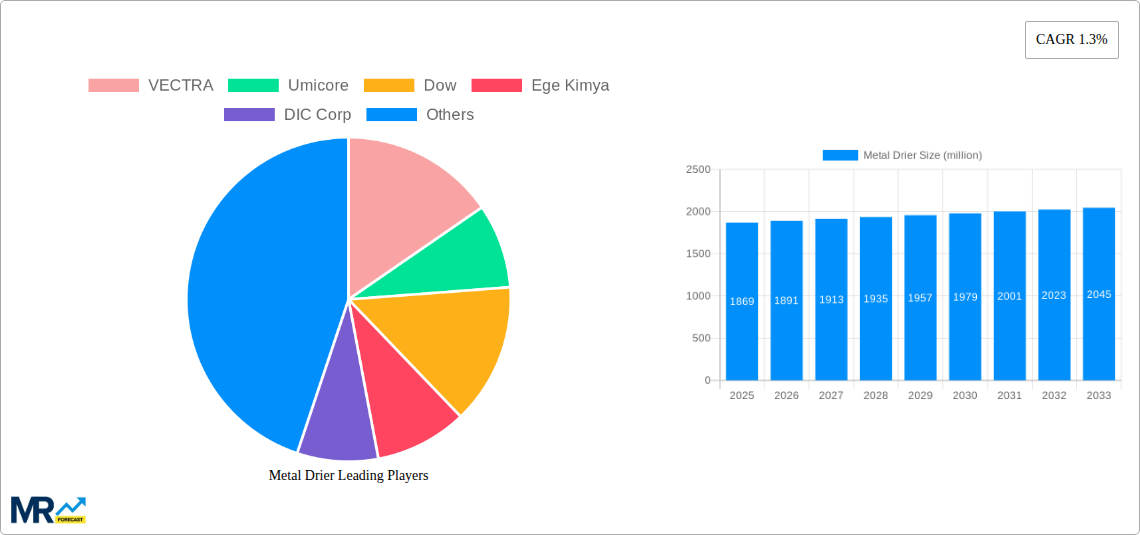

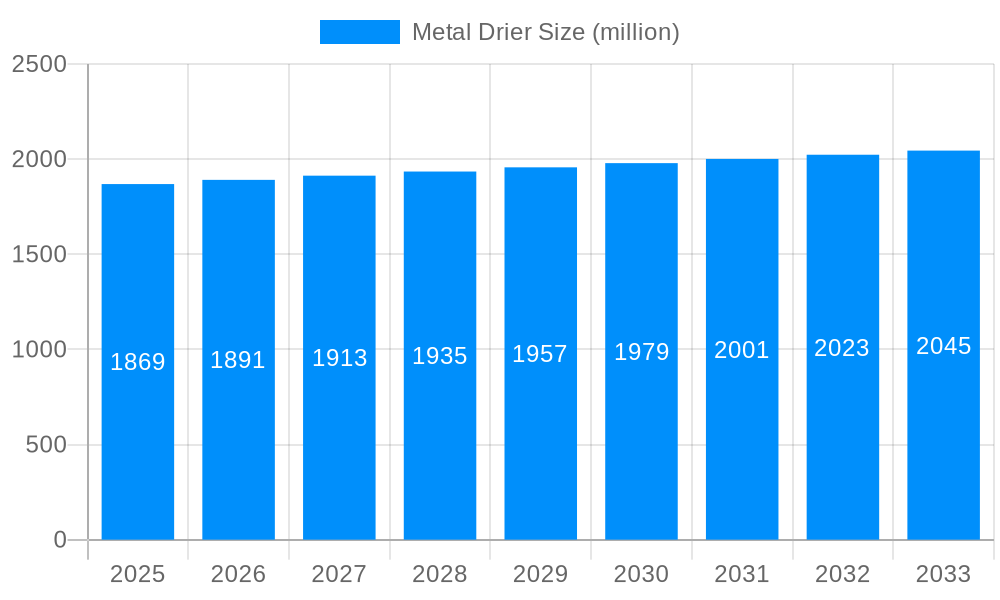

1. What is the projected Compound Annual Growth Rate (CAGR) of the Metal Drier?

The projected CAGR is approximately 1.3%.

