1. What is the projected Compound Annual Growth Rate (CAGR) of the Photovoltaic Module Materials?

The projected CAGR is approximately 7.2%.

Photovoltaic Module Materials

Photovoltaic Module MaterialsPhotovoltaic Module Materials by Type (Monocrystalline Silicon, Polysilicon), by Application (Ground Photovoltaic Power Station, Offshore Photovoltaic Power Station, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

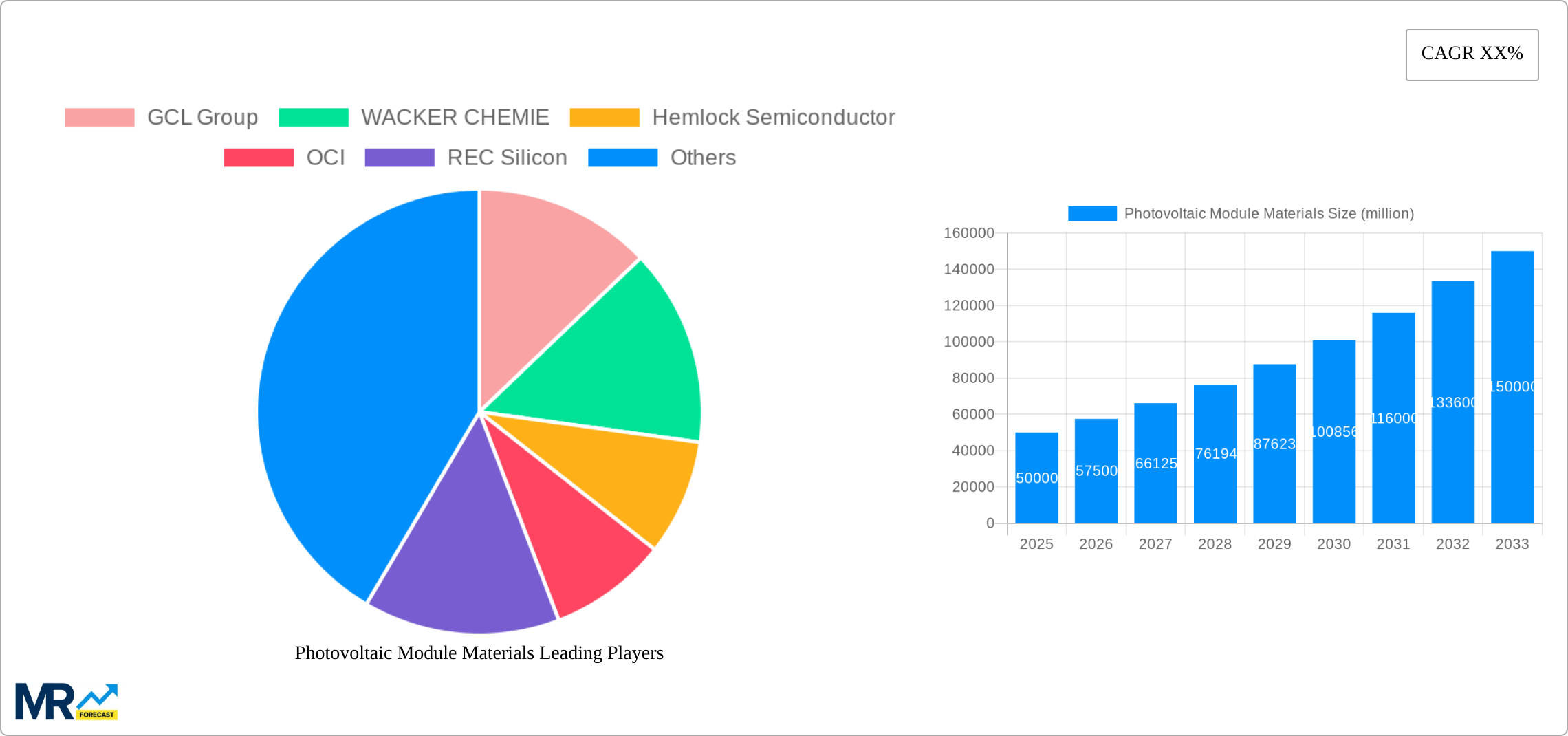

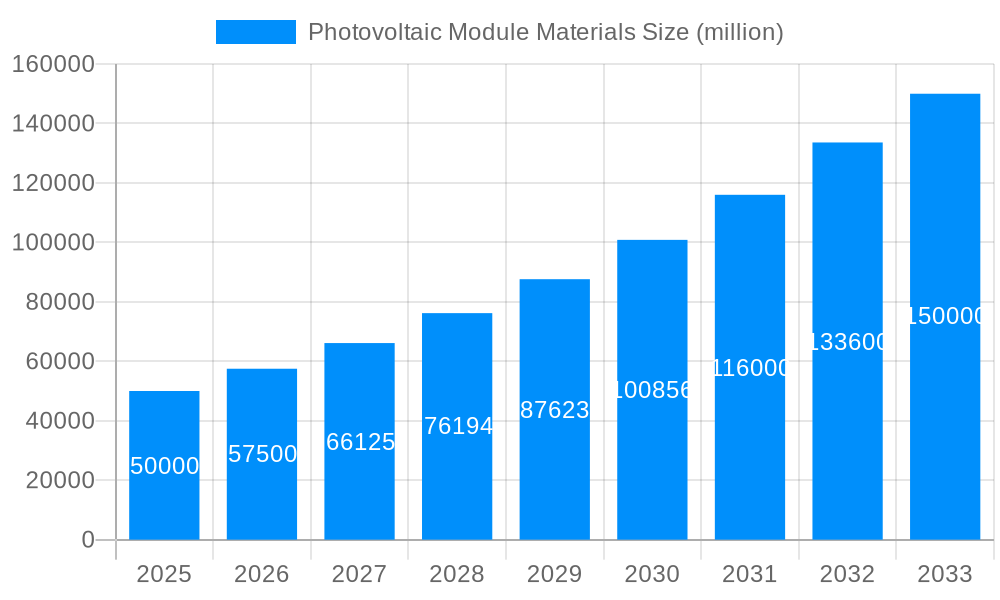

The global photovoltaic (PV) module materials market is poised for significant expansion, driven by the accelerating adoption of renewable energy and supportive governmental frameworks. The market, valued at $361.5 billion in 2025, is projected to grow at a compound annual growth rate (CAGR) of 7.2% from 2025 to 2033, reaching substantial market value by 2033. This growth trajectory is underpinned by key drivers, including the decreasing cost of solar technology, making it a highly competitive energy alternative. Growing global concern for climate change and carbon emission reduction is spurring significant investments in renewable energy infrastructure, directly impacting the demand for PV modules and their essential materials. Furthermore, advancements in monocrystalline silicon and polysilicon production technologies are enhancing efficiency and reducing manufacturing expenses, thereby catalyzing market growth. However, the market is subject to challenges such as raw material price volatility and potential supply chain disruptions. Geographically, Asia-Pacific, led by China, currently dominates market share due to its extensive manufacturing capabilities and large-scale solar projects. North America and Europe present considerable growth opportunities, fueled by increasing governmental incentives and private sector investments. Market segmentation indicates a strong preference for monocrystalline silicon due to its superior efficiency, though polysilicon remains a significant segment due to its cost-effectiveness. Ground-mounted solar power stations represent the largest application, with offshore and niche applications demonstrating promising upward trends.

The competitive landscape features a blend of large multinational corporations and specialized manufacturers. Key industry participants are actively engaged in research and development to enhance PV technology's efficiency, durability, and cost-effectiveness. Strategic initiatives such as vertical integration, strategic alliances, and geographic expansion are crucial for sustained success in this dynamic and competitive market. Future market expansion will be contingent upon continued cost reductions in PV technology, advancements in energy storage solutions to mitigate solar power's intermittency, and sustained governmental support for renewable energy initiatives.

