1. What is the projected Compound Annual Growth Rate (CAGR) of the Ntered Carbon Steel?

The projected CAGR is approximately 5.5%.

Ntered Carbon Steel

Ntered Carbon SteelNtered Carbon Steel by Type (Additive Manufacturing (AM), Traditional Manufacturing, Metal Injection Molding (MIM)), by Application (Electrical, Industrial, Transportation), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

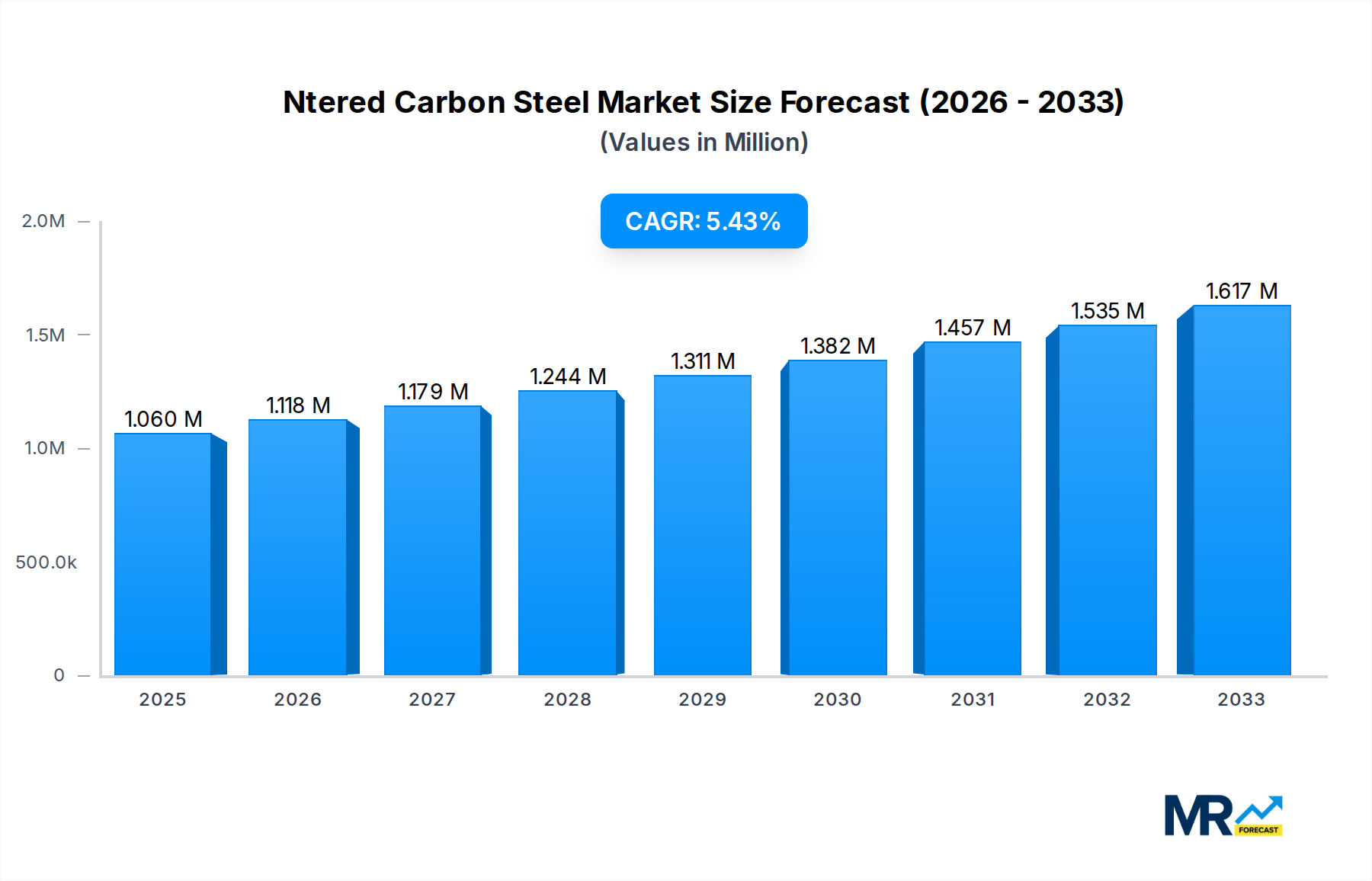

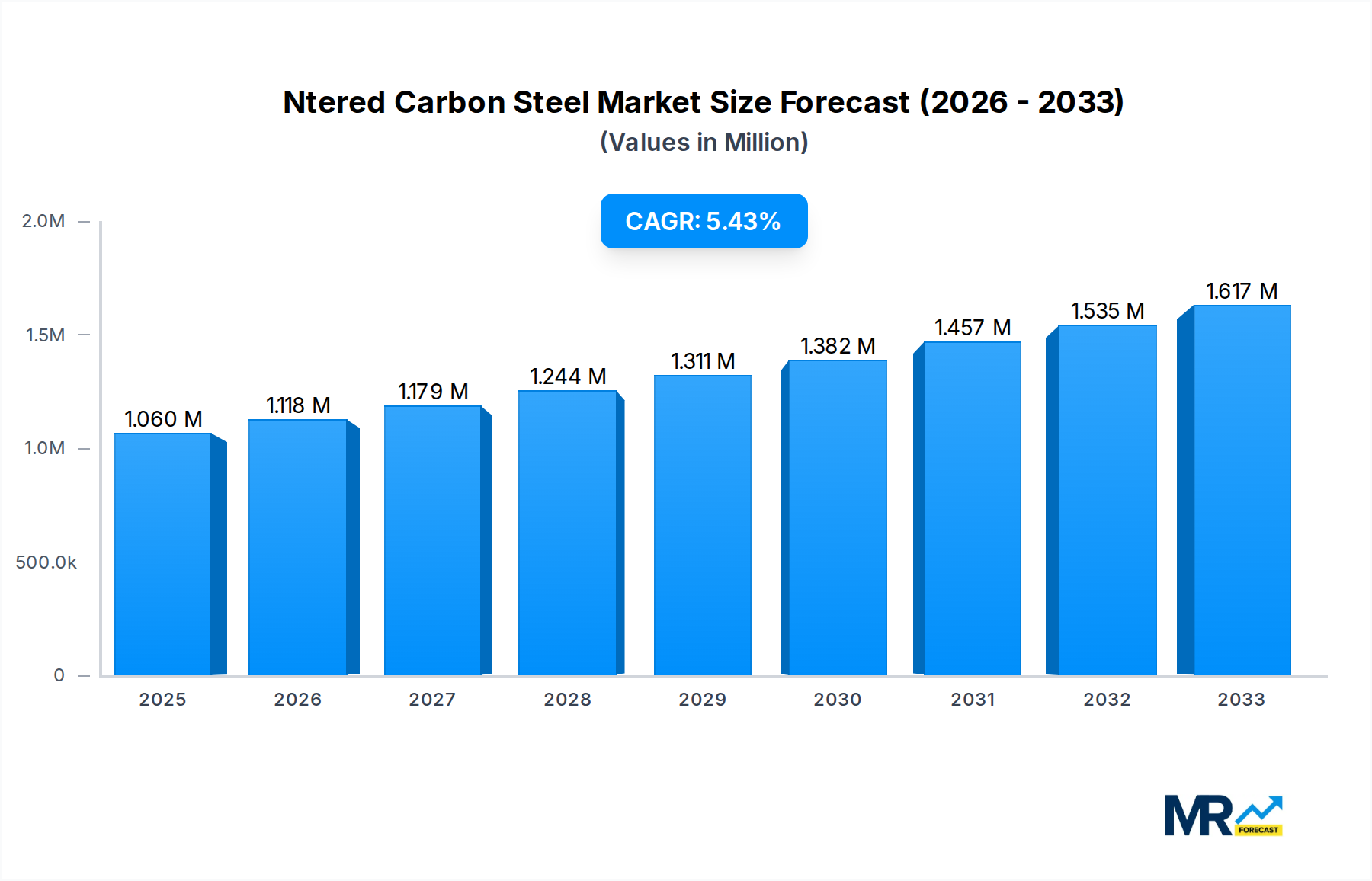

The sintered carbon steel market is poised for robust expansion, projected to reach a substantial value of \$1059.6 billion by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 5.5% throughout the forecast period of 2025-2033. This impressive growth trajectory is underpinned by several key drivers, prominently featuring the increasing adoption of Additive Manufacturing (AM) technologies, which are revolutionizing component production by offering enhanced precision, design flexibility, and material efficiency. Furthermore, the burgeoning demand from the transportation sector, driven by the lightweighting trend for improved fuel efficiency and the increasing complexity of automotive components, significantly fuels market expansion. Traditional manufacturing methods continue to hold relevance, especially for high-volume applications where cost-effectiveness is paramount, while Metal Injection Molding (MIM) is gaining traction for intricate parts requiring high precision and complex geometries, particularly within the electrical and industrial segments.

