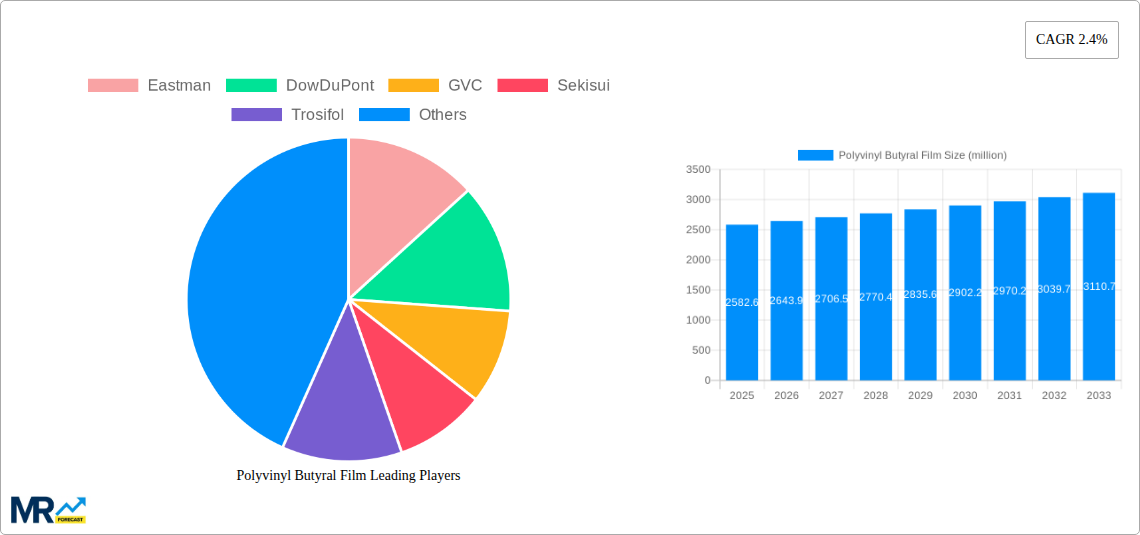

1. What is the projected Compound Annual Growth Rate (CAGR) of the Polyvinyl Butyral Film?

The projected CAGR is approximately 2.4%.

Polyvinyl Butyral Film

Polyvinyl Butyral FilmPolyvinyl Butyral Film by Type (Construction Grade, Automotive Grade, Solar Grade), by Application (Construction, Automotive, Photovoltaic Glass Industry, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

