1. What is the projected Compound Annual Growth Rate (CAGR) of the Non-Dairy Milk Alternatives?

The projected CAGR is approximately 8.63%.

Non-Dairy Milk Alternatives

Non-Dairy Milk AlternativesNon-Dairy Milk Alternatives by Type (Almond, Soy, Coconut, Rice, Oats, Others), by Application (Direct Drink, Confectionery, Bakery, Ice Cream, Cheese, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

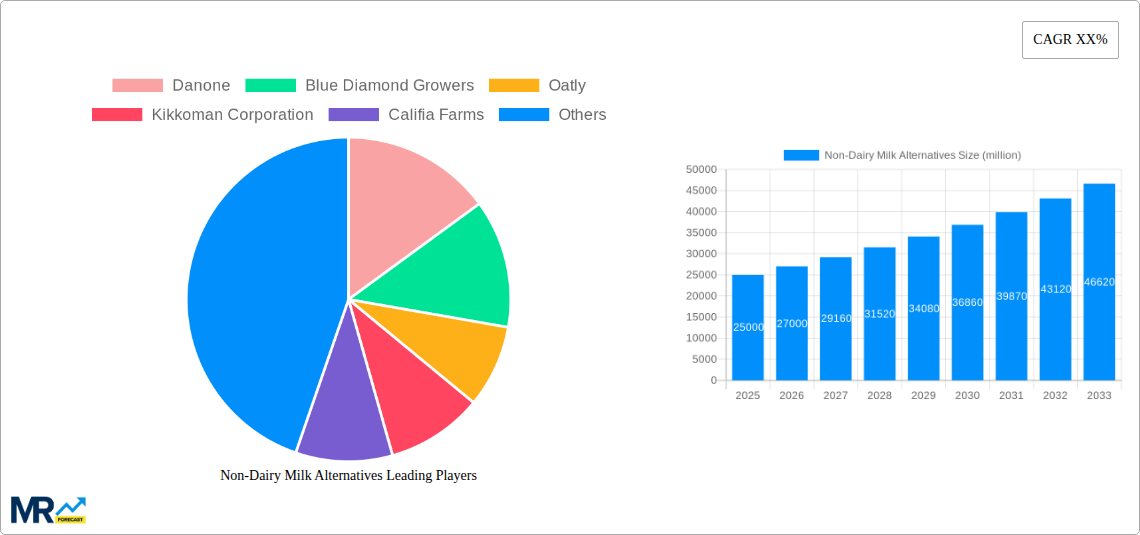

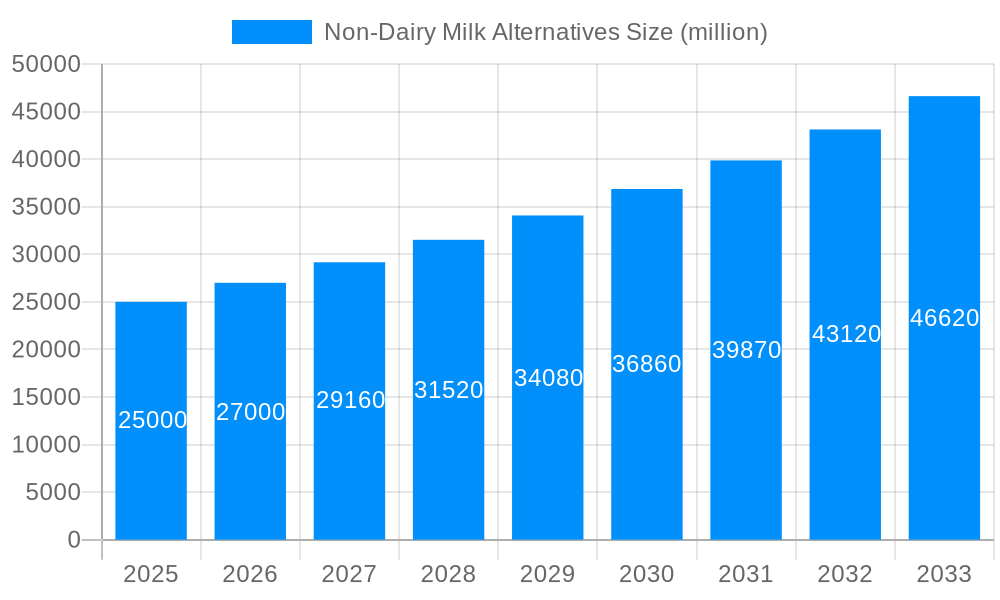

The non-dairy milk alternatives market is experiencing significant expansion, driven by rising consumer preference for plant-based options and growing health consciousness. The market, valued at $27.31 billion in the base year 2025, is projected to achieve a compound annual growth rate (CAGR) of 8.63% from 2025 to 2033. This growth is attributed to several key drivers: increasing awareness of plant-based diets' health benefits, such as improved cardiovascular health; a rise in lactose intolerance and dairy allergies; and the growing adoption of vegan and vegetarian lifestyles. Continuous product innovation, focusing on enhanced flavors, textures, and nutritional profiles, further stimulates demand. Leading companies like Danone, Oatly, and Blue Diamond Growers are actively expanding their product offerings and distribution channels.

