1. What is the projected Compound Annual Growth Rate (CAGR) of the Prepared Vegetables?

The projected CAGR is approximately 4.2%.

Prepared Vegetables

Prepared VegetablesPrepared Vegetables by Type (Ready to Eat (RTE), Ready to Heat (RTH), Ready to Cook (RTC), World Prepared Vegetables Production ), by Application (Online Sales, Offline Sales, World Prepared Vegetables Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

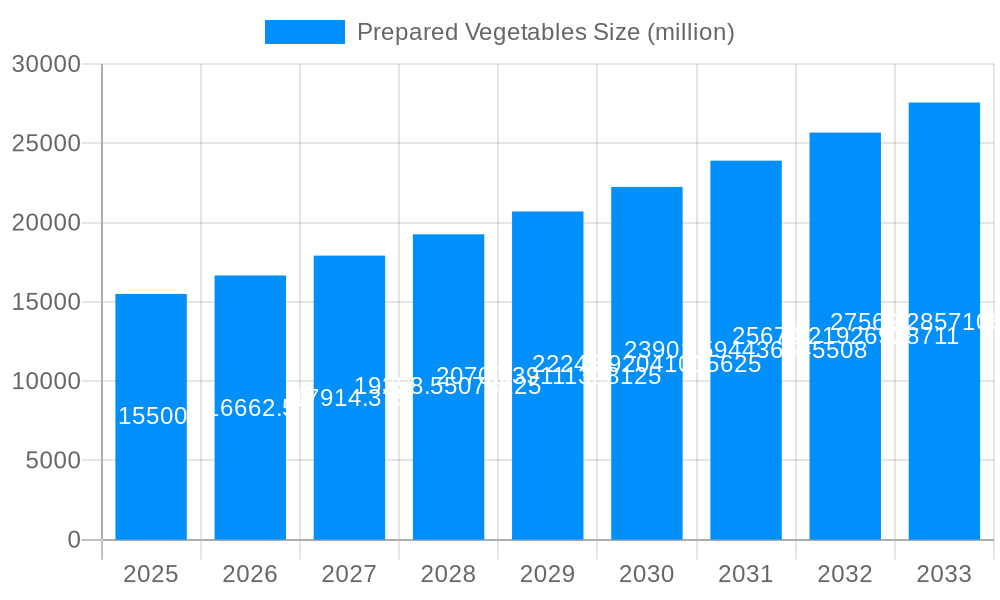

The global Prepared Vegetables market is poised for significant expansion, projected to reach an estimated USD 15,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 7.5% anticipated through 2033. This substantial growth is fueled by evolving consumer lifestyles characterized by increased demand for convenience, rising disposable incomes, and a growing awareness of the health benefits associated with vegetable consumption. The market is strategically segmented by type into Ready to Eat (RTE), Ready to Heat (RTH), and Ready to Cook (RTC) options, catering to diverse consumer needs and preferences for immediate consumption, simple reheating, or minimal preparation. The "World Prepared Vegetables Production" is a key indicator driving these segments, highlighting the increasing global capacity to meet this demand. Furthermore, the application of Online Sales and Offline Sales reflects the dual-channel approach adopted by market players to ensure broad accessibility and capture a wider customer base for prepared vegetable products.

