1. What is the projected Compound Annual Growth Rate (CAGR) of the Paper and Paperboard Tray?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Paper and Paperboard Tray

Paper and Paperboard TrayPaper and Paperboard Tray by Type (Virgin Cellulose, Recycled Cellulose, World Paper and Paperboard Tray Production ), by Application (Food and Beverages, Personal Care and Cosmetics, Healthcare, Others, World Paper and Paperboard Tray Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

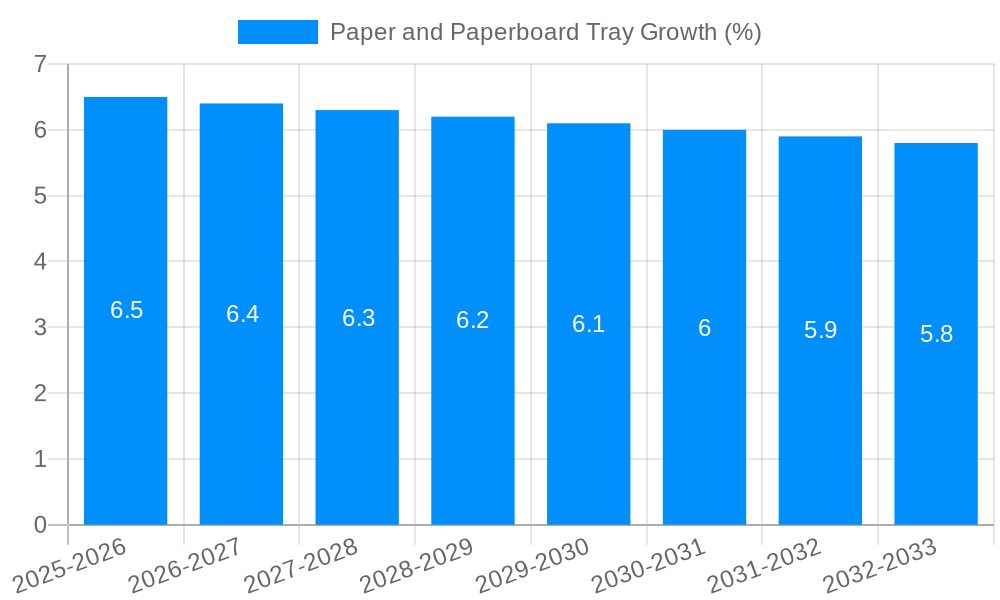

The global paper and paperboard tray market is experiencing robust growth, projected to reach an estimated market size of approximately $30,000 million by 2025, with a compound annual growth rate (CAGR) of around 6.5% expected to persist through 2033. This expansion is primarily fueled by the increasing consumer demand for sustainable packaging solutions across various industries. The surge in environmental consciousness and stricter regulations favoring eco-friendly materials have positioned paper and paperboard trays as a preferred alternative to conventional plastic packaging. Key drivers include the growing food and beverage sector, which relies heavily on these trays for product presentation and protection, and the expanding personal care and cosmetics industry, where aesthetically pleasing and sustainable packaging is a significant differentiator. Furthermore, the healthcare sector's adoption of paper and paperboard trays for medical supplies and disposables is contributing to market momentum. The versatility of these trays, coupled with advancements in their design and functionality, continues to broaden their applicability.

The market is segmented into virgin cellulose and recycled cellulose types, with recycled cellulose gaining significant traction due to its enhanced sustainability profile and cost-effectiveness, aligning with circular economy principles. Geographically, the Asia Pacific region is anticipated to lead the market in terms of both production and consumption, driven by rapid industrialization, a burgeoning middle class, and supportive government initiatives promoting sustainable packaging in countries like China and India. North America and Europe are also significant markets, characterized by mature economies with a strong emphasis on environmental responsibility and innovation in packaging. However, the market faces certain restraints, including the fluctuating prices of raw materials like pulp and paper, and the ongoing competition from alternative sustainable packaging materials such as molded pulp and compostable plastics. Despite these challenges, the overarching trend towards a greener economy and the inherent recyclability and biodegradability of paper and paperboard trays solidify their long-term market prospects.