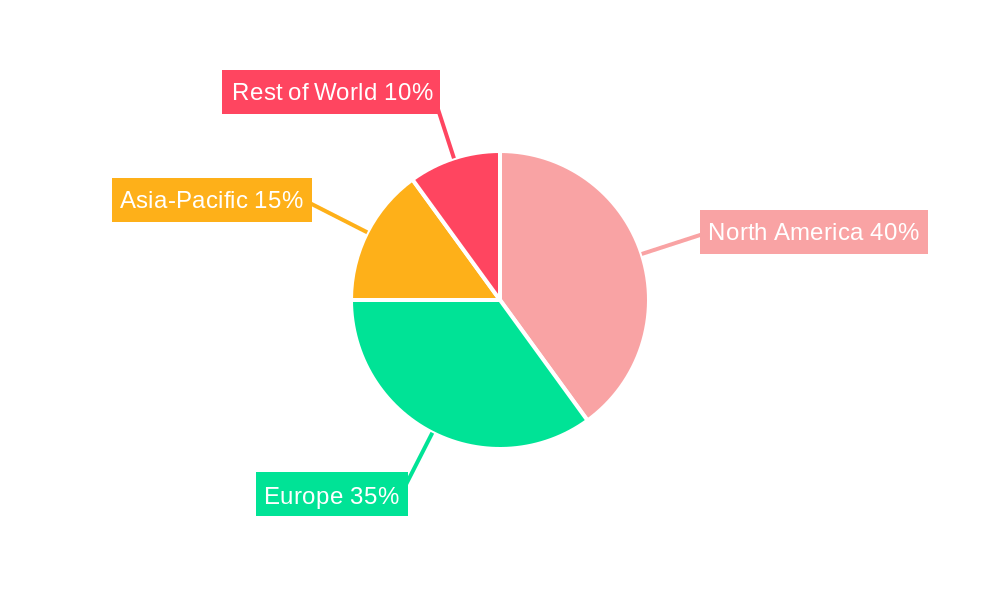

While the market demonstrates a positive growth outlook, challenges include raw material price volatility and competition from more affordable traditional dairy products. However, ongoing research into sustainable and cost-effective production methods is expected to address these concerns. The market is segmented by product type (almond, soy, oat, coconut, etc.), distribution channel (retail, food service), and geography. North America and Europe currently dominate market share, with emerging economies in Asia and Latin America poised for substantial growth, presenting significant expansion opportunities.

The global non-dairy milk alternatives market is experiencing explosive growth, projected to reach hundreds of billions of units by 2033. Driven by a confluence of factors – increasing health consciousness, rising vegan and vegetarian populations, and growing lactose intolerance – the market shows no signs of slowing down. The historical period (2019-2024) witnessed a significant surge in demand, establishing a strong foundation for continued expansion during the forecast period (2025-2033). The estimated market size in 2025 is already in the tens of billions of units, indicating a robust and mature market with ample room for further penetration. This growth is not uniformly distributed across all segments. While soy milk maintains a significant share, almond, oat, and coconut milk are rapidly gaining traction, fueled by innovation in taste, texture, and nutritional profiles. The market is witnessing a diversification of product offerings, with new entrants introducing novel ingredients and formulations, catering to diverse consumer preferences. Furthermore, the increasing focus on sustainability and ethical sourcing is influencing consumer purchasing decisions, pushing companies to adopt more responsible practices throughout their supply chains. This shift toward sustainability is expected to further drive the demand for non-dairy milk alternatives, contributing to the overall market expansion in the coming years. The competitive landscape is also dynamic, with established players alongside innovative startups vying for market share through strategic partnerships, product launches, and aggressive marketing campaigns. This competitive intensity is beneficial for consumers, leading to greater product variety and affordability. Finally, the market is witnessing the expansion into new geographic regions, particularly in developing economies where awareness of non-dairy options is growing rapidly.

