1. What is the projected Compound Annual Growth Rate (CAGR) of the Metalworking Fluids?

The projected CAGR is approximately 3.8%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Metalworking Fluids

Metalworking FluidsMetalworking Fluids by Type (Metal Removal Fluids, Metal Forming Fluids, Metal Protecting Fluids, Metal Treating Fluids), by Application (Automotive, General Industry, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

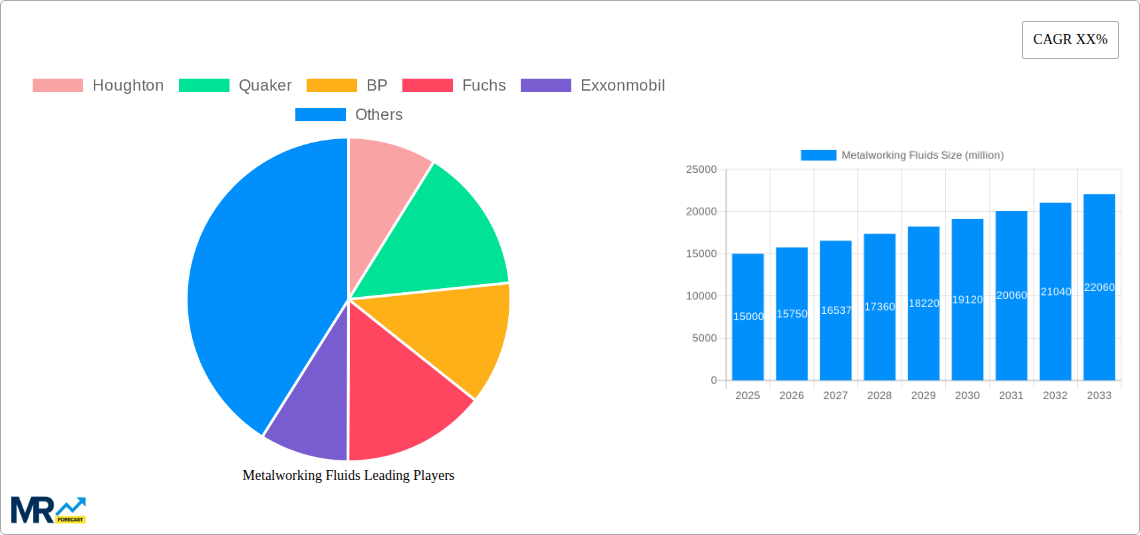

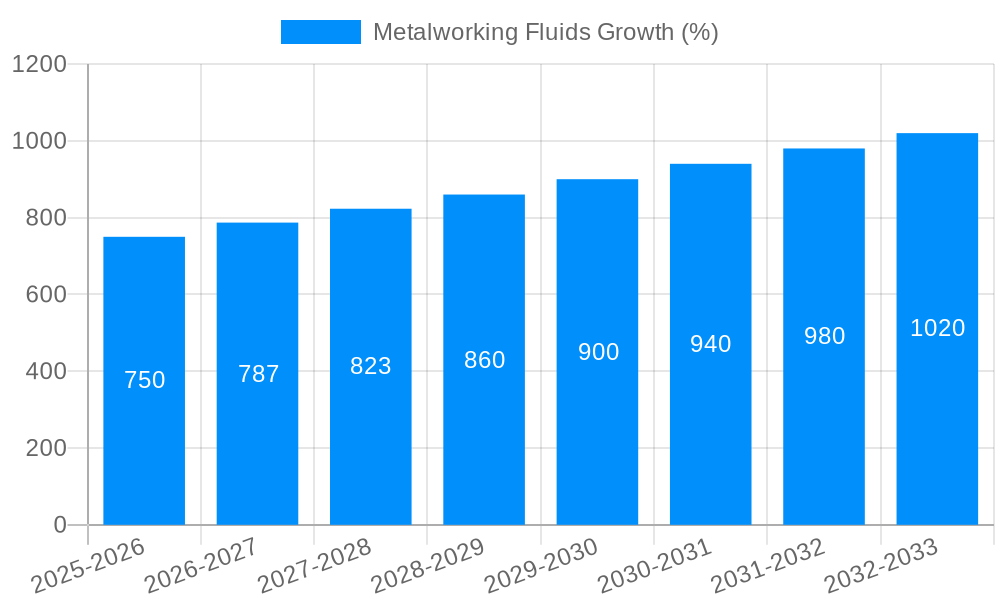

The global Metalworking Fluids market is projected to reach USD 10.8 billion by 2025, demonstrating a steady Compound Annual Growth Rate (CAGR) of 3.8% from 2019 to 2033. This growth is primarily fueled by the expanding automotive sector, which relies heavily on metalworking fluids for machining and fabrication processes, and the broader industrialization across emerging economies. The increasing demand for high-performance lubricants that enhance tool life, improve surface finish, and reduce operational costs directly contributes to market expansion. Furthermore, advancements in fluid formulations, including the development of eco-friendly and biodegradable options, are addressing environmental regulations and growing consumer preference for sustainable manufacturing practices, thereby creating new avenues for market participants. The diverse applications, ranging from metal removal and forming to protection and treatment, cater to a wide spectrum of industries, ensuring consistent demand.

The market is characterized by a competitive landscape featuring major global players like Houghton, Quaker, BP, and Fuchs, alongside specialized lubricant manufacturers. These companies are actively engaged in research and development to innovate fluid technologies that offer superior performance, safety, and environmental compliance. Key trends influencing the market include the adoption of automation in manufacturing, which necessitates advanced fluid management systems, and the growing emphasis on reducing waste and improving energy efficiency in production lines. However, volatile raw material prices, particularly for base oils and additives, present a significant restraint to market growth. Stringent environmental regulations concerning fluid disposal and emissions also pose challenges, pushing manufacturers towards developing more sustainable and less hazardous fluid alternatives. Despite these challenges, the inherent necessity of metalworking fluids in manufacturing, coupled with ongoing technological advancements, positions the market for sustained growth in the coming years.

