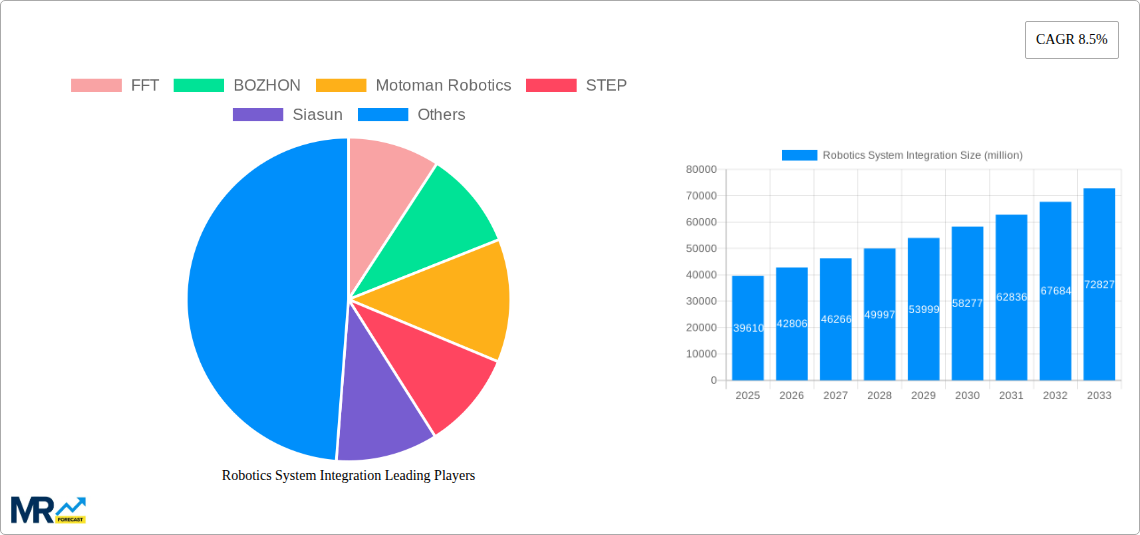

1. What is the projected Compound Annual Growth Rate (CAGR) of the Robotics System Integration?

The projected CAGR is approximately 8.5%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Robotics System Integration

Robotics System IntegrationRobotics System Integration by Type (Hardware, Software and Service), by Application (Automotive, Electrical & Electronics, Metal Industry, Chemical, Rubber and Plastic, Food, Beverages and Pharmaceuticals, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

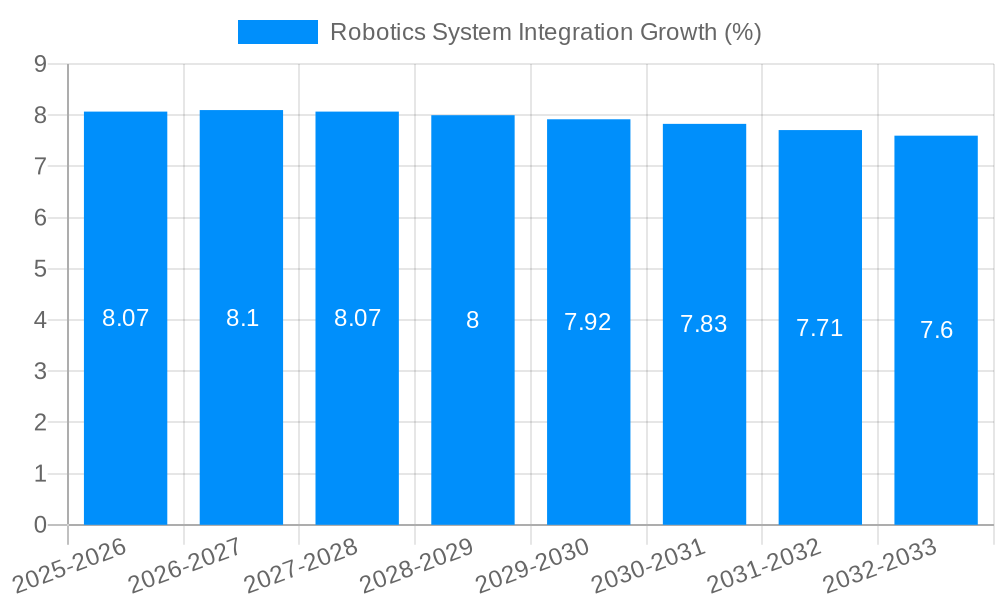

The global Robotics System Integration market is poised for significant expansion, projected to reach a substantial USD 39,610 million in value. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 8.5%, indicating a dynamic and expanding industry. A primary driver for this surge is the increasing adoption of automation across diverse manufacturing sectors, fueled by the need for enhanced productivity, precision, and cost-efficiency. Industries like automotive, electrical & electronics, and metal manufacturing are leading this charge, seeking sophisticated robotic solutions to streamline complex operations, improve worker safety, and maintain competitiveness in a rapidly evolving global landscape. The demand for tailored integration services that optimize robotic workflows, manage data effectively, and ensure seamless deployment is paramount, making system integrators indispensable partners for businesses looking to leverage advanced robotics.

