1. What is the projected Compound Annual Growth Rate (CAGR) of the Pipe Lining & Coating Service?

The projected CAGR is approximately 6.14%.

Pipe Lining & Coating Service

Pipe Lining & Coating ServicePipe Lining & Coating Service by Type (Surface Preparation, Pipe Lining), by Application (Large Enterprises, Small and Medium-sized Enterprises (SMEs)), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global pipe lining and coating services market is poised for significant expansion, propelled by escalating investments in essential infrastructure, notably water and gas transmission pipelines. The imperative to upgrade and replace aging pipeline networks is generating substantial demand for effective and resilient lining and coating solutions. Concurrently, stringent environmental regulations designed to mitigate pipeline leaks and corrosion are accelerating the adoption of sophisticated coating technologies. The market is bifurcated by application, catering to both large enterprises and SMEs, and by surface preparation type, addressing diverse industry requirements and project scales. Major pipeline initiatives undertaken by large enterprises are key contributors to the market's overall value. Regional market share distribution is primarily dictated by infrastructure development priorities. North America and Europe currently dominate due to their extensive established pipeline systems and ongoing modernization efforts. However, accelerated industrialization and urbanization across Asia-Pacific present substantial growth prospects, fostering increased investment in new pipeline construction and maintenance. The market landscape is characterized by intense competition, with numerous entities offering a spectrum of services and technologies. Strategic focus on material and technique innovation aims to enhance pipeline coating durability and performance, further stimulating market growth. Consequently, the outlook for the pipe lining and coating services market remains exceptionally positive, projecting sustained expansion throughout the forecast period.