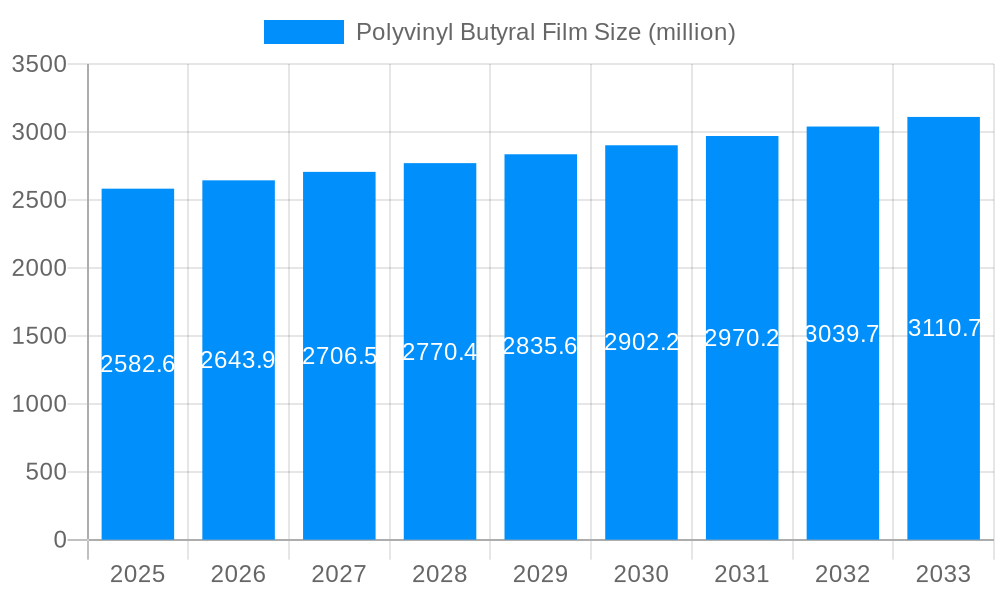

The global Polyvinyl Butyral (PVB) Film market is poised for steady expansion, currently valued at approximately $2582.6 million. With a projected Compound Annual Growth Rate (CAGR) of 2.4% through 2033, the market demonstrates a consistent upward trajectory, driven by robust demand across key sectors. The construction industry represents a significant driver, fueled by the increasing use of laminated safety glass in buildings for enhanced security and insulation. The automotive sector also plays a crucial role, with PVB films being indispensable for windshields and side windows, contributing to vehicle safety and noise reduction. Furthermore, the burgeoning photovoltaic glass industry, demanding specialized PVB films for solar panel lamination, presents a substantial growth opportunity. Emerging economies, particularly in Asia Pacific, are expected to witness accelerated growth due to rapid industrialization and infrastructure development.

The market's growth is further supported by ongoing technological advancements in PVB film production, leading to enhanced performance characteristics such as improved UV resistance, acoustic dampening, and adhesion properties. These innovations cater to evolving industry standards and consumer expectations for safer, more durable, and energy-efficient applications. While the market exhibits strong growth fundamentals, certain restraints such as fluctuating raw material prices and the availability of substitute materials in niche applications could pose challenges. However, the inherent superior properties of PVB films, particularly in safety and durability, are expected to outweigh these concerns, ensuring sustained demand. Key market players are actively investing in research and development and expanding their production capacities to meet the growing global demand, solidifying the PVB Film market's promising future.

This report offers an in-depth analysis of the global Polyvinyl Butyral (PVB) film market, providing crucial insights for stakeholders. The study encompasses the historical period from 2019 to 2024, the base and estimated year of 2025, and extends to a comprehensive forecast period of 2025-2033. With a total market valuation projected to reach $XX million by 2025 and substantial growth anticipated throughout the forecast period, this report is an essential resource for understanding market dynamics.

The global Polyvinyl Butyral (PVB) film market is undergoing a significant transformation, driven by an escalating demand for enhanced safety, durability, and aesthetic appeal across various end-use industries. XXX represents a pivotal inflection point for this market, with several key trends shaping its trajectory. The Automotive Grade segment, a cornerstone of the PVB film industry, is experiencing robust growth, fueled by stringent safety regulations mandating advanced laminated glass for windshields and side windows. These regulations, emphasizing improved impact resistance and shatter mitigation, are directly translating into higher consumption of PVB films. Beyond safety, the automotive sector is also witnessing a surge in demand for advanced functionalities such as acoustic insulation and UV protection, areas where PVB films excel, further bolstering their adoption.

Simultaneously, the Construction Grade segment is demonstrating remarkable resilience and expansion. The burgeoning global construction industry, particularly in emerging economies, is a significant contributor. The increasing emphasis on energy-efficient buildings, enhanced acoustic performance, and architectural innovation requiring larger, more complex glass installations are all key drivers for PVB film consumption in this sector. Furthermore, the growing awareness and adoption of safety glazing in both residential and commercial buildings, driven by improved building codes and a general desire for enhanced security, are propelling the demand for PVB interlayers. The rising popularity of decorative and specialized architectural glass, where PVB films offer a versatile platform for color integration, frosting, and other aesthetic modifications, also contributes to this trend. The market is witnessing a gradual yet steady shift towards higher-performance PVB grades, capable of meeting increasingly demanding specifications.

The Solar Grade segment, while currently representing a smaller share, is poised for significant future growth. With the global push towards renewable energy sources, the solar photovoltaic (PV) industry is expanding at an unprecedented rate. PVB films are gaining traction as an alternative interlayer material in solar panels, offering advantages such as enhanced durability, excellent UV resistance, and improved efficiency compared to traditional encapsulants in certain applications. As the cost-effectiveness and performance benefits of PVB in solar applications become more widely recognized, this segment is expected to become a major growth engine for the overall PVB film market. The increasing focus on longevity and performance of solar modules under diverse environmental conditions will further drive the adoption of high-quality PVB films.

The market is also characterized by a growing demand for specialty PVB films with tailored properties. This includes films with enhanced adhesion to specific glass types, improved optical clarity, and superior resistance to extreme temperatures and humidity. Manufacturers are investing in research and development to create customized solutions that cater to the evolving needs of their clientele. Furthermore, the global supply chain for PVB films is becoming more consolidated, with leading players expanding their production capacities and geographical reach to meet the escalating demand. Strategic partnerships and mergers and acquisitions are also observed as companies seek to strengthen their market position and gain access to new technologies and markets. The overarching trend is towards a more sophisticated and diversified PVB film market, driven by innovation, regulatory mandates, and the pursuit of enhanced performance and sustainability.

