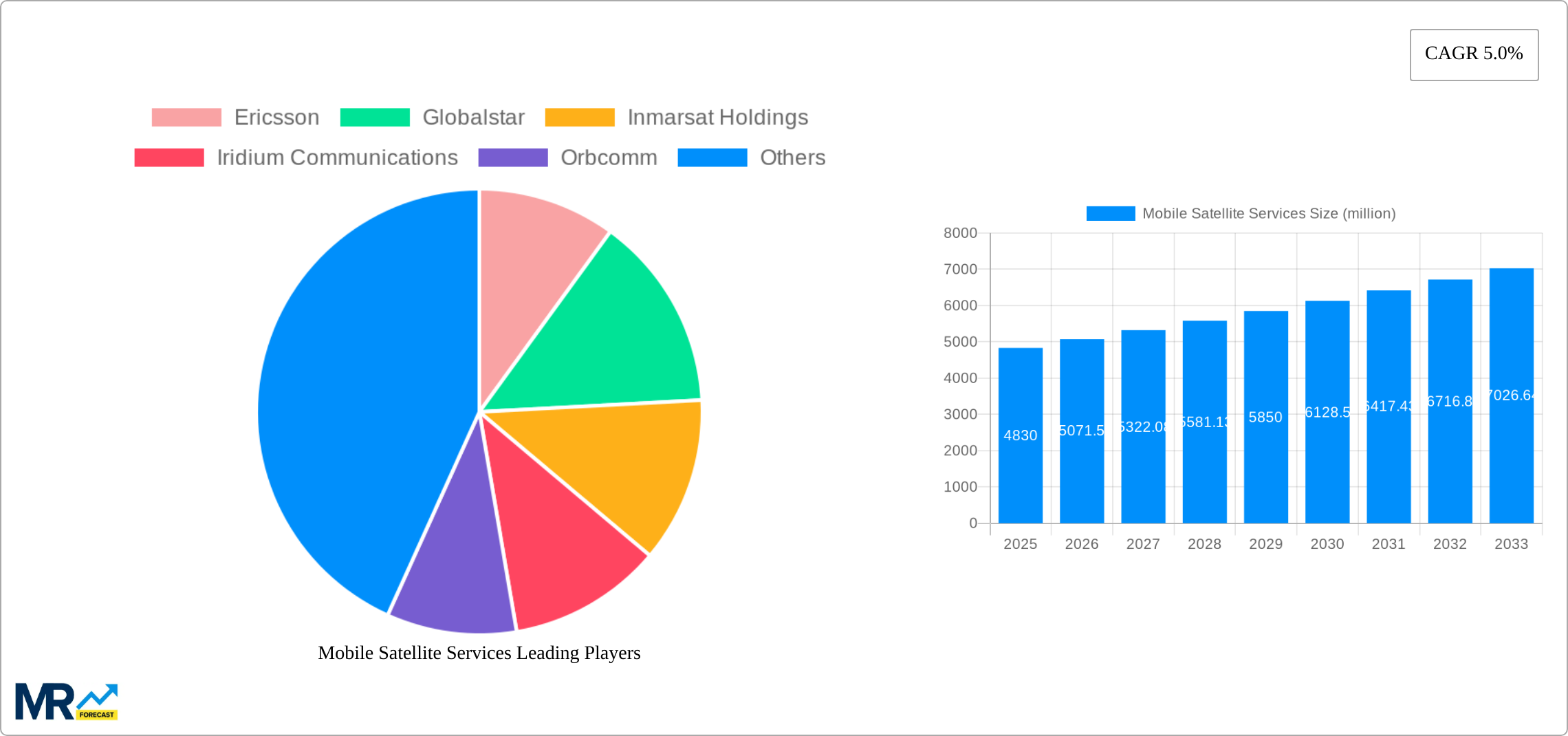

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Satellite Services?

The projected CAGR is approximately 5.0%.