The market's dynamism is further shaped by prevailing trends such as the growing emphasis on sustainable manufacturing practices, leading to a preference for materials and processes that minimize waste and energy consumption. Advancements in powder metallurgy and sintering techniques are also contributing to improved material properties, leading to higher-performance sintered carbon steel components. However, the market faces certain restraints, including the initial capital investment required for advanced sintering equipment and the fluctuating prices of raw materials, which can impact manufacturing costs. Despite these challenges, the consistent demand for durable, cost-effective, and high-performance metal components across a wide array of industries, coupled with ongoing technological innovations, positions the sintered carbon steel market for sustained and significant growth in the coming years.

This comprehensive report delves into the intricate world of sintered carbon steel, providing an in-depth analysis of its market dynamics, technological advancements, and future trajectory. With a meticulous Study Period spanning 2019-2033, the report leverages a robust Base Year of 2025 to offer precise market valuations and forecasts. The Estimated Year is also 2025, allowing for a clear snapshot of the current market landscape. The Forecast Period extends from 2025-2033, projecting future growth and opportunities, while the Historical Period of 2019-2024 provides essential context for understanding past trends and performance. The report aims to equip stakeholders with actionable insights and strategic intelligence in this evolving sector.

The sintered carbon steel market is experiencing a dynamic evolution, driven by a confluence of technological innovation, shifting industrial demands, and a growing emphasis on sustainable manufacturing practices. Throughout the Historical Period (2019-2024), the market demonstrated steady growth, underpinned by the inherent advantages of sintered components – their cost-effectiveness, precise geometry, and desirable material properties. As we move into the Base Year (2025) and the subsequent Forecast Period (2025-2033), several key trends are shaping the landscape. One prominent trend is the increasing adoption of Metal Injection Molding (MIM) for producing complex, high-volume parts, offering intricate designs and exceptional material density. This segment is projected to witness substantial expansion due to its suitability for miniaturization and its ability to achieve near-net-shape components, reducing post-processing costs.

Another significant trend is the growing application of sintered carbon steel in Additive Manufacturing (AM). While still an emerging area, AM is enabling the creation of highly customized and geometrically complex parts that were previously impossible to fabricate using traditional methods. This opens up new avenues for innovation in areas like aerospace, medical devices, and rapid prototyping. Furthermore, the demand for higher performance sintered carbon steel grades, capable of withstanding extreme temperatures, pressures, and corrosive environments, is on the rise. This is fueling research and development into advanced powder metallurgy techniques and novel alloying compositions. The Transportation segment continues to be a major consumer, with an increasing focus on lightweighting and improved fuel efficiency driving the demand for high-strength, low-density sintered parts in engine components, powertrains, and chassis. The Industrial segment also remains a cornerstone, with applications ranging from gears and bearings to structural components in heavy machinery and automation systems. The market’s value is expected to reach billions of dollars by the end of the Forecast Period, reflecting the sustained demand and expanding application spectrum of sintered carbon steel.

Several potent forces are driving the growth and expanding the market for sintered carbon steel. Paramount among these is the unwavering pursuit of cost-efficiency and manufacturing optimization across various industries. Sintering, by its very nature, offers significant advantages in terms of material utilization and reduced waste compared to subtractive manufacturing processes. This inherent cost-effectiveness is particularly attractive in high-volume production scenarios. Secondly, the increasing demand for intricate and complex part geometries is a significant propellant. Advanced sintering techniques, such as Metal Injection Molding (MIM), allow for the creation of highly detailed components with tight tolerances, enabling product designers to achieve innovative solutions that were previously unfeasible. This capability is crucial in sectors like electronics and medical devices.

Furthermore, the relentless drive for improved material performance and durability across diverse applications is fueling innovation in sintered carbon steel. As industries push the boundaries of operational demands, the need for materials that can withstand higher temperatures, greater stresses, and more demanding environments becomes critical. This necessitates advancements in powder metallurgy, alloying, and sintering processes. The growing emphasis on sustainability and environmental consciousness also plays a role. Sintering processes are generally more energy-efficient and generate less waste than traditional manufacturing methods, aligning with the global push for greener industrial practices. Finally, the continuous evolution and refinement of sintering technologies, coupled with advancements in powder production, are making sintered carbon steel a more versatile and accessible material for a wider range of applications, thus propelling its market forward.

Despite its promising growth trajectory, the sintered carbon steel market faces several challenges and restraints that could impede its full potential. One significant hurdle is the inherent limitation in achieving the same level of mechanical properties, particularly tensile strength and ductility, as conventionally manufactured wrought steel. While sintering offers excellent dimensional accuracy, achieving the ultra-high strength characteristics demanded in certain high-performance applications can still be a challenge, often requiring post-sintering treatments or specialized alloying. Another restraint is the initial capital investment required for advanced sintering equipment and tooling. For smaller manufacturers or those transitioning from traditional methods, the upfront cost can be a barrier to entry, limiting wider adoption.