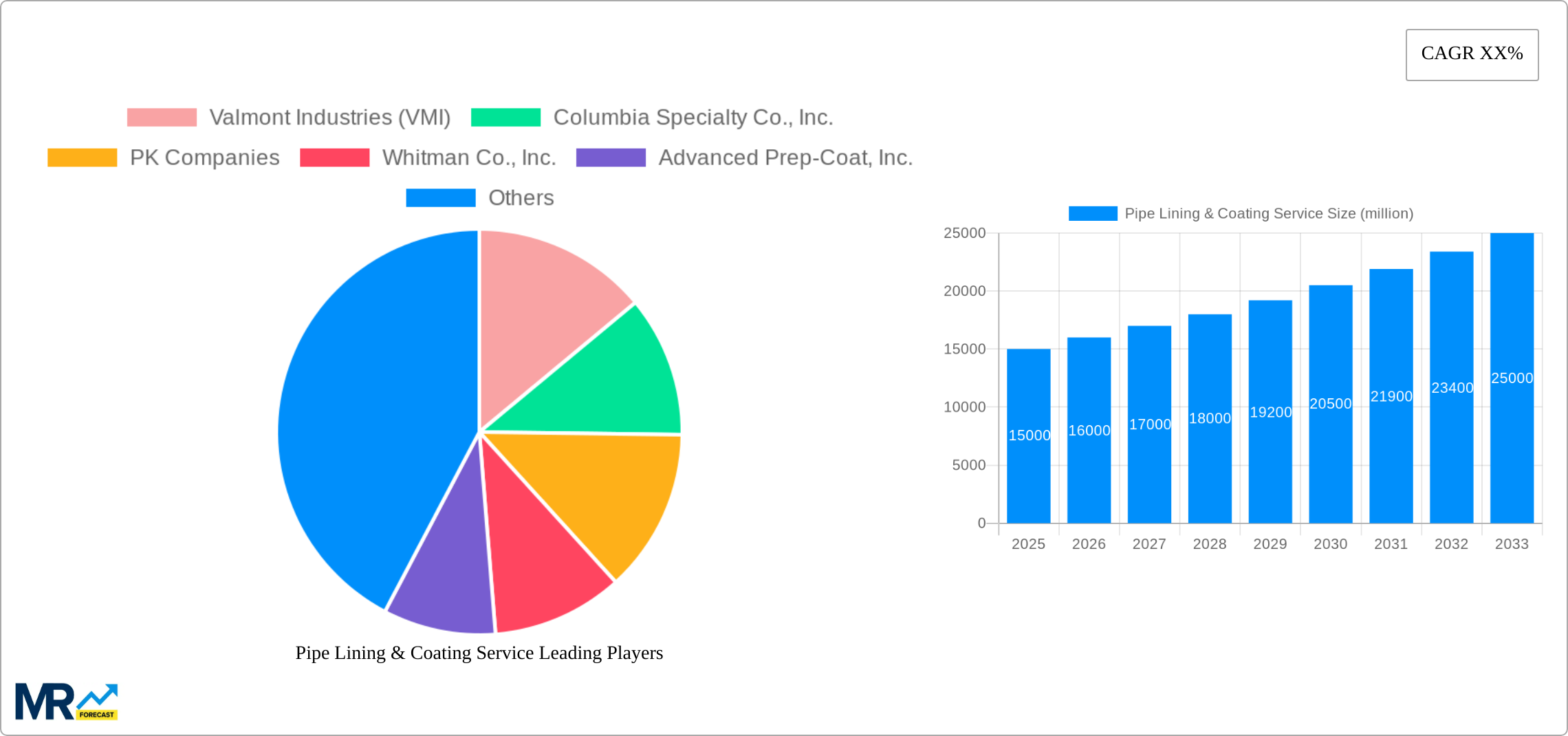

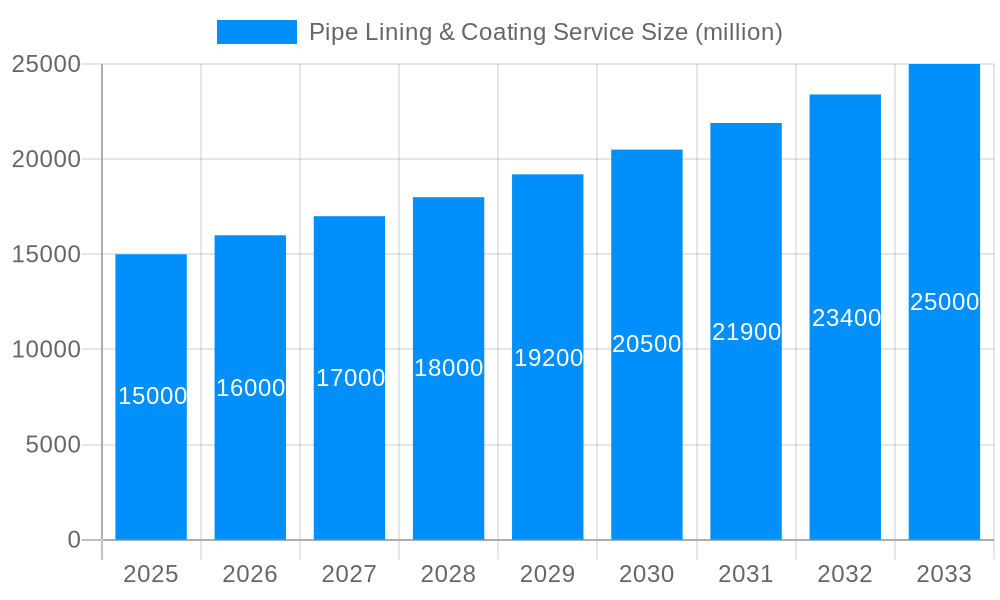

The compound annual growth rate (CAGR) for the pipe lining and coating services market is estimated at 6.14%. This projection is derived from current industry trajectories and covers the forecast period from 2024 to 2033. Key growth drivers include ongoing infrastructure development, the critical need for aging pipeline rehabilitation, and increasingly rigorous environmental regulations. Growth patterns are anticipated to vary geographically, with higher expansion rates in regions undertaking significant infrastructure projects. Market consolidation through strategic acquisitions and expansions by leading players is expected, while smaller firms may concentrate on specialized applications or advanced coating technologies to maintain a competitive edge. Pricing dynamics will be influenced by material and labor costs, alongside technological advancements. Future market expansion hinges on sustained infrastructure investment, the advent of innovative coating technologies, and the stringency of governmental regulations pertaining to pipeline safety and environmental protection. The current market size is valued at $2.1 billion in the base year 2024.