The Polyvinyl Butyral (PVB) film market is experiencing a robust expansion, propelled by a confluence of powerful driving forces that underscore its essential role in modern industries. Foremost among these is the unwavering emphasis on safety and security. Stringent government regulations worldwide, particularly in the automotive and construction sectors, mandate the use of laminated safety glass, where PVB film serves as the critical interlayer. In automotive applications, these regulations are designed to prevent passenger ejection during collisions and minimize the risk of injury from shattered glass. Similarly, in construction, safety glazing incorporating PVB films is crucial for preventing falls through windows and doors, enhancing security against forced entry, and mitigating the impact of potential hazards. This regulatory push directly translates into sustained and increasing demand for PVB films as a non-negotiable component in these applications.

Beyond regulatory mandates, the growing consumer demand for enhanced comfort and performance is another significant driver. In the automotive industry, there is an increasing preference for vehicles offering superior acoustic insulation, reducing cabin noise for a more serene driving experience. PVB films are highly effective in dampening sound vibrations, making them an ideal choice for acoustic laminated glass. Similarly, the demand for UV protection in vehicles and buildings, to prevent fading of interiors and protect occupants from harmful radiation, further boosts PVB film adoption. In the construction sector, the pursuit of energy-efficient buildings, with improved thermal performance and reduced reliance on artificial lighting, is leading to the increased use of sophisticated glazing solutions that often incorporate PVB films for their insulating properties and ability to integrate with low-emissivity coatings. The architectural trend towards larger, more complex glass structures, requiring interlayers that can maintain structural integrity and safety, also fuels the market. The continuous advancements in PVB manufacturing technology, leading to improved film properties such as clarity, adhesion, and durability, further enhance its attractiveness to end-users, creating a positive feedback loop for market growth.

Despite its robust growth trajectory, the Polyvinyl Butyral (PVB) film market is not without its challenges and restraints, which can temper its overall expansion. One of the primary concerns is the volatility of raw material prices. The production of PVB film is heavily reliant on petrochemical derivatives, primarily polyvinyl alcohol (PVA) and butyraldehyde. Fluctuations in crude oil prices and the availability of these precursor chemicals can significantly impact the manufacturing cost of PVB films, leading to price instability and affecting profit margins for producers. This price volatility can also make it challenging for end-users to forecast their material costs accurately, potentially leading to hesitations in large-scale procurement.

Furthermore, the emergence and ongoing development of alternative interlayer materials pose a competitive threat. While PVB film has established itself as a leading choice, ongoing research and development in the field of thermoplastic polyurethanes (TPUs), ethylene-vinyl acetate (EVA) co-polymers, and other advanced polymer interlayers are presenting viable alternatives in specific applications. These alternatives may offer unique properties such as enhanced flexibility, higher impact resistance in certain scenarios, or lower processing temperatures, which could attract certain market segments. The complex manufacturing process and high initial investment required for PVB film production can also act as a restraint, particularly for smaller players or those looking to enter the market. Establishing state-of-the-art production facilities necessitates substantial capital outlay and sophisticated technological expertise, creating barriers to entry.

Moreover, the disposal and recycling of PVB films present an environmental challenge. While PVB is a durable material, its end-of-life management can be complex, especially when integrated within laminated glass structures. Developing efficient and cost-effective recycling processes for post-consumer PVB films remains an area of active research and development. Improper disposal can lead to environmental concerns, potentially impacting the long-term sustainability perception of the material. Finally, geopolitical factors and trade policies can also introduce uncertainties. Tariffs, trade disputes, and varying environmental regulations across different regions can disrupt global supply chains and influence market access, creating operational hurdles for international PVB film manufacturers and suppliers.