The global photovoltaic (PV) module materials market exhibited robust growth throughout the historical period (2019-2024), driven by the increasing demand for renewable energy sources and supportive government policies worldwide. The market size, valued at several billion USD in 2024, is projected to experience exponential growth, reaching tens of billions of USD by 2033. This surge is primarily attributed to the decreasing cost of PV modules, technological advancements leading to higher efficiency, and the growing awareness of climate change. Monocrystalline silicon continues to dominate the market due to its superior efficiency compared to polycrystalline silicon. However, polycrystalline silicon maintains a significant market share due to its lower cost. The application landscape is dominated by ground-based photovoltaic power stations, but the offshore photovoltaic sector shows promising growth potential, fueled by advancements in floating PV technology. Major players in the market are constantly innovating to improve material quality, reduce manufacturing costs, and enhance module efficiency, creating a dynamic and competitive environment. The forecast period (2025-2033) anticipates continued expansion, with significant growth expected in emerging economies and regions with favorable solar irradiance levels. The estimated market value in 2025 surpasses several billion USD, signifying a substantial jump from previous years and setting the stage for an even more expansive future market. The consumption value of photovoltaic module materials will likely surpass tens of billions of USD by 2033, reflecting an impressive Compound Annual Growth Rate (CAGR). This growth is driven by technological breakthroughs in materials science and manufacturing, resulting in more efficient and cost-effective solar panels. This report offers comprehensive market insights covering various aspects of this sector, providing valuable data for stakeholders and investors.

Several key factors propel the growth of the photovoltaic module materials market. Firstly, the urgent need to transition to cleaner energy sources to mitigate climate change is a significant driver. Governments worldwide are enacting supportive policies, including subsidies, tax incentives, and renewable energy mandates, to accelerate the adoption of solar energy. Secondly, the declining cost of PV modules has made solar energy increasingly competitive with traditional fossil fuel-based electricity generation. Continuous technological advancements in silicon manufacturing and module design have significantly improved efficiency and reduced production costs. Thirdly, the increasing awareness among consumers and businesses about the environmental and economic benefits of solar energy is fueling demand. The falling price of solar energy makes it a viable and attractive option for both residential and commercial applications. Finally, the growing deployment of large-scale solar power plants, both on land and offshore, is creating a massive demand for PV module materials. This large-scale deployment is further driven by the increasing need for reliable and sustainable energy sources in both developed and developing countries, fostering market growth across multiple geographical areas.

Despite the positive growth trajectory, several challenges and restraints hinder the market's progress. The fluctuating prices of raw materials, such as silicon, can impact the overall cost of PV module production, creating uncertainty for manufacturers. The complex and geographically dispersed supply chain for raw materials and manufacturing poses logistical challenges and increases vulnerability to disruptions. Furthermore, the environmental impact of silicon production, including energy consumption and waste generation, is a growing concern. Stricter environmental regulations and increasing scrutiny on the environmental footprint of manufacturing processes pose challenges that manufacturers must address. Technological advancements in competing energy technologies, such as wind energy and other renewables, also create competition for investment and market share. The disposal and recycling of end-of-life PV modules is another challenge that requires effective solutions to prevent environmental pollution. Addressing these issues is crucial for sustainable and responsible growth of the photovoltaic module materials market.