This report offers an in-depth analysis of the global Metalworking Fluids market, projecting a robust trajectory over the Study Period (2019-2033), with the Base Year (2025) serving as a pivotal point for estimations. The Estimated Year (2025) market size is anticipated to reach a significant $25.3 Billion, demonstrating substantial growth from the Historical Period (2019-2024). The Forecast Period (2025-2033) anticipates a Compound Annual Growth Rate (CAGR) of approximately 4.7%, further solidifying the market's expansion. Our comprehensive coverage will delve into the intricate dynamics that shape this vital industrial sector, providing actionable insights for stakeholders.

The global metalworking fluids market is experiencing a transformative phase, characterized by a strong emphasis on sustainability, advanced formulation, and specialized applications. Key market insights reveal a discernible shift away from traditional, high-VOC (Volatile Organic Compound) formulations towards eco-friendly alternatives. This includes a growing demand for water-based fluids, biodegradable options, and those with reduced toxicity. The market is also witnessing an increasing adoption of synthetic and semi-synthetic fluids, which offer superior performance in terms of cooling, lubrication, and extended tool life, thereby contributing to operational efficiency and cost savings for end-users. A significant trend is the integration of intelligent additives and nanotechnology into metalworking fluids. These advancements aim to enhance specific properties such as extreme pressure resistance, anti-wear capabilities, and corrosion inhibition, catering to the increasingly demanding requirements of modern manufacturing processes. For instance, the use of nanoparticle-infused fluids is showing promising results in reducing friction and wear in high-speed machining operations. Furthermore, the market is responding to stringent environmental regulations and growing health consciousness among workers. This has spurred innovation in the development of fluids that are not only high-performing but also safer for human health and the environment. The circular economy principles are also beginning to influence the market, with increased focus on fluid recycling and waste reduction strategies. Manufacturers are investing in research and development to create fluids that are easier to filter, recondition, and dispose of responsibly. The Metal Removal Fluids segment, driven by the robust growth in the automotive and general industry sectors, is expected to continue its dominance. However, segments like Metal Protecting Fluids are also gaining traction due to the increased emphasis on asset preservation and extended product lifecycles. The evolution of additive technologies, coupled with a deeper understanding of tribology, is enabling the creation of highly specialized fluids tailored to specific metal alloys and machining operations, paving the way for precision manufacturing and enhanced productivity.