The global pipe lining and coating service market is experiencing robust growth, projected to reach several billion USD by 2033. This expansion is driven by a confluence of factors, including the increasing need for infrastructure upgrades across various sectors—water management, oil and gas, and chemical processing—the growing demand for corrosion prevention and extending the lifespan of existing pipelines, and stringent environmental regulations pushing for minimized leakage and environmentally friendly solutions. The market is witnessing a significant shift towards advanced coating technologies, including fusion-bonded epoxy (FBE) coatings and internal pipe lining techniques like cured-in-place pipe (CIPP) lining. These advanced solutions offer superior corrosion resistance, improved durability, and enhanced operational efficiency, contributing to the market's overall expansion. The demand for pipe lining and coating services is particularly high in regions undergoing rapid industrialization and infrastructure development, as these regions require extensive pipeline networks to support their economic activities. Furthermore, the rising adoption of smart pipelines incorporating advanced sensors and monitoring technologies is increasing the demand for specialized coating and lining services to ensure the integrity and efficiency of these systems. The historical period (2019-2024) shows steady growth, with the base year (2025) exhibiting a significant upswing. The forecast period (2025-2033) anticipates continued expansion, driven by the factors mentioned above, particularly within the large enterprise sector. The market demonstrates a balanced distribution across surface preparation, pipe lining, and application segments, with a significant emphasis on the large enterprise sector due to their extensive pipeline networks and greater budget allocations for maintenance and upgrades.

Several key factors are accelerating the growth of the pipe lining and coating service market. The aging infrastructure in many developed and developing nations necessitates significant investment in pipeline rehabilitation and replacement. This demand is further fueled by increasingly stringent environmental regulations aimed at minimizing pipeline leaks and associated environmental damage, leading to greater adoption of preventative maintenance strategies. The rising cost of pipeline replacement compared to the cost-effectiveness of lining and coating solutions is another major driver. Moreover, the expanding oil and gas, chemical, and water management industries, coupled with the growth of renewable energy sources requiring new pipeline infrastructure, are further bolstering market growth. Technological advancements in coating materials and application techniques, resulting in improved durability, corrosion resistance, and longevity of pipelines, are also contributing factors. Finally, the increasing awareness among stakeholders regarding the long-term cost benefits of preventative maintenance and pipeline rehabilitation compared to emergency repairs further accelerates market growth.

Despite the significant growth potential, the pipe lining and coating service market faces several challenges. The highly specialized nature of the work requires skilled labor, leading to potential labor shortages and increased labor costs. The fluctuating prices of raw materials used in coating and lining materials, coupled with economic uncertainties, can impact project profitability and market growth. Furthermore, the inherent risks associated with working in challenging environments, such as underground pipelines or hazardous industrial settings, can pose safety concerns and necessitate stringent safety protocols, adding to operational costs. Competition from alternative pipeline rehabilitation techniques, such as pipeline replacement, can also limit market growth. Finally, accessing remote or geographically challenging pipeline locations can increase logistical complexity and costs, affecting project timelines and overall profitability. These challenges necessitate innovative solutions, skilled workforce development, and efficient project management strategies to ensure the sustained growth of the market.

The large enterprise segment is expected to dominate the market due to their larger budgets and extensive pipeline networks requiring regular maintenance and upgrades. This sector's demand for advanced coating technologies and specialized services contributes significantly to overall market revenue.

Large Enterprises: Possess the financial resources to invest in advanced technologies and large-scale projects. Their extensive pipeline networks necessitate consistent maintenance and rehabilitation, driving higher demand for pipe lining and coating services. This sector's focus on minimizing downtime and ensuring operational efficiency fuels the adoption of high-performance coatings and lining solutions.

