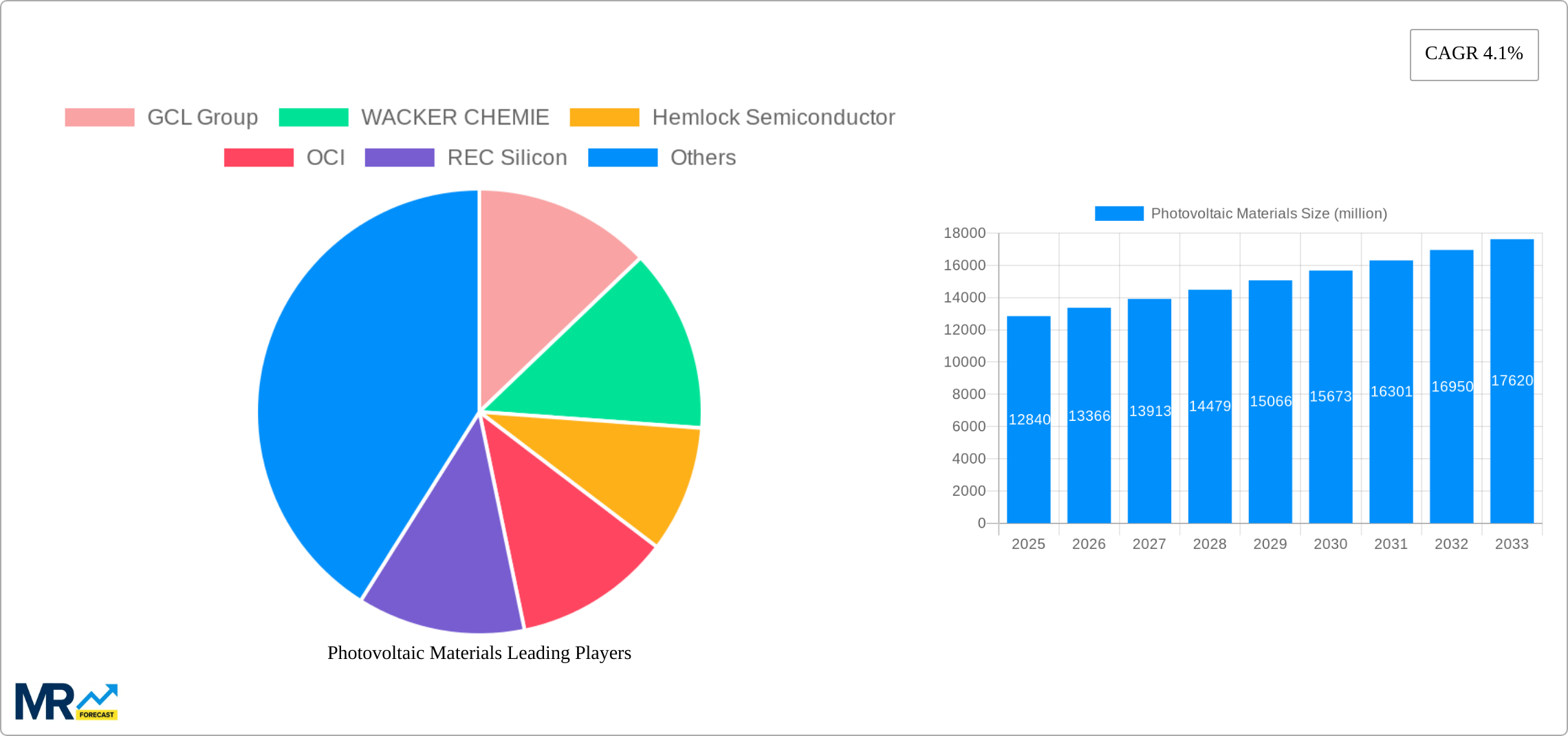

1. What is the projected Compound Annual Growth Rate (CAGR) of the Photovoltaic Materials?

The projected CAGR is approximately 4.1%.

