1. What is the projected Compound Annual Growth Rate (CAGR) of the Metal Materials for Additive Manufacturing?

The projected CAGR is approximately XX%.

Metal Materials for Additive Manufacturing

Metal Materials for Additive ManufacturingMetal Materials for Additive Manufacturing by Type (Selective Laser Melting (SLM), Electronic Beam Melting (EBM), Other), by Application (Automotive Industry, Aerospace Industry, Healthcare & Dental Industry, Academic Institutions, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

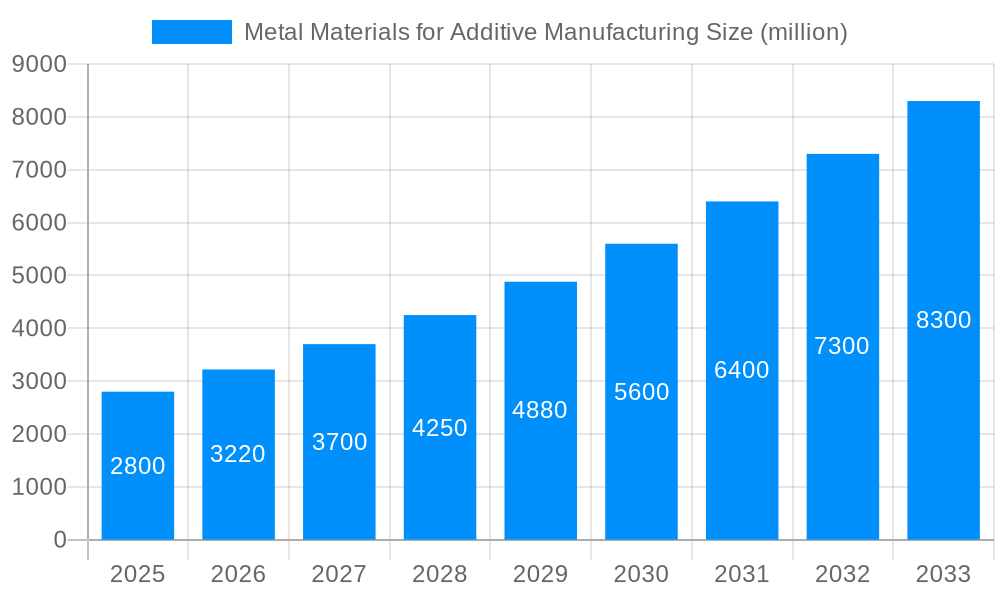

The global market for Metal Materials for Additive Manufacturing (AM) is experiencing robust growth, driven by increasing adoption across diverse industries like aerospace, automotive, and medical. The market's expansion is fueled by several key factors: the rising demand for lightweight and high-strength components, the need for customized designs and faster prototyping, and the ongoing technological advancements in AM processes such as Selective Laser Melting (SLM) and Electron Beam Melting (EBM). The market is segmented by material type (Titanium alloys, Stainless steel, Aluminum alloys, Nickel alloys, etc.), process, and application. While the precise market size in 2025 is unavailable, considering a plausible CAGR of 15-20% based on industry reports and the current market momentum, a reasonable estimate for the 2025 market value would fall within the range of $2.5 billion to $3 billion. This significant figure underscores the substantial investment and innovation within the sector.

Looking ahead to 2033, continued growth is projected, although the CAGR might slightly moderate to around 12-15% as the market matures. Factors influencing this projection include the potential for price stabilization of metal powders, the development of more efficient and cost-effective AM processes, and the broadening adoption across various sectors. However, challenges remain, including the relatively high cost of metal powders compared to traditional manufacturing methods, the need for skilled operators, and the potential for inconsistencies in material properties. Despite these restraints, the overall outlook for Metal Materials for Additive Manufacturing remains extremely positive, driven by continuous innovation and the inherent advantages offered by AM technologies in terms of design flexibility, efficiency, and sustainability.

The global metal materials for additive manufacturing (AM) market is experiencing explosive growth, projected to reach a valuation exceeding $XX billion by 2033, up from $XX billion in 2025. This remarkable expansion is driven by a confluence of factors, including the increasing adoption of AM technologies across diverse industries and the continuous development of new metal alloys optimized for additive processes. The historical period (2019-2024) witnessed significant advancements in material science and printing technologies, laying the groundwork for the robust forecast period (2025-2033). Key market insights reveal a strong preference for titanium alloys and stainless steels, owing to their exceptional strength-to-weight ratios and corrosion resistance, making them ideal for aerospace and medical applications. However, the market is not without its nuances. The high cost of AM materials remains a barrier to wider adoption, particularly in cost-sensitive sectors. This cost factor significantly influences the selection of materials, with companies often opting for materials offering a balance between performance and affordability. Furthermore, the market is witnessing a growing interest in niche materials like nickel-based superalloys and cobalt-chromium alloys, driven by the demand for high-performance components in specific industries like energy and automotive. The market's dynamism is also shaped by ongoing research and development efforts aimed at improving material properties, expanding material selection, and streamlining post-processing methods. The trend towards standardization and certification of AM materials further strengthens market confidence and drives broader acceptance across various industries. The estimated market value in 2025 signifies a crucial juncture, reflecting the culmination of past advancements and the foundation for future expansion.