The global paper and paperboard tray market is poised for significant expansion, with production projected to reach 570 million units by 2033, a substantial increase from the estimated 490 million units in the base year of 2025. This growth trajectory is underpinned by a confluence of factors, notably the escalating consumer preference for sustainable packaging solutions and the inherent recyclability of paper and paperboard materials. As environmental consciousness permeates global consumer behavior, industries are actively seeking alternatives to traditional plastics. Paper and paperboard trays, with their lower environmental footprint and biodegradability, are emerging as a prime substitute across various sectors. The historical period of 2019-2024 witnessed a steady adoption rate, a trend that is expected to accelerate exponentially during the forecast period of 2025-2033. Key market insights reveal a robust demand for both virgin cellulose and recycled cellulose based trays, with recycled cellulose gaining considerable traction due to its cost-effectiveness and circular economy appeal. The Food and Beverages segment continues to be the dominant application, driven by the substantial volume of packaged food products requiring robust and safe containment. However, the Personal Care and Cosmetics and Healthcare segments are exhibiting impressive growth rates, as manufacturers in these industries increasingly recognize the branding and consumer appeal of eco-friendly packaging. Innovations in design and functionality, such as improved moisture resistance and structural integrity, are further broadening the appeal of paper and paperboard trays, allowing them to cater to a wider array of product types. The market's dynamism is further amplified by ongoing research and development efforts focused on enhancing the performance characteristics of these trays, including their barrier properties and printability, ensuring their continued relevance and competitiveness against alternative packaging materials.

The surge in demand for paper and paperboard trays is primarily fueled by a powerful global push towards sustainability. Governments worldwide are implementing stricter regulations on single-use plastics, incentivizing the adoption of eco-friendly alternatives. This regulatory landscape, coupled with a heightened consumer awareness of environmental issues, has created a fertile ground for paper and paperboard packaging. Consumers are actively seeking out products that align with their environmental values, and the packaging is often the first point of contact that communicates this commitment. Furthermore, the inherent properties of paper and paperboard, such as their renewability, biodegradability, and recyclability, make them an attractive choice for businesses aiming to enhance their corporate social responsibility profiles. The versatility of paper and paperboard trays, capable of being molded into various shapes and sizes to accommodate diverse products, further contributes to their market penetration. From delicate cosmetics to perishable food items, these trays offer a protective and aesthetically pleasing packaging solution that can be tailored to specific needs. The cost-effectiveness of paper and paperboard, especially when utilizing recycled materials, also plays a crucial role in its widespread adoption, making it an economically viable option for manufacturers of all scales.

Despite the optimistic outlook, the paper and paperboard tray market is not without its hurdles. A significant challenge lies in the performance limitations of these materials compared to certain plastic counterparts, particularly in applications requiring superior moisture and grease resistance. While advancements are being made, achieving comparable barrier properties without compromising the material's eco-friendly credentials remains an ongoing area of research and development. The initial investment in new manufacturing equipment for paper and paperboard tray production can also be a deterrent for some companies, especially smaller businesses with limited capital. Fluctuations in the cost of raw materials, such as virgin pulp and recycled paper, can impact the overall pricing and profitability of paper and paperboard trays, creating market volatility. Furthermore, the availability and accessibility of high-quality recycled cellulose can be inconsistent, posing a challenge for manufacturers heavily reliant on this resource. Consumer perception also plays a role; while many embrace sustainable options, some may still associate certain paper-based packaging with lower perceived quality or durability, necessitating continued educational efforts and product innovation to overcome such reservations. The transportation and logistics involved in distributing these trays, especially in bulk, can also present challenges related to space optimization and potential damage.