Photovoltaic Materials

Photovoltaic MaterialsPhotovoltaic Materials by Type (Crystalline Materials, Thin Film, Others), by Application (Utility, Commercial, Residential), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

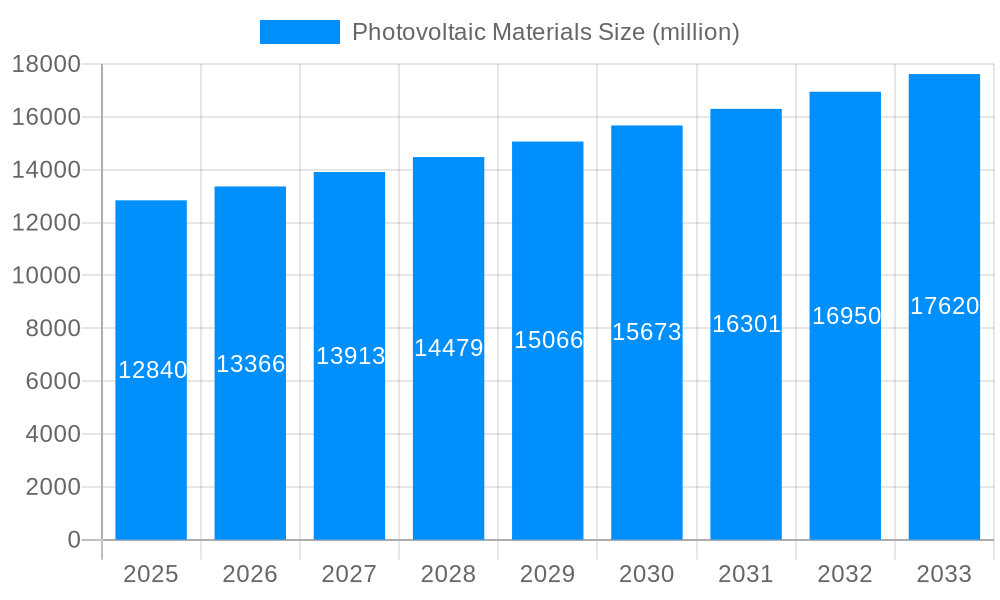

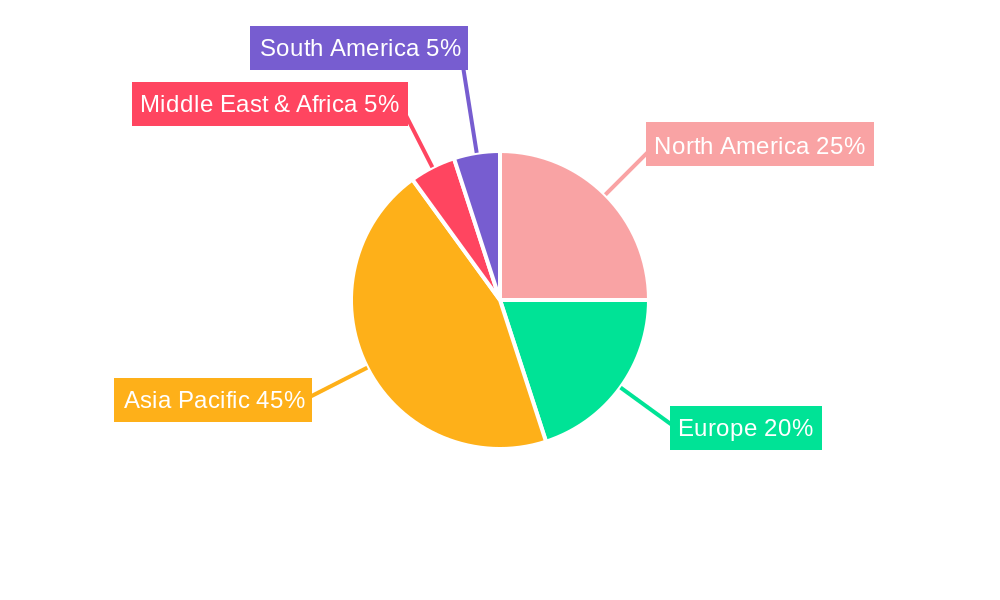

The photovoltaic (PV) materials market, currently valued at $12.84 billion (2025), is projected to experience robust growth, driven by the increasing global demand for renewable energy and supportive government policies promoting solar energy adoption. A compound annual growth rate (CAGR) of 4.1% from 2025 to 2033 suggests a substantial market expansion, reaching an estimated value exceeding $18 billion by 2033. Key growth drivers include the decreasing cost of PV modules, advancements in solar cell technology leading to higher efficiency rates, and a growing awareness of climate change, fueling investments in sustainable energy solutions. The market segmentation reveals a significant share held by crystalline silicon materials due to their established technology and cost-effectiveness. However, thin-film technologies are gaining traction owing to their flexibility and potential for cost reduction in the long run. The application segment is dominated by the utility-scale sector, followed by commercial and residential sectors, reflecting the large-scale deployment of solar farms alongside the increasing adoption of rooftop solar panels. Geographic growth is expected to be diverse, with regions like Asia Pacific, particularly China and India, leading the expansion due to their vast solar energy potential and substantial government investments. North America and Europe will also contribute significantly, driven by strong policy support and increasing environmental awareness. Competitive pressures are high, with numerous established players and emerging companies vying for market share. The ongoing technological innovations and economies of scale will continue to shape the competitive landscape.

The market’s continued growth relies on overcoming challenges such as the intermittent nature of solar energy, the need for efficient energy storage solutions, and the potential environmental impacts associated with the manufacturing process. Addressing these challenges through research and development of advanced materials, improved energy storage technologies, and sustainable manufacturing practices will be crucial to ensuring the long-term sustainability and growth of the PV materials market. The increasing demand for decentralized energy generation and the integration of smart grids will further propel market growth. Continuous advancements in materials science and manufacturing processes are expected to further decrease production costs, ultimately making solar energy more accessible and affordable for a broader range of consumers and businesses worldwide. This will contribute to a larger market size and a higher rate of adoption across all segments and regions.

