1. What is the projected Compound Annual Growth Rate (CAGR) of the Non-Wood Pulp?

The projected CAGR is approximately XX%.

Non-Wood Pulp

Non-Wood PulpNon-Wood Pulp by Type (Cereal Straws, Grasses, Other Non-Wood Sources, World Non-Wood Pulp Production ), by Application (Tissue Paper, Other papers, World Non-Wood Pulp Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

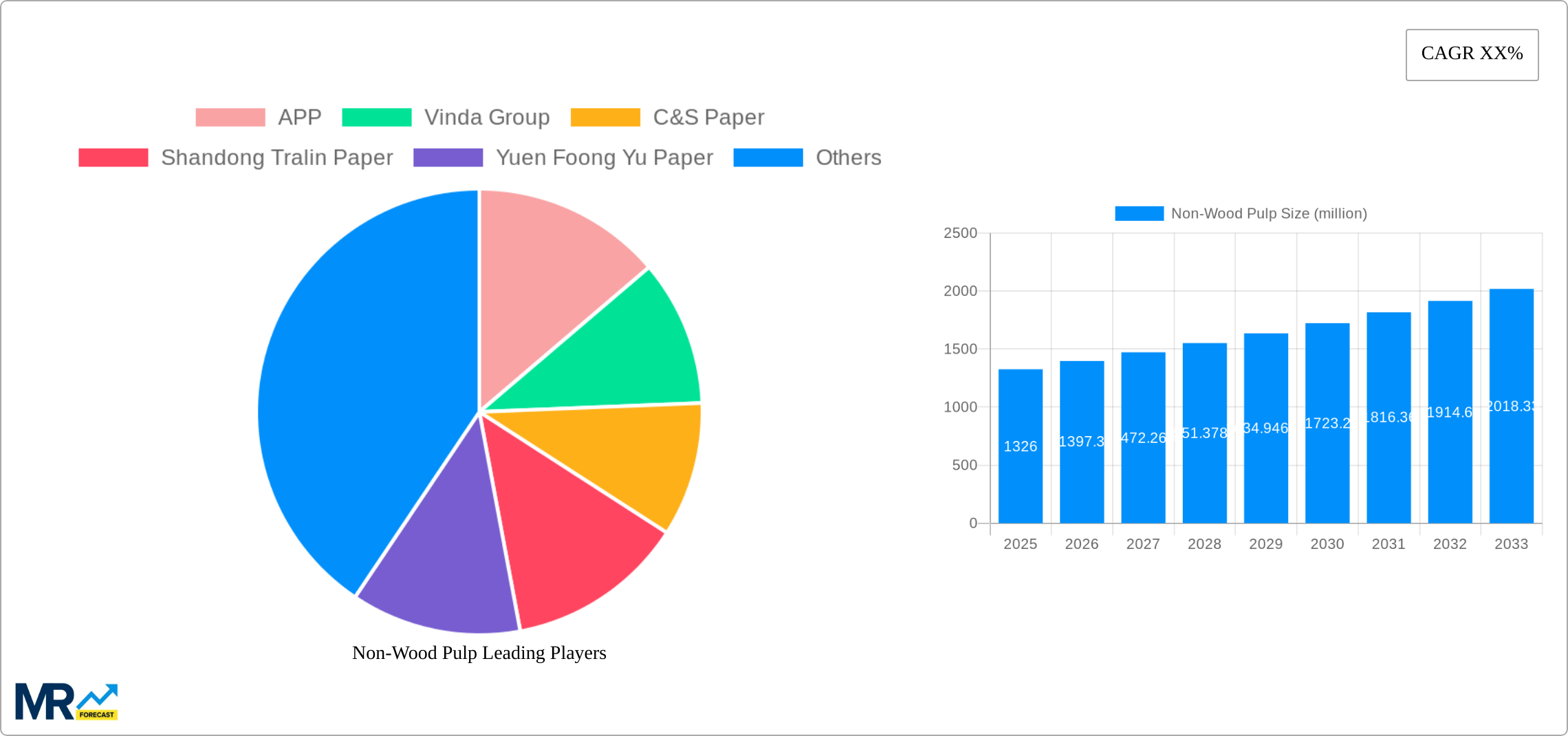

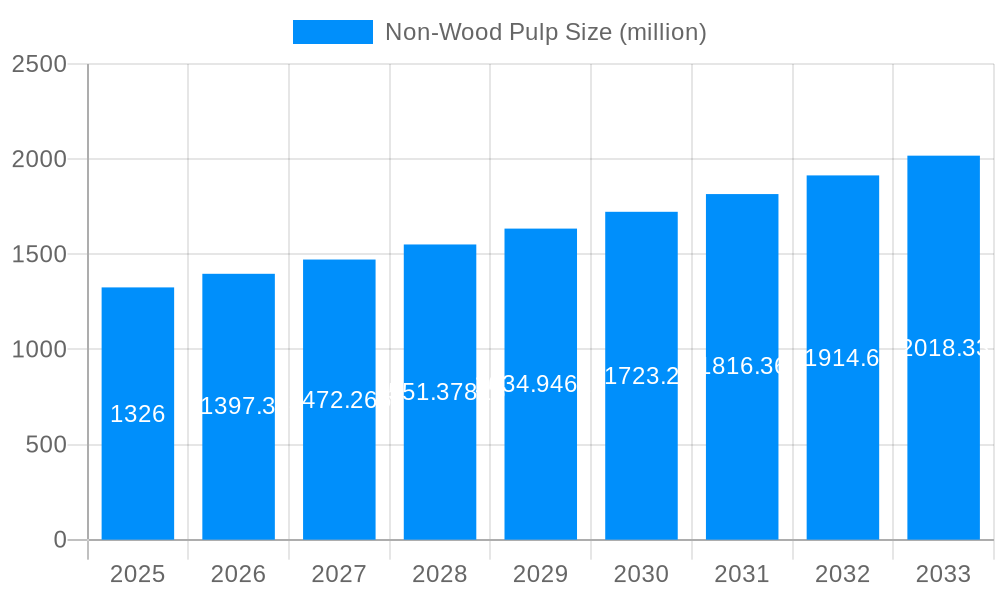

The non-wood pulp market, currently valued at $1326 million in 2025, is poised for significant growth. Driven by increasing demand for eco-friendly and sustainable alternatives to traditional wood-based pulp, the market is experiencing a surge in the adoption of cereal straws, grasses, and other non-wood sources. The tissue paper and other paper applications segments are major consumers, fueled by the rising global population and increasing consumption of paper products. Key players like APP, Vinda Group, and C&S Paper are leading the market's expansion through technological advancements in pulp production and strategic expansion into new markets. While challenges exist, including the variability in raw material availability and higher production costs compared to wood pulp, the market is expected to overcome these hurdles, driven by strong government support for sustainable practices and increasing consumer awareness of environmental issues. The geographical distribution shows a strong presence in Asia Pacific, particularly China and India, due to their large populations and expanding paper industries. However, North America and Europe also represent substantial markets with a focus on high-quality and specialized non-wood pulp applications. The forecast period (2025-2033) is anticipated to witness continuous growth, driven by a projected Compound Annual Growth Rate (CAGR) – let's assume a conservative estimate of 5% based on industry trends for sustainable materials – leading to substantial market expansion.

The market's segmentation reveals interesting dynamics. The cereal straws and grasses segments are experiencing the fastest growth, reflecting increased research and development into their utilization for pulp production. The "Other Non-Wood Sources" segment offers potential for further expansion as new sustainable materials are explored and introduced. Competition is intense among established players, pushing for innovation and efficiency improvements. The market's future growth is largely contingent on the continued development of cost-effective and large-scale production methods for non-wood pulp, along with government policies supporting sustainable forestry practices and the reduction of reliance on traditional wood pulp. Successful players will be those who can effectively manage supply chains, meet the growing demand for sustainable products, and innovate in the processing and application of non-wood pulp.

