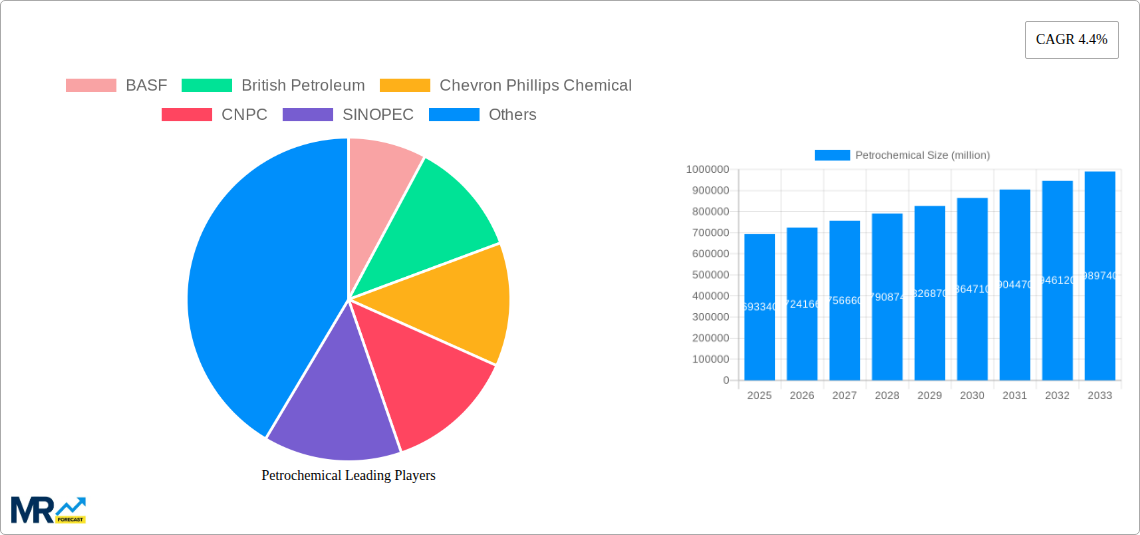

1. What is the projected Compound Annual Growth Rate (CAGR) of the Petrochemical?

The projected CAGR is approximately 4.4%.

Petrochemical

PetrochemicalPetrochemical by Type (Ethylene, Propylene, Butadiene, Benzene, Xylene, Toluene, Vinyls, Styrene, Methanol), by Application (Automotive, Textile, Construction, Industrial, Medical, Pharmaceuticals, Electronics, Consumer Goods Industries), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