The photovoltaic (PV) materials market is experiencing a period of robust growth, driven by the global push towards renewable energy sources and decreasing PV system costs. Between 2019 and 2024, the market witnessed significant expansion, with the production of crystalline silicon materials exceeding several million tons annually. This trend is expected to continue throughout the forecast period (2025-2033), fueled by increasing demand from utility-scale solar projects and government incentives promoting solar energy adoption. By 2033, the market is projected to reach multi-billion-dollar valuations, surpassing previous estimates due to technological advancements leading to higher efficiency and lower production costs. The shift towards larger-scale solar farms, coupled with the decreasing costs of solar panels, makes solar energy a financially viable option for businesses and residential consumers alike. This has created a positive feedback loop, where increased demand triggers further innovation and cost reductions, reinforcing the market's upward trajectory. While the crystalline silicon segment maintains its dominance, the thin-film segment is also witnessing growth, though at a slower pace, driven by its flexibility and potential for low-cost manufacturing. Innovation in materials science continues to push the boundaries of efficiency, paving the way for more cost-effective and higher-performing solar cells. The market is also seeing a rise in the use of innovative PV materials beyond traditional silicon, although they represent a smaller proportion of the overall market at present. The competition among key players is intense, with ongoing efforts to improve manufacturing processes, enhance product quality, and expand market share. This competitive landscape is driving continuous improvements in efficiency and cost-effectiveness within the PV materials sector. The estimated market value for 2025 is projected to be in the billions of dollars, demonstrating the substantial investment and market potential within the sector.

Several key factors are driving the explosive growth of the photovoltaic materials market. Firstly, the escalating global concern about climate change and the urgent need to transition to cleaner energy sources are paramount. Governments worldwide are implementing supportive policies, including subsidies, tax breaks, and renewable portfolio standards, to incentivize the adoption of solar energy. This policy support is creating a favorable environment for the growth of the PV materials industry. Secondly, the continuous decline in the cost of solar energy is making it increasingly competitive with traditional fossil fuels. Advancements in manufacturing technology, economies of scale, and increased competition have all contributed to significant cost reductions in solar panel production, making solar power a more attractive option for both consumers and businesses. Thirdly, technological innovations in PV materials are leading to higher efficiency and longer lifespans of solar panels. This translates to greater energy output and reduced maintenance costs, further enhancing the economic viability of solar energy. Finally, the increasing awareness among consumers and businesses about the environmental benefits of solar energy is boosting demand for solar panels and, consequently, for the PV materials used in their production. This combination of supportive policies, decreasing costs, technological advancements, and rising environmental awareness creates a powerful synergy that drives the continued expansion of the PV materials market.

