1. What is the projected Compound Annual Growth Rate (CAGR) of the Pipeline Construction Services?

The projected CAGR is approximately 8.4%.

Pipeline Construction Services

Pipeline Construction ServicesPipeline Construction Services by Type (Oil and Gas Facility Construction, Design/Build Services, Pipeline Installation and Maintenance, Pipeline Integrity Services, Directional Drilling, Structural Steel & Pipe Fabrication, Others), by Application (Petrochemical, Oil & Gas, Water Treatment, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

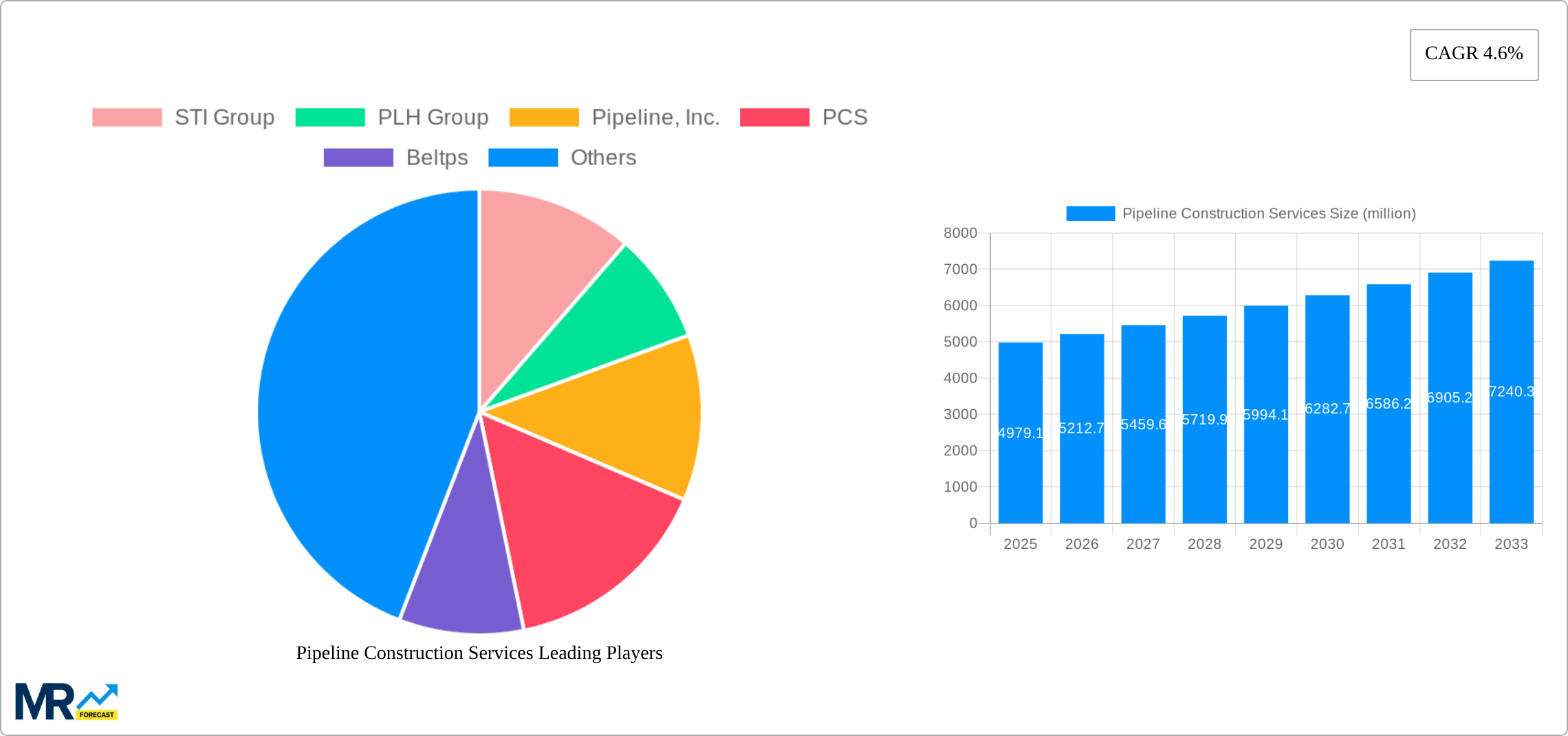

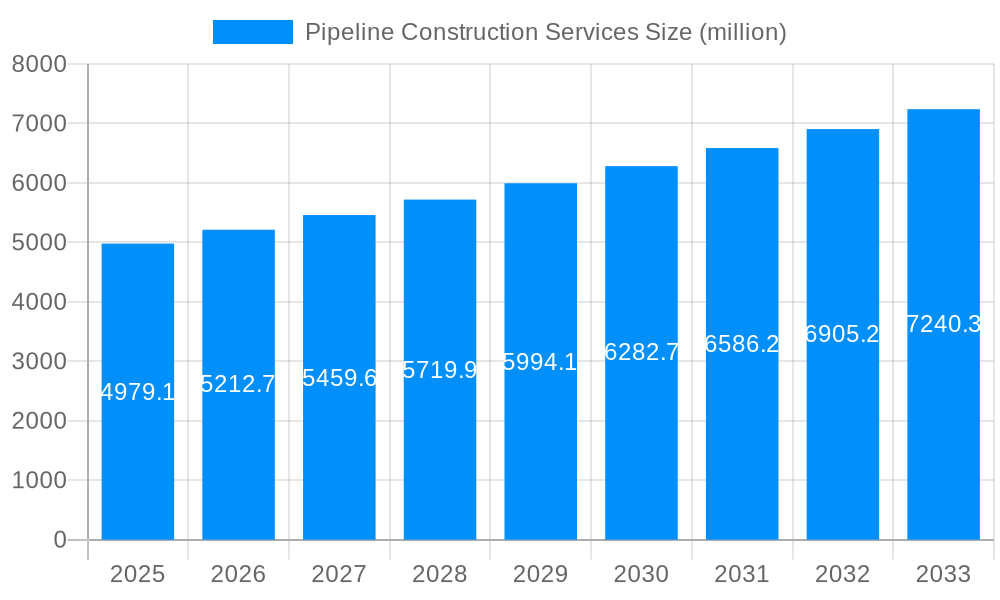

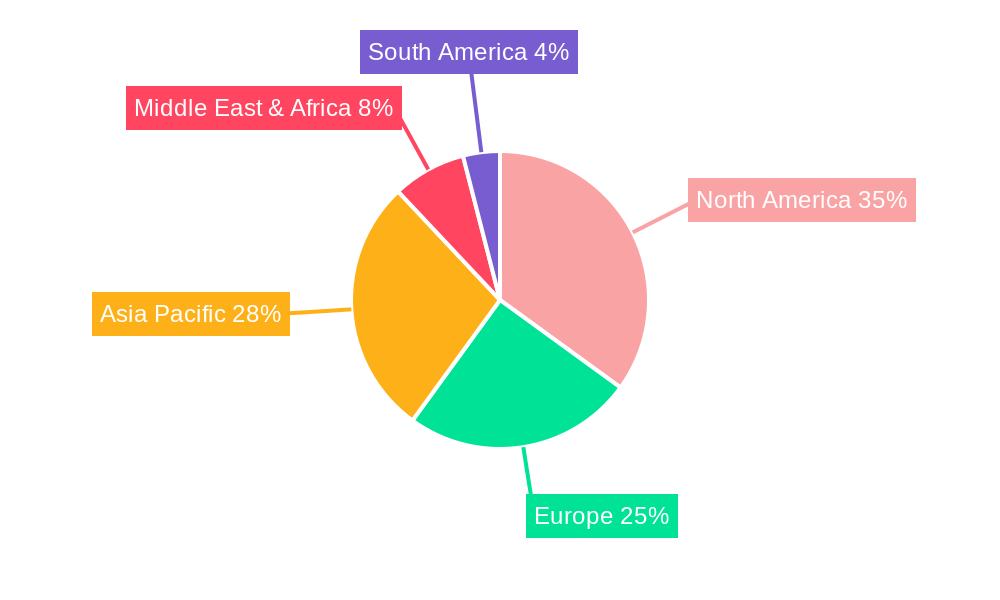

The global pipeline construction services market, valued at $4,979.1 million in 2025, is projected to experience robust growth, driven by increasing investments in oil and gas infrastructure, particularly in emerging economies experiencing rapid industrialization. The market's Compound Annual Growth Rate (CAGR) of 4.6% from 2025 to 2033 indicates a steady expansion, fueled by rising energy demands and the need for efficient energy transportation networks. Significant growth drivers include the expansion of oil and gas exploration and production activities, governmental initiatives promoting energy infrastructure development, and the increasing adoption of advanced technologies like directional drilling and pipeline integrity management systems. The market is segmented by type (Oil and Gas Facility Construction, Design/Build Services, Pipeline Installation and Maintenance, Pipeline Integrity Services, Directional Drilling, Structural Steel & Pipe Fabrication, Others) and application (Petrochemical, Oil & Gas, Water Treatment, Others). While growth is expected across all segments, the Oil & Gas facility construction and pipeline installation and maintenance segments are anticipated to witness the most significant growth due to their crucial role in energy infrastructure development. North America and the Asia-Pacific regions are projected to dominate the market, driven by substantial investments in energy infrastructure projects. However, stringent environmental regulations and fluctuating oil and gas prices pose significant challenges to market growth.