Several key factors are fueling the growth of the metal materials for AM market. Firstly, the increasing demand for lightweight and high-performance components across various industries, particularly aerospace, automotive, and medical, is a major driver. AM’s ability to create complex geometries and intricate designs that are impossible to achieve through traditional manufacturing methods directly addresses this need. Secondly, the rising adoption of AM technologies by small and medium-sized enterprises (SMEs) is expanding the market's reach. While initially adopted primarily by large corporations, the decreasing costs and increasing accessibility of AM systems are enabling SMEs to leverage the technology's benefits. Thirdly, ongoing advancements in material science are continually expanding the range of metal alloys suitable for AM. This allows for the creation of components with tailored properties, optimizing performance for specific applications. Finally, government initiatives and research funding are playing a crucial role in accelerating innovation and fostering market growth. These initiatives aim to promote the development and adoption of AM technologies, making them more accessible and cost-effective. The synergistic effect of these factors is creating a highly dynamic and rapidly evolving market, with significant potential for continued growth in the years to come.

Despite the substantial growth potential, several challenges and restraints hinder the widespread adoption of metal materials in AM. The high cost of metal powders and the complexity of the AM process itself remain significant barriers. The relatively high production costs compared to traditional manufacturing methods often make AM less attractive, especially for large-scale production runs. Furthermore, ensuring the consistent quality and reproducibility of AM parts is crucial, and achieving this can be challenging. Stringent quality control measures are essential to maintain the reliability and performance of AM components, leading to added expenses. Additionally, the availability of skilled personnel to operate and maintain AM systems and to conduct post-processing operations remains a bottleneck. A lack of trained professionals can limit the capacity of industries to adopt AM technologies effectively. Lastly, concerns about the environmental impact of AM, such as powder handling, energy consumption, and waste generation, need to be addressed to ensure sustainable growth. Overcoming these challenges and restraints through continuous innovation in materials, processes, and training will be critical for the continued expansion of the metal materials for AM market.

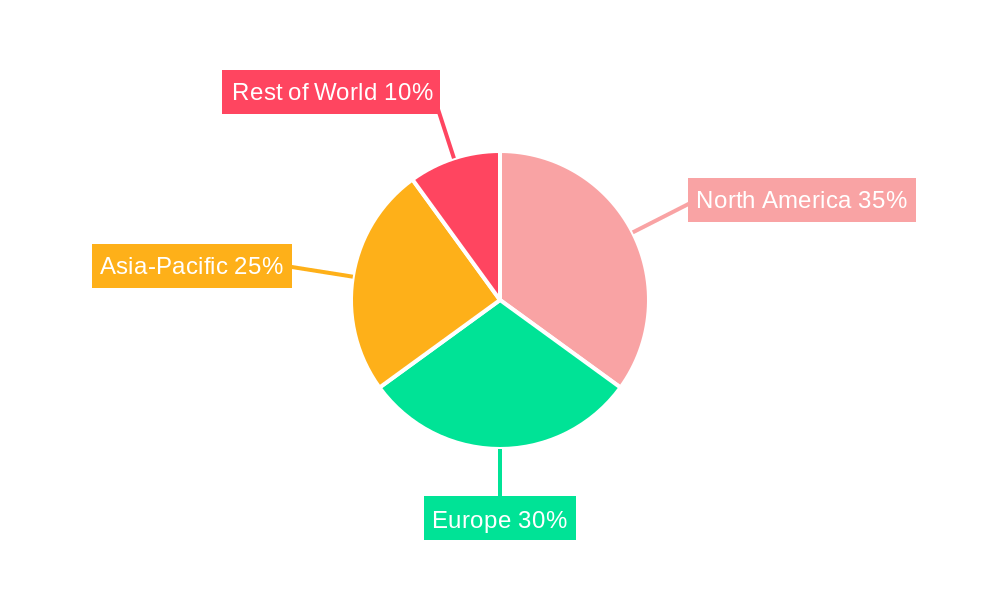

The metal materials for AM market exhibits a geographically diverse landscape, with several key regions and segments emerging as dominant forces.

North America: The region holds a significant share of the market, driven by the presence of major aerospace and medical device manufacturers and strong government support for advanced manufacturing technologies. The US particularly leads in research and development activities in AM.

Europe: The European market is also a significant contributor, bolstered by a robust automotive sector and established AM technology providers. Germany and the UK are key players within this region.

