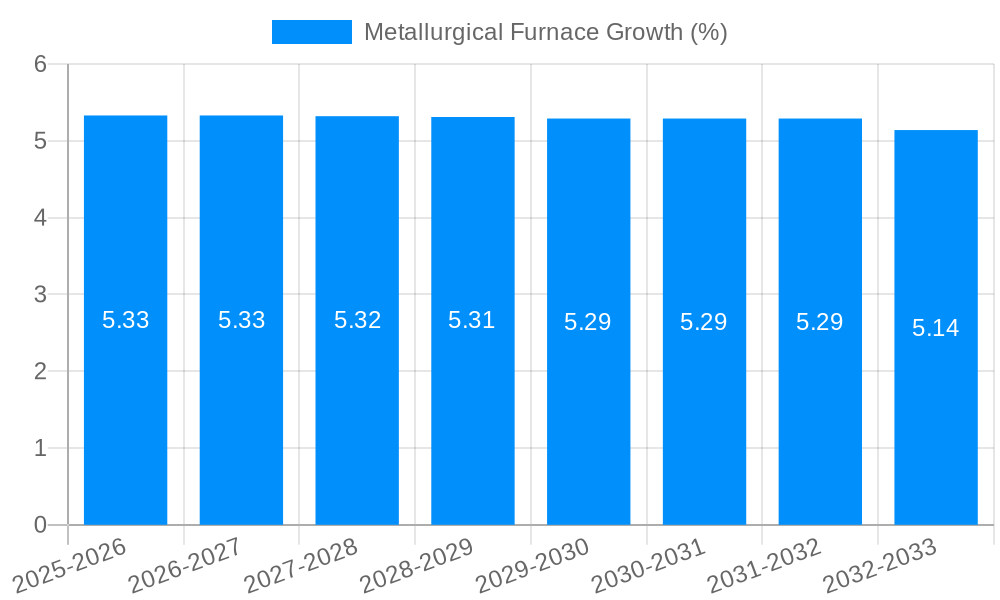

1. What is the projected Compound Annual Growth Rate (CAGR) of the Metallurgical Furnace?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Metallurgical Furnace

Metallurgical FurnaceMetallurgical Furnace by Type (/> Combustion Type, Electric Type), by Application (/> Ironmaking Plant, Steelmaking, Foundry, Laboratory, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

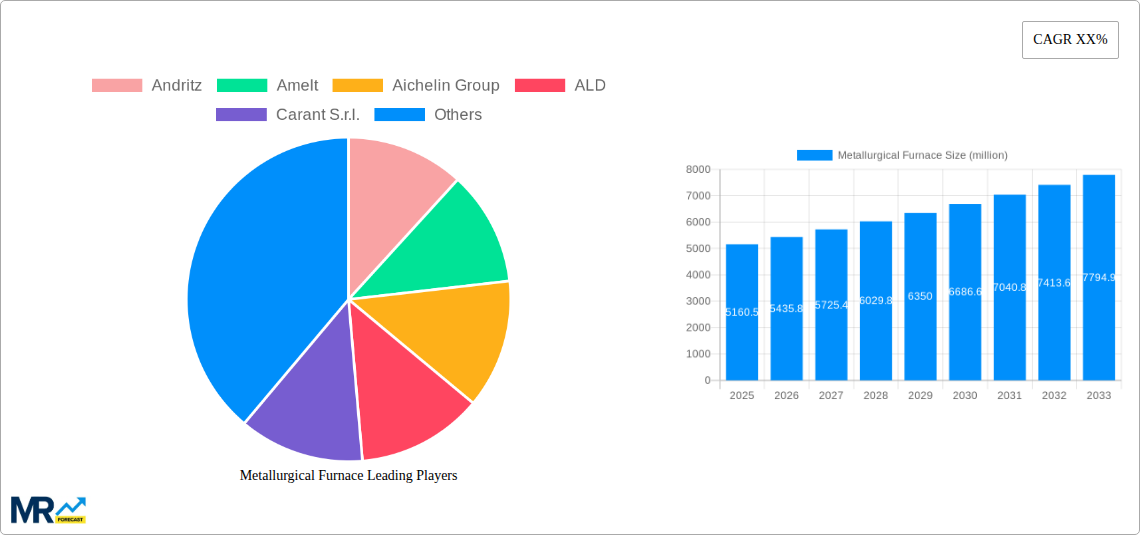

The global metallurgical furnace market is poised for significant expansion, projected to reach USD 5160.5 million by 2025, and is expected to experience robust growth. This surge is fueled by escalating demand from critical industries such as ironmaking, steelmaking, and foundries, driven by ongoing infrastructure development and the automotive sector's increasing need for high-quality metal components. The transition towards more efficient and environmentally friendly manufacturing processes is also a key accelerator. Electric type furnaces, in particular, are gaining traction due to their lower emissions and superior energy efficiency, aligning with global sustainability goals and stringent environmental regulations. Technological advancements leading to improved furnace performance, automation, and predictive maintenance further bolster market prospects.

