1. What is the projected Compound Annual Growth Rate (CAGR) of the Lower GI Series?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Lower GI Series

Lower GI SeriesLower GI Series by Type (/> Double-Contrast, Single-Contrast), by Application (/> Hospital, Clinic, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

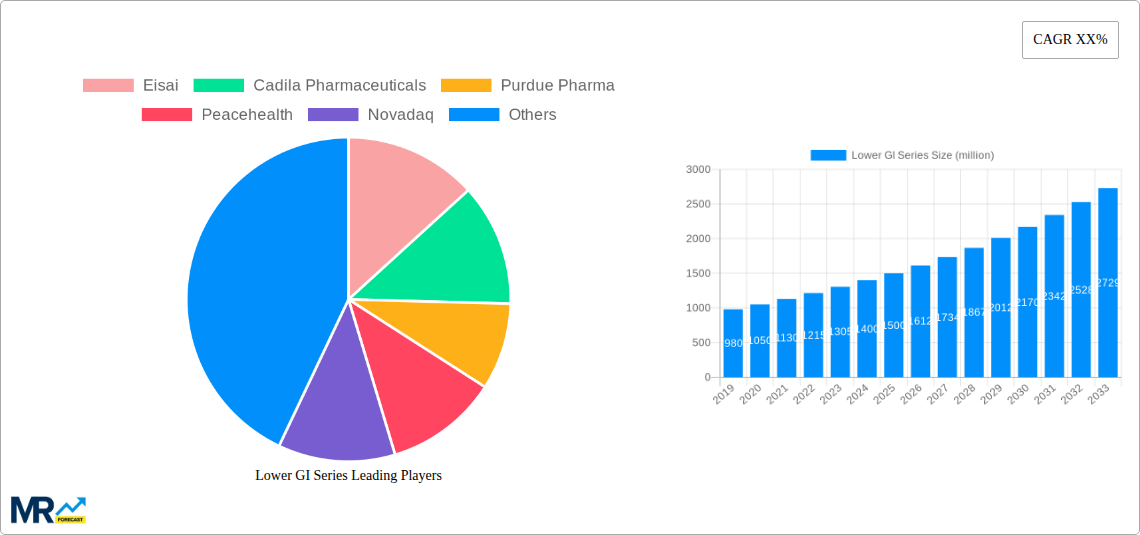

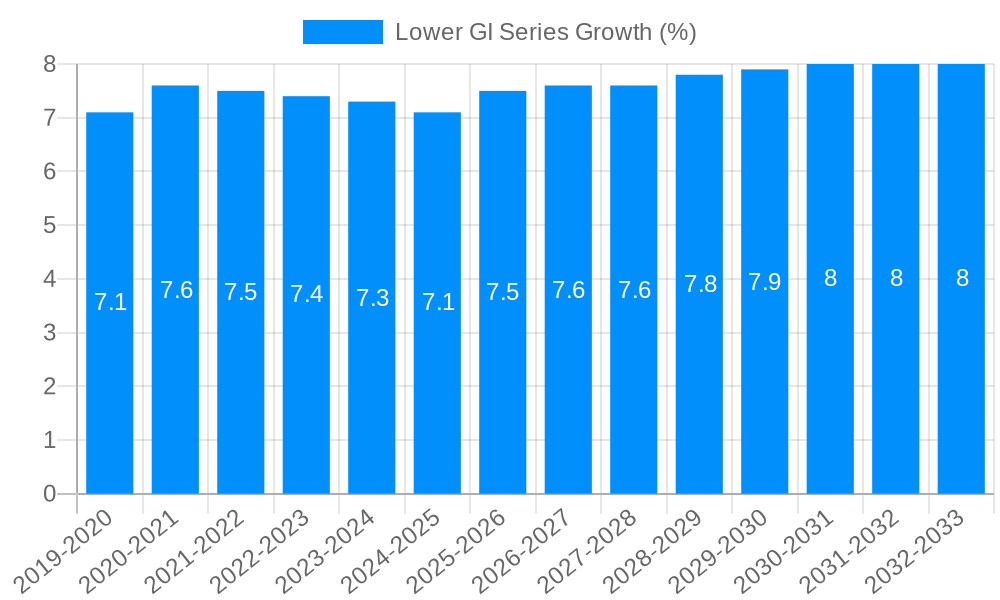

The Lower GI Series market is poised for significant expansion, projected to reach a substantial market size of approximately $1,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of around 8.5% anticipated over the forecast period extending to 2033. This growth is primarily propelled by an increasing prevalence of gastrointestinal disorders globally, including inflammatory bowel diseases, colorectal cancer, and other functional bowel ailments. Enhanced diagnostic capabilities and a growing awareness among healthcare providers and patients regarding the importance of early detection and accurate diagnosis are also key drivers. The market is witnessing a steady demand for both Double-Contrast and Single-Contrast barium studies, with hospitals and specialized clinics being the dominant application segments due to their advanced infrastructure and patient referral networks. Emerging economies, particularly in the Asia Pacific region, are expected to contribute significantly to this growth trajectory, driven by improving healthcare access and rising disposable incomes.