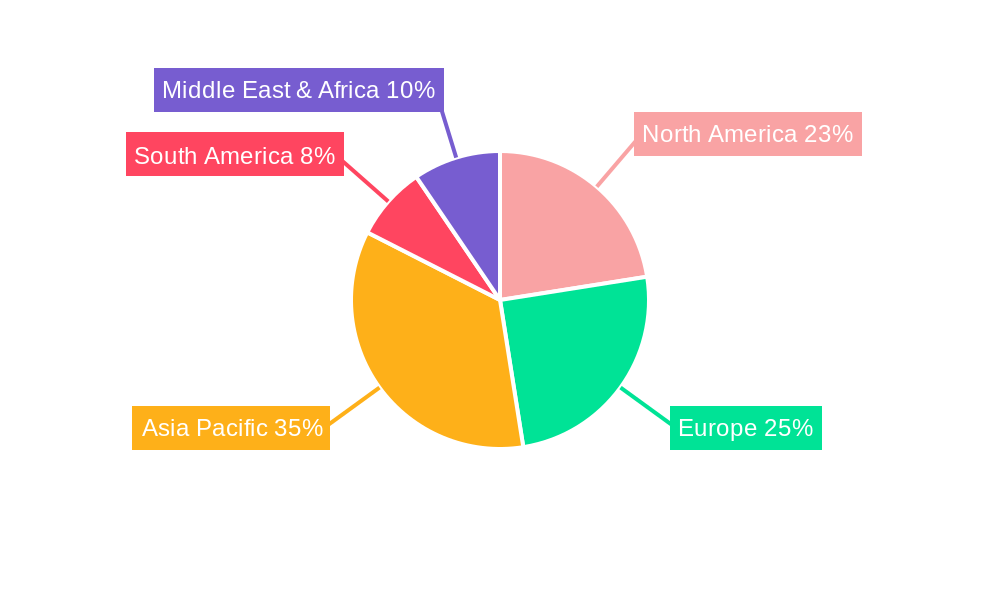

The global Polyvinyl Butyral (PVB) film market is characterized by strong regional dynamics and segment dominance, with Asia-Pacific emerging as a powerhouse and the Automotive Grade segment leading the charge in terms of market share and projected growth.

Asia-Pacific Region: A Dominant Force

The Asia-Pacific region is poised to be the dominant force in the global PVB film market throughout the study period (2019-2033). Several factors contribute to its leading position:

Automotive Grade Segment: The Undisputed Leader

Within the PVB film market segments, the Automotive Grade segment is the undisputed leader and is expected to maintain its dominance throughout the forecast period.

While the Construction Grade segment is also substantial and growing, and the Solar Grade segment shows promising future growth, the sheer volume of automotive production globally and the inherent safety requirements ensure that the Automotive Grade segment will continue to be the primary driver of the PVB film market for the foreseeable future. The synergy between the dominant Asia-Pacific region and the leading Automotive Grade segment creates a powerful market dynamic that will shape the industry landscape.

The Polyvinyl Butyral (PVB) film industry is set for sustained growth, propelled by several key catalysts. The unrelenting global focus on enhanced safety standards across automotive and construction sectors mandates the use of laminated glass, a primary application for PVB. Furthermore, the burgeoning renewable energy sector, particularly the solar photovoltaic industry, is increasingly adopting PVB films for panel encapsulation, driven by their durability and efficiency. Growing consumer demand for improved comfort and performance features in vehicles, such as acoustic insulation and UV protection, also acts as a significant growth catalyst. Continuous technological advancements in PVB film manufacturing, leading to superior properties and cost-effectiveness, further stimulate market expansion.

This report provides a comprehensive overview of the global Polyvinyl Butyral (PVB) film market, delving into intricate details that go beyond surface-level analysis. It offers a deep dive into the market's historical performance, current landscape, and future projections, encompassing the study period of 2019-2033. The report meticulously analyzes key trends, such as the increasing demand for safety and acoustic performance in automotive and construction applications, alongside the burgeoning potential of PVB films in the solar energy sector. It further dissects the critical driving forces, including stringent safety regulations and consumer preference for enhanced comfort, while also acknowledging and addressing the significant challenges and restraints faced by the industry, such as raw material price volatility and the emergence of alternative materials. The report meticulously identifies and elaborates on the dominant regions and segments, with a particular focus on the Asia-Pacific region's stronghold and the unwavering leadership of the Automotive Grade segment. Moreover, it highlights crucial growth catalysts and profiles the leading players in the market, providing valuable competitive intelligence. Finally, the report documents significant industry developments and offers a holistic perspective, equipping stakeholders with the necessary insights to navigate and capitalize on the evolving PVB film market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.4%.

Key companies in the market include Eastman, DowDuPont, GVC, Sekisui, Trosifol, Kuraray, J&S Group, ChangChun, Zhejiang Decent, Lifeng Group, Xinfu Pharm, DuLite, Aojisi, Huakai PVB, Liyang PVB, Meibang, .

The market segments include Type, Application.

The market size is estimated to be USD 2582.6 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Polyvinyl Butyral Film," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Polyvinyl Butyral Film, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.