1. What is the projected Compound Annual Growth Rate (CAGR) of the Point of Care Rapid Diagnosis?

The projected CAGR is approximately XX%.

Point of Care Rapid Diagnosis

Point of Care Rapid DiagnosisPoint of Care Rapid Diagnosis by Type (Blood Glucose Testing, Blood Gas and Electrolytes Analysis, Rapid Coagulation Testing, Rapid Cardiac Markers Diagnostic, Drugs of Abuse Screening, Food Pathogens Screening, Hemoglobin Diagnostics, Infectious Disease Testing, Others, World Point of Care Rapid Diagnosis Production ), by Application (Clinics, Hospitals, Laboratory, Others, World Point of Care Rapid Diagnosis Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

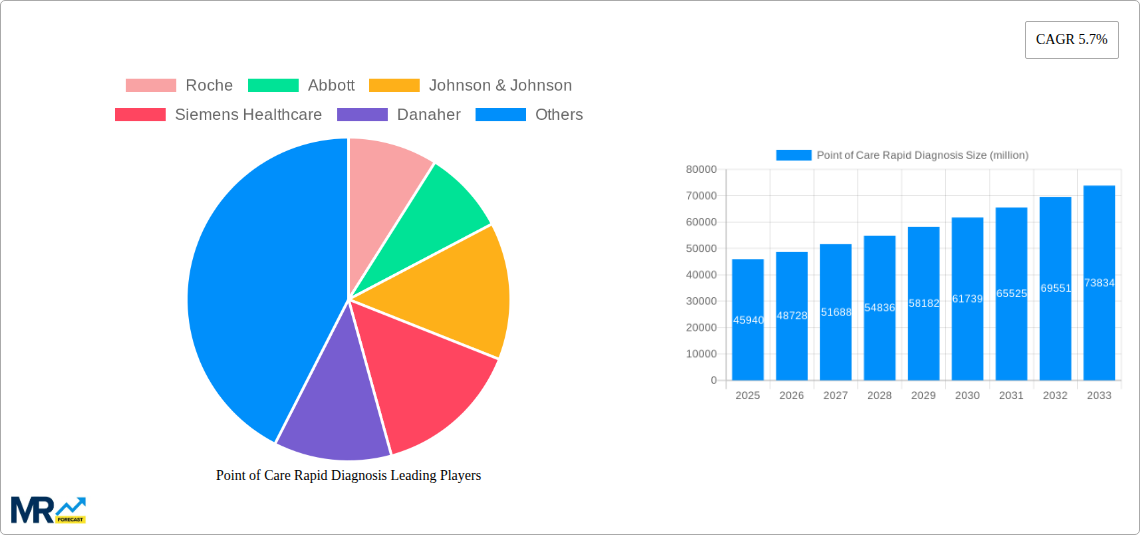

The Point-of-Care (POC) rapid diagnostics market, valued at $67.91 billion in 2025, is experiencing robust growth driven by several key factors. The increasing prevalence of chronic diseases necessitates faster diagnostic capabilities, leading to a surge in demand for POC tests that deliver immediate results at the patient's side. Technological advancements, such as improved assay formats (e.g., lateral flow immunoassays, electrochemical biosensors) and miniaturized devices, have enhanced the accuracy, speed, and ease of use of these tests, further propelling market expansion. Furthermore, the rising adoption of POC diagnostics in resource-limited settings, where access to centralized laboratories is constrained, is a significant driver. This is particularly true in developing economies where the demand for affordable and accessible healthcare solutions is high. The market is segmented by test type (blood glucose, blood gas, coagulation, cardiac markers, etc.), application (clinics, hospitals, laboratories), and geography. North America and Europe currently hold significant market shares due to well-established healthcare infrastructure and higher adoption rates, but growth potential in Asia Pacific and other emerging markets is significant. Challenges include regulatory hurdles for new diagnostic technologies, and the need for continuous improvement in test accuracy and sensitivity to ensure reliable results.