The market landscape for the Lower GI Series is characterized by a dynamic interplay of technological advancements and strategic collaborations among key industry players. Companies like AstraZeneca, Cadila Pharmaceuticals, and Eisai are at the forefront, investing in research and development to refine imaging techniques and contrast agents, thereby improving diagnostic accuracy and patient comfort. However, the market faces certain restraints, including the increasing adoption of alternative diagnostic modalities such as colonoscopies and advanced imaging techniques like MRI and CT scans, which offer direct visualization and biopsy capabilities. Furthermore, the cost-effectiveness of traditional barium studies in certain healthcare settings and reimbursement policies can influence market dynamics. Nonetheless, the inherent advantages of Lower GI Series, such as its relative affordability and widespread availability, ensure its continued relevance, especially in resource-constrained environments. Strategic initiatives like product innovation and market penetration in underserved regions will be crucial for sustained market leadership.

The global Lower GI Series market, a crucial diagnostic tool for evaluating the large intestine and rectum, is poised for significant expansion, projecting a market value of $5.2 million by 2033. This growth is underpinned by a confluence of factors, including an aging global population susceptible to colorectal diseases, increasing awareness and early detection initiatives, and continuous advancements in imaging technologies. The study period, spanning from 2019 to 2033, with a base year of 2025 and an estimated year also of 2025, highlights a dynamic market trajectory. The historical period of 2019-2024 laid the groundwork for this anticipated surge, with initial market values demonstrating a steady upward trend. The forecast period, from 2025 to 2033, is expected to witness an accelerated growth rate, driven by innovations and an expanding patient base seeking comprehensive gastrointestinal diagnostics. The market is segmented by type, including Double-Contrast and Single-Contrast procedures, and by application, encompassing hospitals, clinics, and other healthcare settings. Each segment plays a vital role in shaping the overall market landscape, with hospitals historically leading in adoption due to the availability of advanced infrastructure and specialized personnel. However, the increasing establishment of specialized diagnostic clinics and the growing trend of outpatient procedures are also contributing to a diversified application landscape. Industry developments, such as enhanced image resolution, reduced radiation exposure, and improved patient comfort during procedures, are continuously refining the efficacy and appeal of lower GI series examinations, further solidifying its position as an indispensable diagnostic modality in modern healthcare. The market's evolution is also influenced by evolving healthcare policies and reimbursement structures, which can either stimulate or temper its growth. Nonetheless, the intrinsic diagnostic value of lower GI series in detecting conditions like polyps, diverticulitis, inflammatory bowel disease, and cancer ensures its sustained relevance and demand.

The burgeoning demand for lower GI series is primarily propelled by an escalating global prevalence of gastrointestinal disorders, most notably colorectal cancer and inflammatory bowel diseases. As the world’s population ages, the incidence of these conditions naturally rises, creating a substantial and consistent need for accurate diagnostic tools. Furthermore, there's a marked increase in public health campaigns and physician advocacy for early detection and screening of colorectal cancers. This heightened awareness translates directly into higher patient volumes presenting for lower GI series examinations, often at earlier, more treatable stages. Technological advancements also play a pivotal role. Innovations in contrast media have led to improved visualization of mucosal details, enhancing diagnostic accuracy. Similarly, advancements in X-ray detector technology and imaging software are leading to higher resolution images, shorter examination times, and reduced radiation doses for patients, making the procedure safer and more comfortable. The growing emphasis on personalized medicine and precision diagnostics further fuels the need for detailed anatomical and pathological insights provided by lower GI series. As healthcare systems globally strive for better patient outcomes and cost-effectiveness, the role of minimally invasive, high-yield diagnostic procedures like lower GI series becomes increasingly prominent. The expanding healthcare infrastructure in emerging economies, coupled with a rising disposable income, is also contributing to increased access to and utilization of these diagnostic services.

Despite the promising growth trajectory, the lower GI series market faces several significant challenges and restraints that could impede its full potential. A primary concern is the increasing competition from alternative diagnostic modalities, most notably colonoscopy. Colonoscopy offers direct visualization and the ability to perform biopsies and polyp removal during the same procedure, making it a preferred choice for many clinicians and patients, especially when considering its therapeutic capabilities in addition to diagnostics. The perceived invasiveness and patient discomfort associated with barium enemas, a common component of lower GI series, can also act as a deterrent, leading some patients to opt for less uncomfortable alternatives, even if less definitive for certain conditions. Furthermore, the cost of advanced imaging equipment and the specialized training required for radiologists and technicians to perform and interpret lower GI series can represent a substantial barrier, particularly for smaller healthcare facilities or those in resource-limited regions. Reimbursement policies and coverage limitations for lower GI series in certain healthcare systems can also influence its adoption and utilization rates. Stringent regulatory hurdles associated with the approval of new contrast agents and imaging technologies can slow down the introduction of innovative solutions to the market. Lastly, the potential for complications, although rare, such as barium impaction or perforation, can create apprehension among both patients and healthcare providers, leading to a preference for safer alternatives.