The global paper and paperboard tray market is characterized by robust growth, with certain regions and segments poised to lead this expansion. The Food and Beverages segment is undeniably the dominant application, driven by the sheer volume of products requiring safe and convenient packaging. This segment is expected to continue its stronghold throughout the forecast period of 2025-2033. Within this segment, trays for ready-to-eat meals, frozen foods, fresh produce, and baked goods are particularly in high demand. The increasing consumer trend towards convenience and on-the-go consumption further bolsters the market for food and beverage paperboard trays.

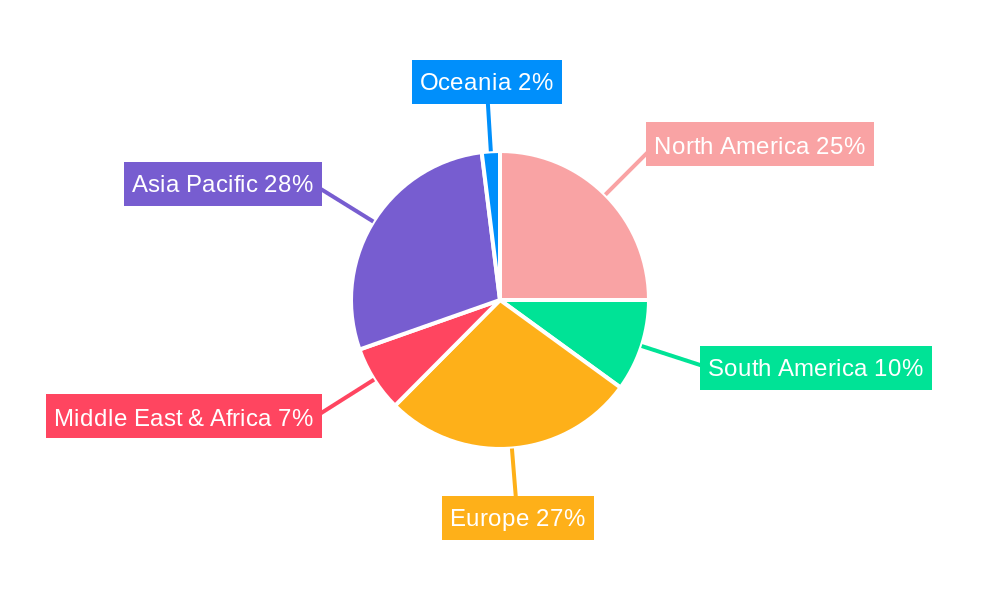

Geographically, North America and Europe are anticipated to be key dominant regions, largely due to stringent environmental regulations, high consumer awareness regarding sustainability, and the presence of major food and beverage manufacturers.