Metal Drier

Metal DrierMetal Drier by Type (Cobalt Driers, Lead Driers, Zirconium Driers, Calcium Driers, Strontium Driers, Manganese Driers, Zinc Driers, Barium Driers, Cerium Driers, Others), by Function (Primary Drier, Auxiliary Drier, Through Drier), by Solvent (Solvent-based, Water-based), by Application (Paints, Coatings, Printing Inks, Adhesives & Sealants, Others), by Sales Channel (Direct Sales, Distributors/Wholesalers, Online), by End User Industry (Building & Construction, Automotive & Transportation, Industrial Manufacturing, Marine, Wood & Furniture, Packaging, Consumer Goods, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global Metal Drier Market is a critical component within the broader industrial chemicals landscape, primarily serving the paints, coatings, inks, and adhesives sectors. Valued at an estimated USD 1841.8 million in the base year, this market is projected to reach approximately USD 2071.0 million by 2033, demonstrating a steady Compound Annual Growth Rate (CAGR) of 1.3% over the forecast period. This moderate growth trajectory reflects a mature market characterized by stringent regulatory shifts and continuous innovation. The demand for metal driers is intrinsically linked to the performance requirements of oxidative curing systems, which are essential for achieving desired film properties in various applications.

Key demand drivers include the robust expansion of the global building & construction industry, particularly in emerging economies, and the sustained growth in automotive and transportation sectors, which heavily rely on advanced coatings. Furthermore, the increasing adoption of water-based and high-solids formulations across industries, driven by environmental regulations and sustainability goals, necessitates the development and use of specialized metal driers that offer enhanced performance in these systems. The historical dominance of conventional driers, such as those based on cobalt, is gradually being challenged by the advent of lead-free and low-VOC alternatives, including zirconium, calcium, and bismuth-based formulations. This transition underscores a fundamental shift in product development strategies, focusing on eco-friendliness without compromising drying efficiency.

Macro tailwinds such as rapid urbanization, infrastructure development projects, and the rising disposable incomes fueling demand for consumer goods contribute significantly to the consumption of paints and coatings, thereby indirectly boosting the Metal Drier Market. However, the market faces headwinds from volatile raw material prices, particularly for the metallic components and organic acids used in drier production, and increasingly strict environmental legislations. The outlook for the Metal Drier Market remains stable, with innovation in non-toxic and high-performance solutions poised to shape its future trajectory, ensuring its continued relevance within the Specialty Chemicals Market.

The application segment for paints and coatings stands as the undeniable dominant force within the global Metal Drier Market, representing the largest share of revenue. Metal driers are indispensable additives in solvent-borne and certain water-borne paint and coating formulations, facilitating the oxidative polymerization of film-forming binders (such as alkyds, epoxies, and polyurethanes) to accelerate drying and hardening processes. This critical function ensures the rapid development of film properties like hardness, gloss, and chemical resistance, which are vital for protective and decorative applications across numerous end-use industries.

The widespread usage of metal driers in the Paints & Coatings Market can be attributed to several factors. Firstly, the sheer volume of paint and coating production globally, driven by sectors such as building & construction, automotive & transportation, industrial manufacturing, and wood & furniture, creates a constant, high demand for these essential additives. From architectural coatings for residential and commercial structures to corrosion-protective coatings for industrial machinery and automotive finishes, the versatility and performance requirements of paints and coatings necessitate efficient drying mechanisms.

Historically, the Cobalt Driers Market has played a pivotal role in this segment due to cobalt's exceptional catalytic activity in initiating surface drying. However, increasing regulatory scrutiny regarding the toxicity of cobalt has spurred a significant shift towards alternative solutions. This has led to a growing emphasis on zirconium driers and calcium driers, often used in synergistic combinations or as primary alternatives, to achieve comparable drying performance with a more favorable environmental profile. For instance, Zirconium Driers Market formulations are increasingly preferred for their ability to promote through-drying and improve film hardness, while the Calcium Driers Market is expanding as a highly effective auxiliary drier, enhancing the performance of primary driers and improving pigment wetting.

Key players in the Metal Drier Market are heavily invested in developing new drier technologies specifically tailored for the paints and coatings industry. This includes research into low-VOC (Volatile Organic Compound) and lead-free drier packages that meet stringent environmental standards like REACH in Europe and similar regulations globally. The segment's dominance is further solidified by the continuous innovation in coating technologies, such as advancements in high-solids, water-based, and UV-curable systems, each requiring specific drier chemistries to optimize performance. Despite the challenges posed by regulatory pressure and the need for reformulation, the paints and coatings application segment is expected to maintain its leading position, driven by ongoing construction activities, industrial expansion, and the constant demand for durable and aesthetically pleasing surface finishes.

