1. What is the projected Compound Annual Growth Rate (CAGR) of the Optically Transparent Antennas?

The projected CAGR is approximately 20%.

Optically Transparent Antennas

Optically Transparent AntennasOptically Transparent Antennas by Type (90% Transparent, 98% Transparent, Others, World Optically Transparent Antennas Production ), by Application (Mobile Display Technologies, Automotive, Satellite, Smart Buildings, Others, World Optically Transparent Antennas Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

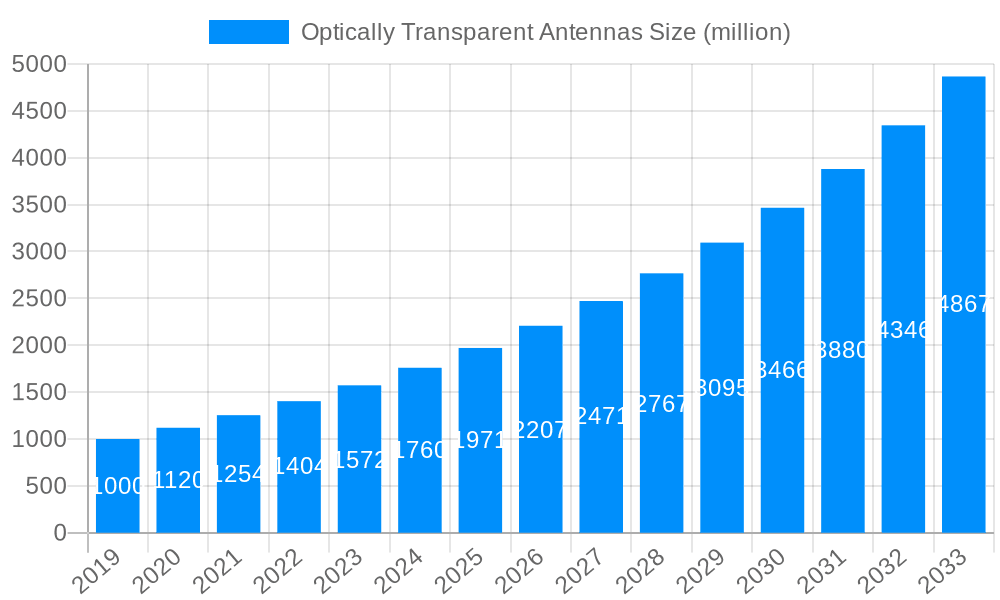

The global Optically Transparent Antennas market is poised for remarkable expansion, projected to reach a substantial $3000 million value by 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 20% throughout the forecast period. This robust growth is primarily fueled by the escalating demand for seamless integration of communication technology into everyday devices and infrastructure. Mobile display technologies, in particular, are a significant catalyst, as manufacturers seek to embed antennas discreetly within screens for a sleeker aesthetic and enhanced user experience. The automotive sector is also a key growth driver, with the increasing adoption of advanced driver-assistance systems (ADAS) and in-car connectivity solutions necessitating compact and visually unobtrusive antennas. Furthermore, the burgeoning smart buildings market, with its focus on integrated IoT devices and smart home functionalities, presents a substantial opportunity for optically transparent antennas to blend into architectural elements.