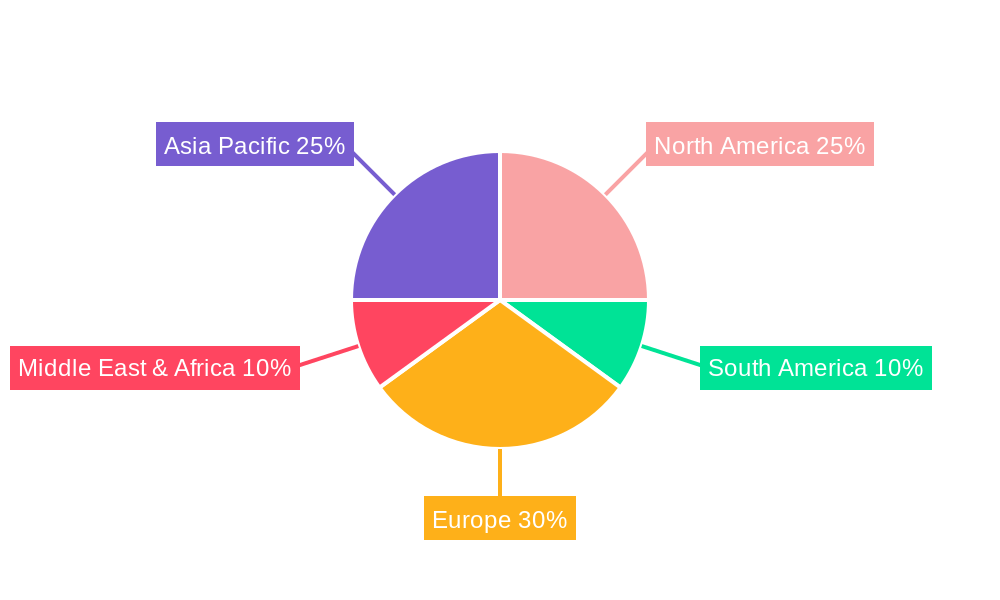

The market landscape is dynamic, influenced by several key drivers and emerging trends. The increasing adoption of advanced processing technologies, such as IQF (Individually Quick Frozen) and dehydration, enhances the shelf-life and nutritional value of prepared vegetables, making them more attractive to consumers. Innovations in packaging, including retort pouches and modified atmosphere packaging (MAP), further contribute to product appeal and market penetration. However, certain restraints, such as the perception of processed foods being less nutritious than fresh counterparts and potential price sensitivity among some consumer segments, could temper growth. The competitive environment is shaped by major players like Nestle, SYSCO, and Kobe Bussan, who are actively investing in product innovation, market expansion, and strategic collaborations to solidify their market positions. The Asia Pacific region, led by China and India, is expected to be a dominant force due to its large population, rapid urbanization, and growing middle class.

This comprehensive report delves into the dynamic global Prepared Vegetables market, offering a detailed analysis from the historical period of 2019-2024, with a base year of 2025 and an extensive forecast period spanning 2025-2033. The study meticulously examines market trends, driving forces, challenges, key regional and segmental dominance, growth catalysts, leading players, and significant industry developments. The global prepared vegetables market is projected to experience a significant upward trajectory, reaching an estimated USD 150,000 million by 2025, with continued robust growth expected throughout the forecast period, potentially exceeding USD 250,000 million by 2033. This report provides invaluable insights for stakeholders seeking to navigate and capitalize on the evolving landscape of this essential food sector.

The global Prepared Vegetables market is experiencing a multifaceted evolution driven by shifting consumer lifestyles, technological advancements in food processing, and an increasing awareness of health and convenience. The overarching trend is a move towards greater convenience without compromising on perceived health benefits. Ready-to-Eat (RTE) and Ready-to-Heat (RTH) segments are witnessing substantial growth as busy urban populations prioritize quick meal solutions. These segments are not merely about convenience; manufacturers are increasingly focusing on offering a wider variety of ethnically diverse cuisines and incorporating novel ingredients to cater to evolving palates. The demand for minimally processed, nutrient-rich options is also on the rise, pushing innovation in packaging and preservation techniques that retain nutritional value and natural flavors. XXX The market is also seeing a surge in value-added products, such as vegetable mixes with sauces or seasonings, further simplifying meal preparation for consumers. This signifies a move beyond basic chopping and dicing towards more sophisticated product offerings. Furthermore, sustainability and ethical sourcing are gaining prominence. Consumers are increasingly scrutinizing the environmental impact of their food choices, leading to a greater demand for sustainably grown and ethically produced prepared vegetables. This includes a focus on reducing food waste throughout the supply chain, from farm to fork, and promoting responsible packaging solutions. The market is also being shaped by advancements in cold chain logistics and ultra-low temperature processing, which are crucial for maintaining the freshness and quality of prepared vegetables, thereby expanding their reach and shelf life. This technological integration is critical for meeting the growing demand in regions with complex supply chains. The rise of e-commerce and online grocery platforms is also revolutionizing the distribution of prepared vegetables, making them more accessible to a wider consumer base and fostering a more direct relationship between producers and consumers. This digital shift is expected to contribute significantly to market expansion in the coming years.

Several key factors are propelling the growth of the global Prepared Vegetables market. Foremost among these is the accelerating pace of urbanization and the subsequent rise in dual-income households. As individuals lead increasingly hectic lives, the demand for convenient and time-saving meal solutions has surged. Prepared vegetables directly address this need, offering pre-portioned and often pre-cooked ingredients that significantly reduce preparation time. The growing health consciousness among consumers globally is another significant driver. Despite the convenience factor, there is a concurrent demand for healthy food options. Manufacturers are responding by developing prepared vegetable products that are perceived as nutritious, often highlighting their vitamin and mineral content and offering options with reduced sodium and fat. Furthermore, advancements in food processing technologies, such as improved freezing, blanching, and packaging methods, have enhanced the shelf life and quality of prepared vegetables, making them more appealing and accessible to a broader market. The increasing adoption of e-commerce and online grocery platforms has also expanded the reach of prepared vegetables, allowing consumers to easily purchase these products from the comfort of their homes. This convenience, coupled with the growing availability of diverse culinary options within the prepared vegetable category, is further fueling market expansion. The rise of the foodservice industry, including restaurants and catering services, also contributes to the demand for bulk prepared vegetables, further solidifying their market presence.