The Metal Drier Market operates under a complex interplay of demand-side drivers and supply-side constraints, necessitating strategic navigation for sustained growth. One primary driver is the robust expansion of downstream industries, notably the global Paints & Coatings Market, which itself is projected to exceed USD 200 billion by 2028 with a CAGR of around 4-5%. This growth translates directly into a higher demand for metal driers as essential additives for various coating applications, from architectural finishes to industrial protective coatings. Similarly, the burgeoning Printing Inks Market, driven by packaging and digital printing trends, requires efficient driers to ensure rapid setting times and print quality, contributing significantly to market demand. The increasing use of high-performance coatings in the automotive and aerospace industries, often demanding accelerated curing for faster production cycles and enhanced durability, further acts as a key market impetus.

Another significant driver is the increasing focus on sustainability and environmental compliance. The push for low-VOC (Volatile Organic Compound) and lead-free formulations in paints, coatings, and inks is compelling manufacturers to innovate in the Metal Drier Market. This regulatory pressure, exemplified by directives like REACH in Europe and stringent environmental standards in North America and Asia, mandates the development of safer and more eco-friendly drier solutions. This has led to the development of alternative driers based on metals like bismuth, calcium, and zinc, replacing traditional lead and often reducing the reliance on cobalt. Furthermore, the growth in the Adhesives & Sealants Market also drives demand, particularly for solvent-based systems requiring efficient drying to achieve optimal bonding strength and cure profiles.

Conversely, several significant constraints impact the market. Foremost among these is the volatility and upward trend in raw material prices. The costs of key metals such as cobalt, zirconium, manganese, and zinc, as well as the Carboxylic Acid Market components (e.g., naphthenic acid, 2-ethylhexanoic acid) used in their synthesis, can fluctuate significantly due to global supply chain disruptions, geopolitical events, and commodity market dynamics. These price instabilities directly affect the manufacturing costs of metal driers, subsequently pressuring profit margins for producers. Additionally, the aforementioned stringent environmental regulations, while driving innovation, also pose a constraint by increasing the complexity and cost of product development, testing, and compliance for manufacturers. The performance trade-offs associated with some eco-friendly alternatives (e.g., slower drying times, need for higher dosages) can also act as a constraint, requiring formulators to balance environmental goals with performance expectations.

The Metal Drier Market is characterized by a mix of established multinational corporations and specialized regional players, all vying for market share through product innovation, strategic partnerships, and regional expansion. The competitive landscape is dynamic, with a constant push towards developing more environmentally friendly and high-performance solutions.

Other notable companies contributing to the competitive landscape include DIC Corporation, Venator Materials PLC, Faith Industries Ltd., Prakash Chemicals International Pvt. Ltd., Chemelyne Specialities Pvt. Ltd., Parmanand Chemical, Akzo Nobel Egypt S.A.E., and Troy Corporation, all playing crucial roles in various segments and geographies within the Metal Drier Market.

August 2024: A leading European chemical manufacturer announced the launch of a new range of bismuth-based driers specifically designed for water-borne alkyd emulsions, offering enhanced drying performance and excellent adhesion in low-VOC formulations. This development targets the growing demand for sustainable architectural coatings.

June 2024: A major Asian supplier inaugurated an expanded production facility for zirconium and calcium driers in Southeast Asia, aiming to meet the escalating demand from the region's rapidly growing building & construction and automotive sectors. The expansion signifies a strategic move to strengthen supply chain resilience.

March 2024: A strategic partnership was forged between an American specialty chemicals company and an Indian distributor to enhance the market penetration of advanced cobalt-free drier packages across the Indian subcontinent. This collaboration focuses on providing technical support and customized solutions to local paint and ink manufacturers.

November 2023: New regulatory guidelines were implemented in parts of the European Union, further restricting the use of certain lead-containing compounds in industrial coatings, which accelerated the adoption of alternative driers and prompted significant reformulation efforts across the Metal Drier Market.

September 2023: Research findings published by a consortium of industry players highlighted the efficacy of novel manganese-based drier combinations in achieving through-drying comparable to traditional cobalt driers, particularly in solvent-based alkyd systems, opening avenues for broader commercialization of these alternatives.

July 2023: An acquisition was announced involving a specialized drier manufacturer by a larger chemicals conglomerate, aimed at integrating their complementary product portfolios and leveraging combined R&D capabilities to innovate in eco-friendly drier technologies.