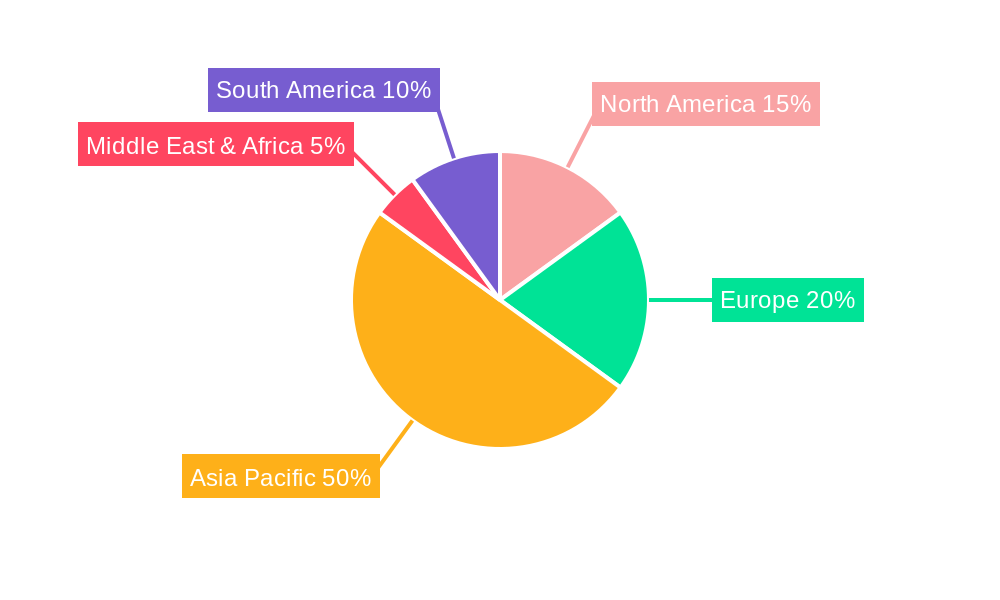

The Asia-Pacific region, particularly China, is currently the dominant market for photovoltaic module materials, accounting for a significant portion of global production and consumption. This dominance is due to the large-scale deployment of solar power projects, supportive government policies, and a robust manufacturing base in the region. However, other regions like Europe and North America are also exhibiting strong growth, driven by increasing renewable energy targets and environmental regulations.

Dominant Segment: Monocrystalline Silicon

Monocrystalline silicon dominates the PV module materials market due to its superior efficiency compared to polycrystalline silicon. This higher efficiency translates to more power generation per unit area, making it the preferred choice for many applications. Despite a higher cost compared to polycrystalline silicon, the ongoing advancements in manufacturing technologies are gradually narrowing the price gap, further solidifying its dominance in the market. The demand for monocrystalline silicon is projected to increase significantly over the forecast period, driven by the global shift towards higher-efficiency PV modules. This segment's growth is anticipated to significantly contribute to the overall expansion of the photovoltaic module materials market.

Dominant Application: Ground Photovoltaic Power Stations

Ground-mounted photovoltaic power stations represent the largest application segment, accounting for a significant majority of global photovoltaic module consumption. Large-scale solar farms and ground-mounted systems are being installed across various regions, including both developed and developing countries. The continued expansion of utility-scale solar projects is anticipated to sustain the dominance of this segment throughout the forecast period.

The PV module materials industry is experiencing significant growth propelled by several key catalysts. Falling manufacturing costs coupled with increased efficiency in solar panel technology are making solar energy increasingly affordable and competitive. Government policies and incentives globally are promoting the adoption of renewable energy sources, directly driving market demand. Furthermore, heightened awareness about climate change and the need for sustainable energy solutions are further stimulating market growth and adoption among both individuals and corporations. These factors collectively contribute to a positive outlook for the industry's continued expansion.

This report provides a comprehensive overview of the photovoltaic module materials market, encompassing historical data, current market trends, and future projections. It offers detailed analysis of market segments, key players, driving factors, challenges, and regional dynamics. The report's insights and forecasts provide valuable guidance for stakeholders involved in this rapidly evolving industry, enabling informed decision-making and strategic planning.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.2%.

Key companies in the market include GCL Group, WACKER CHEMIE, Hemlock Semiconductor, OCI, REC Silicon, TBEA, SunEdision, Sichuan Yongxiang, KCC, Tokuyama, Bosch Solar Energy, Frontier Solar, Jinko Solar, Toledo Solar, Reel Solar.

The market segments include Type, Application.

The market size is estimated to be USD 361.5 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Photovoltaic Module Materials," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Photovoltaic Module Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.