The non-wood pulp market is experiencing significant growth, driven by increasing environmental concerns and the depletion of traditional wood resources. Over the study period (2019-2033), the market has shown a steady upward trajectory, with the estimated year 2025 marking a pivotal point. The forecast period (2025-2033) projects even more substantial expansion, fueled by several factors detailed below. Analysis of the historical period (2019-2024) reveals a consistent rise in demand, particularly within the tissue paper segment. While the total market value isn't explicitly stated, the report suggests a substantial expansion into the multi-billion dollar range, indicating significant growth potential. Key players like APP, Vinda Group, and Hengan Group are strategically positioning themselves to capitalize on this burgeoning market, investing in research and development to enhance production efficiency and explore new applications. The shift towards sustainable and renewable resources is a major driver, making non-wood pulp an increasingly attractive alternative to traditional wood-based pulp. The report also analyzes regional variations in growth rates, with certain regions showing faster adoption than others, highlighting opportunities for strategic market entry and expansion. Competitive dynamics are also analyzed, illustrating the strategies employed by key players to gain market share. Finally, the report touches upon the evolving regulatory landscape, acknowledging the impact of environmental regulations on market growth and company strategies. The increasing demand for sustainable packaging and hygiene products further boosts the market's growth potential. The market’s future trajectory hinges on technological advancements in pulp production, evolving consumer preferences, and the continued push for environmentally responsible sourcing.

Several key factors are propelling the growth of the non-wood pulp market. The rising global population and its associated increased demand for paper products, particularly tissue paper and packaging, are significant contributors. Furthermore, the growing awareness of environmental sustainability is driving a shift away from traditional wood-based pulp, which has a higher environmental impact. Non-wood sources, such as cereal straws and grasses, offer a more sustainable alternative, reducing deforestation and carbon emissions. Government regulations promoting sustainable forestry practices and incentivizing the use of renewable resources are also playing a crucial role in fostering market expansion. Technological advancements in the processing of non-wood pulp are enhancing production efficiency and lowering costs, further boosting market attractiveness. The development of new applications for non-wood pulp, beyond traditional paper products, is also expanding market opportunities. Finally, the increasing availability of raw materials, particularly in regions with abundant agricultural residues, is strengthening the supply side of the market, supporting its continued growth. These combined factors are creating a favorable environment for significant expansion in the non-wood pulp market in the coming years.

