1. What is the projected Compound Annual Growth Rate (CAGR) of the Pet Dog Food and Treats?

The projected CAGR is approximately 11.9%.

Pet Dog Food and Treats

Pet Dog Food and TreatsPet Dog Food and Treats by Type (Dry Food, Wet Food, Treats), by Application (Online Retail, Store Sales), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

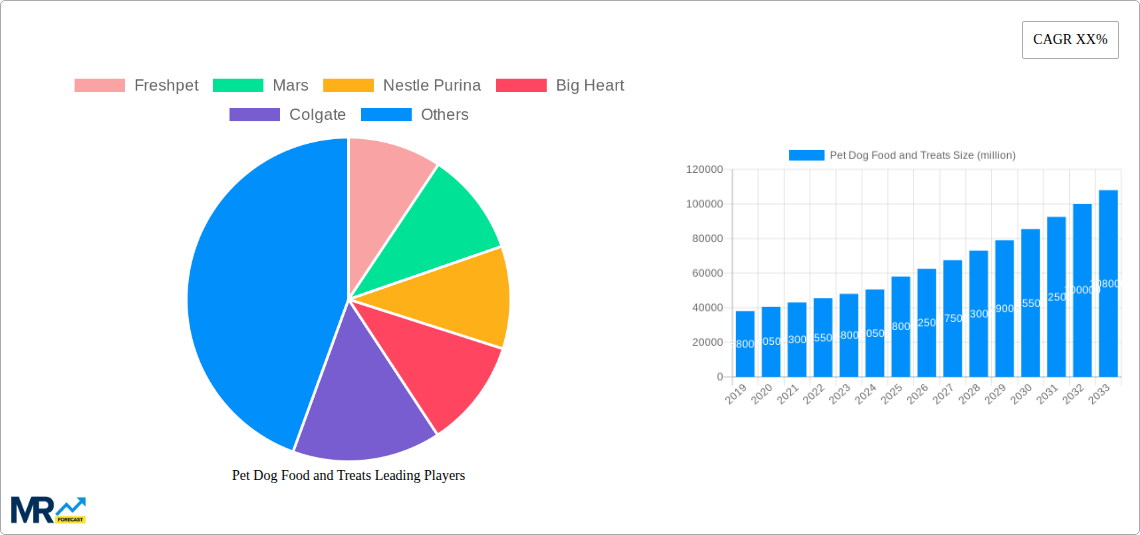

The global pet dog food and treats market is a substantial and rapidly growing sector, exhibiting a dynamic interplay of factors driving its expansion. While precise market size figures are not provided, considering typical growth rates in the pet food industry and the substantial presence of major players like Mars, Nestle Purina, and others, a reasonable estimate for the 2025 market size could be in the range of $80-100 billion USD. This substantial market value is fueled by several key drivers: the increasing humanization of pets, leading to greater spending on premium and specialized food products; rising pet ownership, particularly in developing economies; and a growing awareness among pet owners of the importance of nutrition for their dog's health and wellbeing. Further propelling this growth is the expansion of e-commerce channels, offering convenience and access to a broader range of products. Trends indicate a significant shift toward premiumization, with pet owners increasingly opting for natural, organic, and grain-free options. The market also showcases increasing innovation in functional foods designed to address specific health concerns, such as joint health or allergies. Despite this positive outlook, challenges remain, including supply chain disruptions, fluctuating raw material costs, and increasing competition. Segment-wise, the dry food segment likely holds the largest market share due to its affordability and shelf-life, while the wet food and treats segments are experiencing rapid growth, driven by increasing consumer preference for palatability and variety. The online retail channel is also expanding rapidly, providing convenient purchasing options for pet owners.

