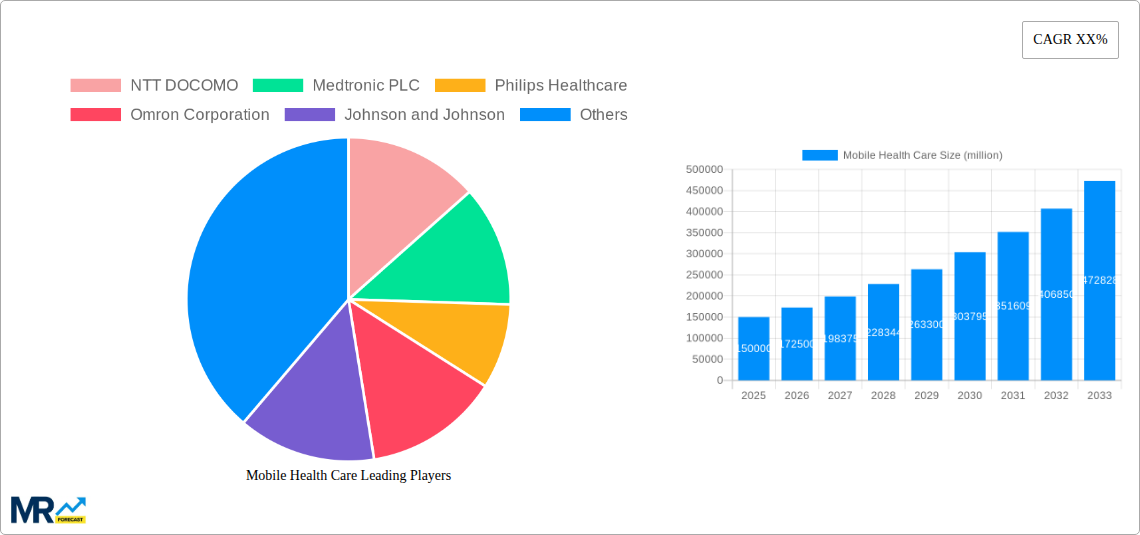

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Health Care?

The projected CAGR is approximately 30.3%.

Mobile Health Care

Mobile Health CareMobile Health Care by Type (/> Monitoring Services, Diagnostic Services, Treatment Services, Wellness and Fitness Solutions, Others), by Application (/> Self/Home Care, Hospital & Clinics, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global mobile healthcare market is poised for significant expansion, driven by widespread smartphone and wearable adoption, coupled with rapid advancements in mobile technology and a growing demand for remote patient monitoring solutions. Key growth drivers include the increasing prevalence of chronic diseases, the rising affordability of mHealth devices, and the escalating preference for convenient and accessible healthcare services. Telehealth consultations, remote diagnostics, and personalized health management via mobile applications are transforming patient care and healthcare delivery. Leading companies are investing heavily in R&D, fostering continuous innovation, enhanced data security, superior user experiences, and seamless integration with existing healthcare infrastructure.

While the outlook is positive, challenges persist. Paramount among these are data privacy and security concerns, necessitating robust regulatory frameworks and advanced technological solutions. Addressing interoperability issues across diverse mHealth platforms is crucial for seamless data exchange and holistic patient care. Furthermore, the digital divide and unequal technology access require targeted initiatives to ensure equitable adoption of mobile health solutions. Despite these obstacles, the mobile healthcare market is projected to witness substantial growth, revolutionizing healthcare access and management globally.

