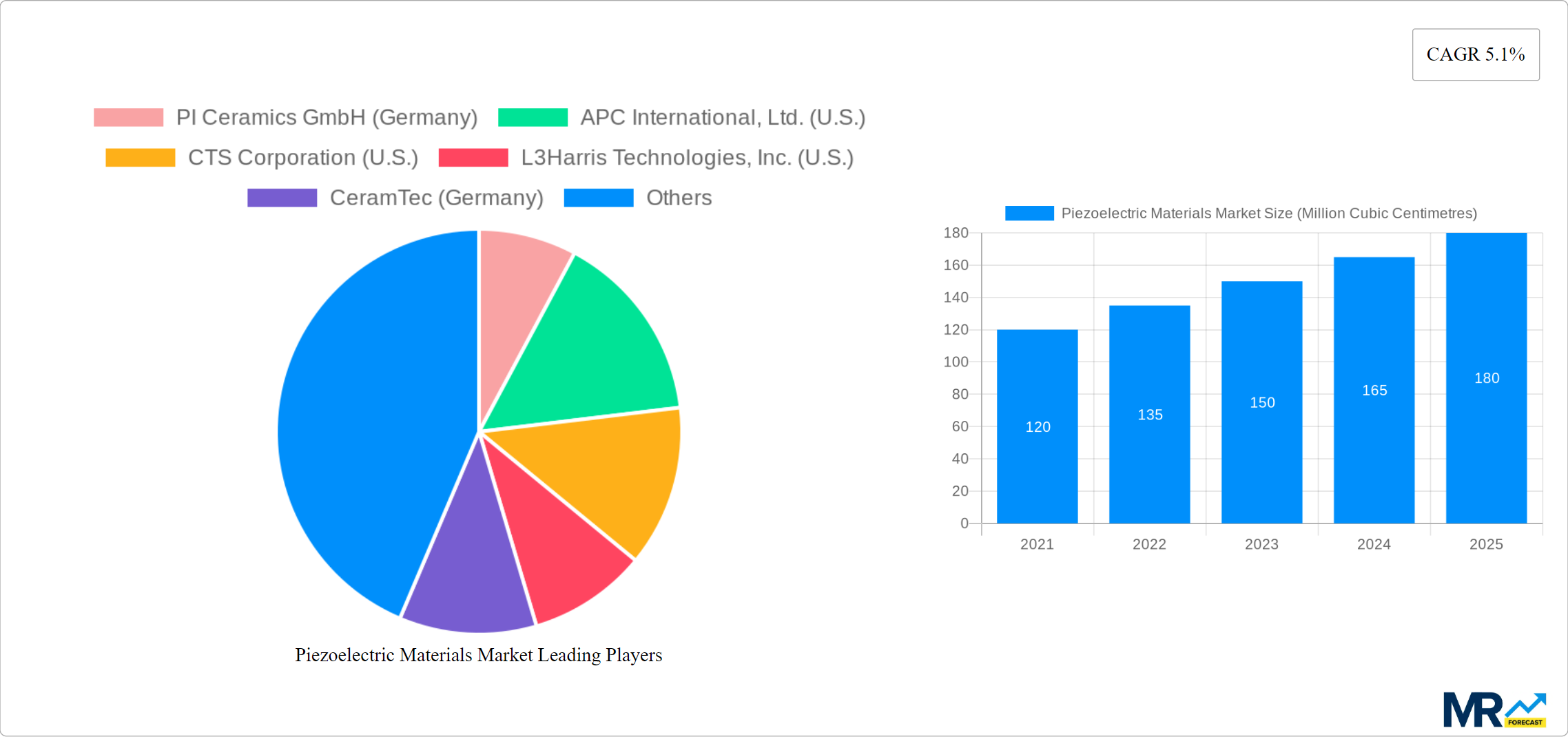

1. What is the projected Compound Annual Growth Rate (CAGR) of the Piezoelectric Materials Market?

The projected CAGR is approximately 5.1%.