The complexity of achieving uniform density and avoiding porosity throughout larger or more intricate sintered parts can also pose a challenge. Inconsistent density can lead to variations in mechanical properties and potential failure points, necessitating stringent quality control measures. Furthermore, the market is sensitive to fluctuations in the price and availability of raw material powders, particularly specialized alloys, which can impact manufacturing costs and profit margins. Competition from alternative manufacturing processes, such as advanced casting, forging, or even additive manufacturing using different material types, also presents a continuous competitive pressure. Finally, the need for specialized expertise and skilled labor to operate and maintain advanced sintering equipment, as well as to design parts optimized for the sintering process, can be a limiting factor in certain regions.

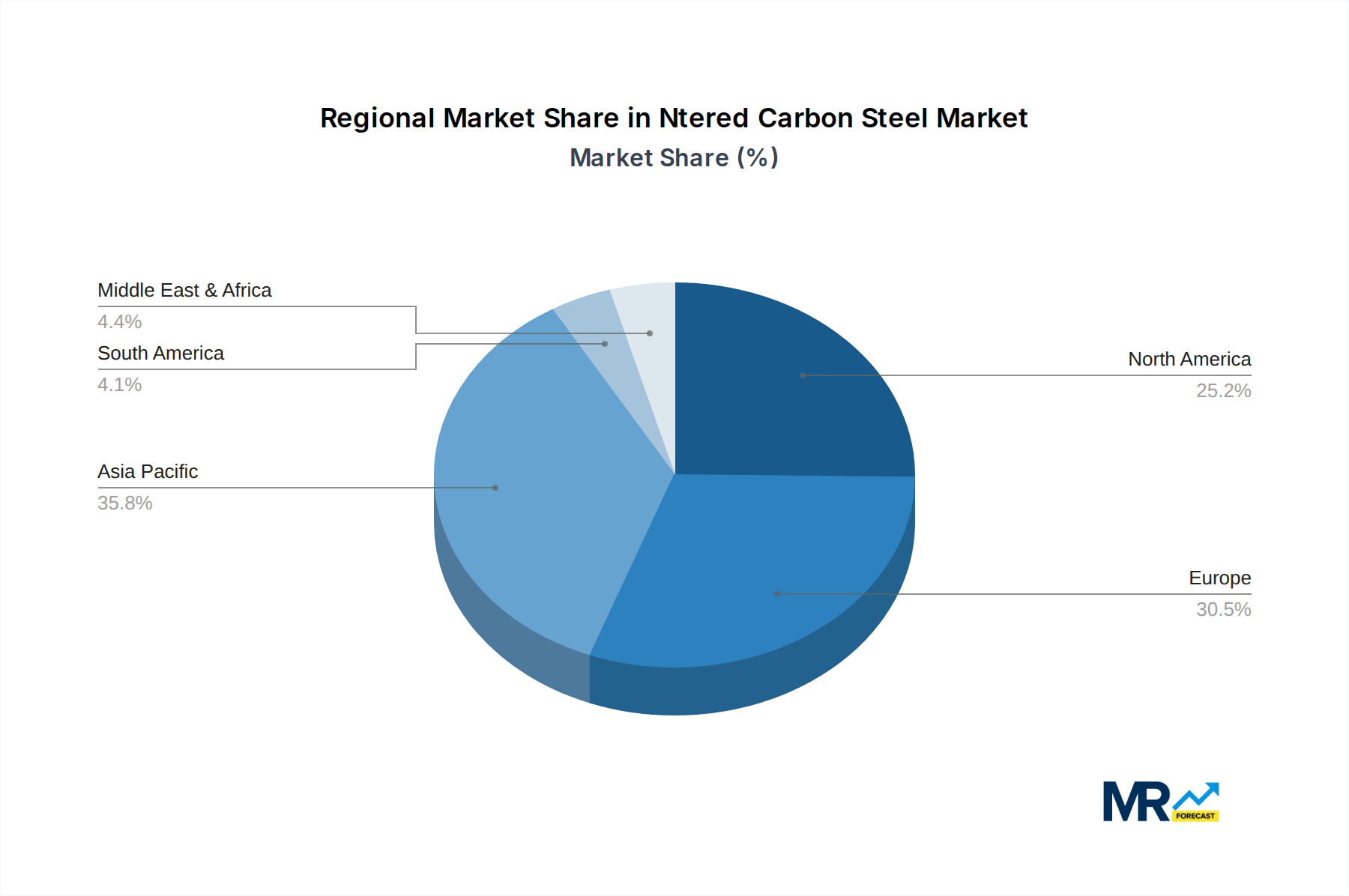

The sintered carbon steel market's dominance is a complex interplay of regional manufacturing prowess and specific segment demands. Among the regions, Asia-Pacific is poised to be a significant dominant force, driven by its robust manufacturing base, particularly in China and India. The presence of a large and growing automotive industry, a major consumer of sintered components, coupled with expanding industrial and electrical sectors, provides a fertile ground for market growth. Governments in these regions are also actively promoting domestic manufacturing and technological advancements, further catalyzing the adoption of sintered carbon steel. The region's cost-competitiveness in manufacturing, coupled with a burgeoning demand for high-performance and precision components, solidifies its leading position.

Within the Asia-Pacific region, China stands out as a critical hub due to its extensive manufacturing ecosystem, encompassing everything from raw material production to finished component assembly. Its sheer scale of industrial output and its integral role in global supply chains make it a primary driver of demand for sintered carbon steel. Countries like India are also experiencing rapid industrialization, with a growing automotive sector and increasing investments in infrastructure and manufacturing, further bolstering the market.

When examining the Segments, Transportation emerges as a clear dominant force. The automotive industry's continuous pursuit of lightweighting for improved fuel efficiency and reduced emissions, coupled with the need for durable and cost-effective engine, transmission, and chassis components, makes sintered carbon steel an indispensable material. The ability to produce complex shapes like gears, cams, and connecting rods with high precision and in high volumes is crucial for automotive manufacturers.

The Industrial segment also holds substantial sway. This broad category encompasses a vast array of applications, including power tools, agricultural machinery, industrial automation, fluid power systems, and home appliances. The demand for reliable, wear-resistant, and dimensionally stable components in these applications consistently drives the consumption of sintered carbon steel. The cost-effectiveness and design flexibility offered by sintering are highly valued in this diverse and extensive market.

