1. What is the projected Compound Annual Growth Rate (CAGR) of the No Added Sugar Baby Complementary Food?

The projected CAGR is approximately 15.57%.

No Added Sugar Baby Complementary Food

No Added Sugar Baby Complementary FoodNo Added Sugar Baby Complementary Food by Type (Birth to 3 Months, 4 to 7 Months, 8 to 11 Months, 12 to 23 Months, 24 Months and Above), by Application (Online Sale, Offline Sale), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

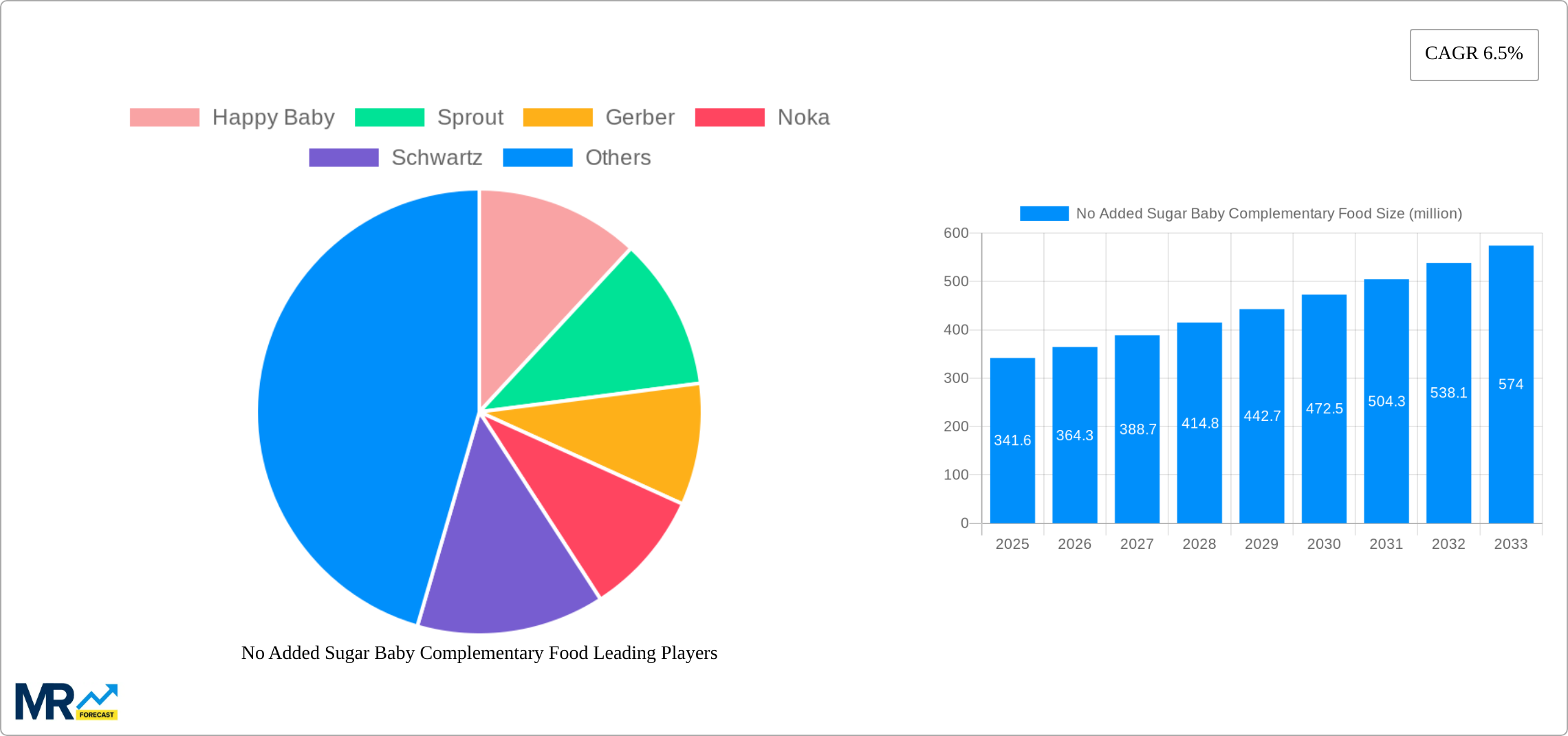

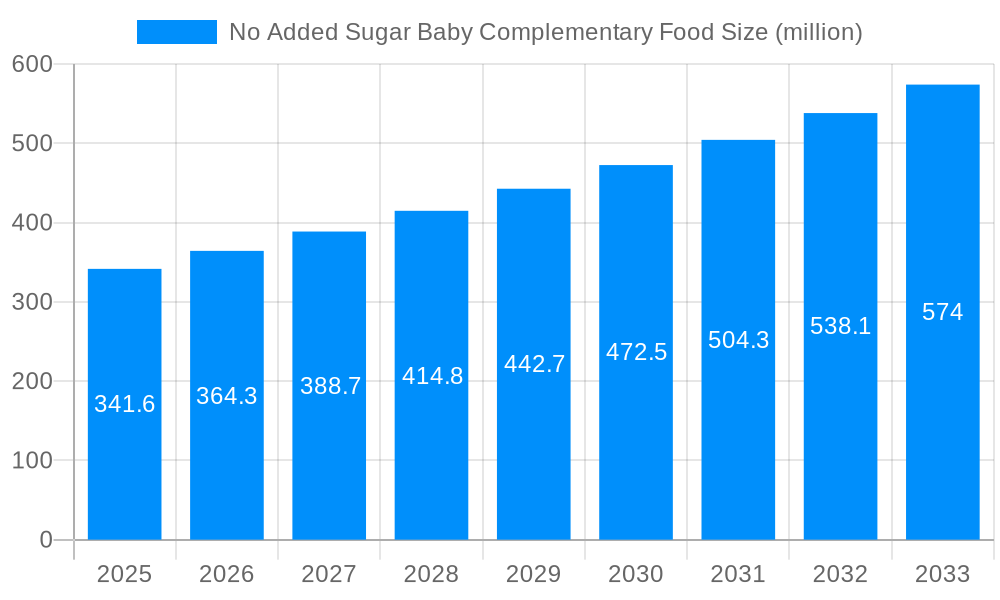

The global market for no-added-sugar baby complementary food is experiencing robust growth, projected at a Compound Annual Growth Rate (CAGR) of 6.5% from 2019 to 2033. In 2025, the market size reached $341.6 million. This expansion is fueled by increasing awareness among parents regarding the importance of healthy eating habits in early childhood, a preference for organic and natural food products, and a rising demand for convenient and nutritious options. The segment encompassing babies aged 4 to 7 months shows particularly strong growth, driven by the early introduction of solids into their diet. Online sales channels are contributing significantly to market growth, reflecting evolving consumer behavior and the ease of online purchasing. Key players such as Happy Baby, Gerber, and Ella's Kitchen are leveraging brand recognition and product innovation to maintain market share, while emerging brands are focusing on niche markets, like specific dietary needs or unique flavor profiles, to gain traction. Geographic distribution shows strong demand across North America and Europe, though Asia Pacific represents a significant growth opportunity as consumer awareness increases and disposable incomes rise. While regulatory hurdles related to food safety and labeling might pose some restraints, the overall market outlook remains positive, with significant potential for further expansion in the coming years.

The market segmentation reveals that the "4 to 7 months" age group is a significant driver of growth, potentially exceeding other age categories in terms of sales volume. The strong preference for online sales suggests a need for brands to invest in robust e-commerce strategies. Regional differences in growth trajectories are expected, with developed markets showing steady growth while emerging markets like those in Asia-Pacific will likely experience accelerated expansion due to increasing health consciousness and purchasing power. The competitive landscape is characterized by both established brands leveraging their brand equity and innovative startups introducing specialized products. The continued focus on organic and natural ingredients, coupled with product innovation to meet diverse parental needs, will be key for sustained market success. Further market research may pinpoint more precise growth estimates for specific segments and regions, informing tailored marketing strategies and investment decisions.

