1. What is the projected Compound Annual Growth Rate (CAGR) of the Nuclear Waste Material Disposal?

The projected CAGR is approximately XX%.

Nuclear Waste Material Disposal

Nuclear Waste Material DisposalNuclear Waste Material Disposal by Application (Nuclear Power Industry, Defense & Research), by Type (Low Level Waste, Medium Level Waste, High Level Waste), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

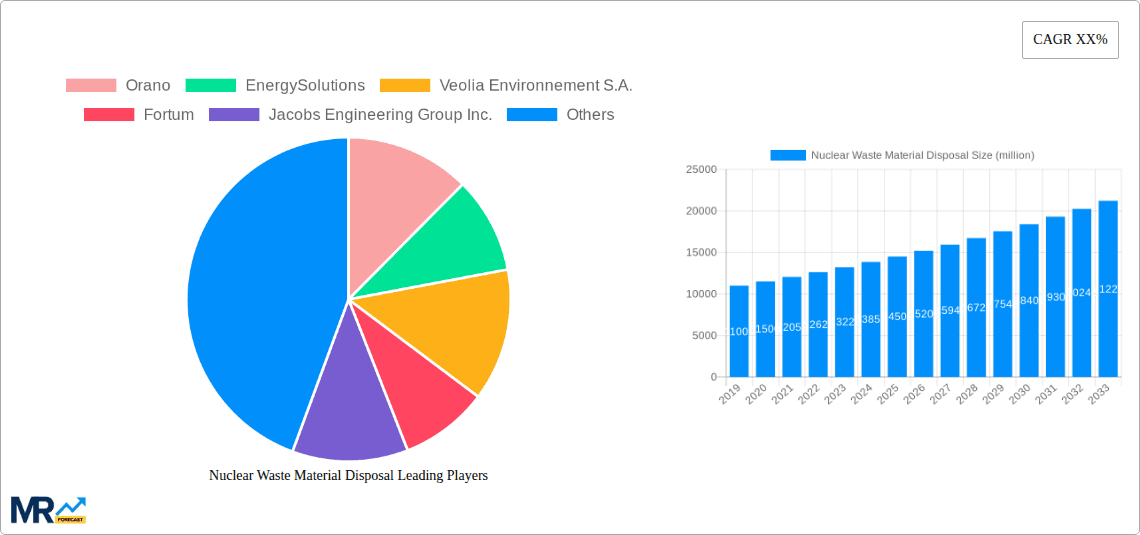

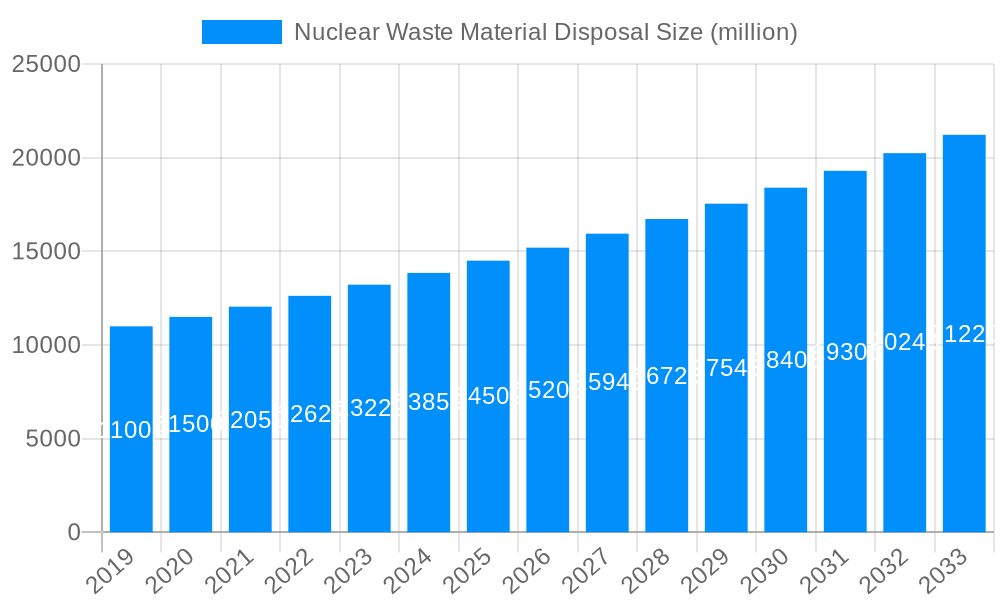

The global Nuclear Waste Material Disposal market is poised for significant expansion, driven by the increasing global demand for energy and the continued reliance on nuclear power as a low-carbon energy source. With a projected market size of approximately $15,500 million, the industry is set to experience a compound annual growth rate (CAGR) of around 5.2% from 2019 to 2033. This robust growth is fueled by the need for safe, secure, and environmentally responsible management of radioactive waste generated from nuclear power plants, research facilities, and defense applications. Key drivers include stringent regulatory frameworks, advancements in disposal technologies such as deep geological repositories and modular reactor waste solutions, and the ongoing decommissioning of aging nuclear facilities worldwide. The demand for efficient disposal solutions for low-level waste (LLW) and medium-level waste (MLW) is particularly high, though the long-term challenges associated with high-level waste (HLW) continue to shape research and investment. Emerging economies with expanding nuclear programs are also becoming crucial markets.