Several key trends are shaping the metallurgical furnace landscape. The increasing adoption of advanced materials and sophisticated alloying techniques in various applications necessitates highly controlled thermal processing environments, which modern metallurgical furnaces provide. Furthermore, the integration of Industry 4.0 technologies, including IoT sensors and data analytics, is optimizing furnace operations, reducing downtime, and enhancing product consistency. While the market is dynamic, potential restraints include the high initial capital investment required for advanced furnace systems and the fluctuating raw material costs that can impact operational expenses for end-users. Despite these challenges, the strategic importance of metallurgical furnaces in the production of essential metals, coupled with continuous innovation, ensures a promising outlook for market growth in the coming years.

This report provides a comprehensive analysis of the global metallurgical furnace market, offering strategic insights for stakeholders looking to navigate its evolving landscape. Spanning a study period of 2019-2033, with a base year of 2025, the report leverages historical data from 2019-2024 and forecasts future trends from 2025-2033. The market is segmented by furnace type (combustion and electric) and application (ironmaking plants, steelmaking, foundries, laboratories, and others). We will explore key industry developments, driving forces, challenges, regional dominance, and leading players, painting a clear picture of market dynamics, with a focus on the estimated market size in the millions.

The global metallurgical furnace market is poised for significant expansion, projected to reach an estimated value of USD 15,000 million by the end of 2025. This robust growth trajectory is underpinned by a confluence of factors, including the burgeoning demand for high-performance metals across diverse industrial sectors, an increasing emphasis on energy efficiency and sustainability within metal processing operations, and continuous technological advancements aimed at enhancing furnace performance and reducing environmental impact. The historical period of 2019-2024 witnessed steady growth, driven by infrastructure development and the automotive industry's robust demand for steel and aluminum. Looking ahead, the forecast period of 2025-2033 is expected to accelerate this growth, fueled by emerging applications in aerospace, defense, and renewable energy sectors, all of which rely heavily on specialized metallurgical processes.

Furthermore, the market is experiencing a discernible shift towards electric furnaces, particularly induction and arc furnaces, owing to their superior energy efficiency, precise temperature control, and reduced emissions compared to traditional combustion furnaces. This trend is further amplified by increasing government regulations and incentives aimed at curbing greenhouse gas emissions, pushing manufacturers to adopt cleaner and more sustainable metal processing technologies. The application segment of steelmaking is expected to remain the largest contributor to market revenue, driven by the ongoing global demand for construction materials and automotive components. However, the foundry segment is also demonstrating remarkable growth, propelled by the increasing adoption of advanced casting techniques and the rising demand for complex metal parts in various industries. The integration of advanced automation, AI-powered process control, and smart manufacturing technologies is also becoming a critical trend, promising to optimize furnace operations, improve product quality, and reduce operational costs. The overall market sentiment is optimistic, with continuous innovation and a growing awareness of sustainability driving significant investment and development in the metallurgical furnace sector.

The metallurgical furnace market is experiencing a powerful surge driven by several interconnected forces. Foremost among these is the ever-increasing global demand for metals, particularly steel and aluminum, which are fundamental to infrastructure development, construction, and the manufacturing of automobiles, aircraft, and electronic devices. As economies worldwide continue to grow and urbanize, the need for these essential materials escalates, directly translating into a higher demand for the furnaces that process them. Furthermore, a critical catalyst for growth is the relentless pursuit of energy efficiency and environmental sustainability within the metals industry. With increasing scrutiny on carbon footprints and stricter environmental regulations, there is a palpable shift towards adopting advanced furnace technologies that minimize energy consumption and reduce harmful emissions. This includes a growing preference for electric furnaces over traditional combustion-based systems due to their inherent efficiency and lower environmental impact, especially when powered by renewable energy sources.