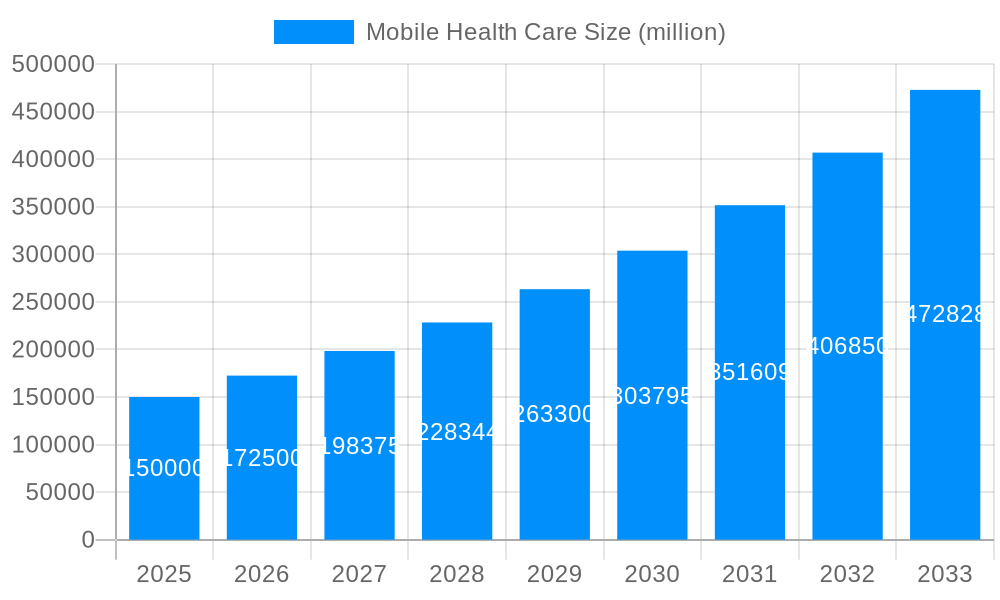

The global mobile health care market is experiencing explosive growth, projected to reach hundreds of billions of dollars by 2033. This surge is driven by a confluence of factors, including the increasing affordability and accessibility of smartphones and mobile internet, coupled with advancements in sensor technology, data analytics, and telehealth platforms. The historical period (2019-2024) witnessed a significant rise in the adoption of mHealth solutions across various healthcare segments, laying the foundation for the substantial expansion forecast for the period 2025-2033. Key market insights reveal a strong preference for remote patient monitoring (RPM) solutions, particularly among aging populations and those with chronic conditions. The integration of artificial intelligence (AI) and machine learning (ML) is further enhancing diagnostic capabilities and personalized treatment plans delivered through mobile platforms. Furthermore, the increasing demand for cost-effective healthcare solutions and the growing burden of chronic diseases are major contributing factors to the market's upward trajectory. The estimated market value for 2025 is already in the tens of billions, demonstrating the rapid pace of adoption. Government initiatives promoting telehealth and digital health are also playing a crucial role, alongside increasing investments in research and development by both established players and innovative startups. The shift towards value-based care models is also encouraging the use of mHealth to improve patient outcomes and reduce healthcare costs. This is evidenced by the expanding partnerships between healthcare providers, technology companies, and insurance providers to integrate mHealth solutions into their workflows. Finally, the ease of access and convenience offered by mHealth apps and devices are proving to be extremely popular with patients and clinicians alike, accelerating market growth.

Several powerful forces are accelerating the growth of the mobile health care market. Firstly, the widespread adoption of smartphones and the increasing penetration of mobile internet, especially in developing nations, is creating a massive pool of potential users for mHealth applications. This is coupled with the decreasing cost of mobile devices and data plans, making mHealth solutions accessible to a broader demographic. Secondly, technological advancements, particularly in areas like AI, ML, and sensor technology, are enabling the development of more sophisticated and accurate diagnostic tools and treatment options delivered through mobile platforms. This includes advanced wearables capable of continuous health monitoring and remote diagnostics. Thirdly, the rising prevalence of chronic diseases globally places a significant strain on healthcare systems. mHealth provides a cost-effective and scalable solution for managing these conditions through remote monitoring, medication adherence programs, and virtual consultations, reducing the burden on hospitals and clinics. Finally, regulatory support and governmental initiatives aimed at promoting the adoption of digital health technologies are creating a favorable environment for mHealth companies to flourish. These initiatives often involve financial incentives, regulatory streamlining, and public awareness campaigns that drive both supply and demand.

Despite the impressive growth trajectory, several challenges and restraints impede the full realization of mHealth's potential. Data security and privacy concerns are paramount, with the transmission and storage of sensitive patient data requiring robust and compliant security measures. The lack of standardized regulations across different countries and regions creates complexities for mHealth companies seeking to expand their operations globally. Interoperability issues between different mHealth devices and platforms remain a significant obstacle, hindering seamless data exchange and integrated care delivery. Furthermore, the digital divide, particularly in underserved communities with limited access to technology and internet connectivity, limits the reach and effectiveness of mHealth solutions. The need for reliable and consistent internet access is also a constraint in many regions. Finally, ensuring patient adoption and engagement with mHealth technologies requires robust educational programs and effective user interfaces to overcome potential barriers to understanding and usability. Addressing these challenges requires collaborative efforts between technology developers, healthcare providers, policymakers, and patient advocacy groups.