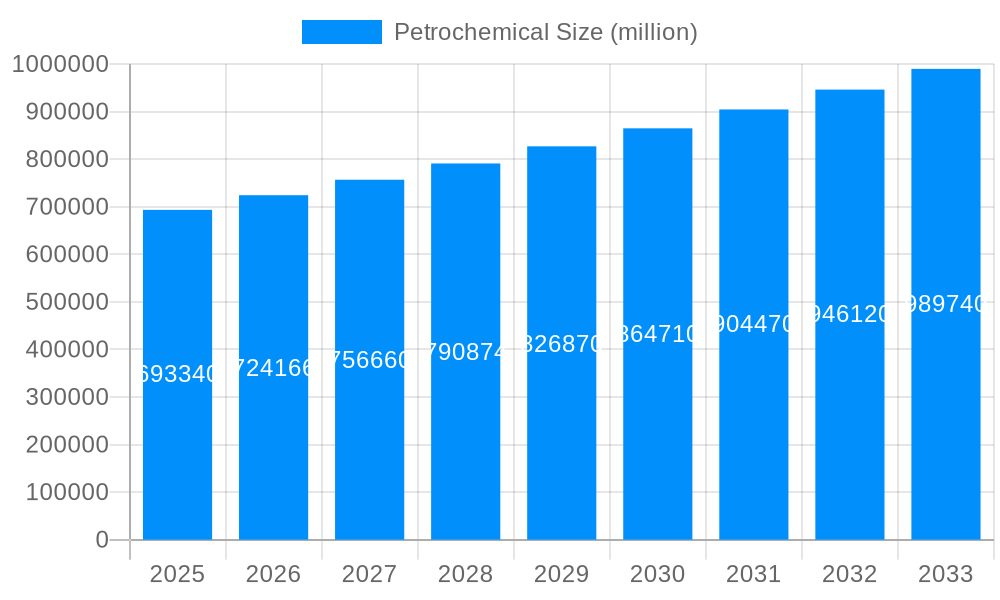

The global petrochemical market, valued at $693.34 billion in 2025, is projected to experience robust growth, driven by increasing demand from key end-use sectors like packaging, construction, and automotive. A compound annual growth rate (CAGR) of 4.4% from 2025 to 2033 indicates a significant expansion of the market to approximately $1,000 billion by 2033. This growth is fueled by rising global population and disposable incomes, leading to increased consumption of plastics and other petrochemical-derived products. Furthermore, technological advancements in polymer chemistry are contributing to the development of more sustainable and high-performance materials, further stimulating market expansion. However, fluctuating crude oil prices, stringent environmental regulations aimed at reducing plastic waste, and concerns regarding the environmental impact of petrochemical production pose significant challenges to sustained growth.

The competitive landscape is dominated by major multinational companies such as BASF, BP, Chevron Phillips Chemical, CNPC, SINOPEC, DuPont, ExxonMobil, INEOS, LyondellBasell, Shell, SABIC, and Dow, who are constantly investing in research and development to enhance their product portfolio and improve production efficiency. These companies are also actively pursuing strategies to mitigate environmental concerns through the development of bio-based petrochemicals and improved recycling technologies. Regional growth will vary depending on economic development, infrastructure investment, and government policies. Regions with robust industrial growth and expanding manufacturing sectors are anticipated to experience higher growth rates within the forecast period. The successful navigation of environmental concerns and the continued innovation in sustainable solutions will be critical factors in shaping the future trajectory of the petrochemical market.

The global petrochemical market, valued at $600 billion in 2024, is projected to experience robust growth, reaching an estimated $850 billion by 2033. This expansion is fueled by several interconnected factors. Increasing global population and rising disposable incomes in developing economies are driving demand for plastics, synthetic fibers, and other petrochemical-derived products. The construction industry, a significant consumer of petrochemicals, is also witnessing substantial growth, particularly in emerging markets, further boosting market demand. Moreover, advancements in technology are leading to the development of more efficient and sustainable petrochemical processes, contributing to increased production and potentially mitigating some environmental concerns. However, fluctuations in crude oil prices remain a significant factor impacting profitability and market stability. The shift towards a circular economy and growing concerns regarding plastic waste are also introducing new challenges and opportunities for the industry, forcing companies to explore sustainable alternatives and improve recycling infrastructure. Geopolitical instability and regional conflicts can disrupt supply chains and influence pricing, adding another layer of complexity to the market outlook. The forecast period (2025-2033) anticipates a compound annual growth rate (CAGR) exceeding 4%, indicating a continued strong upward trajectory for the industry, although the rate of growth may fluctuate year-on-year based on global economic conditions and political factors. The report details these factors and provides a granular analysis of regional variations in growth.

Several key factors are driving the growth of the petrochemical industry. Firstly, the continued expansion of the global middle class, especially in Asia and Africa, is significantly increasing the demand for consumer goods manufactured using petrochemicals. This translates into higher demand for plastics in packaging, automotive components, and consumer electronics. Secondly, the burgeoning construction sector, both residential and commercial, necessitates a large amount of petrochemical-based materials like pipes, insulation, and paints. Thirdly, technological advancements in petrochemical processing, including the development of more efficient and less environmentally damaging production methods, contribute to increased production capacity and reduced costs. Finally, government policies promoting infrastructure development in various regions indirectly stimulate the petrochemical sector by creating greater demand for construction materials and consumer goods. However, the long-term sustainability of this growth depends on the industry's ability to address environmental concerns and transition towards more sustainable practices, which include reducing carbon emissions and promoting recycling.

Despite the positive growth outlook, the petrochemical industry faces considerable challenges. Fluctuations in crude oil prices represent a major risk, impacting production costs and profitability. Environmental concerns surrounding plastic waste and greenhouse gas emissions are increasingly influencing public opinion and leading to stricter regulations. The growing push for sustainability is prompting a shift towards bio-based alternatives and a greater focus on recycling, posing a significant challenge to traditional petrochemical players. Furthermore, competition from emerging economies with lower production costs can impact market share for established players. Geopolitical risks, such as trade wars and supply chain disruptions, also create uncertainty and potentially hinder growth. Finally, investing in research and development to create more sustainable and efficient processes requires significant capital expenditure, limiting the growth potential for smaller companies.