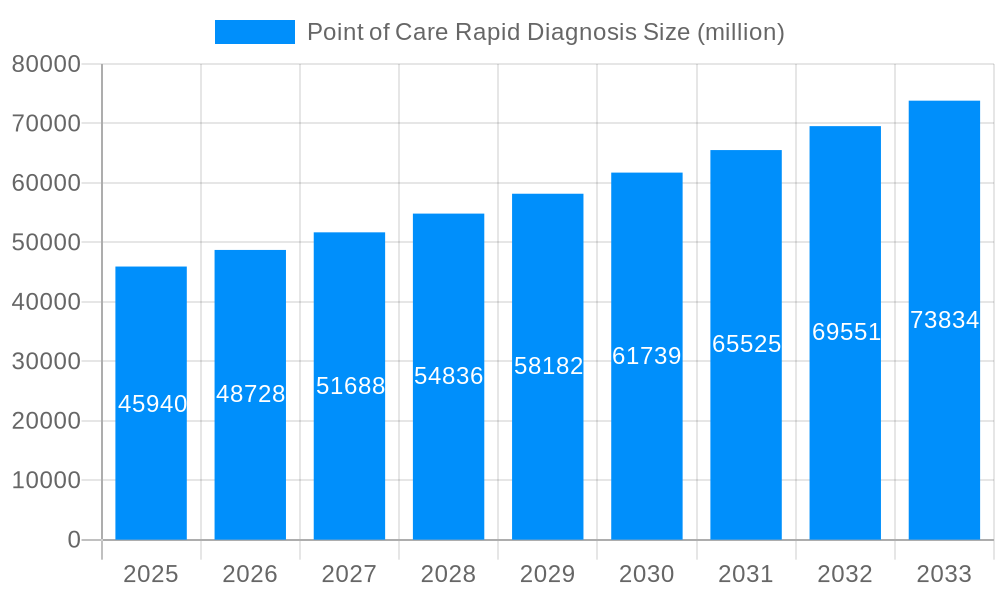

The forecast period (2025-2033) projects continued expansion of the POC rapid diagnostics market, fueled by sustained demand and ongoing technological innovations. Several factors contribute to this projection. The aging global population increases the prevalence of chronic conditions requiring frequent monitoring, creating consistent demand for convenient POC tests. Government initiatives promoting healthcare accessibility and advancements in telemedicine are expected to increase the demand for remote diagnostics using POC technology. The market will likely see continued consolidation, with larger companies acquiring smaller innovative players to expand their product portfolios. While pricing remains a factor influencing adoption, particularly in low-resource settings, continuous innovation is driving down costs, making POC testing more accessible. The competitive landscape is characterized by established players and emerging companies focusing on developing novel diagnostic tools and expanding their global reach.

The point-of-care (POC) rapid diagnosis market is experiencing robust growth, driven by several converging factors. The global market, valued at several billion dollars in 2024, is projected to reach tens of billions of dollars by 2033, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 7%. This expansion is fueled by the increasing prevalence of chronic diseases, the rising demand for faster diagnostic results, and the expanding adoption of POC testing in diverse healthcare settings. Technological advancements, such as the miniaturization of diagnostic devices and the integration of digital technologies, are further enhancing the accessibility and efficiency of POC testing. Furthermore, the rising geriatric population, coupled with the increasing incidence of infectious diseases, is significantly bolstering the demand for rapid diagnostic solutions. The market is also witnessing a shift towards decentralized healthcare models, with an increased focus on home healthcare and remote patient monitoring. This trend directly benefits POC diagnostics, allowing for timely interventions and improved patient outcomes. The integration of artificial intelligence (AI) and machine learning (ML) into POC devices is poised to revolutionize the accuracy and speed of diagnostics, making them even more impactful in healthcare delivery. This technological synergy will contribute to the market's continued expansion and improved overall healthcare efficiency in the coming years. The market exhibits a diverse landscape of players, ranging from established multinational corporations to emerging innovative companies, leading to a dynamic and competitive market environment. Key players are actively engaged in research and development, aiming to introduce advanced POC diagnostic tools. The ongoing investment in R&D will ultimately lead to the development of more sophisticated and effective POC diagnostic solutions, thereby further accelerating market growth. Moreover, lucrative partnerships and acquisitions within the market are prevalent, further consolidating market dominance and accelerating the introduction of technologically advanced products.