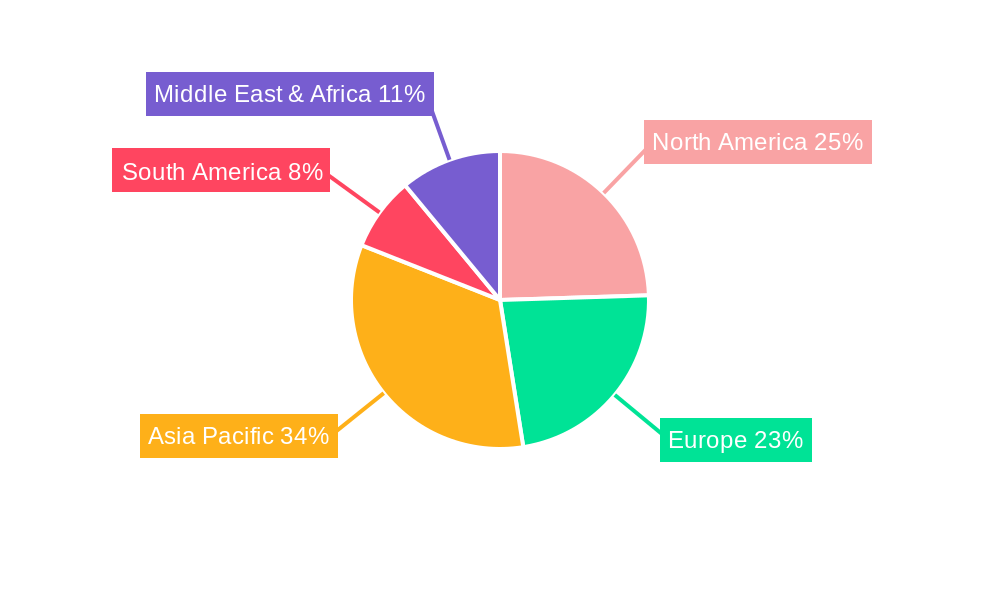

The global Metal Drier Market exhibits distinct dynamics across various geographical regions, shaped by differing industrial growth rates, regulatory environments, and raw material availability. While specific regional CAGRs are not provided, an analysis of key demand drivers and industrial output allows for an informed breakdown.

Asia Pacific is recognized as the largest and fastest-growing market for metal driers. Countries like China, India, Japan, South Korea, and the ASEAN nations are experiencing robust industrialization, rapid urbanization, and significant investments in infrastructure and manufacturing sectors. This fuels substantial demand for paints, coatings, printing inks, and adhesives in the building & construction, automotive, and packaging industries. The primary demand driver in this region is the sheer volume of production and consumption, coupled with increasing disposable incomes leading to higher per capita usage of coated goods. While still transitioning, there's a growing awareness and adoption of lead-free and low-VOC driers.

Europe represents a mature yet stable market. Driven by stringent environmental regulations such as REACH, this region has been at the forefront of adopting eco-friendly and sustainable drier solutions. The demand here is primarily from the automotive, industrial coatings, and wood & furniture sectors, with a strong emphasis on high-performance, compliant formulations. Innovation in non-cobalt and lead-free driers is a key characteristic of the European market, which sees a steady but not explosive growth due to its established industrial base.

North America also constitutes a significant and mature market. Similar to Europe, it is characterized by well-established manufacturing industries and a strong regulatory framework promoting environmentally conscious products. The demand for metal driers in North America is driven by the construction sector, automotive re-finishes, and industrial applications, with a consistent focus on product performance and compliance with VOC emission standards. The market here experiences steady growth, bolstered by continuous innovation and adoption of advanced drier technologies.

Middle East & Africa (MEA) and South America are emerging markets demonstrating promising growth potential. In MEA, infrastructure development, particularly in the GCC countries, and industrial expansion are key demand drivers. South America benefits from growing construction activities and manufacturing output, especially in countries like Brazil and Argentina. These regions are increasingly adopting modern coating technologies, leading to a rising demand for metal driers, though they may still have a higher reliance on conventional drier types compared to Europe or North America, gradually transitioning as regulations become stricter.