Mobile Satellite Services

Mobile Satellite ServicesMobile Satellite Services by Service Type (Voice Services, Data Services, Video Services, Tracking & Monitoring Services, Others), by Frequency Band (L-Band, S-Band, Ku-Band, Ka-Band, Others), by Application (Satellite Communication, Fleet Management, Asset Tracking, Remote Monitoring, Others), by End User Industry (Aerospace and Defense, Government & Defense, Maritime, Oil & Gas, Mining, Transportation & Logistics, Agriculture, Energy & Utilities, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The Mobile Satellite Services Market is currently valued at an estimated USD 4830 million in 2025, demonstrating its critical role in global connectivity, particularly in remote and underserved areas. Projections indicate robust expansion, with the market expected to reach approximately USD 7136 million by 2033, advancing at a Compound Annual Growth Rate (CAGR) of 5.0% over the forecast period. This growth trajectory is underpinned by a confluence of factors, including increasing governmental incentives aimed at enhancing universal broadband access and supporting critical infrastructure. The escalating demand for ubiquitous connectivity, especially from industrial sectors for operational efficiency and safety, is a primary catalyst.

Macro tailwinds such as the global push for digitalization, the expansion of commercial and defense aerospace activities, and the growing importance of safety and communication protocols in the maritime sector are significantly boosting market demand. Furthermore, strategic partnerships between satellite operators and terrestrial telecommunication providers are fostering hybrid network solutions, expanding reach and service reliability. While the initial prompt mentions the popularity of virtual assistants as a driver, for the Mobile Satellite Services Market, this is more accurately interpreted as the increasing integration of smart, connected devices and the need for robust backhaul for distributed AI and data processing in remote locations, which in turn fuels the broader IoT Connectivity Market. The proliferation of low-Earth orbit (LEO) and medium-Earth orbit (MEO) satellite constellations is poised to revolutionize the market by offering lower latency and higher bandwidth services, challenging traditional geostationary (GEO) satellite paradigms. This technological evolution is not only expanding the addressable market but also driving innovation in user equipment, making Satellite Terminal Market solutions more compact and affordable. The imperative for reliable communication in disaster relief, emergency services, and critical infrastructure monitoring continues to be a steadfast demand driver, ensuring the sustained growth and strategic importance of mobile satellite services.

Within the Mobile Satellite Services Market, the Voice Services segment has historically held a commanding revenue share, establishing itself as a cornerstone of global satellite communication. This dominance is primarily attributable to the fundamental need for reliable voice communication in areas beyond the reach of terrestrial networks. For decades, satellite voice services have been indispensable for critical applications such as maritime safety, aeronautical communication, military operations, and remote industrial activities in sectors like oil & gas, mining, and agriculture. Companies like Iridium Communications, Inmarsat, and Globalstar have built their foundational service offerings around robust voice capabilities, ensuring vital connections for emergency services, remote workers, and adventurers alike. The simplicity and reliability of voice communication, even in bandwidth-constrained environments, have cemented its position as a primary service type.

However, while the Voice Services Market continues to see absolute growth due to the expanding global demand for basic connectivity, its relative share within the broader Mobile Satellite Services Market is experiencing a gradual shift. The rapid advancements in satellite technology and the increasing sophistication of user demands are propelling the growth of other service segments. Specifically, the Data Services Market is rapidly gaining traction, driven by the proliferation of bandwidth-intensive applications such as high-definition video streaming, internet browsing, and extensive data transfer for business operations. The rising adoption of IoT solutions and the demand for real-time Remote Monitoring Market capabilities in various industries are further accelerating the expansion of data-centric satellite services. Although voice remains crucial for safety-of-life and mission-critical communications, the future growth narrative of the Mobile Satellite Services Market is increasingly leaning towards enhanced data and video capabilities. Nevertheless, the Voice Services Market remains an essential revenue generator, particularly for legacy systems and in applications where minimal latency and guaranteed connection are paramount, underpinning a significant portion of the global Satellite Communication Market infrastructure. The innovation in smaller, more efficient Satellite Terminal Market devices also helps sustain the utility and accessibility of voice services.