Moreover, technological innovation plays a pivotal role in propelling the market forward. Continuous research and development are leading to the creation of more sophisticated and efficient furnaces equipped with advanced control systems, improved insulation, and optimized heating mechanisms. These advancements not only enhance productivity and product quality but also contribute to significant cost savings for manufacturers. The growing demand for high-performance alloys and specialized metals for advanced applications in sectors like aerospace, defense, and renewable energy also fuels the need for specialized metallurgical furnaces capable of achieving precise temperature control and unique processing conditions. The development of smaller, more flexible furnaces for niche applications and laboratory research further broadens the market's scope. Ultimately, the combination of fundamental demand, sustainability imperatives, and technological progress creates a dynamic and expanding environment for the metallurgical furnace industry.

Despite the promising growth trajectory, the metallurgical furnace market is not without its impediments. A significant challenge revolves around the high initial capital investment required for acquiring and installing advanced metallurgical furnaces. These sophisticated pieces of industrial equipment, especially those incorporating cutting-edge technologies like induction heating or advanced automation, represent a substantial financial outlay for manufacturers, particularly for small and medium-sized enterprises (SMEs) or those operating in emerging economies. This can act as a considerable restraint on market penetration and adoption rates, slowing down the transition to more efficient and sustainable technologies. Furthermore, the increasingly stringent environmental regulations and emission standards, while a driver for sustainable technologies, also pose a challenge. Companies need to invest heavily in retrofitting existing furnaces or procuring new ones that meet these evolving standards, which can be a complex and costly undertaking.

Another restraint stems from the availability and cost of skilled labor. Operating and maintaining advanced metallurgical furnaces requires a highly specialized workforce with expertise in metallurgy, electrical engineering, and automation. A shortage of such skilled professionals can lead to operational inefficiencies, increased downtime, and hinder the effective utilization of advanced furnace technologies. The volatility in raw material prices, such as scrap metal and ferroalloys, can also impact the overall profitability of metallurgical operations, indirectly affecting investment in new furnace technologies. Additionally, the long replacement cycles for existing furnaces mean that widespread adoption of new technologies can take considerable time, even when the benefits are evident. Finally, geopolitical uncertainties and trade barriers can disrupt supply chains for components and raw materials, potentially leading to production delays and increased costs, thereby acting as a restraint on market expansion.

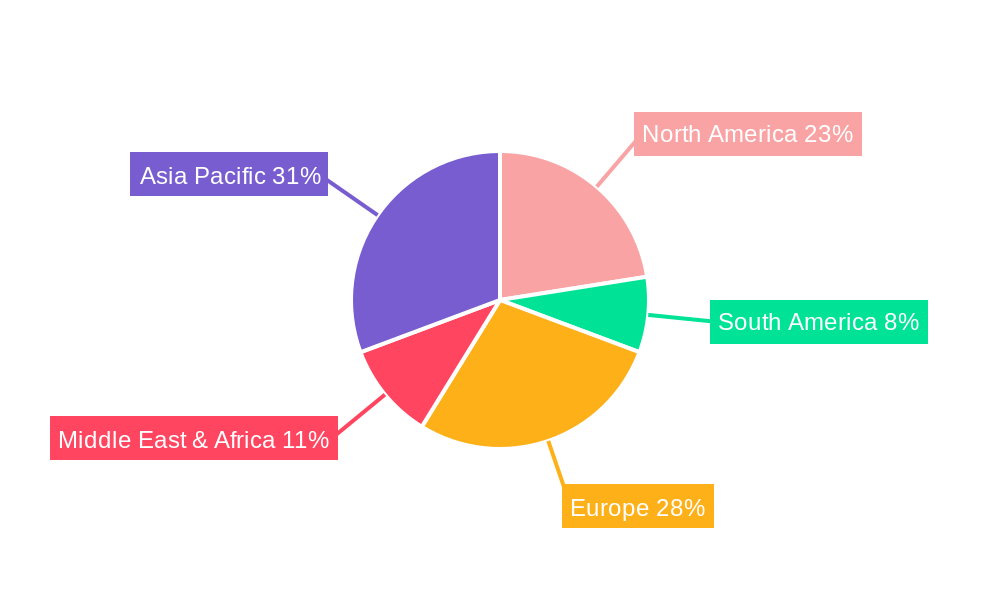

The global metallurgical furnace market is characterized by a significant regional concentration of demand and production, with Asia Pacific emerging as the dominant force. This dominance is largely attributed to the region's robust industrial base, burgeoning manufacturing sector, and massive infrastructure development initiatives. Countries like China and India, in particular, are leading the charge, driven by their expansive steel and aluminum production capabilities, a growing automotive industry, and substantial investments in construction projects. China, as the world's largest producer of steel, naturally commands a significant share of the metallurgical furnace market, with a strong presence of domestic manufacturers and a consistent demand for both new installations and upgrades. India's rapidly industrializing economy and ambitious infrastructure plans further bolster its position. The increasing adoption of advanced manufacturing technologies and a focus on enhancing production efficiency within these nations are significant drivers for the adoption of sophisticated furnace solutions.