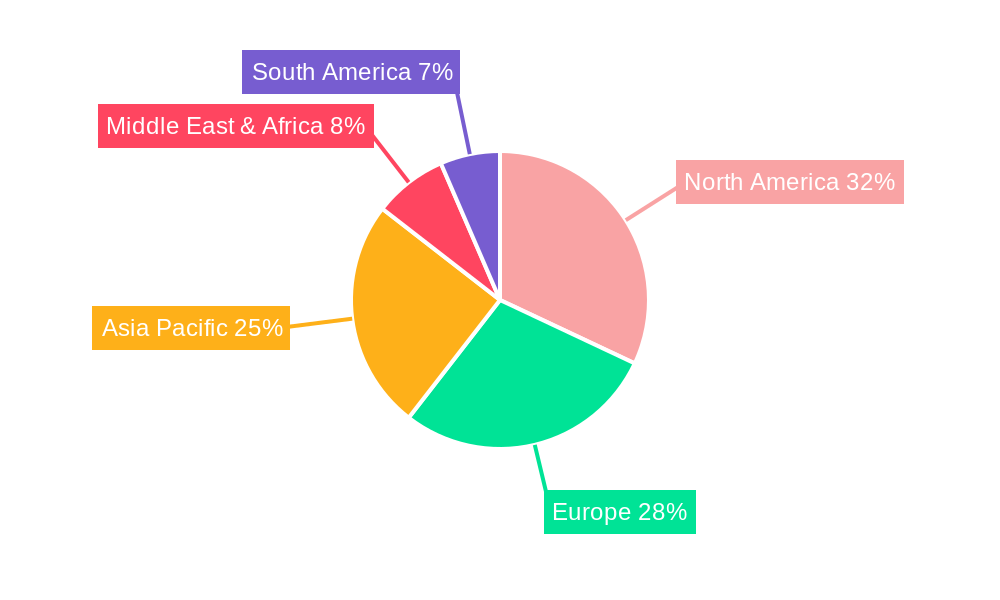

The global Lower GI Series market is projected to be dominated by North America and Europe due to their well-established healthcare infrastructures, high prevalence of gastrointestinal diseases, and a strong emphasis on early cancer detection. Within these regions, the Hospital segment is anticipated to hold the largest market share. Hospitals, equipped with advanced imaging technologies and specialized medical personnel, are the primary centers for complex diagnostic procedures, including lower GI series. The increasing incidence of colorectal cancer and other gastrointestinal disorders in these developed nations further bolsters the demand for hospital-based diagnostic services. The Double-Contrast type is also expected to lead the market. This technique, which involves instilling both barium sulfate and air into the colon, provides superior visualization of the mucosal lining, allowing for the detection of subtle abnormalities and small polyps. The enhanced diagnostic accuracy offered by double-contrast procedures makes it the preferred method for comprehensive evaluations of the colon and rectum.

Key Regions/Countries Dominating the Market:

Key Segments Dominating the Market:

The continued investment in upgrading hospital facilities and the increasing adoption of advanced imaging technologies in these regions will further solidify their dominance in the coming years. The consistent rise in the incidence of colorectal cancers and other gastrointestinal ailments will continue to drive demand for these diagnostic procedures.

Several key factors are acting as potent growth catalysts for the Lower GI Series industry. The persistent rise in the incidence of colorectal cancer globally, coupled with an increasing emphasis on early detection and screening programs, is a fundamental driver. Advances in imaging technology, leading to improved resolution, reduced radiation exposure, and enhanced patient comfort, are making these procedures more accessible and appealing. The development of novel contrast agents that offer better mucosal coating and visualization further amplifies diagnostic accuracy. Furthermore, the expanding healthcare infrastructure in emerging economies, alongside a growing middle class with increased healthcare spending capacity, is opening up new markets and driving demand.

This comprehensive report delves into the intricate dynamics of the global Lower GI Series market, providing an in-depth analysis of its current status and future projections. It meticulously examines market trends, identifies key driving forces, and outlines potential challenges and restraints. The report also highlights dominant regions and segments, offering valuable insights into market leadership and growth potential. Furthermore, it showcases the leading industry players and chronicles significant developments that are shaping the sector. This detailed coverage ensures stakeholders have a thorough understanding of the market landscape, enabling informed strategic decision-making for growth and investment in the evolving field of gastrointestinal diagnostics.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Eisai, Cadila Pharmaceuticals, Purdue Pharma, Peacehealth, Novadaq, Astrazeneca, Ironwood Pharmaceuticals.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Lower GI Series," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Lower GI Series, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.