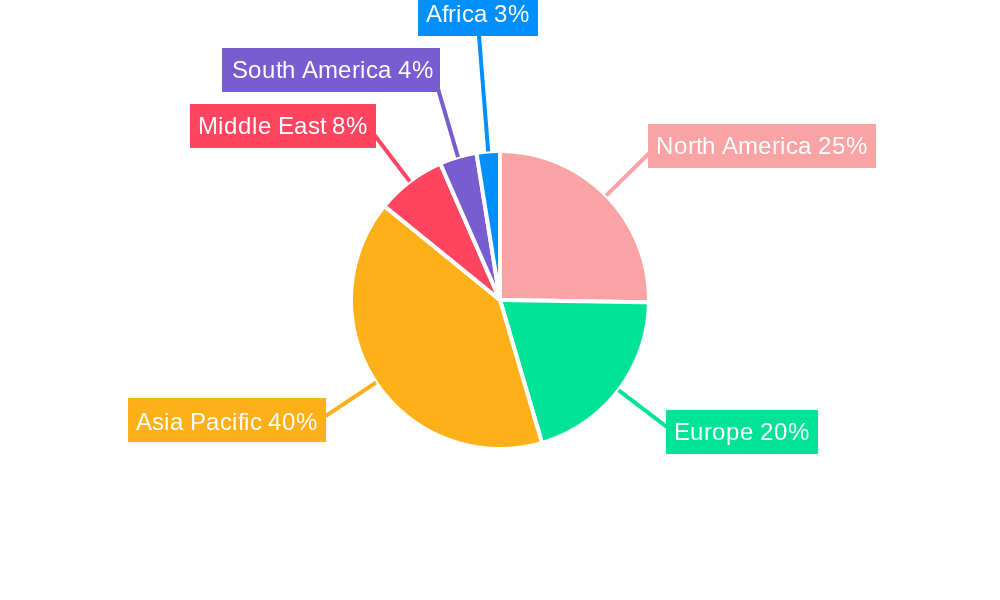

Asia-Pacific: This region is projected to dominate the market throughout the forecast period due to its rapidly expanding economies, burgeoning population, and significant investments in infrastructure development. China and India, in particular, are key drivers of growth within this region, with a combined demand exceeding that of any other nation. The region’s high demand for plastics, packaging, and construction materials fuels substantial consumption of petrochemicals.

North America: Although slightly less dominant than Asia-Pacific, North America maintains a significant market share, driven by robust domestic consumption and strong manufacturing capabilities. The region's emphasis on technological advancement and relatively stable political landscape contributes to its sustained growth.

Middle East: Possessing substantial oil and gas reserves, the Middle East acts as a significant producer and exporter of petrochemicals. The region’s strategic location contributes to its influence in the global market.

Europe: The region faces stricter environmental regulations, driving innovation in sustainable petrochemical production and recycling technologies. Its established chemical industry contributes to substantial output and export.

South America: This region shows moderate growth, with its development rate largely influenced by economic conditions and government policies.

Dominant Segments: The ethylene and propylene segments are projected to hold the largest market share due to their widespread use as feedstock in the production of various downstream products, including plastics, fibers, and solvents. The polyethylene segment, due to its applications in plastic packaging, films and various other applications, is also projected to witness significant growth.

The industry's growth is primarily fueled by rising global demand for consumer goods, spurred by population growth and increasing disposable incomes. The construction boom in developing nations significantly boosts demand for petrochemical-derived building materials. Technological advancements in production efficiency and the emergence of sustainable practices contribute to enhanced market competitiveness. Favorable government policies in certain regions promoting industrial development indirectly accelerate market expansion.

This report offers a comprehensive analysis of the global petrochemical market, providing insights into market size, growth drivers, challenges, key players, and future trends. It also incorporates detailed regional and segmental breakdowns, enabling a thorough understanding of the market dynamics. The report includes a thorough forecast for the period 2025-2033, offering valuable insights for strategic decision-making within the industry. The research methodology employed involves a combination of primary and secondary sources, guaranteeing the accuracy and reliability of the data presented.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.4%.

Key companies in the market include BASF, British Petroleum, Chevron Phillips Chemical, CNPC, SINOPEC, DuPont, ExxonMobil, INEOS, LyondellBasell, Shell Global, SABIC, Dow, .

The market segments include Type, Application.

The market size is estimated to be USD 693340 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Petrochemical," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Petrochemical, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.