Despite the significant growth potential, the photovoltaic materials market faces several challenges and restraints. One major concern is the intermittent nature of solar energy, which requires efficient energy storage solutions to ensure a reliable power supply. The development and deployment of large-scale energy storage systems are crucial for maximizing the utilization of solar power and mitigating its intermittency. Another challenge is the dependence on raw materials, such as silicon, which can experience price fluctuations impacting the overall cost of PV systems. Securing a reliable and sustainable supply chain for these raw materials is essential for the long-term stability of the industry. Furthermore, the manufacturing process of PV materials can be energy-intensive, raising concerns about its environmental footprint. Efforts to improve the sustainability of manufacturing processes are crucial for reducing the industry's overall carbon emissions. In addition, the disposal and recycling of end-of-life solar panels are emerging as significant environmental issues, requiring the development of effective recycling technologies. Finally, land use requirements for large-scale solar power projects can lead to conflicts with other land uses, particularly in densely populated regions. Careful planning and consideration of land use impacts are essential for minimizing environmental and social disruptions.

The crystalline silicon segment is projected to dominate the PV materials market throughout the forecast period (2025-2033). Its established technology, high efficiency, and relatively low cost make it the preferred choice for most solar panel manufacturers.

Crystalline Silicon's Dominance: This segment's continued dominance stems from its mature technology, resulting in cost-effective and efficient solar cells. Improvements in manufacturing processes further enhance its competitiveness. The vast majority of solar panels currently produced utilize crystalline silicon.

China's Leading Role: China is expected to remain the leading producer and consumer of PV materials, driven by its substantial investments in solar energy infrastructure and its robust manufacturing base. The country's supportive government policies significantly contribute to its leading market position.

Utility-Scale Applications: The utility-scale segment is anticipated to register the most significant growth, driven by the increasing demand for large-scale solar power plants to meet the rising global energy needs. This segment benefits from economies of scale, leading to lower costs per watt.

Regional Variations: While China holds a dominant position, other regions, such as Europe and North America, are expected to show considerable growth, driven by increasing renewable energy targets and supportive government policies. These regions are experiencing a significant uptake of residential and commercial solar installations, contributing to the overall market expansion.

In summary: The combination of the crystalline silicon segment's technological maturity and China's substantial manufacturing capacity and supportive policies positions this segment as the clear market leader. The utility-scale application segment further accentuates this dominance due to its scale and demand.

Several factors are acting as catalysts for the industry's growth. Continued government support through subsidies and tax incentives plays a crucial role. Technological advancements, especially in improving efficiency and reducing production costs, are also key drivers. The increasing affordability of solar energy systems is making them accessible to a broader consumer base, furthering the market expansion. Furthermore, growing environmental awareness and the global shift toward sustainable energy are creating strong underlying demand.

This report provides a detailed analysis of the photovoltaic materials market, offering valuable insights into market trends, growth drivers, challenges, and key players. The comprehensive study covers the historical period (2019-2024), base year (2025), and forecast period (2025-2033), presenting a thorough understanding of the industry's past, present, and future trajectory. The report meticulously analyzes various market segments, including crystalline materials, thin-film materials, and others, along with their respective applications in the utility, commercial, and residential sectors. It also profiles major players in the industry, providing a competitive landscape analysis. This analysis offers actionable insights for businesses looking to invest or operate in the dynamic photovoltaic materials market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.1%.

Key companies in the market include GCL Group, WACKER CHEMIE, Hemlock Semiconductor, OCI, REC Silicon, TBEA, SunEdision, Sichuan Yongxiang, KCC, Tokuyama, HanKook Silicon, Daqo New Energy, Dun'an Group, LDK Solar, Hanwha Chemical, Luoyang China Silicon, Asia Silicon, Yichang CSG, .

The market segments include Type, Application.

The market size is estimated to be USD 12840 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Photovoltaic Materials," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Photovoltaic Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.