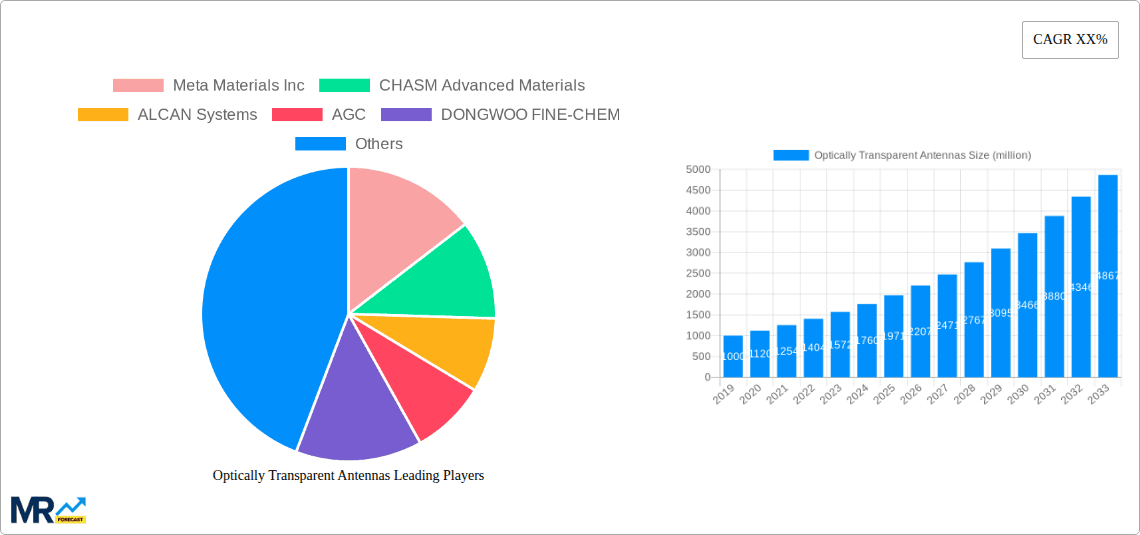

The market is characterized by a strong preference for 90% and 98% transparent antenna types, reflecting the industry's focus on achieving both high signal integrity and near-invisibility. While the "Others" segment for transparency exists, it represents a smaller portion of the market. Key players like Meta Materials Inc., CHASM Advanced Materials, and AGC are at the forefront of innovation, developing cutting-edge solutions that address the evolving needs of these dynamic application areas. Geographically, Asia Pacific, led by China and Japan, is expected to be a dominant region due to its manufacturing prowess and rapid adoption of advanced technologies. North America and Europe also represent significant markets, driven by technological advancements and growing consumer demand for integrated smart devices. Restraints, such as potential manufacturing complexities and cost considerations in the initial stages of development, are being steadily overcome by ongoing research and development efforts and economies of scale.

The global market for Optically Transparent Antennas (OTAs) is poised for a remarkable surge, projected to reach $X.XX billion by 2033, experiencing a significant CAGR of XX% during the forecast period of 2025-2033. This burgeoning demand is intricately linked to the insatiable need for seamless wireless connectivity integrated discreetly into everyday objects and structures. The historical period of 2019-2024 witnessed initial research and development, laying the groundwork for the commercialization and widespread adoption seen in the base year of 2025 and beyond. The evolution of materials science, particularly in conductive transparent films and inks, has been a pivotal factor, enabling the creation of antennas that are both highly functional and aesthetically unobtrusive. As we move through the study period of 2019-2033, the landscape of OTA technology is characterized by an increasing focus on achieving higher transparency levels, particularly the 98% transparent segment, which is expected to garner substantial market share. Concurrently, the 90% transparent segment will continue to be a strong contender, offering a balance between transparency and performance for a wider range of applications. The "Others" category, encompassing novel transparency levels and specialized material compositions, will also contribute to the market's dynamism. The demand is driven by advancements in miniaturization and the integration of antennas into increasingly complex electronic devices, pushing the boundaries of what is technologically feasible. The market is also observing a growing emphasis on sustainable manufacturing practices and the exploration of eco-friendly materials for OTA production. This includes research into bio-based conductive materials and recyclable substrates, aligning with global environmental initiatives. The future of OTAs will be defined by innovation in material conductivity, electromagnetic performance optimization, and the development of cost-effective manufacturing processes to facilitate mass production. This growth trajectory suggests that OTAs will transition from a niche technology to an indispensable component in a multitude of consumer electronics, automotive systems, and smart infrastructure. The continuous innovation in this field is set to redefine how we interact with wireless technology, making it an integral and invisible part of our environment. The market's expansion is also fueled by increasing investments in R&D by leading players, aiming to overcome existing limitations and unlock new application frontiers.