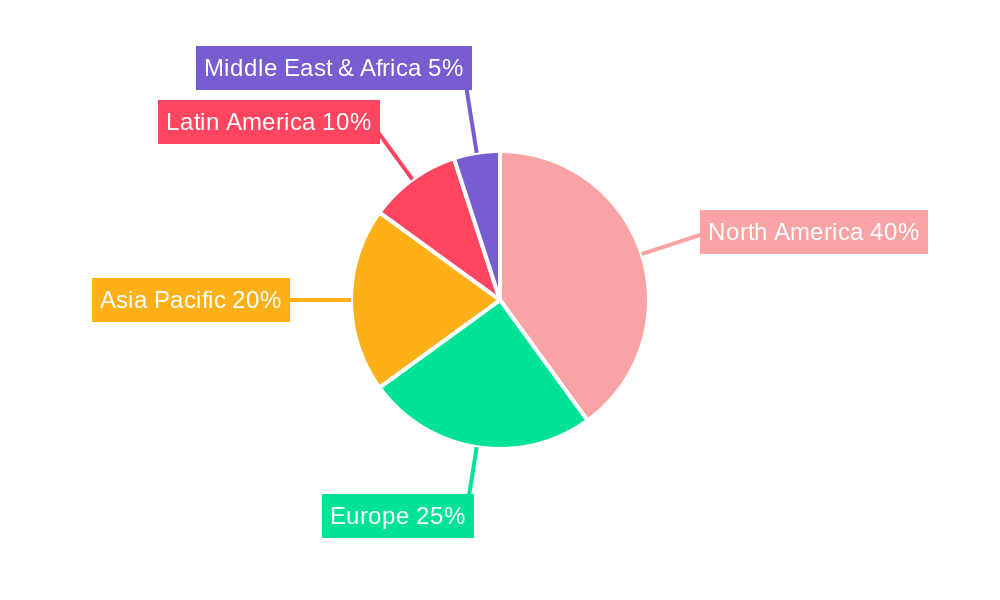

North America: This region is projected to maintain a dominant position due to high technology adoption rates, strong regulatory support, and substantial investments in digital health initiatives. The mature healthcare infrastructure and strong presence of major technology companies further contribute to this dominance. The region’s high per capita healthcare expenditure and willingness to adopt new technologies also play a significant role.

Europe: Significant growth is anticipated, driven by increasing healthcare expenditure, government initiatives supporting digitalization, and the growing prevalence of chronic diseases. Stringent data privacy regulations like GDPR, while presenting challenges, also foster trust in data security, promoting market growth in a compliant environment.

Asia Pacific: This region is expected to witness rapid growth due to the expanding middle class, rising smartphone penetration, and increasing demand for affordable and accessible healthcare. Government investments in digital health infrastructure and the presence of several major technology players are further boosting this market segment.

Segments: Remote Patient Monitoring (RPM) will continue to be a dominant segment, given the growing need for effective management of chronic diseases and the advantages of continuous health tracking. Telemedicine, encompassing virtual consultations and remote diagnosis, is another crucial segment, driven by patient preference for convenience and accessibility. Mobile health apps for personalized wellness and health management are also gaining significant traction.

The paragraph below summarises the above:

The North American and European markets are expected to lead the global mobile health care market in the coming years, driven by factors like high technology adoption, strong regulatory support, and robust healthcare infrastructure. However, the Asia-Pacific region is anticipated to witness the most significant growth due to a burgeoning middle class, increasing smartphone penetration, and rising healthcare expenditure. Within the segments, Remote Patient Monitoring (RPM) and telemedicine will likely dominate, fueled by the growing need for efficient chronic disease management and convenient healthcare access.

The mobile health care industry is fueled by several key growth catalysts. These include the increasing prevalence of chronic diseases demanding efficient management solutions, the rising affordability and accessibility of smartphones and mobile internet, and continuous advancements in sensor technology and data analytics, which are improving the accuracy and functionality of mHealth devices and apps. Government initiatives and regulatory support further encourage market expansion by promoting telehealth and digital health adoption. The trend toward value-based care models also incentivizes the use of mHealth to improve patient outcomes while reducing costs.

This report provides a comprehensive overview of the mobile healthcare market, analyzing historical trends (2019-2024), current market status (2025), and future projections (2025-2033). It delves into key market drivers, challenges, and growth opportunities, offering in-depth analysis of major market segments and key players. The report also highlights significant industry developments and provides a detailed regional analysis, allowing stakeholders to make informed strategic decisions in this rapidly evolving sector. The base year for the analysis is 2025, with the study period extending from 2019 to 2033. Market values are presented in millions of units, providing a clear understanding of the market's substantial size and growth potential.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 30.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 30.3%.

Key companies in the market include NTT DOCOMO, Medtronic PLC, Philips Healthcare, Omron Corporation, Johnson and Johnson, Qualcomm Life, Apple, AT&T, Cisco Systems, Bayer, Samsung Healthcare Solutions, Sanofi, iHealth, Boston Scientific, Athenahealth, BioTelemetry, GE Healthcare, .

The market segments include Type, Application.

The market size is estimated to be USD 172.87 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Mobile Health Care," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Mobile Health Care, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.