The competitive landscape is characterized by a mix of established multinational corporations and smaller, specialized brands. Large companies benefit from economies of scale and extensive distribution networks, while smaller brands often succeed by focusing on niche markets and offering highly specialized products. Geographical variations are expected, with North America and Europe likely holding the largest market shares due to high pet ownership rates and established pet food markets. However, significant growth potential exists in Asia-Pacific and other emerging markets where pet ownership is increasing rapidly. Future growth is expected to be fueled by innovation in areas such as personalized nutrition, functional foods, and sustainable packaging. Addressing concerns regarding pet obesity and allergies will also play a significant role in shaping the market trajectory in the coming years. Continued market segmentation, offering products tailored to specific breeds, life stages, and health needs, will remain crucial for success. The forecast period (2025-2033) suggests continued growth, potentially reaching $150-$200 billion USD by 2033, assuming a moderate CAGR. This growth projection incorporates a realistic assessment of market trends, considering potential economic fluctuations and unforeseen events.

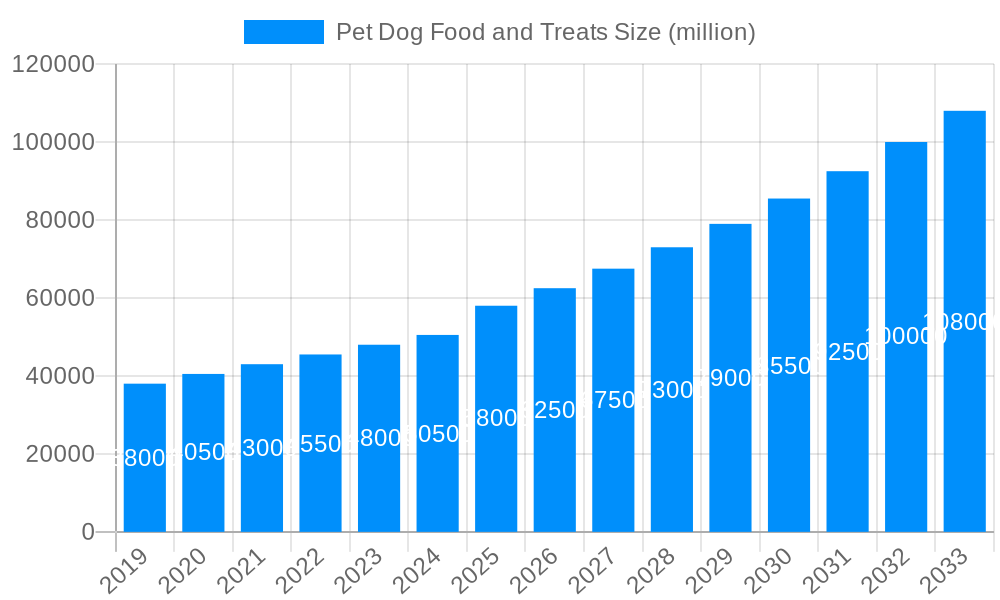

The global pet dog food and treats market experienced robust growth throughout the historical period (2019-2024), driven by increasing pet ownership, rising pet humanization trends, and a growing awareness of pet health and nutrition. The market is characterized by a diverse range of products catering to various dog breeds, ages, and dietary needs. Dry food continues to hold the largest market share due to its convenience, affordability, and long shelf life. However, the wet food segment is experiencing significant growth, propelled by the perception of its higher palatability and nutritional value. The treats segment is also thriving, with innovative products focusing on functionality, such as dental chews or training aids, alongside indulgent options. E-commerce channels are witnessing rapid expansion, offering convenience and a wider product selection to consumers. Premiumization is a key trend, with owners increasingly willing to spend more on high-quality, natural, and specialized dog food and treats. This trend is evident in the rising popularity of grain-free, organic, and single-source protein options. The market also shows a strong emphasis on transparency and traceability, with consumers seeking brands that clearly communicate ingredient sourcing and manufacturing processes. Competition is intense, with both established multinational corporations and smaller niche players vying for market share. Innovation remains a critical success factor, with companies constantly developing new products to meet evolving consumer demands and address specific dietary requirements. The forecast period (2025-2033) anticipates continued growth, fueled by the factors mentioned above and further penetration in emerging markets. Overall, the market demonstrates strong resilience and a positive outlook, reflecting the enduring bond between humans and their canine companions. The estimated market value in 2025 is projected to be in the hundreds of millions of units, with significant growth expected throughout the forecast period.

