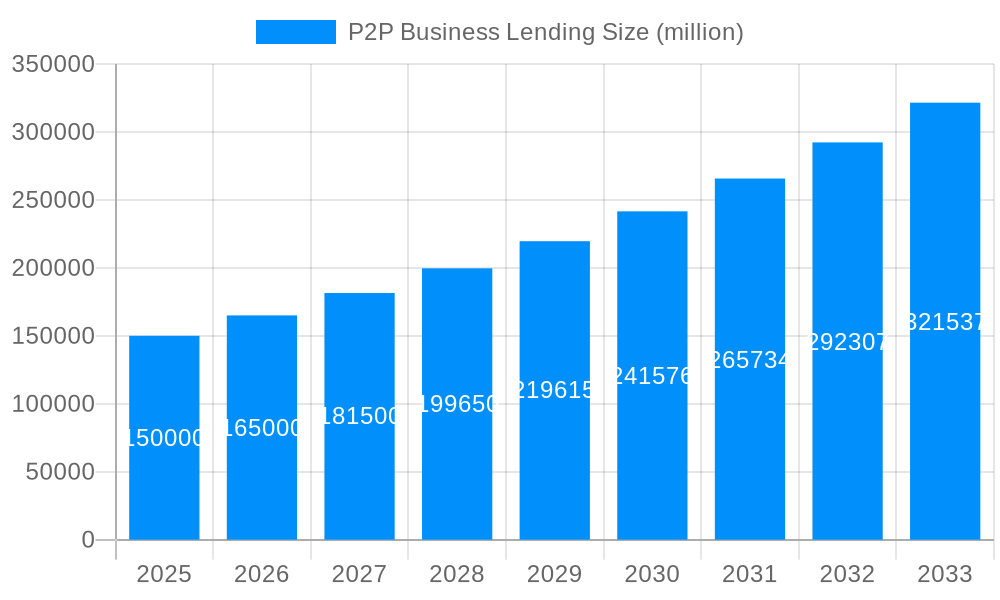

1. What is the projected Compound Annual Growth Rate (CAGR) of the P2P Business Lending?

The projected CAGR is approximately 21.7%.

P2P Business Lending

P2P Business LendingP2P Business Lending by Type (Term Loan, Revolving Loan, Others), by Application (Large Enterprise, SMEs), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