Despite the robust growth, the Prepared Vegetables market faces certain challenges and restraints. One of the primary concerns revolves around perceived freshness and quality. Consumers often associate fresh produce with superior taste and nutritional value, and some may be hesitant to embrace prepared vegetables due to concerns about spoilage, nutrient degradation, or the use of preservatives. Maintaining consistent quality and freshness throughout the supply chain, from processing to delivery, is paramount and requires significant investment in cold chain infrastructure. Another significant restraint is the price sensitivity of a segment of consumers. While convenience is a key selling point, the cost of prepared vegetables can sometimes be higher than purchasing raw ingredients, which can deter budget-conscious shoppers. Consumer preferences and taste profiles also present a dynamic challenge. The demand for diverse flavors and ingredients is constantly evolving, requiring manufacturers to continuously innovate and adapt their product offerings to remain competitive and cater to niche culinary trends. Furthermore, supply chain disruptions, whether due to adverse weather conditions affecting crop yields, geopolitical issues, or transportation challenges, can impact the availability and cost of raw vegetables, subsequently affecting the production and pricing of prepared vegetables. The regulatory landscape surrounding food safety and labeling also demands strict adherence, and any lapse can lead to significant reputational and financial damage. Finally, the skepticism regarding the health benefits of processed foods, in general, can sometimes cast a shadow over prepared vegetable products, necessitating clear communication about their nutritional value and processing methods.

The Ready to Eat (RTE) segment, alongside the Offline Sales application, is poised to dominate the global Prepared Vegetables market in the coming years. This dominance is particularly pronounced in Asia Pacific and North America.

Ready to Eat (RTE) Segment Dominance:

North America: The sustained growth of the RTE prepared vegetables segment in North America is driven by its highly urbanized population, dual-income households, and a deeply ingrained culture of convenience. Consumers in this region have a high disposable income and are willing to pay a premium for products that save them time and effort in meal preparation. The increasing prevalence of single-person households and a growing elderly population also contribute to the demand for single-serving or easy-to-prepare RTE options. Furthermore, the strong presence of major food manufacturers and retailers in North America, coupled with their extensive distribution networks, ensures widespread availability of RTE prepared vegetables. Innovations in packaging, such as microwaveable pouches and ready-to-eat meal kits, have further enhanced the appeal of this segment. The market is also witnessing a rise in premium RTE options that cater to specific dietary needs, such as organic, gluten-free, and plant-based offerings, appealing to health-conscious consumers.

Asia Pacific: The Asia Pacific region is expected to exhibit the most dynamic growth within the RTE prepared vegetables segment. Rapid economic development, increasing disposable incomes, and a rapidly expanding middle class are transforming consumer lifestyles. Urbanization is leading to a significant influx of people into cities, where time is a scarce commodity. This, coupled with a growing adoption of Western dietary habits, is fueling the demand for convenient food solutions like RTE prepared vegetables. Countries like China, India, and Southeast Asian nations are witnessing a surge in demand driven by younger demographics who are more open to trying new food products and embracing convenience. The penetration of modern retail formats, including supermarkets and hypermarkets, is increasing, making RTE products more accessible. Furthermore, the burgeoning foodservice industry and the rise of online food delivery platforms are significantly contributing to the popularity and consumption of RTE prepared vegetables. The diverse culinary landscape of Asia also presents an opportunity for manufacturers to develop localized RTE options, incorporating popular regional flavors and ingredients.

Offline Sales Application Dominance:

The combined dominance of the RTE segment and offline sales channels, particularly in the rapidly evolving Asia Pacific and the established North American markets, signifies a strong and enduring demand for convenient, accessible, and evolving prepared vegetable solutions globally.

The growth of the Prepared Vegetables industry is significantly catalyzed by the increasing demand for convenience-driven food solutions due to busy lifestyles and urbanization. This is complemented by a growing consumer focus on health and wellness, leading to a preference for nutrient-rich, minimally processed options. Technological advancements in food processing and preservation, such as improved freezing and packaging techniques, are extending shelf life and maintaining quality, thereby expanding market reach. The expanding penetration of modern retail formats and the burgeoning e-commerce sector are further enhancing accessibility and consumer reach.

This report provides an exhaustive analysis of the global Prepared Vegetables market, offering a deep dive into market dynamics, consumer behavior, and technological innovations. It meticulously covers the historical performance from 2019-2024 and projects future trends through 2033, with a specific focus on the base and estimated year of 2025. The report details the market's value in the millions, highlighting key segments like Ready to Eat (RTE), Ready to Heat (RTH), and Ready to Cook (RTC), and explores application channels such as Online and Offline Sales. Its comprehensive nature ensures that stakeholders receive actionable insights to navigate the competitive landscape effectively.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.2%.

Key companies in the market include SYSCO, Nestle, Kobe Bussan, Nichirei, Mash Direct Ltd, Willow Run Foods, Milne Foods Limited, Simped Foods, Farmfresh Fine Foods, Autor Foods, Jinlongyu, Fujian Sunner, Shandong Longda, Zhanjiang Guolian, Fu Jian Anjoy Foods Co, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Prepared Vegetables," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Prepared Vegetables, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.