Piezoelectric Materials Market

Piezoelectric Materials MarketPiezoelectric Materials Market by Material (Piezoceramics [Lead Zirconate Titanate {PZT}, Lead-free Ceramics], Piezopolymers, Piezocomposites, Others), by Application (Actuators, Motors, Transducers, Sensors, SONAR, Generators & Transformers, Acoustic Devices, Resonators, Others), by End-Use Industry (Automotive, Healthcare, IT & Telecom, Consumer Goods, Aerospace & Defense, Others), by By Geography (North America) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

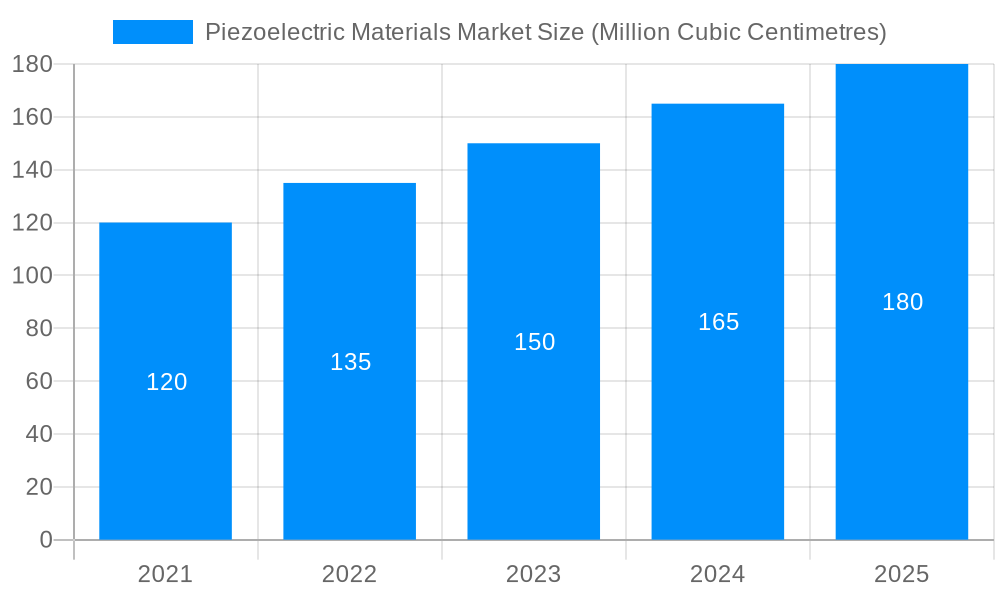

The Piezoelectric Materials Marketsize was valued at USD 1.31 Million Cubic Centimetres in 2023 and is projected to reach USD 1.86 Million Cubic Centimetres by 2032, exhibiting a CAGR of 5.1 % during the forecast period.Piezoelectric materials are the unacknowledged achievers of the modern technical era, capturing mechanical power through electrical energy and in reverse. These unique materials exhibit a remarkable property: when exposed to mechanical stress, they actually produce electric charge, and on the other hand, they compress under a kind of electric field. Piezoelectric materials are presented in the field of precision engineering, where their capacity to exactly control motions is a life provision. From the simple but necessary daily installations to the highly professional research ones, the materials still continue to lead by exploring new ideas, showing how they have an essential place in our information age.

Material

Application

End-Use Industry

Regional Insight

Consumer Side Analysis

Demand Side Analysis

Import And Export Analysis

Pricing Strategies

Segmentation

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.1%.

Key companies in the market include PI Ceramics GmbH (Germany), APC International, Ltd. (U.S.), CTS Corporation (U.S.), L3Harris Technologies, Inc. (U.S.), CeramTec (Germany), Arkema (France), Solvay (Belgium), Mad City Labs, Inc. (U.S.), Piezosystem jena GmbH (Germany).

The market segments include Material, Application, End-Use Industry.

The market size is estimated to be USD 1.31 USD Billion as of 2022.

Shifting Demand from Plywood to Medium Density Fiberboard Can Foster Market Growth.

N/A

Lack of Differentiation between Signals and Noise to Diminish the Adoption of Piezoelectric Materials.

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4850, USD 5850, and USD 6850 respectively.

The market size is provided in terms of value, measured in USD Billion and volume, measured in K Tons .

Yes, the market keyword associated with the report is "Piezoelectric Materials Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Piezoelectric Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.