Asia-Pacific: This region is witnessing rapid growth, propelled by increasing investments in AM technologies from countries such as China, Japan, and South Korea. Their burgeoning manufacturing sectors are fueling the demand for AM materials.

Segments:

Titanium Alloys: The high strength-to-weight ratio and biocompatibility of titanium alloys make them highly sought after in aerospace and medical applications, positioning this segment for substantial growth. The demand is particularly high for aerospace applications, where weight reduction is critical.

Stainless Steels: The versatility and corrosion resistance of stainless steels make them suitable for a wide range of applications, contributing significantly to market volume. The cost-effectiveness compared to other high-performance materials also fuels its popularity.

Nickel-Based Superalloys: These alloys offer exceptional high-temperature strength and creep resistance, making them crucial for applications in aerospace engines and energy generation. Although a smaller segment compared to others, it shows impressive growth potential due to its high added value.

Cobalt-Chromium Alloys: The biocompatibility and wear resistance of cobalt-chromium alloys establish them as a leading material for medical implants, ensuring stable growth in this niche segment. The demand is closely tied to the increasing prevalence of orthopedic surgeries and other implant procedures.

In summary, while North America and Europe currently hold leading market positions, the Asia-Pacific region is rapidly catching up, fueled by significant economic growth and investment in AM technologies. Within the segments, titanium alloys and stainless steels lead in terms of volume, while niche materials like nickel-based superalloys and cobalt-chromium alloys are experiencing strong growth due to their high-performance characteristics and specialized applications. The overall market is characterized by strong growth across all regions and segments, signifying considerable potential for future expansion.

The metal materials for additive manufacturing industry is experiencing robust growth driven by several key catalysts. The increasing demand for lightweight yet high-strength components in industries like aerospace and automotive is a significant factor. Further advancements in material science lead to the development of new alloys optimized for additive manufacturing processes, which in turn expand the scope of potential applications. Growing adoption of AM across various sectors, coupled with government support and increasing research investments, is also accelerating market expansion.

This report provides a comprehensive analysis of the metal materials for additive manufacturing market, offering detailed insights into market trends, driving forces, challenges, key players, and significant developments. The report covers the historical period from 2019 to 2024, providing a robust base for understanding current market dynamics and estimating future growth (2025-2033). The detailed analysis helps businesses to understand the market landscape, identify opportunities, and develop effective strategies for success in this rapidly evolving sector. The report also encompasses regional and segmental breakdowns, providing a granular view of market dynamics across different geographical locations and material types.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

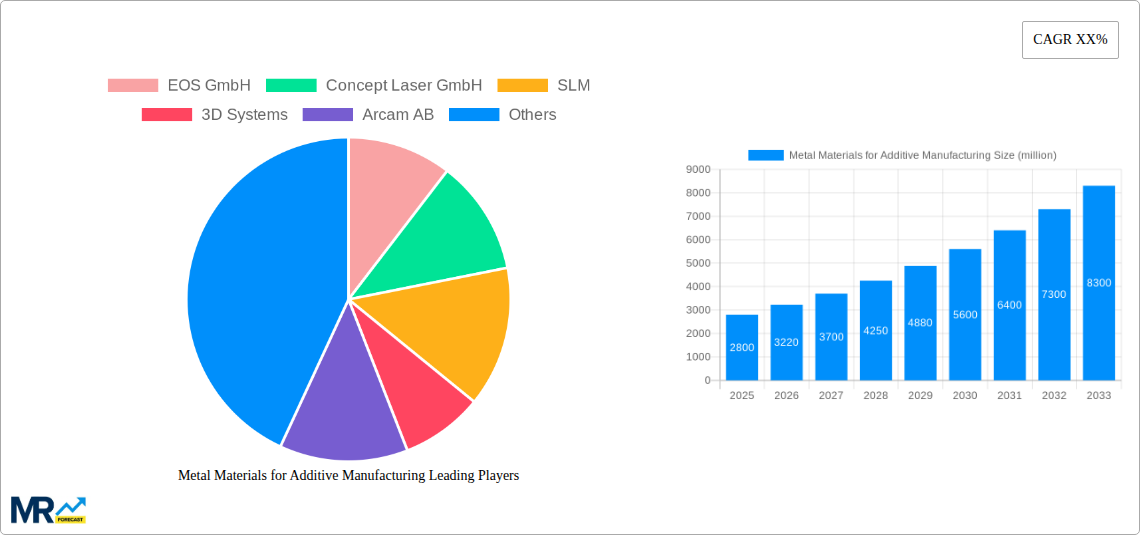

Key companies in the market include EOS GmbH, Concept Laser GmbH, SLM, 3D Systems, Arcam AB, ReaLizer, Renishaw, Exone, Wuhan Binhu, Bright Laser Technologies, Huake 3D, Syndaya, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Metal Materials for Additive Manufacturing," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Metal Materials for Additive Manufacturing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.