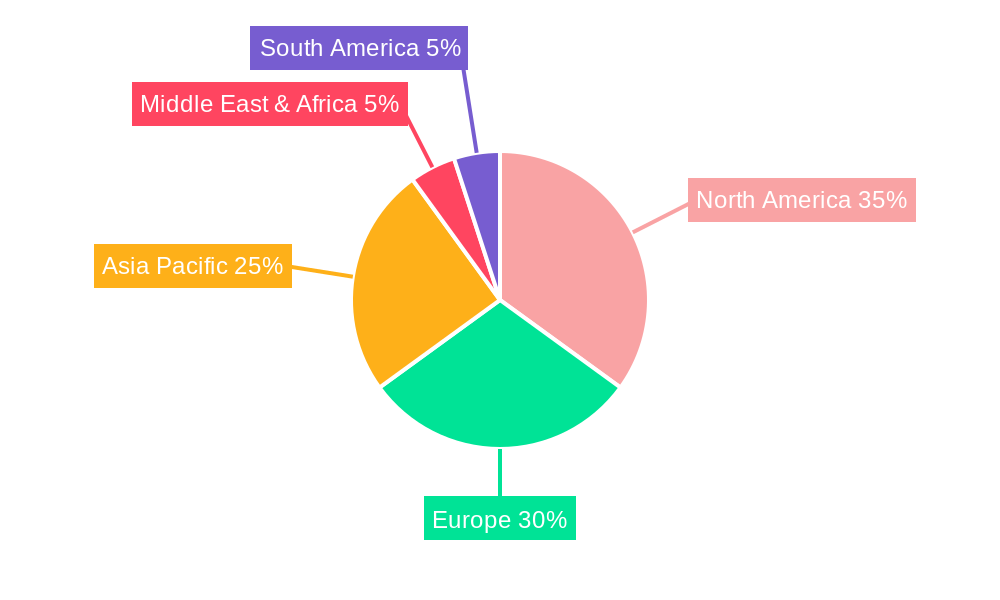

Geographic Dominance: North America and Europe currently hold significant market share, driven by substantial investments in infrastructure upgrades, stringent environmental regulations, and a robust presence of major players in the pipe lining and coating industry. However, regions with rapid industrialization and expanding infrastructure projects, such as parts of Asia and the Middle East, are projected to show the highest growth rates in the coming years.

Surface Preparation Segment: This segment is crucial for ensuring the long-term success of pipe lining and coating projects. Thorough surface preparation significantly impacts the adhesion and performance of the applied coatings. The increasing demand for advanced preparation techniques ensures optimal surface conditions before coating application and extends the lifespan of the pipeline.

The combination of the large enterprise sector's financial capacity and the crucial role of proper surface preparation contributes to their prominent position within the market. The growth of the overall market will be largely dependent on the continued investment in infrastructure and expansion of industrial activity in these key regions and segments.

The pipe lining and coating service industry is experiencing accelerated growth due to several catalysts. The increasing focus on infrastructure development and renewal across the globe creates a significant demand for pipeline rehabilitation and new installations. Stringent environmental regulations emphasizing leak prevention and sustainable practices are driving the adoption of advanced coating solutions. Technological advancements in coating materials and application techniques improve the durability, lifespan, and performance of pipelines.

This report provides a comprehensive analysis of the pipe lining and coating service market, offering insights into market trends, drivers, challenges, key players, and future growth prospects. The report's detailed segmentation analysis allows for a granular understanding of market dynamics within key regions, application areas, and service types. This detailed information enables businesses to make informed decisions regarding investment strategies, market entry, and product development. The forecast period projections offer valuable insights into the expected growth trajectory of the market, empowering stakeholders to plan for future opportunities and challenges.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.14% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.14%.

Key companies in the market include Valmont Industries (VMI), Columbia Specialty Co., Inc., PK Companies, Whitman Co., Inc., Advanced Prep-Coat, Inc., Browns Hill Sand, Lambert Jones Rubber Co., OPC Liquid Coating Co., Abbey Metal Services, Inc., Our Powder Coating, Great Lakes Maintenance Co., Inc., Allied Powder Coating, Inc., PEP, A Ryan Herco Flow Solutions Company, Blastco Industrial Services Group, Precision Industrial Coatings, Inc., .

The market segments include Type, Application.

The market size is estimated to be USD 2.1 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Pipe Lining & Coating Service," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pipe Lining & Coating Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.