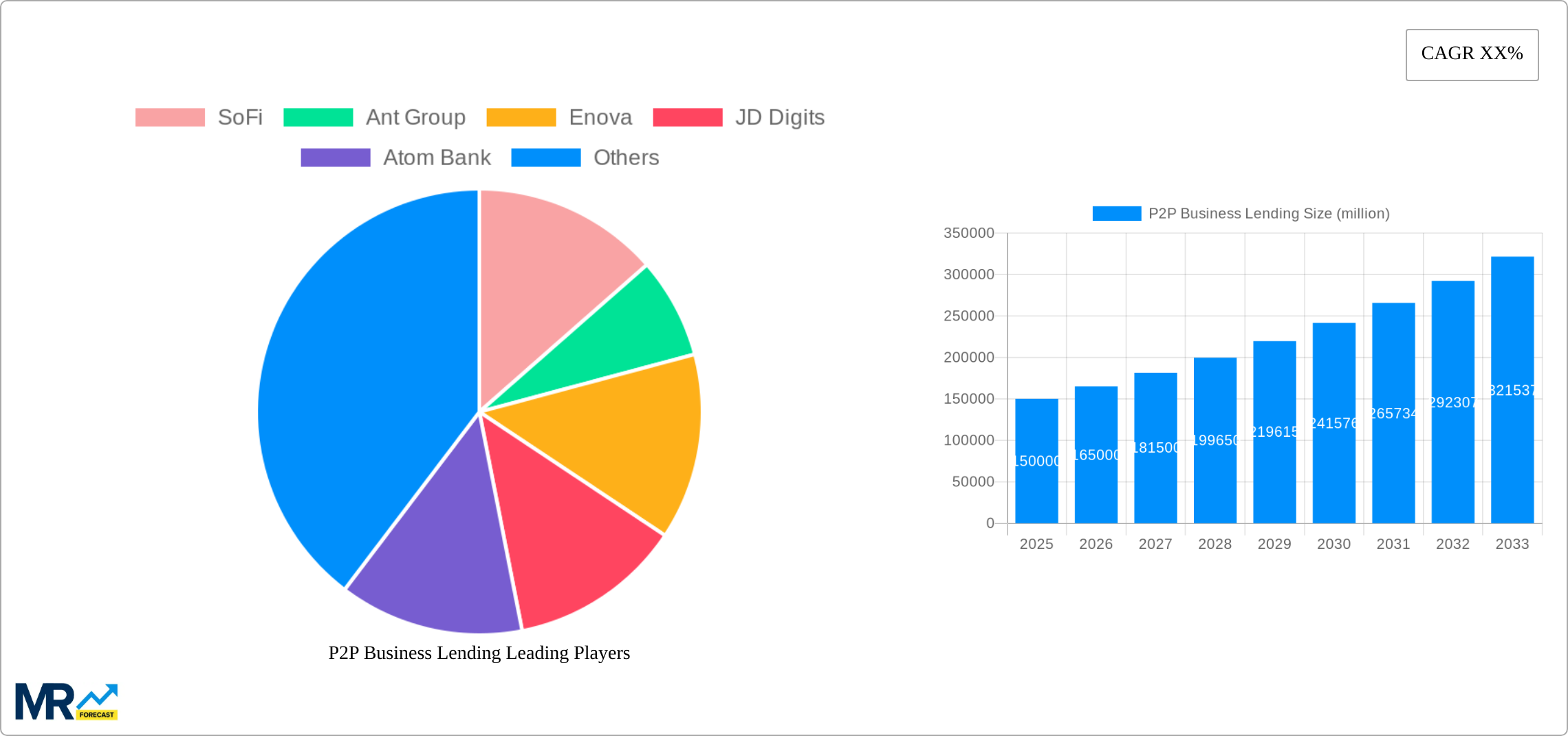

The Peer-to-Peer (P2P) business lending market is experiencing robust growth, driven by increasing demand for alternative financing options from small and medium-sized enterprises (SMEs) and large enterprises alike. The market's expansion is fueled by several key factors: the relatively faster and simpler application processes compared to traditional bank loans, the potential for lower interest rates due to the direct lending model, and the increased accessibility for businesses that may not qualify for traditional financing. Technological advancements, particularly in fintech, have played a significant role in streamlining operations, improving risk assessment, and enhancing the overall borrower and lender experience. While regulatory scrutiny and potential credit risks remain challenges, the market's overall trajectory suggests continued expansion. The segment breakdown shows a considerable portion of the market is allocated to term loans, reflecting a preference for structured repayment plans among borrowers. The geographical distribution indicates strong growth across North America and Europe, with significant potential in Asia-Pacific driven by its rapidly growing SME sector. The substantial presence of key players like SoFi, Ant Group, and Lending Club highlights the market's maturity and competitive landscape.

Looking ahead, the P2P business lending market is poised for sustained growth, projected to maintain a healthy compound annual growth rate (CAGR). Continued technological innovation will likely lead to more efficient and transparent lending platforms, further broadening access to capital for businesses of all sizes. Expansion into underserved markets and the development of innovative credit scoring models will also contribute to market expansion. However, maintaining a balance between growth and risk management will be crucial, demanding robust risk assessment frameworks and adherence to evolving regulatory standards. The diversification of product offerings, including revolving credit lines in addition to term loans, will cater to a broader range of business needs and further propel market growth. The ongoing competition among established players and new entrants is likely to drive innovation and potentially lead to improved terms and conditions for borrowers.