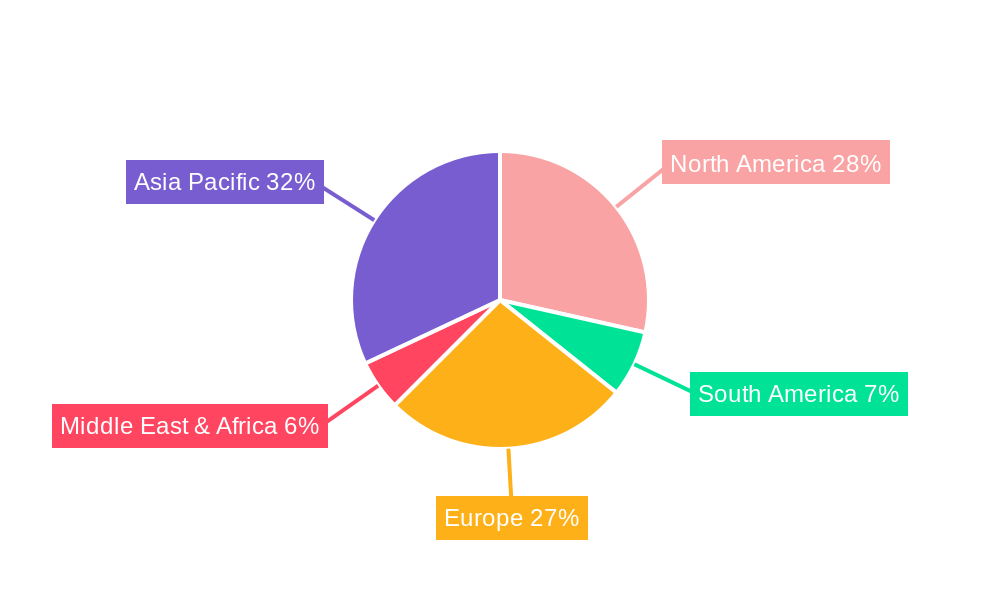

Further fueling this market trajectory is the growing emphasis on smart manufacturing and Industry 4.0 initiatives, which necessitate intelligent and interconnected robotic systems. Software and service segments are expected to witness substantial growth, complementing the hardware advancements. These segments are crucial for developing advanced algorithms, artificial intelligence-powered decision-making, and comprehensive support services that enable businesses to maximize their return on investment from robotic deployments. While the market benefits from widespread automation trends and technological innovation, potential restraints such as high initial investment costs and the need for skilled workforce development in robotics may present challenges. However, the overwhelming benefits in terms of operational efficiency, product quality, and competitive advantage are expected to outweigh these concerns, driving sustained market expansion across key geographical regions like Asia Pacific and North America.

The global Robotics System Integration market is poised for significant expansion, projected to reach a valuation exceeding $50,000 million by 2033. This growth is underpinned by a confluence of factors, including the increasing adoption of automation across diverse industries and the continuous evolution of robotic technologies. XXX, a leading market research firm, highlights that the market experienced a robust CAGR of approximately 15% during the historical period of 2019-2024, reaching an estimated $25,000 million in the base year of 2025. Looking ahead, the forecast period of 2025-2033 is anticipated to witness sustained momentum, driven by advancements in AI, machine learning, and the burgeoning demand for smart manufacturing solutions. The integration of collaborative robots (cobots) alongside traditional industrial robots is a prominent trend, enabling enhanced human-robot collaboration and offering greater flexibility in production lines. Furthermore, the increasing focus on Industry 5.0, emphasizing human-centric, sustainable, and resilient manufacturing, is expected to fuel the demand for sophisticated robotics system integration. The market's trajectory also indicates a growing preference for cloud-based integration platforms and modular robotic systems, allowing for quicker deployment and easier scalability. The report will delve into the intricate dynamics of this market, analyzing the interplay of hardware, software, and service components, and their impact on various industry applications. Insights into the emerging use cases in sectors beyond traditional manufacturing, such as logistics, healthcare, and agriculture, will also be a key focus. The increasing investment in research and development by key players, aimed at creating more intelligent, adaptive, and cost-effective robotic solutions, will further shape the market landscape. Ultimately, the Robotics System Integration market represents a dynamic and rapidly evolving sector with substantial growth potential, driven by the relentless pursuit of efficiency, productivity, and innovation across the global industrial spectrum. The report aims to provide a comprehensive understanding of these trends and their implications for stakeholders.