Several key factors are driving the expansion of the pet dog food and treats market. The increasing humanization of pets is a major contributor, with owners viewing their dogs as integral members of the family and willing to invest in their health and well-being. This translates into increased spending on premium products, specialized diets, and functional treats. The rising disposable incomes in many parts of the world, particularly in developing economies, also contribute significantly to market growth, as more people can afford to purchase higher-quality pet food and treats. The growing awareness of pet health and nutrition is another significant driver. Consumers are increasingly educated about the importance of balanced nutrition for their dogs, leading to a demand for products that meet specific dietary needs and address health concerns, such as allergies or weight management. Furthermore, the expansion of e-commerce channels provides consumers with easy access to a wide range of products and brands, boosting overall market sales. Innovative product development and the introduction of new formulations, flavors, and functional treats cater to the diverse preferences of both dogs and their owners. The market is also witnessing an increase in the demand for natural, organic, and sustainable pet food options, aligned with the broader consumer trend toward health-conscious consumption.

Despite its strong growth trajectory, the pet dog food and treats market faces several challenges. Fluctuations in raw material prices, particularly protein sources, can impact production costs and profitability. Maintaining consistent product quality and ensuring food safety are crucial considerations for manufacturers, demanding stringent quality control measures. Stringent regulations and compliance requirements regarding ingredient labeling, food safety, and environmental sustainability add to operational complexities and costs. The increasing competition from both established players and emerging brands necessitates continuous innovation and marketing efforts to maintain market share. Maintaining a sustainable supply chain, ensuring ethical sourcing practices, and managing environmental impacts are also becoming increasingly important considerations for manufacturers. Consumer concerns about specific ingredients, such as artificial colors and preservatives, or controversies related to specific dietary approaches, can negatively impact brand perception and sales. Economic downturns can also affect consumer spending on discretionary items like premium pet food and treats, potentially slowing market growth. Effectively managing these challenges requires a proactive approach to cost management, continuous quality improvement, transparent communication, and a focus on sustainable practices.