The Peer-to-Peer (P2P) business lending market has experienced significant growth over the past decade, evolving from a niche sector to a substantial component of the global financial landscape. The study period of 2019-2033 reveals a dynamic trajectory, marked by periods of rapid expansion interspersed with periods of consolidation and adaptation. The historical period (2019-2024) witnessed the emergence of numerous platforms, intense competition, and a gradual shift towards more sophisticated risk management techniques. The estimated market value in 2025 will be in the billions, reflecting the increasing adoption of P2P lending by SMEs and large enterprises alike. The forecast period (2025-2033) suggests continued expansion driven by technological advancements, regulatory clarity in key markets, and a growing demand for alternative financing solutions. This growth is not uniform across all segments; while term loans have historically dominated, the market is witnessing a surge in demand for revolving credit facilities, especially amongst SMEs seeking flexible financing options. The rise of fintech companies, offering streamlined processes and data-driven risk assessment, is a key factor in this trend. Geographic distribution also plays a crucial role; while certain regions like North America and Asia have seen robust growth, others are still developing their P2P lending infrastructure. The increasing availability of data analytics and machine learning tools allows for improved credit scoring and risk mitigation, leading to a more efficient and inclusive lending landscape. The increasing integration of blockchain technology offers potential benefits in transparency and security further enhancing the efficiency of these platforms. Moreover, the shifting regulatory environment, which may include stricter guidelines on consumer protection and data privacy, will be instrumental in shaping the future of P2P business lending. The evolving needs of businesses, coupled with continuous technological advancements, will continuously reshape the competitive dynamics within this sector.

Several factors are fueling the remarkable expansion of the P2P business lending market. Firstly, traditional banking systems often present significant hurdles for small and medium-sized enterprises (SMEs), particularly in accessing timely and affordable financing. P2P platforms offer a viable alternative, bypassing the lengthy application processes and stringent requirements often associated with traditional lenders. Secondly, technological advancements, including sophisticated algorithms for credit scoring and risk assessment, have greatly enhanced the efficiency and scalability of P2P lending platforms. These technologies enable lenders to make faster and more informed decisions, reducing processing times and expanding access to capital for a wider range of businesses. Thirdly, the growing awareness and acceptance of alternative financing options among businesses contribute to the market's growth. SMEs are increasingly seeking flexible and transparent financing solutions, and P2P platforms often provide this by offering more personalized loan terms and a greater degree of transparency throughout the lending process. Finally, the increasing availability of data, coupled with the improved analytical capabilities of P2P platforms, allows for more accurate risk assessment and pricing, leading to a more efficient allocation of capital and a reduction in overall lending costs. This data-driven approach promotes a more inclusive lending market, empowering businesses that may have traditionally struggled to secure financing from conventional sources.

Despite its impressive growth, the P2P business lending market faces several challenges. Regulatory uncertainty in various jurisdictions poses a significant obstacle, hindering the expansion of certain platforms and creating a complex regulatory landscape for businesses operating across multiple countries. Furthermore, the risk of defaults and losses remains a considerable concern. While sophisticated algorithms and data analysis techniques help mitigate risk, the inherent volatility of the market necessitates robust risk management strategies to protect investors and lenders. Maintaining investor confidence is also crucial for the sustained growth of the sector; any significant downturn or large-scale defaults could negatively impact the industry's image and attract increased regulatory scrutiny. Competition is intense amongst existing and emerging P2P lending platforms, requiring continuous innovation and adaptation to remain competitive. Cybersecurity threats are also a growing concern, given the sensitive financial data handled by these platforms, demanding significant investment in robust security measures to protect both borrowers and lenders. Finally, the potential for fraud and misrepresentation, coupled with the challenges in verifying the authenticity of borrower information, presents significant risks that require effective mitigation strategies.

The SME segment is poised for significant growth within the P2P business lending market. SMEs constitute a vast majority of businesses globally and face consistent challenges in accessing sufficient capital through traditional banking channels. P2P lending presents a highly attractive alternative with its speed, flexibility, and often less stringent requirements.