Several key factors are propelling the remarkable growth of the non-dairy milk alternatives market. Firstly, the rising prevalence of lactose intolerance globally is a major driver. Millions of people suffer from lactose intolerance, leading them to seek dairy-free alternatives. Secondly, the increasing popularity of vegan and vegetarian lifestyles is significantly boosting demand. As more consumers adopt plant-based diets for ethical, environmental, or health reasons, the consumption of non-dairy milk alternatives is naturally increasing. Thirdly, growing health consciousness among consumers is another powerful driver. Many non-dairy milk alternatives are perceived as healthier options, being lower in saturated fat and cholesterol than cow's milk. The market is also responding to consumer demand for functional foods and beverages, with fortified non-dairy milks offering added vitamins and minerals. Furthermore, the expanding availability of non-dairy milk alternatives in various retail channels – supermarkets, convenience stores, online platforms – makes them easily accessible to consumers. The increasing innovation in product development, leading to improved taste, texture, and functionality, is another important factor. Companies are constantly striving to create non-dairy milk alternatives that closely replicate the taste and experience of cow's milk, attracting even more consumers. Finally, growing concerns about the environmental impact of dairy farming are pushing consumers towards more sustainable alternatives.

Despite the significant growth potential, the non-dairy milk alternatives market faces certain challenges and restraints. One significant hurdle is the often higher price point of non-dairy milks compared to conventional cow's milk, limiting accessibility for some consumers, particularly in price-sensitive markets. The perception of inferior taste and texture compared to cow's milk also persists among some consumers, hindering wider adoption. This perception is however constantly being challenged by ongoing product innovation. Another challenge lies in maintaining a consistent supply chain and ensuring the sustainability of the raw materials used in the production of non-dairy milk alternatives. This is particularly true for certain plant-based sources which require significant land and water resources. Furthermore, potential allergens present in some non-dairy milks, such as soy or nuts, pose a challenge for consumers with allergies. Stricter regulations and labelling requirements in different regions also add to the complexity of navigating the market. The fluctuating prices of raw materials, especially agricultural commodities used in the production of non-dairy milks, can also affect the profitability and pricing strategies of manufacturers. Finally, building consumer trust and addressing concerns about the nutritional value and long-term health effects of consuming non-dairy milks requires ongoing research and transparent communication.

The North American and European markets currently dominate the non-dairy milk alternatives sector, driven by high consumer awareness, strong regulatory frameworks, and established distribution networks. However, Asia-Pacific is showing rapid growth, fueled by rising disposable incomes and a burgeoning middle class adopting westernized dietary habits.

Dominant Segments:

The paragraph above highlights how the interplay of regional factors and specific product segments shape the overall market landscape. The dominance of certain regions and the rise of specific types of milk will continue to evolve as consumer preferences and technological advancements shape the future of the industry.

The non-dairy milk alternatives industry is poised for continued growth due to several key catalysts. Increased product innovation, focusing on improved taste, texture, and nutritional profiles, is attracting a broader range of consumers. The rising popularity of plant-based diets and growing awareness of lactose intolerance are significantly driving demand. Furthermore, advancements in sustainable agricultural practices and supply chain management are building consumer trust and confidence in the industry's environmental responsibility. These factors, coupled with expanding distribution channels and targeted marketing campaigns, will continue to fuel the market's impressive growth trajectory.

This report provides a comprehensive overview of the non-dairy milk alternatives market, encompassing historical data, current market trends, and future projections. It offers in-depth analysis of key market drivers, restraints, and growth opportunities, providing valuable insights for stakeholders across the value chain. The report also profiles major players in the industry, analyzing their competitive strategies and market positioning. Through this detailed analysis, businesses can make well-informed decisions about investments, product development, and market expansion strategies within the rapidly evolving non-dairy milk alternatives sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.63% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.63%.

Key companies in the market include Danone, Blue Diamond Growers, Oatly, Kikkoman Corporation, Califia Farms, Earth's Own Food Company, Ezaki Glico, Ripple Foods, Marusan-Ai Co. Ltd, Campbell Soup Company, SunOpta, Nutrisoya Foods, Elmhurst Milked Direct, Panos Brands, Jindilli Beverages (milkadamia), Hebei Yangyuan Zhihui, He Bei Cheng De Lolo, Coconut Palm Group, V V Food and Beverage, Vitasoy International Holdings, .

The market segments include Type, Application.

The market size is estimated to be USD 27.31 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Non-Dairy Milk Alternatives," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Non-Dairy Milk Alternatives, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.