The no added sugar baby complementary food market is experiencing robust growth, driven by increasing health consciousness among parents and a rising awareness of the detrimental effects of excessive sugar consumption in early childhood. The market, valued at several billion units in 2024, is projected to reach tens of billions of units by 2033, reflecting a significant Compound Annual Growth Rate (CAGR). This growth is fueled by several key factors. Firstly, a shift towards healthier eating habits for infants and toddlers is evident globally. Parents are actively seeking out food options that prioritize natural ingredients and avoid added sugars, artificial sweeteners, and preservatives. Secondly, the expanding online retail sector has played a crucial role in market expansion. E-commerce platforms provide convenient access to a wider selection of no added sugar baby food options, reaching consumers beyond traditional retail channels. This has broadened the market reach, leading to increased sales and market penetration. Furthermore, the market is witnessing the introduction of innovative product formats and flavors, catering to the evolving preferences of both parents and babies. The development of convenient, portable options like pouches and single-serving containers has boosted market appeal. Finally, the growing prevalence of allergies and dietary restrictions has led to increased demand for specialized no added sugar baby foods tailored to specific needs, further expanding market segmentation and growth opportunities. While the market is experiencing significant growth, competition remains intense, with major players continually innovating to meet consumer demands and stay ahead of the curve.

Several key factors are propelling the growth of the no added sugar baby complementary food market. The primary driver is the increasing awareness among parents regarding the health implications of added sugar in their children's diets. Early exposure to high sugar intake is linked to increased risks of obesity, diabetes, and dental problems. This awareness, fueled by public health campaigns and media attention, is pushing parents towards healthier options for their babies. Furthermore, the rising disposable incomes in many developing countries are enabling parents to afford premium, healthier food products, including those free from added sugar. This increase in purchasing power is directly contributing to market expansion. The growing preference for organic and natural ingredients is also a significant driver. Parents are increasingly seeking out products with clean labels, free from artificial additives, and made from organic ingredients. This preference for natural and wholesome foods has created a strong demand for no added sugar options. Finally, the expanding online retail channels are simplifying the process of purchasing these specialized products, further accelerating market growth. The convenience offered by online platforms, coupled with wider product availability, is making these healthier options easily accessible to consumers worldwide.