The exponential growth of the Optically Transparent Antennas (OTAs) market is fundamentally propelled by an undeniable convergence of technological advancements and evolving consumer preferences. The relentless pursuit of seamless and aesthetically pleasing integration of electronic components within devices and environments is a primary driver. As electronic devices become more ubiquitous and integrated into our daily lives, the demand for antennas that are virtually invisible – offering high optical transparency – has skyrocketed. This is particularly evident in the burgeoning mobile display technologies sector, where smartphone and tablet manufacturers are striving for edge-to-edge displays and minimal visible components. Furthermore, the rapid expansion of the Internet of Things (IoT) ecosystem necessitates a proliferation of connected devices, many of which require discreet antenna solutions. Smart buildings, wearables, and advanced automotive systems all represent significant growth avenues where the unobtrusive nature of OTAs is a critical differentiator. The increasing sophistication of materials science has unlocked the potential for conductive transparent films and inks with enhanced performance characteristics, including improved conductivity, durability, and flexibility, which are essential for widespread adoption. The desire for enhanced user experience, free from bulky and visible antennas, is a powerful motivator for product designers and engineers across industries. This, coupled with the increasing pervasiveness of wireless communication standards and the constant demand for faster and more reliable connectivity, creates a fertile ground for OTA market expansion. The ongoing advancements in manufacturing techniques, such as roll-to-roll processing and inkjet printing, are also making OTA production more cost-effective and scalable, further accelerating their adoption.

Despite the promising outlook, the Optically Transparent Antennas (OTAs) market faces several significant challenges and restraints that could temper its growth trajectory. A primary hurdle remains the inherent trade-off between optical transparency and electromagnetic performance. Achieving extremely high transparency, especially in the 98% transparent category, often comes at the expense of antenna efficiency, gain, and bandwidth. This delicate balance requires sophisticated material engineering and antenna design to ensure optimal functionality without compromising visual aesthetics. The cost of manufacturing advanced transparent conductive materials, such as indium tin oxide (ITO) and newer alternatives like silver nanowires and graphene, can still be prohibitive for mass-market applications, especially when compared to traditional antenna technologies. This cost factor is a significant restraint, particularly for price-sensitive segments. Furthermore, the durability and long-term reliability of these transparent conductive materials in various environmental conditions, including exposure to moisture, UV radiation, and physical stress, remain a concern. Ensuring the longevity and consistent performance of OTAs over the lifespan of the product is crucial for widespread adoption and customer satisfaction. The complexity of integrating OTAs into existing manufacturing processes also presents a challenge for some industries. Developing new fabrication techniques and ensuring compatibility with existing production lines requires significant investment and expertise. Finally, a lack of standardization in performance metrics and testing methodologies can create confusion for designers and consumers, hindering the establishment of clear performance benchmarks and market trust. Overcoming these challenges will be critical for unlocking the full potential of the OTA market.