Despite these challenges, the market's future looks promising. Technological advancements in pipeline construction techniques, including the utilization of robotics and automation for enhanced efficiency and safety, are expected to drive further growth. Moreover, increasing focus on pipeline integrity management and safety standards will necessitate substantial investment in pipeline maintenance and repair, thus supporting market expansion. The rise of renewable energy sources, although presenting some challenges in the short term, could eventually contribute to the market's long-term growth, as pipelines may still play a role in transporting biofuels and hydrogen. Competition within the industry is fierce, with numerous major players and smaller specialized contractors vying for market share. Strategic mergers and acquisitions, coupled with a focus on technological innovation, are key survival strategies for companies in this dynamic market. Companies are also focusing on sustainability initiatives, aligning with global climate goals.

The global pipeline construction services market exhibited robust growth during the historical period (2019-2024), reaching an estimated value of $XXX million in 2024. This growth is projected to continue throughout the forecast period (2025-2033), driven by increasing global energy demand, particularly in developing economies. The market is characterized by a diverse range of services, including oil and gas facility construction, pipeline installation and maintenance, and specialized services like directional drilling and pipeline integrity management. The Oil & Gas application segment continues to be the dominant driver, fueled by ongoing exploration and production activities worldwide. However, increasing investments in water infrastructure projects are also creating significant opportunities for pipeline construction companies in the water treatment application segment. The Design/Build service model is gaining traction as clients seek streamlined project delivery and reduced risk. This trend is particularly evident in larger-scale projects where integrated design and construction capabilities offer significant cost and time advantages. Technological advancements, such as the use of advanced materials and data analytics for predictive maintenance, are further transforming the industry, enhancing efficiency and reducing operational costs. Competition within the market is intense, with a mix of large multinational corporations and smaller specialized contractors vying for projects. The consolidation trend, involving mergers and acquisitions, is expected to continue as companies seek to expand their geographic reach and service offerings. The market is also witnessing a shift toward sustainable practices, with an increasing focus on reducing the environmental impact of pipeline construction and operation. This is leading to the adoption of environmentally friendly construction techniques and materials. Overall, the pipeline construction services market is poised for significant growth in the coming years, driven by a confluence of factors including rising energy demand, infrastructure development, and technological innovation. The estimated market value for 2025 is projected to be $XXX million, indicating substantial growth compared to previous years.

Several key factors are driving the expansion of the pipeline construction services market. Firstly, the ever-increasing global demand for energy, especially oil and gas, is a primary catalyst. To meet this demand, extensive pipeline infrastructure development is required, creating a substantial need for construction, maintenance, and integrity services. Secondly, the growing focus on energy security and diversification across nations is bolstering investment in pipeline projects. Governments are prioritizing the development of robust and reliable energy transportation networks to enhance energy independence and reduce reliance on volatile global markets. Thirdly, the shift towards cleaner energy sources, while presenting challenges, also presents opportunities. The construction of pipelines for transporting renewable fuels like biofuels and hydrogen is emerging as a significant segment within the market. Furthermore, the aging pipeline infrastructure in many developed countries necessitates significant investment in maintenance, repair, and replacement, further contributing to market growth. This includes upgrading existing systems to meet stricter safety and environmental regulations. Lastly, technological advancements in pipeline construction techniques, materials, and inspection methods are improving efficiency, reducing costs, and enhancing safety, making pipeline projects more attractive and feasible. These technological improvements range from advanced directional drilling techniques to the utilization of robotics and drones for inspection and maintenance.