Despite the substantial growth potential, the no added sugar baby complementary food market faces certain challenges. One major hurdle is the higher cost of production compared to conventional baby foods with added sugar. The use of high-quality, organic ingredients and specialized manufacturing processes can increase the price, potentially making these products less accessible to budget-conscious consumers. This price sensitivity can limit market penetration, especially in price-sensitive regions. Another challenge is the shorter shelf life of some no added sugar products compared to their counterparts with preservatives. This requires careful management of supply chains and logistics to ensure product freshness and minimize waste. Maintaining a balance between product quality, shelf life, and affordability remains a critical challenge for manufacturers. Furthermore, intense competition among established and emerging players is a constant pressure. Companies need to differentiate themselves through innovation, marketing, and brand building to capture market share in this fiercely contested market. Finally, inconsistent regulatory frameworks across different countries can pose challenges for companies operating internationally, adding complexity to product development and marketing strategies.

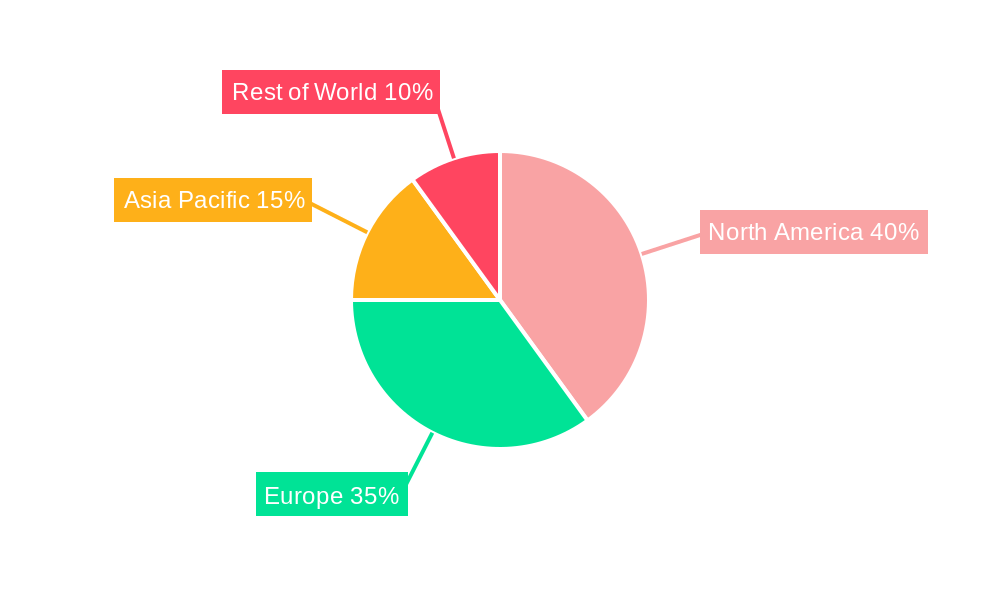

The no added sugar baby complementary food market exhibits strong growth across various regions, but developed nations in North America and Europe are currently leading the market due to higher health consciousness and disposable incomes. However, rapidly developing economies in Asia-Pacific are witnessing significant growth potential, fueled by rising awareness of health and nutrition and increasing urbanization.

Dominant Segments:

Market Dominance Explained: The 4-7 months and 8-11 months age group dominates because this is the critical period where parents actively seek healthy complementary foods to introduce solids to their babies' diet. The convenience of online sales is driving their growth, especially in developed countries where e-commerce is highly developed.

The growth of the no added sugar baby complementary food market is primarily driven by the increasing awareness of health risks associated with added sugar in early childhood. This, coupled with rising disposable incomes and the expansion of online retail, is creating a favorable environment for market expansion. Innovation in product formats, flavors, and specialized dietary options further fuels the growth.

This report provides a comprehensive analysis of the no added sugar baby complementary food market, covering historical data (2019-2024), current estimates (2025), and future projections (2025-2033). It delves into market trends, driving forces, challenges, key players, and significant developments, providing valuable insights for businesses operating in this dynamic sector. The report also highlights key segments and regions to watch for future growth opportunities.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.57% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 15.57%.

Key companies in the market include Happy Baby, Sprout, Gerber, Noka, Schwartz, SmartyPants, Orgain, Goldfish, GoGo squeeZ, Nesquik, Quaker, Jack Link's, Rip Van, YumEarth, BARNEY, Natierra, Plum Organics, New Chapter, MaryRuth's, Happy Baby Organics, Ella's Kitchen, Beech-Nut, Little Spoon, Earth's Best Organic, NurturMe, Parent's Choice, Organix, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "No Added Sugar Baby Complementary Food," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the No Added Sugar Baby Complementary Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.