The Metal Drier Market, being a specialized segment of the chemical industry, is significantly influenced by global trade flows, export dynamics, and evolving tariff structures. Major trade corridors for metal driers primarily connect regions with high manufacturing capabilities (e.g., China, Germany, USA) to regions with robust end-use industries (e.g., India, Southeast Asia, Brazil). Leading exporting nations typically include Germany, China, the United States, and certain European countries that possess advanced chemical production infrastructures and readily available raw materials. Conversely, leading importing nations are often those with burgeoning construction and automotive sectors, such as India, various ASEAN members, and parts of South America, which may not have sufficient domestic production capacity.

Trade flows for metal driers are often intra-regional within established economic blocs like the EU, facilitating smoother cross-border movement. However, inter-continental trade is also substantial, driven by specialized product requirements and the global supply chain dynamics of large chemical conglomerates. Non-tariff barriers, such as stringent regulatory approvals (e.g., REACH compliance in Europe) and complex customs procedures, can significantly impact trade volumes and increase lead times. These barriers necessitate that exporters ensure their products meet the specific health, safety, and environmental standards of importing countries, often requiring considerable investment in testing and documentation.

Recent trade policy impacts, such as tariffs imposed during global trade disputes (e.g., between the U.S. and China), have led to increased costs for imported metal driers, potentially shifting sourcing strategies and driving some regional manufacturers to seek local alternatives. For instance, specific tariffs on chemical imports, which could range from 5% to 25% depending on the product classification and trade agreement, directly raise the landed cost of driers, putting upward pressure on prices for downstream industries. This can lead to a redistribution of trade flows, with companies prioritizing suppliers from countries not subject to punitive tariffs, or investing in regional production to circumvent trade barriers. The Metal Drier Market is therefore highly sensitive to geopolitical tensions and multilateral trade agreements, with any changes having ripple effects on supply chain efficiency and product pricing.

The pricing dynamics in the Metal Drier Market are a complex interplay of raw material costs, manufacturing efficiencies, competitive intensity, and regulatory compliance. Average Selling Price (ASP) trends for metal driers tend to be relatively stable for established chemistries but can see upward pressure for innovative, eco-friendly formulations that require significant R&D investment. For example, lead-free and cobalt-free alternatives, while commanding a premium, face continuous pricing scrutiny as their production volumes increase and formulation efficiencies improve.

Margin structures across the value chain are generally under pressure. Manufacturers face increasing costs for key metallic raw materials such as cobalt, zirconium, manganese, and calcium, whose prices are subject to global commodity market fluctuations, geopolitical factors, and mining supply dynamics. The Carboxylic Acid Market also exerts influence, as organic acids used in drier synthesis (e.g., 2-ethylhexanoic acid, naphthenic acid) are petroleum-derived or bio-based chemicals, subject to their own supply-demand and energy cost volatility. This dual pressure from both metal and organic raw materials can significantly squeeze profit margins, particularly for producers of high-volume, standard drier types where differentiation is minimal.

Key cost levers primarily include the procurement cost of metals and organic acids, energy consumption during synthesis, and the expenses associated with meeting stringent environmental regulations. The development and continuous reformulation of products to achieve low-VOC, lead-free, and non-toxic profiles entail substantial R&D expenditure, which must be amortized into product pricing. This often creates a tiered pricing structure, where conventional driers are commodity-like with thin margins, while specialized, high-performance, and compliant driers command healthier premiums.

Competitive intensity, stemming from a fragmented market with numerous regional and global players, also affects pricing power. Manufacturers differentiate themselves through product performance, technical support, supply chain reliability, and the breadth of their portfolio. In highly competitive segments, price leadership can become a key strategy, potentially leading to price erosion. Furthermore, the bargaining power of large downstream customers (major paint, ink, and coatings manufacturers) can exert downward pressure on drier prices. Overall, while innovation in sustainable solutions offers opportunities for value-added pricing, the Metal Drier Market is expected to navigate persistent margin pressure due to volatile input costs and the ongoing drive for regulatory compliance.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 1.3%.

Key companies in the market include Borchers GmbH, Arkema S.A., Ege Kimya San. ve Tic. A.Ş., Patcham FZC, The Shepherd Chemical Company, Valtris Specialty Chemicals, DIC Corporation, Venator Materials PLC, OMG Americas Inc., Faith Industries Ltd., Prakash Chemicals International Pvt. Ltd., Chemelyne Specialities Pvt. Ltd., Parmanand Chemical, Akzo Nobel Egypt S.A.E., Troy Corporation, Others.

The market segments include Type, Function, Solvent, Application, Sales Channel, End User Industry.

The market size is estimated to be USD 1841.8 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Metal Drier," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Metal Drier, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.