While Metal Injection Molding (MIM) is a rapidly growing type of manufacturing within the sintered carbon steel landscape, and Electrical applications are also significant, the sheer volume and consistent demand from the Transportation and broad Industrial sectors cement their dominance in terms of market share and influence. The continuous innovation in these two segments, directly translating into increased demand for sintered carbon steel components, ensures their leading position in shaping the market's future. The forecast period (2025-2033) is expected to see these trends solidify, with Asia-Pacific at the forefront and Transportation and Industrial segments leading the charge in terms of consumption and application development.

The sintered carbon steel industry is fueled by several key growth catalysts. The relentless pursuit of cost-effective manufacturing solutions across sectors, especially in high-volume applications, positions sintering as a preferred choice. Advancements in powder metallurgy and sintering technologies are enabling the production of increasingly complex and high-performance components, broadening the material's applicability. The growing demand for lightweight and durable parts in the automotive and aerospace industries, driven by efficiency and sustainability goals, is a significant catalyst. Furthermore, the expanding use of sintered carbon steel in emerging technologies and the continuous innovation in material science are opening up new avenues for growth, ensuring a dynamic and upward market trajectory.

This report provides a holistic view of the sintered carbon steel market, encompassing a detailed examination of its various facets. Beyond the trends, drivers, and challenges, the report meticulously analyzes the market's segmentation by type and application, offering granular insights into the performance and potential of segments like Additive Manufacturing (AM), Traditional Manufacturing, Metal Injection Molding (MIM), and applications in Electrical, Industrial, and Transportation sectors. It delves into the strategic initiatives and technological advancements undertaken by key players, as well as the potential for mergers and acquisitions that could reshape the competitive landscape. The report also scrutinizes the regulatory environment and its potential impact on market growth, providing a complete picture for informed strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.5%.

Key companies in the market include Advanced Technology(Bazhou)Special Powder, AMES Sintered Metallic Components, ASCO Sintering, Capstan, Changsha Hualiu Metal Powders Ltd(HL Powder), CNPC Powder North America, Erasteel India Private, Federal-Mogul Goetze, Fine Sinter, GKN, Hitachi Chemical Company, Hitachi Chemical Sintercom India, Hoganas AB, Miba AG, POLEMA, Pometon, Samvardhana Motherson Group, Samvardhana Motherson Group, Sandvik, Schunk Sintermetalltechnik GmbH, Sintercom India Limited, SMC Corporation, SSI Sintered Specialties, Sumitomo Electric Industries Limited, Technymon Global Bearing Technologies, United States Metal Powders, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Ntered Carbon Steel," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Ntered Carbon Steel, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.