The Mobile Satellite Services Market is propelled by several potent drivers, chief among them being the increasing demand for ubiquitous connectivity across remote and underserved regions. For instance, the expansion of resource extraction activities in remote areas, such as new mining sites in Australia or offshore oil & gas platforms, necessitates reliable communication for operational efficiency and worker safety. This drives significant uptake in the Remote Monitoring Market, as companies leverage satellite solutions for real-time asset tracking and sensor data transmission. Moreover, government incentives and regulatory mandates for maritime and aeronautical safety, such as the Global Maritime Distress and Safety System (GMDSS) requirements for the Maritime Communication Market, necessitate the adoption of satellite-based communication systems, ensuring a steady demand stream for critical voice and data services. The strategic partnerships between satellite operators and terrestrial Telecommunication Services Market providers are also crucial, enabling hybrid networks that extend the reach of 5G and other advanced cellular services into areas historically reliant solely on satellite, thereby expanding the addressable market.

Despite these drivers, the market faces notable constraints. The high initial capital expenditure associated with launching and maintaining satellite constellations, along with the extensive ground infrastructure required, presents a significant barrier to entry for new players. Furthermore, the regulatory landscape, characterized by complex spectrum allocation and licensing procedures governed by international bodies like the ITU and national regulators, can be cumbersome and slow, impeding rapid innovation and market entry. Competition from expanding terrestrial networks, especially in peri-urban and even some rural areas with fiber and advanced cellular deployments, poses a challenge, particularly for routine communication needs where the higher latency and cost of satellite services might be less competitive. While the Satellite Terminal Market is becoming more affordable, the overall cost of satellite services can still be a deterrent for some consumers and small businesses. Lastly, while low-Earth orbit (LEO) constellations are addressing latency, existing geostationary (GEO) satellite systems still contend with inherent signal delay, which can impact real-time, interactive applications and user experience for some Data Services Market offerings.

The competitive landscape of the Mobile Satellite Services Market is characterized by a mix of established players with extensive satellite constellations and ground infrastructure, alongside innovative new entrants leveraging next-generation technologies. These companies are continually investing in R&D, network expansion, and strategic alliances to enhance their service offerings and market reach.

Recent years have witnessed a surge in innovation and strategic activity within the Mobile Satellite Services Market, driven by technological advancements and evolving connectivity demands.