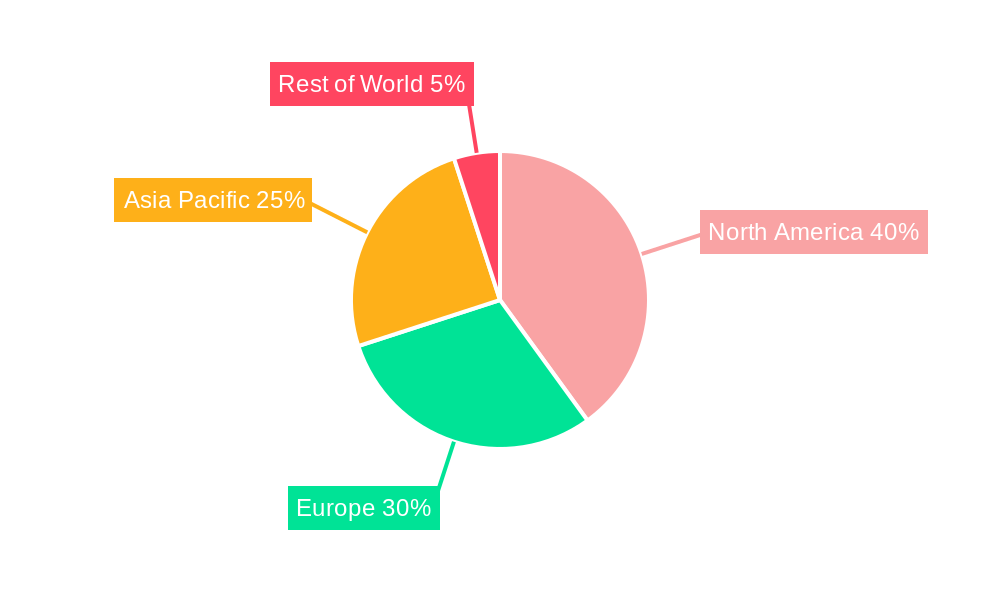

North America: This region is expected to maintain its leading position, driven by a robust economy, a high concentration of technology companies, and a supportive regulatory environment in certain areas.

Asia (Specifically China): China's substantial SME sector and the rapid expansion of fintech companies contribute significantly to Asia's dominance. Ant Group and JD Digits, for example, have played a pivotal role in shaping this market.

Term Loans: While revolving credit is gaining traction, term loans still constitute a substantial portion of P2P business lending, due to their predictability and suitability for various investment plans. This segment is likely to continue to dominate.

The dominance of these regions and segments reflects the interplay between technological advancements, conducive regulatory frameworks, and the specific financial needs of businesses within each region.

Paragraph Expansion: The SME segment within the P2P lending market is projected to experience exponential growth due to several factors. First, the traditionally restrictive lending criteria of traditional banks make it difficult for SMEs to secure loans, hindering their ability to expand or even maintain operations. P2P platforms present a more accessible alternative, focusing on alternative data points to assess creditworthiness beyond traditional financial statements. Second, the rapid growth of the technology sector supporting this industry facilitates quick and efficient loan processing, reducing processing times compared to banks. This efficiency is especially important for SMEs that need capital quickly to seize opportunities. Third, regulatory reforms and increased investor confidence are creating a more stable and conducive environment for growth in the sector. Fourth, an ever-increasing demand for innovative financing solutions among SMEs supports the market's steady upward trend, reinforcing the position of P2P lending as an essential alternative. The key to continued dominance in the SME segment lies in continued technological development and refining of risk assessment models to minimize losses and increase the efficiency of the process.

The continued growth of the P2P business lending market is driven by several key catalysts. The increasing adoption of digital technologies for loan origination and underwriting allows for faster and more efficient processing, significantly reducing costs and streamlining the lending process. Greater regulatory clarity and supportive government policies in key markets will help to foster investor confidence and stimulate further growth. Finally, the rising demand for alternative financing solutions among businesses unable to access traditional credit channels will continue to fuel the adoption of P2P lending platforms.

This report provides a comprehensive overview of the P2P business lending market, encompassing historical data, current market trends, and future projections. It analyzes key market drivers, challenges, and growth opportunities, providing valuable insights for stakeholders across the industry. The report also profiles leading players and examines significant developments shaping the future of P2P business lending. The detailed segmentation analysis offers a granular perspective on various market segments, helping businesses to identify lucrative growth opportunities and make strategic decisions. The forecast period extends to 2033, providing long-term projections that enable informed planning and investment strategies within this dynamic sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 21.7%.

Key companies in the market include SoFi, Ant Group, Enova, JD Digits, Atom Bank, GrabFinance, Lending Club, Du Xiaoman Finance, Avant, Prosper, Funding Circle, Upstart, Zopa, OnDeck, RateSetter, October, Borro, Auxmoney, GreeSky, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "P2P Business Lending," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the P2P Business Lending, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.