth drivers, challenges, key players, and future trends. The detailed market segmentation, including by instrument type, application, and region, allows for a granular understanding of the market dynamics. The report also includes an in-depth analysis of the competitive landscape, highlighting the key strategies employed by leading players to maintain their market positions. Forecasts for the next decade offer valuable insights for investors, manufacturers, and other stakeholders involved in the semiconductor industry. The report’s robust methodology, leveraging both primary and secondary research, ensures reliable and relevant information for informed decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6%.

Key companies in the market include Zygo, TSI Incorporated, Hitachi High-Tech Analytical Science, SemiProbe, Cascade Microtech, KEYENCE, MicroSense, Technic, Xenemetrix, Advanced Energy Industries, Park Systems, Filmetrics, Phenom-World, Hiden Analytical, Rigaku, WDI Wise Device, StellarNet, Nikon Metrology, MTI Instruments, Nanotronics Imaging, Copper Mountain Technologies, Bruker, Beijing Saifan, Shanghai Yizhi, Shanghai Aiyao, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Semiconductor Metrology Instrument," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Metrology Instrument, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.