The metalworking fluids market is experiencing a powerful surge driven by several interconnected factors. A primary impetus is the relentless growth in manufacturing activities globally, particularly within the automotive and general industrial sectors. The increasing production of vehicles, machinery, and complex components necessitates a corresponding increase in metalworking operations, directly translating to higher demand for effective fluids. Automation and the adoption of advanced manufacturing technologies, such as CNC machining, are also significant drivers. These sophisticated processes require highly specialized and performant metalworking fluids to ensure precision, speed, and the longevity of cutting tools and machinery. The pursuit of enhanced operational efficiency and reduced downtime further fuels this demand, as businesses seek to optimize production cycles and minimize costs. Moreover, ongoing technological advancements in fluid formulation are playing a crucial role. Innovations in synthetic and semi-synthetic fluid technologies, coupled with the integration of novel additives, are leading to fluids with superior cooling, lubrication, and corrosion protection properties. This allows manufacturers to achieve tighter tolerances, improve surface finish, and extend the lifespan of their equipment. The growing global emphasis on sustainability and environmental responsibility is also a key propellant, albeit with a dual effect. While it drives the development of eco-friendlier fluids, it also necessitates investment in research and development, pushing the market towards more advanced and compliant solutions. Furthermore, rising industrialization in emerging economies, coupled with substantial government investments in manufacturing infrastructure, is creating new avenues for market expansion and increased consumption of metalworking fluids.

Despite its robust growth trajectory, the metalworking fluids market encounters several significant challenges and restraints that warrant careful consideration. One of the foremost hurdles is the increasing stringency of environmental regulations worldwide. Compliance with evolving standards regarding biodegradability, toxicity, and waste disposal necessitates substantial investment in research and development for new formulations, increasing operational costs for manufacturers. The disposal of spent metalworking fluids also presents a considerable challenge, as improper disposal can lead to severe environmental contamination, leading to regulatory penalties and reputational damage. Another restraint is the volatile pricing of raw materials, particularly petrochemical derivatives that form the base of many conventional metalworking fluids. Fluctuations in crude oil prices can directly impact the cost of production, affecting profit margins and potentially leading to price increases for end-users. The economic downturns and recessions experienced globally can also dampen demand for metalworking fluids, as manufacturing output slows down. Furthermore, the initial capital investment required for advanced fluid management systems, including filtration and recycling equipment, can be a barrier for small and medium-sized enterprises (SMEs), limiting their adoption of more efficient and sustainable practices. The need for specialized training for personnel in handling and maintaining these fluids also adds to the operational complexity. Finally, the competition from alternative manufacturing processes, such as additive manufacturing (3D printing), which may require different or no metalworking fluids at all in certain stages, poses a long-term, albeit nascent, threat to traditional metalworking fluid consumption.