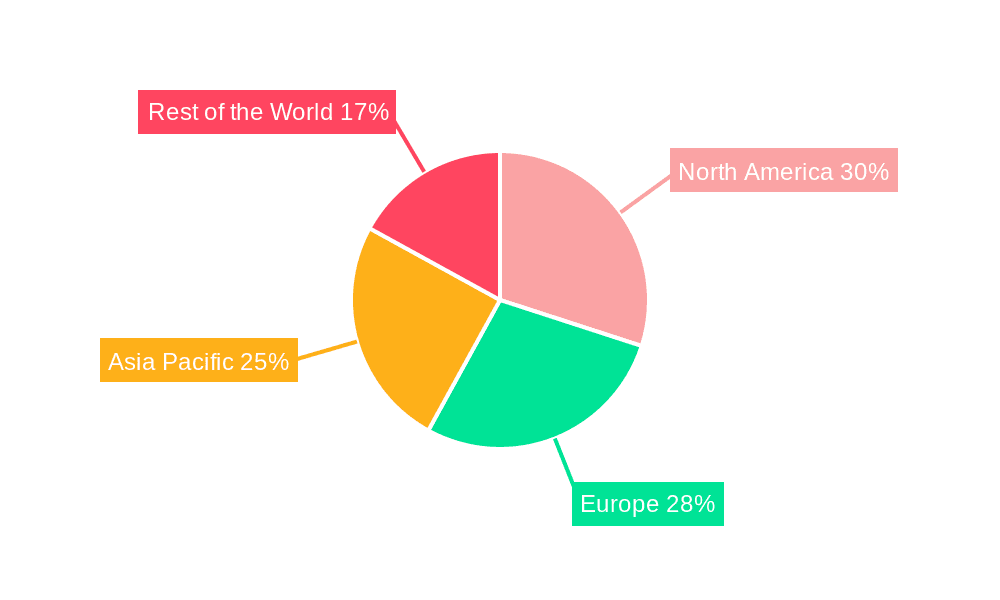

The competitive landscape features a mix of established players and specialized service providers, including Orano, EnergySolutions, Veolia Environnement S.A., and Westinghouse Electric Company LLC. These companies are actively investing in R&D to develop innovative disposal and management techniques, focusing on cost-effectiveness and adherence to international safety standards. Geographically, North America and Europe currently dominate the market due to their established nuclear infrastructure and mature regulatory environments. However, the Asia Pacific region, led by China and India, is expected to witness the fastest growth due to substantial investments in new nuclear power capacity. Restraints such as the high cost of developing and maintaining disposal facilities, public perception, and the long lead times for regulatory approvals present ongoing challenges. Nevertheless, the overarching imperative for sustainable and secure nuclear waste management ensures a positive outlook for the market.

This report offers a comprehensive analysis of the global Nuclear Waste Material Disposal market, providing in-depth insights into market dynamics, key trends, and future projections. Spanning a Study Period of 2019-2033, with a Base Year and Estimated Year of 2025, and a Forecast Period of 2025-2033, the report meticulously examines the Historical Period from 2019-2024. It leverages extensive quantitative data, with market values often expressed in the million unit, to present a robust understanding of this critical sector.

XXX – The global nuclear waste material disposal market is undergoing a transformative phase, driven by an escalating need for secure and sustainable management of radioactive byproducts. The Nuclear Power Industry continues to be a primary generator of nuclear waste, with a growing installed capacity worldwide necessitating advanced disposal solutions. Concurrently, the Defense & Research sector, encompassing legacy waste from weapons programs and ongoing scientific endeavors, also contributes significantly to the overall waste stream. A key trend observed is the increasing investment in research and development for novel disposal technologies, moving beyond traditional containment methods towards more permanent and geologically stable solutions. The market is witnessing a gradual shift in the types of waste being prioritized for disposal, with a growing emphasis on the safe handling and long-term isolation of High Level Waste (HLW), which poses the most significant radiological hazard. While Low Level Waste (LLW) and Medium Level Waste (MLW) still constitute a substantial portion of the waste volume, the complexity and cost associated with HLW disposal are driving innovation and creating specialized market segments. Regulatory frameworks are also evolving, becoming more stringent and harmonized globally, pushing companies to adopt best practices and invest in state-of-the-art infrastructure. This evolving landscape is fostering a more consolidated market, with leading players demonstrating a commitment to technological advancement and environmental stewardship. The demand for integrated waste management solutions, encompassing collection, treatment, transportation, and final disposal, is also on the rise, creating opportunities for full-service providers. Furthermore, the growing public awareness and concern surrounding nuclear safety and environmental protection are exerting pressure on governments and industries to adopt the most responsible and secure disposal practices. This heightened scrutiny is a significant factor shaping market trends and investment decisions. The market is characterized by a substantial but steadily growing revenue, projected to expand significantly over the forecast period as aging nuclear facilities are decommissioned and new ones come online, all requiring robust waste management strategies.