Several key factors are propelling the growth of the point-of-care rapid diagnosis market. The increasing prevalence of chronic diseases like diabetes and cardiovascular diseases necessitates frequent monitoring and timely interventions, driving the demand for rapid diagnostic tools. These tests, conducted near the patient, allow for immediate treatment decisions, improving patient outcomes and reducing hospital readmissions. Furthermore, the rise of infectious diseases, coupled with the need for rapid detection and containment, fuels the demand for quick and accurate diagnostic solutions. The global pandemic underscored the crucial role of rapid diagnostics in managing outbreaks, significantly accelerating market growth. The convenience and efficiency offered by POC testing are also key drivers. These tests minimize the turnaround time for results, eliminating the delays associated with sending samples to centralized laboratories. This speed allows for quicker diagnosis and treatment initiation, improving patient care and potentially saving lives. Advances in technology, such as miniaturization, improved sensitivity and specificity of assays, and integration with digital platforms, are significantly enhancing the capabilities and adoption of POC diagnostics. The increasing demand for decentralized healthcare, including home healthcare and remote patient monitoring, further enhances the utility and market appeal of point-of-care rapid diagnostic tests. Finally, supportive government initiatives and increasing healthcare expenditure globally are creating a favorable environment for market expansion.

Despite the significant growth potential, the point-of-care rapid diagnosis market faces several challenges. The high cost of advanced POC devices and tests can limit accessibility, particularly in low- and middle-income countries. Ensuring the accuracy and reliability of POC tests is crucial, and maintaining quality control across diverse settings presents a significant challenge. The need for continuous training and education for healthcare professionals to effectively utilize POC diagnostic technologies is also a factor impacting widespread adoption. Regulatory hurdles and variations in regulatory approvals across different regions pose complexities for market expansion. The integration of POC devices with electronic health records (EHRs) and healthcare information systems can be challenging, requiring standardized data formats and interoperability solutions. Furthermore, the potential for inaccurate results due to improper sample collection or handling can lead to misdiagnosis and inappropriate treatment decisions, impacting patient safety and eroding confidence in POC testing technologies. The complexity of managing supply chains and ensuring timely access to reagents and consumables, especially in remote areas, remains a logistical hurdle. Lastly, the limited reimbursement policies for certain POC tests in some healthcare systems restrict market growth.