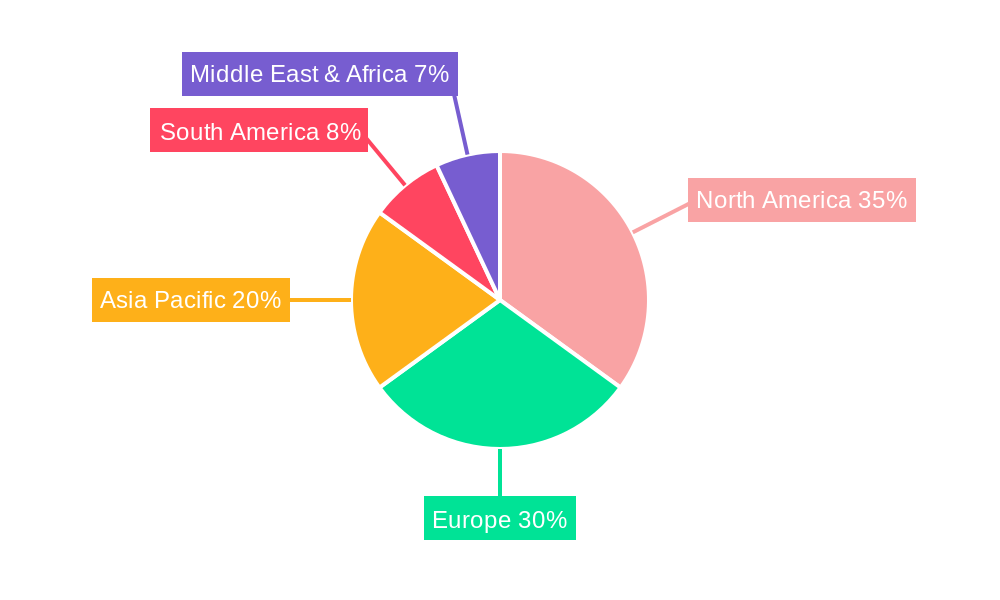

The North American market, particularly the United States, holds a dominant position in the global pet dog food and treats market due to high pet ownership rates, strong consumer spending power, and the presence of major players in the industry. The European market also represents a significant portion of the global market. However, emerging economies in Asia-Pacific, particularly China and India, are exhibiting rapid growth driven by increasing pet ownership and rising disposable incomes.

Dominant Segment: The dry food segment maintains the largest market share due to its convenience, affordability, and extended shelf life compared to wet food. Its ease of storage and cost-effectiveness makes it particularly appealing to a large consumer base. Dry food encompasses various formulations, such as kibble and extruded snacks, catering to different dietary needs and preferences. The segment continues to innovate, with new product offerings incorporating improved nutritional profiles, functional ingredients, and appealing textures.

Dominant Application: While both online and store sales contribute significantly, store sales (including supermarkets, pet specialty stores, and veterinary clinics) continue to hold a larger share of the market, providing immediate access and a tangible shopping experience. However, the online retail segment is growing rapidly, driven by convenience, a wider product selection, and competitive pricing. Online retailers are leveraging data analytics to target specific consumer segments and promote tailored product offerings, fostering further market expansion.

Within North America:

United States: High pet ownership, combined with a culture of pet humanization and high disposable incomes, fuels substantial demand for pet dog food and treats.

Canada: Similar to the U.S., Canada exhibits robust growth due to high pet ownership rates and a growing awareness of pet nutrition.

Within Europe:

Germany: A large and developed pet market, characterized by strong consumer interest in premium and specialized pet food products.

United Kingdom: High pet ownership and significant spending on pet care contribute to strong market growth.

Within Asia-Pacific:

China: Rapidly expanding pet ownership and increasing consumer spending power are driving significant growth in the dog food and treat sector.

India: Similar to China, India is seeing a surge in pet ownership and a consequent rise in demand for pet food products.

The market is expected to continue this growth trajectory over the forecast period, with these regions and segments leading the way. Innovation in product offerings, targeted marketing strategies, and expanding distribution channels will further fuel this expansion.

Several factors are catalyzing growth in the pet dog food and treats industry. The increasing humanization of pets and their elevated status within families directly translates to higher spending on premium and specialized food products. Advances in pet nutrition research and the development of functional foods that address specific health concerns are driving demand for products tailored to unique dietary needs. The continued rise of online retail channels provides convenient access to a broader selection of products and strengthens market reach. Finally, an increasing awareness of sustainability and responsible sourcing encourages a shift towards eco-friendly and ethically produced pet food, further fueling market development.

This report provides a detailed analysis of the pet dog food and treats market, encompassing market sizing, segmentation, trends, drivers, challenges, and competitive landscape. It offers valuable insights into consumer behavior, product innovation, and market dynamics, allowing stakeholders to make informed decisions regarding investments, product development, and market strategies. The report includes historical data, current market estimations, and future projections to provide a comprehensive understanding of the market's trajectory. Furthermore, the study identifies key market players and analyzes their strategies, contributing to a complete picture of the competitive landscape. This information is essential for businesses seeking to understand and capitalize on opportunities within this thriving market segment.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 11.9%.

Key companies in the market include Freshpet, Mars, Nestle Purina, Big Heart, Colgate, Diamond pet foods, Blue Buffalo, Heristo, Unicharm, Mogiana Alimentos, Affinity Petcare, Nisshin Pet Food, Total Alimentos, Ramical, Butcher’s, MoonShine, Big Time, Yantai China Pet Foods, Gambol, Paide Pet Food, Wagg, .

The market segments include Type, Application.

The market size is estimated to be USD 40.52 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Pet Dog Food and Treats," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pet Dog Food and Treats, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.