The robotics system integration market is experiencing a powerful surge driven by several fundamental forces. Foremost among these is the escalating imperative for enhanced operational efficiency and productivity across manufacturing and industrial sectors. Businesses are increasingly recognizing that sophisticated robotics integration is a critical pathway to streamlining processes, reducing cycle times, and minimizing errors, thereby achieving a significant competitive edge. The continuous advancements in robotic technology itself, including greater precision, dexterity, and artificial intelligence capabilities, are making robots more versatile and suitable for a wider array of complex tasks. This technological evolution directly fuels the demand for integration services to seamlessly incorporate these advanced robots into existing workflows. Furthermore, the pressing need for cost reduction in labor-intensive operations, coupled with the rising labor costs and shortages in many regions, is pushing companies towards automation as a viable and economically attractive alternative. The growing emphasis on workplace safety is another significant driver; robots can be deployed in hazardous environments, protecting human workers from injury and exposure to dangerous conditions. The global push towards digital transformation and smart factories, often referred to as Industry 4.0, is intrinsically linked to robotics system integration, as robots form a cornerstone of automated and interconnected manufacturing ecosystems. This holistic approach to automation, where robots communicate with other machines and systems, amplifies the benefits of integration and drives further adoption.

Despite the robust growth trajectory, the robotics system integration market is not without its hurdles. A primary challenge lies in the significant initial investment required for acquiring robotic hardware and implementing integration solutions. This capital expenditure can be a considerable barrier, particularly for small and medium-sized enterprises (SMEs) who may struggle with the upfront costs. The complexity of integrating diverse robotic systems with existing legacy infrastructure and disparate software platforms presents another substantial challenge. Ensuring seamless interoperability and data flow requires specialized expertise and can lead to prolonged implementation timelines and increased project costs. A shortage of skilled professionals capable of designing, implementing, and maintaining these complex robotic systems is also a major restraint. The demand for robotics integration engineers, software developers with automation expertise, and maintenance technicians often outstrips the available supply. Cybersecurity concerns also loom large, as increasingly connected robotic systems become potential targets for cyberattacks, necessitating robust security measures and protocols. Furthermore, the perception of robots as job displacers can lead to resistance from workforces and unions, requiring careful change management strategies and a focus on reskilling and upskilling programs. The standardization of robotic hardware and software protocols is still evolving, which can complicate integration efforts and lead to vendor lock-in. Addressing these challenges effectively will be crucial for unlocking the full potential of the robotics system integration market.

The global Robotics System Integration market is projected to be dominated by a few key regions and specific industry segments, driven by a combination of advanced technological adoption, strong industrial bases, and supportive government initiatives.

Dominant Regions/Countries:

Dominant Segment: Application - Automotive

The Automotive sector is expected to be the leading application segment driving the demand for robotics system integration throughout the study period (2019-2033).

While other segments like Electrical & Electronics also show substantial growth due to the high volume production and miniaturization demands, the established and continuously evolving automation needs of the Automotive sector position it as the primary driver of the global Robotics System Integration market for the foreseeable future. The integration of AI and machine learning into automotive production lines, facilitated by system integrators, will further solidify this dominance.

The robotics system integration industry is propelled by several key growth catalysts. The accelerating adoption of Industry 4.0 principles and the development of smart factories are a primary driver, demanding sophisticated automation solutions. Furthermore, the increasing global demand for manufacturing efficiency and productivity, coupled with rising labor costs, makes robotic integration an economically attractive proposition. The continuous innovation in robotics hardware, including more versatile and intelligent robots, and advancements in software for intuitive programming and control, are expanding the application possibilities. The growing emphasis on workplace safety, leading to the deployment of robots in hazardous environments, also fuels market expansion.

This report provides an in-depth analysis of the global Robotics System Integration market, covering the historical period from 2019 to 2024 and offering robust forecasts up to 2033, with 2025 serving as both the base and estimated year. It meticulously examines market dynamics, including key trends, driving forces, and challenges that shape the industry's trajectory. The report delves into the market segmentation by type (Hardware, Software, Service), application (Automotive, Electrical & Electronics, Metal Industry, Chemical, Rubber and Plastic, Food, Beverages and Pharmaceuticals, Others), and analyzes significant industry developments. Furthermore, it identifies the leading players, offering insights into their market presence and strategic contributions. With a comprehensive scope, this report aims to equip stakeholders with the critical intelligence needed to navigate and capitalize on the evolving landscape of robotics system integration.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.5% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.5%.

Key companies in the market include FFT, BOZHON, Motoman Robotics, STEP, Siasun, HGZN, JEE, CSG Smart Science, Colibri Technologies, ZHIYUN, EFFORT, SINYLON, Guangzhou Risong Technology, Guangdong Topstar Technology, SCOTT, Genesis Systems (IPG Photonics), CBWEE, Jiangsu Beiren Robot System, HCD, SIERT, Acieta, QUICK, SVIA (ABB), BOSHIAC, Midwest Engineered Systems, APT Manufacturing Solutions, Motion Controls Robotics, Geku Automation, Tigerweld, .

The market segments include Type, Application.

The market size is estimated to be USD 39610 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Robotics System Integration," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Robotics System Integration, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.