The nuclear waste material disposal market is propelled by a confluence of powerful forces, with the sustained and indeed expanding global reliance on nuclear energy serving as a primary engine. As nations continue to invest in nuclear power as a low-carbon energy source to combat climate change, the generation of associated radioactive waste is an inherent consequence that demands responsible management. This inherent generation necessitates continuous advancements and investments in disposal infrastructure. Simultaneously, the legacy of decades of defense activities, including nuclear weapons development and testing, has left behind significant volumes of nuclear waste that require secure and long-term isolation. The global push towards decommissioning aging nuclear power plants, a process that inherently produces large quantities of LLW and MLW, also acts as a significant market driver, requiring specialized disposal services. Furthermore, stringent and increasingly harmonized international and national regulations are compelling stakeholders to adopt safer, more secure, and environmentally sound disposal practices, thereby stimulating demand for compliant solutions and technologies. The growing awareness of the long-term risks associated with radioactive materials and the commitment to intergenerational equity are fostering a proactive approach to waste management, encouraging the development and implementation of advanced disposal strategies.

Despite the robust growth potential, the nuclear waste material disposal market faces significant challenges and restraints that can impede its trajectory. The most prominent of these is the immense public perception and political sensitivity surrounding the disposal of radioactive materials. The "Not In My Backyard" (NIMBY) phenomenon often leads to protracted permitting processes and significant public opposition, delaying or even halting the development of crucial disposal facilities. The extremely long half-lives of certain radioactive isotopes present a formidable technical challenge, requiring disposal solutions that can ensure containment and isolation for millennia, a feat that demands cutting-edge engineering and extensive geological studies. The substantial capital investment required for establishing and operating state-of-the-art disposal facilities, particularly for High Level Waste, can be a significant barrier, especially for smaller companies or in regions with limited financial resources. Moreover, the absence of universally accepted, permanent deep geological repositories for High Level Waste in many parts of the world creates uncertainty and necessitates interim storage solutions, adding complexity and cost to the overall waste management chain. The potential for accidental releases or security breaches, however remote, also necessitates rigorous safety protocols and constant vigilance, contributing to operational costs and public concern. Finally, the evolving regulatory landscape, while driving progress, can also introduce complexities and compliance burdens that require continuous adaptation and investment.

The global nuclear waste material disposal market is characterized by distinct regional strengths and dominant segments, with a pronounced concentration of activity and investment in specific geographical areas and waste types.

Dominant Regions/Countries:

North America (United States & Canada):

Europe (France, UK, Sweden, Finland):

Asia-Pacific (China, Japan, South Korea):

Dominant Segments:

High Level Waste (HLW):

Nuclear Power Industry (Application):

The nuclear waste material disposal industry is propelled by several key growth catalysts. The increasing global demand for clean energy, leading to the expansion of nuclear power, directly translates into higher volumes of radioactive waste requiring disposal. Furthermore, the ongoing decommissioning of aging nuclear power plants worldwide necessitates robust waste management solutions. Advancements in disposal technologies, particularly for High Level Waste, are unlocking new possibilities and attracting investment. Stricter environmental regulations and a growing emphasis on public safety are compelling stakeholders to adopt more advanced and secure disposal practices, thereby driving innovation and market growth.

This report offers unparalleled comprehensive coverage of the nuclear waste material disposal market, delving into every facet of this complex industry. It provides granular analysis of market segmentation by application, type of waste, and key regional players. The report scrutinizes the intricate interplay of driving forces, challenges, and future growth catalysts, painting a clear picture of the market's evolution. With in-depth insights into industry developments and a detailed overview of leading companies, this report is an indispensable resource for stakeholders seeking to understand the current landscape and anticipate future trends in this vital sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Orano, EnergySolutions, Veolia Environnement S.A., Fortum, Jacobs Engineering Group Inc., Fluor Corporation, Swedish Nuclear Fuel and Waste Management CompanyGC Holdings Corporation, Westinghouse Electric Company LLC, Waste Control Specialists, LLC, Perma-Fix Environmental Services, Inc., US Ecology, Inc., Stericycle, Inc., SPIC Yuanda Environmental Protection Co., Ltd, Anhui Yingliu Electromechanical Co., Ltd., Chase Environmental Group, Inc., .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Nuclear Waste Material Disposal," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Nuclear Waste Material Disposal, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.