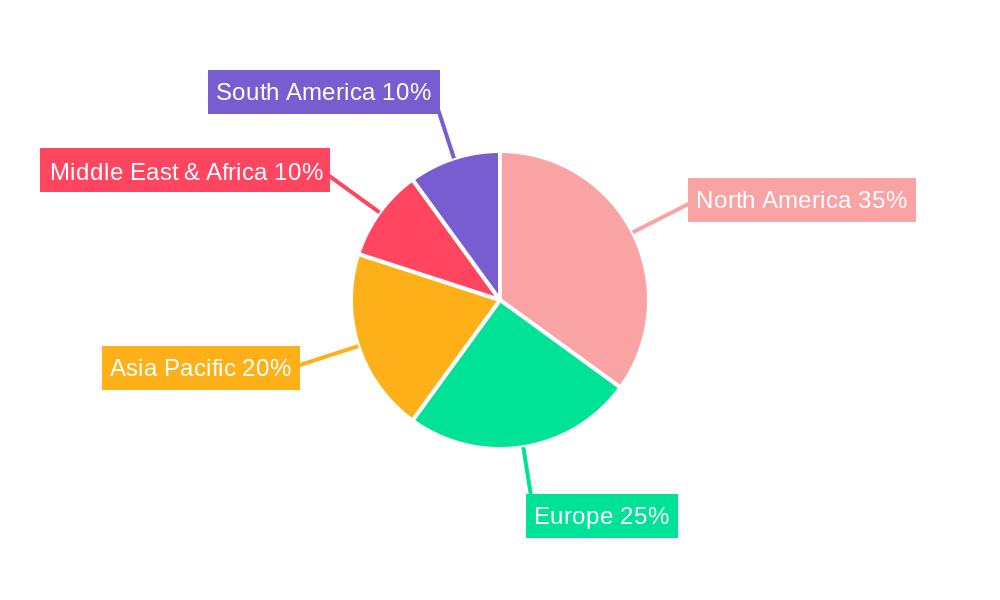

Maritime Communication Market solutions, focusing on real-time vessel monitoring, crew welfare, and autonomous shipping capabilities using high-throughput satellite links.Aerospace and Defense Market segment's reliance on resilient satellite infrastructure.Telecommunication Services Market coverage.Data Services Market package was launched, specifically designed for industrial IoT Connectivity Market applications in remote areas, offering tiered data plans optimized for sensor networks and asset tracking.The Mobile Satellite Services Market exhibits distinct regional dynamics, influenced by varying levels of infrastructure development, economic conditions, and specific industry demands. North America currently holds a substantial revenue share, largely due to a mature Aerospace and Defense Market, significant investment in advanced communication technologies, and a high demand for connectivity in remote areas for industries such as oil & gas, mining, and agriculture. The presence of key market players and robust R&D activities also contributes to its market dominance, alongside strong governmental support for satellite-based solutions.

Europe represents another significant market, driven by its extensive maritime industry, necessitating advanced Maritime Communication Market solutions, and a growing emphasis on public safety and emergency services. The region also sees considerable adoption in the energy and utilities sector for grid management and remote asset monitoring. Regulatory frameworks designed to enhance safety and provide reliable communication across borders further stimulate the market.

Asia Pacific is projected to be the fastest-growing region in the Mobile Satellite Services Market, propelled by rapid industrialization, expanding economies, and increasing investments in infrastructure development, particularly in countries like China and India. The vast geographical areas and remote populations in these regions demand satellite solutions to bridge the digital divide and support critical sectors like agriculture, transportation, and disaster management. The rising adoption of IoT Connectivity Market solutions for fleet management and asset tracking is a major driver.

Middle East & Africa also demonstrate promising growth, primarily fueled by the burgeoning oil & gas sector, defense initiatives, and the need for connectivity in areas with limited terrestrial infrastructure. Countries in the GCC region, alongside parts of Africa, are investing in satellite technology to support economic diversification and enhance national security. However, socio-economic disparities and political instability in some parts of the region can pose challenges. South America, while smaller, shows steady growth, particularly in supporting remote mining operations and agricultural industries, with Brazil and Argentina leading in the adoption of Remote Monitoring Market and Voice Services Market solutions.

The Mobile Satellite Services Market is undergoing a profound technological transformation, driven by innovations poised to reshape its capabilities and reach. One of the most disruptive trends is the proliferation of Low-Earth Orbit (LEO) and Medium-Earth Orbit (MEO) constellations. Companies like Starlink (SpaceX) and OneWeb (now part of Eutelsat Group) are deploying thousands of satellites, drastically reducing latency compared to traditional geostationary (GEO) satellites. This shift enables new applications requiring real-time responsiveness and higher bandwidth, threatening incumbent GEO-based business models by offering competitive speeds and often lower service costs, thereby expanding the addressable Satellite Communication Market for general internet access and high-speed Data Services Market. Adoption timelines are accelerating, with significant R&D investment in both space-based and ground infrastructure. These constellations reinforce incumbent models by providing backhaul for terrestrial networks in remote areas, but also introduce intense competition for direct-to-consumer and enterprise services.