Despite the significant growth potential, the pipeline construction services market faces several challenges and restraints. Firstly, the volatility of commodity prices, particularly for oil and gas, can significantly impact investment decisions and project timelines. Fluctuations in energy prices can lead to delays or cancellations of projects, hindering market growth. Secondly, stringent environmental regulations and the need for robust environmental impact assessments can increase the complexity and cost of pipeline projects. Obtaining necessary permits and approvals can be a lengthy and challenging process, delaying project implementation. Thirdly, the risk of pipeline accidents and leaks poses a significant threat to the industry's reputation and can lead to substantial financial losses and environmental damage. This necessitates continuous investment in safety measures and rigorous quality control throughout the project lifecycle. Furthermore, skilled labor shortages in specialized areas like welding and directional drilling are hindering the efficient execution of projects. Competition for qualified personnel is intense, driving up labor costs and potentially delaying project completion. Lastly, geopolitical instability and conflicts in certain regions can disrupt projects and hinder access to resources, adding uncertainty to the market outlook.

The Oil & Gas application segment is expected to dominate the market throughout the forecast period. Driven by the continued global demand for energy and ongoing exploration and production activities, this segment represents a significant share of the overall market value. Within the oil and gas sector, the Pipeline Installation and Maintenance type of service is predicted to be a key growth driver, owing to the extensive network of existing pipelines requiring regular maintenance and upgrades. The large-scale projects inherent in this segment contribute substantially to the market revenue.

North America: This region is expected to maintain a significant market share due to extensive existing pipeline infrastructure and ongoing investments in energy exploration and production, particularly in the shale gas sector. The robust regulatory framework and established industry presence also contribute to this region’s dominance.

Middle East & Africa: This region boasts substantial oil and gas reserves and is undergoing massive infrastructure development, creating significant growth opportunities for pipeline construction services. Large-scale projects, often involving international collaborations, are driving growth within this region.

Asia-Pacific: Rapid industrialization and urbanization across many Asian countries are fueling increasing energy demand, making this region an attractive market for pipeline construction. Growth here is further spurred by government initiatives promoting energy security and infrastructure development.

Within the Type segment:

Oil and Gas Facility Construction: This will remain a significant segment due to the ongoing need for new processing facilities and expansion of existing ones to meet growing energy demands.

Design/Build Services: This integrated approach streamlines project delivery and minimizes risk, making it increasingly attractive to clients and boosting market demand.

Pipeline Integrity Services: The increasing focus on pipeline safety and the need for regular inspection and maintenance to prevent leaks and accidents will continue to drive demand in this segment.

The substantial investments in pipeline infrastructure, coupled with the aforementioned growth drivers in specific regions and segments, ensure a promising outlook for the pipeline construction services market.

Several factors are catalyzing growth in the pipeline construction services industry. The escalating global energy demand is a major driver, pushing the need for enhanced pipeline infrastructure to transport oil, gas, and potentially renewable fuels. Simultaneously, the aging pipeline networks in developed nations necessitate extensive maintenance, repair, and replacement, further fueling industry expansion. Technological advancements, encompassing superior materials, sophisticated construction techniques, and data-driven predictive maintenance, significantly enhance efficiency and reduce operational costs. Moreover, government initiatives promoting energy security and infrastructure development in several regions are stimulating investments in pipeline projects, creating substantial opportunities for service providers. Finally, the increasing adoption of design-build services streamlines projects and mitigates risks, boosting market appeal.

(Note: I do not have access to real-time information, including website URLs. Therefore, I cannot provide hyperlinks to company websites.)

(Note: These are example developments. Specific significant developments would require access to real-time industry news and reports.)

This report offers a detailed analysis of the pipeline construction services market, encompassing historical data, current market trends, and future projections. It provides valuable insights into market drivers, challenges, and growth opportunities. The report covers key segments, geographical regions, and leading players in the industry, offering a comprehensive understanding of the market dynamics and competitive landscape. Key findings include projections of substantial market growth driven by global energy demand, technological advancements, and increased investment in pipeline infrastructure. The report also highlights challenges such as regulatory hurdles, environmental concerns, and competition for skilled labor. In short, this report serves as a valuable resource for stakeholders looking to navigate the evolving landscape of the pipeline construction services market and make informed business decisions.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.4%.

Key companies in the market include STI Group, PLH Group, Pipeline, Inc., PCS, Beltps, Pipeworx, Snelson, Topline, White Horse Contractors, Sunland Construction, MPG Pipeline Contractors, Bobcat Contracting, United Piping, Jones Contractors, TLC Pipeline Construction, Energy Services South, Pipeline and Construction Supplies ltd, Pipeline Construction & Maintenance, Inc., Obmac Field Service Ltd, American Pipeline Construction LLC, Michels Corporation, Mid America Pipeline Construction Inc., Jomax Construction Company, Driver Pipeline, U.S. Pipeline, .

The market segments include Type, Application.

The market size is estimated to be USD 52.5 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Pipeline Construction Services," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pipeline Construction Services, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.