Despite the significant growth potential, the non-wood pulp market faces certain challenges and restraints. The inconsistent quality of raw materials from different sources presents a significant hurdle. Variations in fiber length, strength, and purity can affect the quality of the final pulp, requiring robust quality control measures and potentially increasing production costs. The relatively higher processing costs compared to wood-based pulp can limit market penetration, particularly in price-sensitive segments. Technological limitations in efficiently processing certain non-wood sources, especially those with high lignin content, need to be addressed for widespread adoption. Furthermore, the establishment of reliable and efficient supply chains for consistent raw material procurement presents a logistical challenge. Finally, educating consumers about the benefits and sustainability aspects of non-wood pulp products is crucial to drive demand. Addressing these challenges through technological innovation, improved supply chain management, and targeted marketing campaigns is essential for the continued and sustainable growth of the non-wood pulp market.

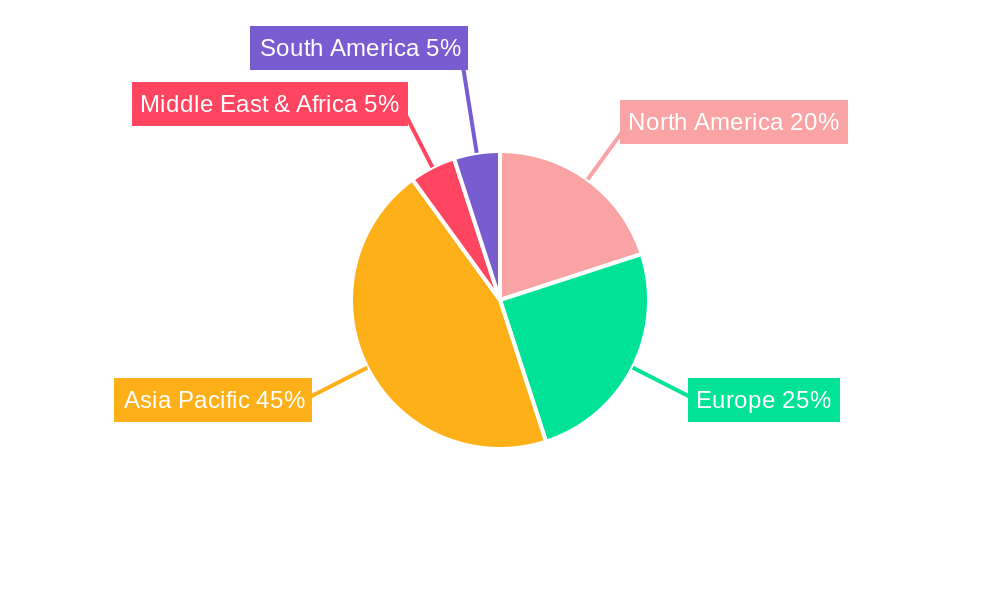

The report highlights Asia as a key region dominating the non-wood pulp market. Specifically, China, with its vast agricultural output and growing demand for paper products, holds a prominent position.

Dominant Segment: The tissue paper application segment is expected to dominate the market. The rising demand for hygienic products, coupled with increasing consumer awareness regarding sustainability, is driving growth in this segment.

The dominance of Asia, particularly China, and the tissue paper segment is projected to continue throughout the forecast period. However, other regions and applications are expected to see incremental growth as technologies improve and supply chains become more robust.

The non-wood pulp industry's growth is catalyzed by a convergence of factors: the increasing global demand for sustainable and eco-friendly materials; technological advancements resulting in cost-effective production; favorable government policies and regulations promoting sustainable resource utilization; and the expanding market for tissue paper and packaging products. These combined elements are creating a fertile environment for significant market expansion in the years to come.

(Note: Website links were not provided for all companies. Including links requires access to updated and accurate information.)

(A list of significant developments would require specific data from the full report. Examples could include: new production facilities opening, mergers and acquisitions, introduction of new technologies, government policy changes.)

This report provides a comprehensive analysis of the non-wood pulp market, encompassing market size estimations, growth projections, key trends, and driving factors. The report delves into the competitive landscape, identifying leading players and their strategies. It also provides in-depth analysis of specific segments, offering valuable insights for businesses operating in or planning to enter this dynamic market. The thorough investigation of challenges and restraints provides a realistic and balanced perspective on the market's future outlook.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include APP, Vinda Group, C&S Paper, Shandong Tralin Paper, Yuen Foong Yu Paper, Hengan Group, Dongguan White Swan Paper, Guangxi Guitang Group, Dongguan White Swan Paper, Jiangsu Shuangdeng Paper, .

The market segments include Type, Application.

The market size is estimated to be USD 1326 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Non-Wood Pulp," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Non-Wood Pulp, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.