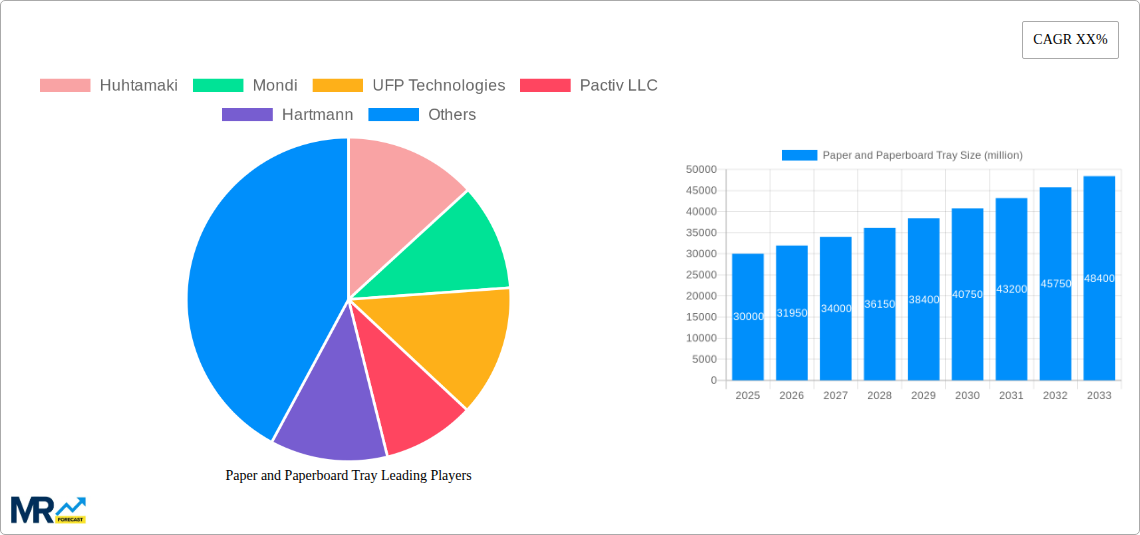

North America: The United States and Canada are expected to drive significant growth. The increasing demand for sustainable packaging in the e-commerce sector, coupled with a strong emphasis on recyclable materials, positions North America as a key player. The Personal Care and Cosmetics segment in North America is also witnessing a notable uptick in the adoption of paper and paperboard trays due to the premium branding opportunities and eco-conscious consumer base. Companies like Pactiv LLC and Huhtamaki have a substantial presence here, catering to these demands.

Europe: European countries, with their ambitious climate goals and well-established recycling infrastructure, are at the forefront of adopting sustainable packaging solutions. The Food and Beverages segment, particularly for baked goods, dairy products, and fresh produce, is exceptionally strong. Germany, France, and the United Kingdom are major contributors to this market. The Healthcare segment is also showing promising growth in Europe, as pharmaceutical companies explore biodegradable and compostable packaging solutions for certain medical supplies and personal care items. Mondi and Hartmann are key players in this region, actively innovating in paper-based solutions.

Beyond these established markets, the Asia Pacific region is emerging as a significant growth engine. Rapid urbanization, a burgeoning middle class, and increasing disposable incomes are driving demand for packaged goods. While the market is still maturing compared to North America and Europe, the adoption of paper and paperboard trays is accelerating, particularly in countries like China and India. The Others application segment, encompassing electronics, industrial goods, and general retail, is also contributing to the growth, as businesses increasingly look for protective and eco-friendly transit packaging.

The Recycled Cellulose type segment is expected to witness the fastest growth rate across all regions. This is driven by cost advantages, reduced environmental impact compared to virgin cellulose, and growing regulatory support for circular economy principles. Manufacturers are increasingly investing in technologies to improve the quality and performance of recycled cellulose-based trays, making them competitive with virgin cellulose for a wider range of applications.

The paper and paperboard tray industry is propelled by several powerful growth catalysts. The escalating global demand for sustainable and eco-friendly packaging solutions is paramount, driven by both consumer preference and stringent government regulations against single-use plastics. The inherent recyclability, biodegradability, and renewability of paper and paperboard materials position them as ideal alternatives. Innovations in material science and manufacturing processes are continually enhancing the performance characteristics of these trays, such as improved moisture and grease resistance, thereby expanding their application scope across diverse industries. The cost-effectiveness of paper and paperboard, especially when derived from recycled cellulose, further contributes to its widespread adoption, making it an economically attractive choice for manufacturers.

This report offers an in-depth analysis of the global paper and paperboard tray market, providing comprehensive insights into market dynamics, trends, and future projections. It meticulously covers the study period of 2019-2033, with a focus on the base year of 2025 and the forecast period of 2025-2033, drawing upon data from the historical period of 2019-2024. The report delves into key market drivers such as the increasing consumer demand for sustainable packaging and stringent environmental regulations. It also addresses the challenges and restraints impacting market growth, including performance limitations and raw material cost volatility. Furthermore, the report identifies dominant regions and segments, offering detailed analysis of their market share and growth potential. Leading players and their strategic initiatives are profiled, alongside significant market developments and technological advancements. This comprehensive coverage equips stakeholders with the crucial information needed to navigate the evolving landscape of the paper and paperboard tray industry.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Huhtamaki, Mondi, UFP Technologies, Pactiv LLC, Hartmann, Orcon Industries Corporation, International Paper, Arthena Superpack Private Limited, Papertech, Solut, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Paper and Paperboard Tray," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Paper and Paperboard Tray, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.