Within the Asia Pacific region, the Steelmaking application segment is projected to be the largest contributor to market revenue, projected to account for over USD 7,000 million by 2025. This is directly linked to the sheer volume of steel produced globally, essential for everything from skyscrapers to consumer goods. The demand for high-quality steel, necessitating advanced smelting and refining processes, fuels the need for specialized furnaces. Following closely, the Foundry segment is also experiencing substantial growth, driven by the increasing demand for intricate metal components in sectors such as automotive, aerospace, and heavy machinery. The ability of modern foundries to produce complex shapes and high-precision parts relies heavily on advanced casting and heat treatment furnaces.

Another key factor in the Asia Pacific's dominance is the region's proactive approach to adopting Electric Type furnaces. Driven by both economic incentives and increasing environmental consciousness, countries in this region are actively transitioning towards electric arc furnaces (EAFs) and induction furnaces due to their higher energy efficiency and lower emissions compared to conventional combustion furnaces. The availability of abundant energy, coupled with government policies promoting cleaner industrial practices, further accelerates this shift. While other regions like North America and Europe are significant markets, particularly for high-end, specialized furnace technologies and in the pursuit of decarbonization, the sheer scale of industrial activity and manufacturing output in Asia Pacific positions it as the undeniable leader in terms of overall market volume and revenue. The continuous investment in new capacity and technological upgrades within this region solidifies its leading position for the foreseeable future.

Several key factors are acting as potent growth catalysts for the metallurgical furnace industry. The persistent global demand for metals, driven by infrastructure development, automotive manufacturing, and emerging technologies, provides a foundational impetus. Simultaneously, the urgent need for sustainability and reduced environmental impact is forcing industries to adopt more energy-efficient and low-emission furnace technologies, thereby driving innovation and market expansion. Advancements in automation, AI, and smart manufacturing are enabling higher productivity, better quality control, and cost savings, making newer furnace models increasingly attractive to manufacturers. Finally, the growing demand for specialized alloys and high-performance metals for niche applications in aerospace, defense, and renewable energy sectors is spurring the development and adoption of highly specialized and precise metallurgical furnaces.

The metallurgical furnace market is populated by a diverse range of global and regional players, each contributing to the industry's innovation and growth. Prominent companies shaping this landscape include:

The metallurgical furnace sector has witnessed several key advancements and strategic moves in recent years, highlighting the industry's dynamic nature. These developments, often driven by technological innovation and market demands, are crucial indicators of future trends:

This report offers a holistic and in-depth examination of the metallurgical furnace market, providing actionable intelligence for strategic decision-making. It meticulously analyzes market size and growth projections, underpinned by robust historical data and future forecasts, with estimated market values in the millions. The report delves into the intricate interplay of driving forces, such as escalating global metal demand and the imperative for sustainable practices, alongside the challenges posed by high capital expenditure and stringent regulations. It identifies dominant regions and key application segments, offering insights into where future market opportunities lie. Furthermore, it highlights crucial growth catalysts and provides a comprehensive overview of leading industry players and their recent strategic developments. This all-encompassing approach ensures that stakeholders are equipped with the knowledge to effectively navigate the complexities and capitalize on the opportunities within the evolving metallurgical furnace landscape.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Andritz, Amelt, Aichelin Group, ALD, Carant S.r.l., Danieli, DOWA HOLDINGS, ECM Group, Inductotherm Corp, IHI Corp, JP Steel Plantech Co., Kalyani Furnaces, Nabertherm, MG Electricals, Phoenix Furnace, Primetals Technologies, SECO/WARWICK, SMS Group, Silcarb Recrystallized, Tenova, .

The market segments include Type, Application.

The market size is estimated to be USD 5160.5 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Metallurgical Furnace," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Metallurgical Furnace, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.