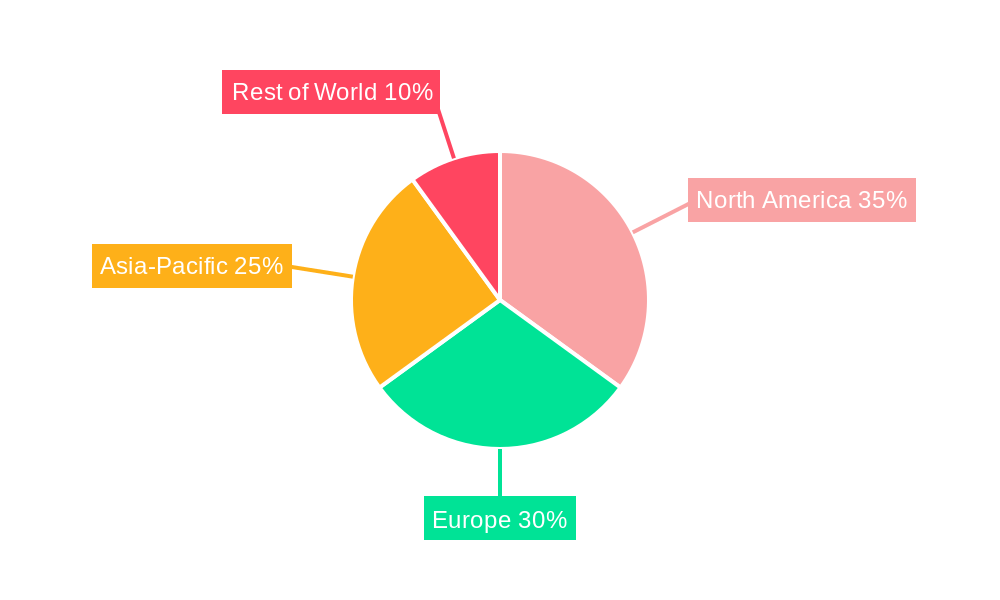

The global metalworking fluids market is characterized by regional dominance and segment leadership, with the Automotive application segment and the Asia Pacific region poised to be the primary drivers of growth.

Asia Pacific Region: This region is set to dominate the metalworking fluids market due to a confluence of factors.

Automotive Application Segment: The automotive sector is expected to be the largest and most influential segment within the metalworking fluids market.

Other significant regions and segments contributing to market growth include the General Industry segment, which encompasses a broad range of manufacturing activities, and the Europe and North America regions, which, while mature, continue to drive demand through technological innovation and high-value manufacturing.

Several key factors are acting as significant growth catalysts for the metalworking fluids industry. The increasing demand for high-performance and sustainable fluid formulations, driven by stringent environmental regulations and a growing focus on worker safety, is pushing innovation. Advancements in nanotechnology and intelligent additives are enabling the development of fluids with enhanced properties, such as superior lubrication, cooling, and wear resistance, catering to the evolving needs of precision manufacturing. The robust growth in the automotive sector, coupled with the expanding manufacturing base in emerging economies, is directly translating to higher consumption of metalworking fluids. Furthermore, the adoption of advanced manufacturing technologies like automation and CNC machining necessitates the use of specialized and efficient fluids, creating a sustained demand.

This comprehensive report delves into the intricacies of the global metalworking fluids market, offering a detailed outlook from the Historical Period (2019-2024) through the Study Period (2019-2033), with a focus on the Base Year (2025) and its projections. The market is estimated to reach $25.3 Billion in 2025, showcasing a dynamic growth trajectory. Our analysis covers critical segments such as Metal Removal Fluids, Metal Forming Fluids, Metal Protecting Fluids, and Metal Treating Fluids, and their applications across the Automotive, General Industry, and Others sectors. The report meticulously explores prevailing market trends, driving forces like industrial growth and technological advancements, and the challenges posed by environmental regulations and raw material price volatility. Furthermore, it highlights key regions and segments poised for dominance, particularly the Asia Pacific region and the Automotive application. The report also identifies significant growth catalysts and provides an exhaustive list of leading players in the industry, alongside a timeline of crucial developments that have shaped and will continue to shape this vital market. This in-depth coverage equips stakeholders with the knowledge necessary to navigate the evolving landscape of metalworking fluids.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.8%.

Key companies in the market include Houghton, Quaker, BP, Fuchs, Exxonmobil, Metalworking Lubricants, Chevron, Henkel, Milacron, Chemtool, Yushiro, Master Chemical, Blaser, Dow.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Metalworking Fluids," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Metalworking Fluids, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.