Another critical innovation is the integration of Non-Terrestrial Networks (NTN) with 5G standards. This development aims to seamlessly extend 5G coverage to areas beyond terrestrial infrastructure, allowing standard unmodified 5G devices to connect directly to satellites. This is a game-changer for the Telecommunication Services Market, promising ubiquitous connectivity and enhancing the capabilities of IoT Connectivity Market applications by providing global reach for sensors and devices. R&D investments are high, with collaborations between satellite operators and telecom giants focused on standardizing interfaces and protocols. This technology represents both a threat and a reinforcement: it threatens traditional satellite phone markets by making regular phones satellite-capable, but reinforces the role of satellite as a crucial component of a truly global 5G network, expanding the market for Voice Services Market and Data Services Market significantly.

Finally, advancements in Software-Defined Satellites (SDS) and Advanced Antenna Technologies, particularly phased array antennas, are transforming the Satellite Terminal Market. SDS allows satellites to reconfigure their beams and payloads in orbit, offering unparalleled flexibility in adapting to changing demand, dynamic spectrum allocation, and target specific geographies. Simultaneously, phased array antennas are enabling smaller, lighter, and more efficient ground terminals that can electronically steer beams without mechanical movement. This reduces the cost and complexity of user equipment, making satellite services more accessible and easier to deploy, which directly impacts the Remote Monitoring Market and Aerospace and Defense Market by enabling smaller, more discreet communication nodes. These innovations reinforce incumbent business models by improving efficiency and reducing costs, while also creating new market opportunities for specialized, high-performance Satellite Terminal Market solutions.

The Mobile Satellite Services Market operates within a complex and evolving regulatory and policy landscape, primarily governed by international treaties and national regulations. At the global level, the International Telecommunication Union (ITU) plays a pivotal role in allocating radio frequency spectrum and orbital slots for satellites, ensuring equitable access and preventing harmful interference. This framework is critical for operators to secure the necessary resources for their constellations and services, impacting everything from Voice Services Market to high-speed Data Services Market. Recent ITU World Radiocommunication Conferences (WRC) have focused on spectrum for 5G Non-Terrestrial Networks (NTN) and the increasing number of LEO constellations, signaling a global push for integrated terrestrial-satellite communications.

Nationally, regulatory bodies such as the Federal Communications Commission (FCC) in the United States, Ofcom in the United Kingdom, and similar agencies worldwide are responsible for licensing satellite service providers, regulating service quality, and ensuring consumer protection. These bodies also oversee the implementation of national security directives that often leverage the Aerospace and Defense Market for secure satellite communication. Recent policy changes, particularly in the U.S., have aimed to streamline licensing processes for non-geostationary satellite systems, accelerating the deployment of new LEO constellations and fostering competition in the Satellite Communication Market. This has a projected positive market impact by enabling faster service rollout and broader coverage.

Specific sectoral regulations also heavily influence the market. The International Maritime Organization (IMO) and the International Civil Aviation Organization (ICAO) set standards for safety-of-life communications in the Maritime Communication Market and aviation sectors, respectively. The Safety of Life at Sea (SOLAS) convention mandates satellite communication systems for distress and safety, providing a consistent demand driver for Voice Services Market and Data Services Market in the maritime domain. Recent updates to these standards often require enhanced bandwidth and reliability, pushing innovation in Satellite Terminal Market technology. Furthermore, data privacy and cybersecurity regulations, such as GDPR in Europe, are increasingly relevant as satellite networks transmit vast amounts of sensitive data. Compliance with these regulations is crucial for market entry and operational continuity, particularly for the Remote Monitoring Market and IoT Connectivity Market applications that often handle critical infrastructure data. The ongoing geopolitical climate also influences policies regarding national control over satellite assets and data sovereignty, adding another layer of complexity to global market operations.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.0% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.0%.

Key companies in the market include Iridium Communications, Inmarsat, Viasat, Globalstar, Thuraya Telecommunications Company, EchoStar Corporation, Orbcomm, Space42, Omnispace, AST SpaceMobile, Ligado Networks, Eutelsat Group, Others.

The market segments include Service Type, Frequency Band, Application, End User Industry.

The market size is estimated to be USD 4830 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Mobile Satellite Services," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Mobile Satellite Services, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.