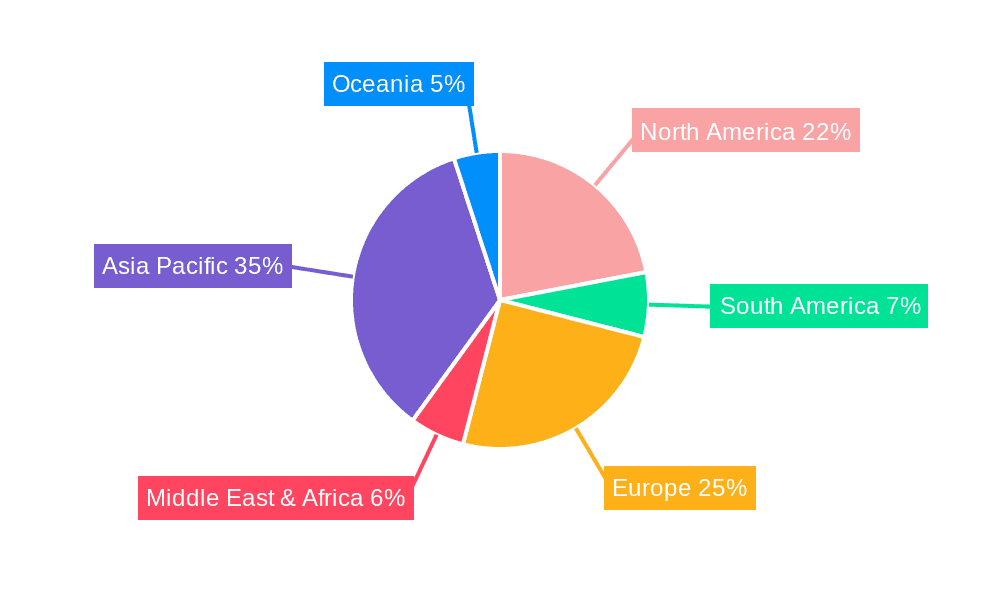

The global Optically Transparent Antennas (OTAs) market is poised for significant growth, with the Asia-Pacific region emerging as a dominant force, largely driven by its robust electronics manufacturing ecosystem and the burgeoning demand from its vast consumer base. Countries like China, South Korea, and Taiwan are at the forefront of technological innovation and production, housing major players in both material science and electronic device manufacturing. This region's dominance is further amplified by its leading role in the Mobile Display Technologies segment. The sheer volume of smartphone, tablet, and wearable device production in Asia-Pacific, coupled with the increasing consumer demand for sleeker, bezel-less designs, makes it a natural hub for the adoption of OTAs. The push for higher transparency levels, particularly the 98% transparent segment, is directly fueled by the aesthetic requirements of premium mobile devices manufactured in this region.

Furthermore, the Automotive sector within Asia-Pacific is also a significant contributor to OTA market dominance. As vehicles become increasingly connected and equipped with advanced infotainment systems, 5G capabilities, and autonomous driving features, the need for integrated and aesthetically pleasing antenna solutions is paramount. The adoption of OTAs in automotive displays, windows, and body panels is gaining traction, driven by both design considerations and the functional necessity of reliable wireless communication.

The World Optically Transparent Antennas Production within the Asia-Pacific region is characterized by a concentration of leading material suppliers and antenna manufacturers, fostering a competitive environment that drives innovation and cost reduction. This region's ability to rapidly scale production and adapt to evolving technological demands positions it as the primary driver of global OTA output.

While Asia-Pacific leads, North America and Europe are also significant markets, particularly for the Smart Buildings and Satellite applications. The increasing adoption of smart home technologies and the deployment of next-generation satellite communication systems are creating new opportunities for OTAs in these regions. However, the sheer scale of mobile device production and the aggressive pace of technological integration in Asia-Pacific are expected to keep it at the helm of the global OTA market in terms of both production and consumption throughout the forecast period. The continuous investment in research and development by companies based in this region, coupled with supportive government policies aimed at fostering technological advancement, further solidifies its leading position.

The Optically Transparent Antennas (OTAs) industry is experiencing powerful growth catalysts that are shaping its future. The ever-increasing demand for seamless integration of wireless connectivity into everyday objects, driven by the Internet of Things (IoT) and the proliferation of smart devices, is a primary catalyst. As consumers and industries prioritize aesthetics and minimalist design, OTAs offer a solution that enhances user experience by being virtually invisible. Furthermore, advancements in materials science, particularly in the development of highly conductive and transparent thin films, are enabling the creation of more efficient and cost-effective OTAs. The continuous push for higher data speeds and more reliable wireless communication, such as the rollout of 5G technology, necessitates innovative antenna solutions that can be integrated into a wider range of form factors.

This comprehensive report delves into the intricate dynamics of the Optically Transparent Antennas (OTAs) market, providing in-depth analysis and strategic insights for stakeholders. Covering the study period of 2019-2033, with a base year of 2025, the report offers a robust understanding of market trends, driving forces, and challenges. It meticulously analyzes key segments such as 90% Transparent, 98% Transparent, and Others, alongside production volumes and application areas including Mobile Display Technologies, Automotive, Satellite, Smart Buildings, and Others. The report presents a forward-looking perspective on industry developments and identifies the leading players shaping the OTA landscape. Through detailed market sizing, segmentation, and regional analysis, this report equips businesses with the knowledge needed to navigate this rapidly evolving sector and capitalize on emerging opportunities, projecting a market value of $X.XX billion by 2033.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 20%.

Key companies in the market include Meta Materials Inc, CHASM Advanced Materials, ALCAN Systems, AGC, DONGWOO FINE-CHEM, Dengyo, VENTI Group, Taoglas, Nippon Electric Glass, Kreemo (and Sivers Semiconductors).

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Optically Transparent Antennas," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Optically Transparent Antennas, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.