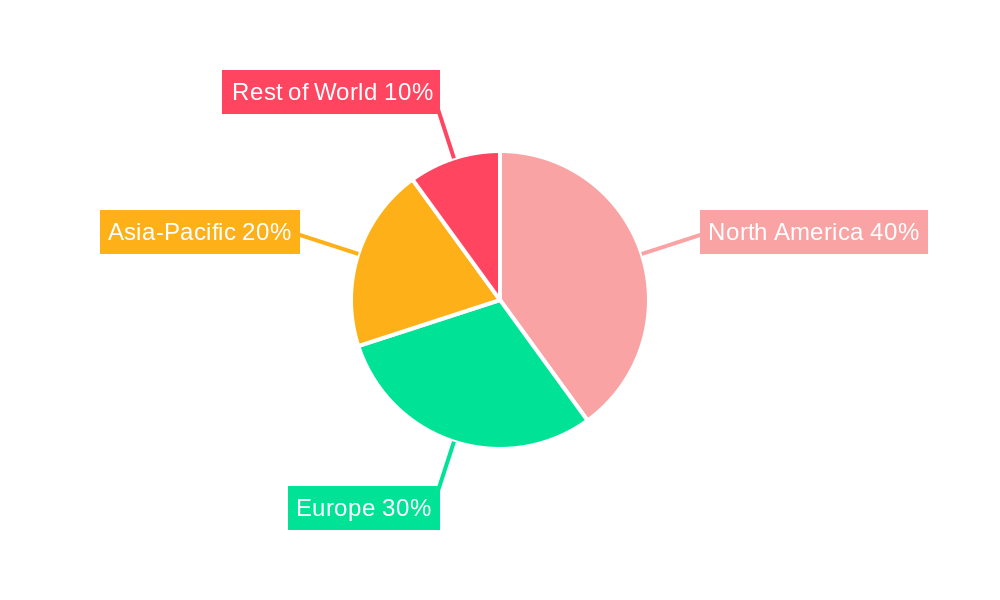

The North American market is expected to maintain its dominance in the POC rapid diagnosis market throughout the forecast period (2025-2033), driven by factors such as robust healthcare infrastructure, high technological adoption rates, and substantial investments in healthcare R&D. However, the Asia-Pacific region is poised for significant growth, driven by rising healthcare expenditure, increasing prevalence of chronic diseases, and expanding healthcare accessibility initiatives.

Dominant Segment: Infectious Disease Testing is a rapidly growing segment, accounting for a significant share of the market. The rising incidence of infectious diseases globally, coupled with the need for rapid diagnosis and containment, fuels demand for POC infectious disease tests. The segment is projected to continue its strong growth trajectory throughout the forecast period, driven by technological advancements and increasing awareness of the importance of rapid infectious disease diagnostics. This segment's growth is further fueled by the increasing prevalence of antibiotic-resistant infections, necessitating faster and more accurate diagnostic tools to guide appropriate treatment.

Specific countries within regions: The United States, within North America, is expected to remain the largest market, followed by Germany and other countries in Europe. Within Asia-Pacific, China and India are projected to witness strong growth, driven by significant population increases, rising healthcare expenditure, and expanding healthcare infrastructure.

Reasons for Dominance: The high prevalence of chronic and infectious diseases, coupled with strong healthcare infrastructure, supportive regulatory environments, and high technological adoption rates in North America and selected countries in Europe, accounts for their leading market positions. The Asia-Pacific region's growth is primarily fueled by its large and rapidly growing population, increasing healthcare expenditure, and government initiatives to improve healthcare access and quality.

Several factors are catalyzing growth in the POC rapid diagnosis industry. These include technological advancements resulting in smaller, faster, and more accurate diagnostic devices. Increased healthcare spending globally is driving demand for improved healthcare solutions. A growing focus on preventative care and early diagnosis is promoting the adoption of POC testing, and the rise of chronic diseases and infectious outbreaks necessitates rapid diagnosis and treatment options.

This report provides a comprehensive overview of the point-of-care rapid diagnosis market, encompassing market size and trends, growth drivers and challenges, key market segments, leading players, and significant developments. It offers a detailed analysis to support strategic decision-making within the industry. The information presented is based on extensive research and analysis of market data from the historical period (2019-2024), the base year (2025), and the estimated and forecast periods (2025-2033). The report provides valuable insights into the dynamics of this rapidly evolving market, offering a comprehensive perspective on opportunities and potential risks for industry stakeholders.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Roche, Abbott, Johnson & Johnson, Siemens Healthcare, Danaher, Ascensia, Bio-Rad Laboratories, BioMerieux, Nova Biomedical, Trividia Health, Quidel, Accriva, OraSure Technologies, Helena Laboratories, A. Menarini Diagnostics, Abaxis (Zoetis), Ortho Clinical Diagnostics, Phamatech, Chembio Diagnostics, Trinity Biotech, ELITech Group, Response Biomedical, Princeton BioMeditech, Alfa Wassermann, ARKRAY, .

The market segments include Type, Application.

The market size is estimated to be USD 67910 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Point of Care Rapid Diagnosis," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Point of Care Rapid Diagnosis, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.