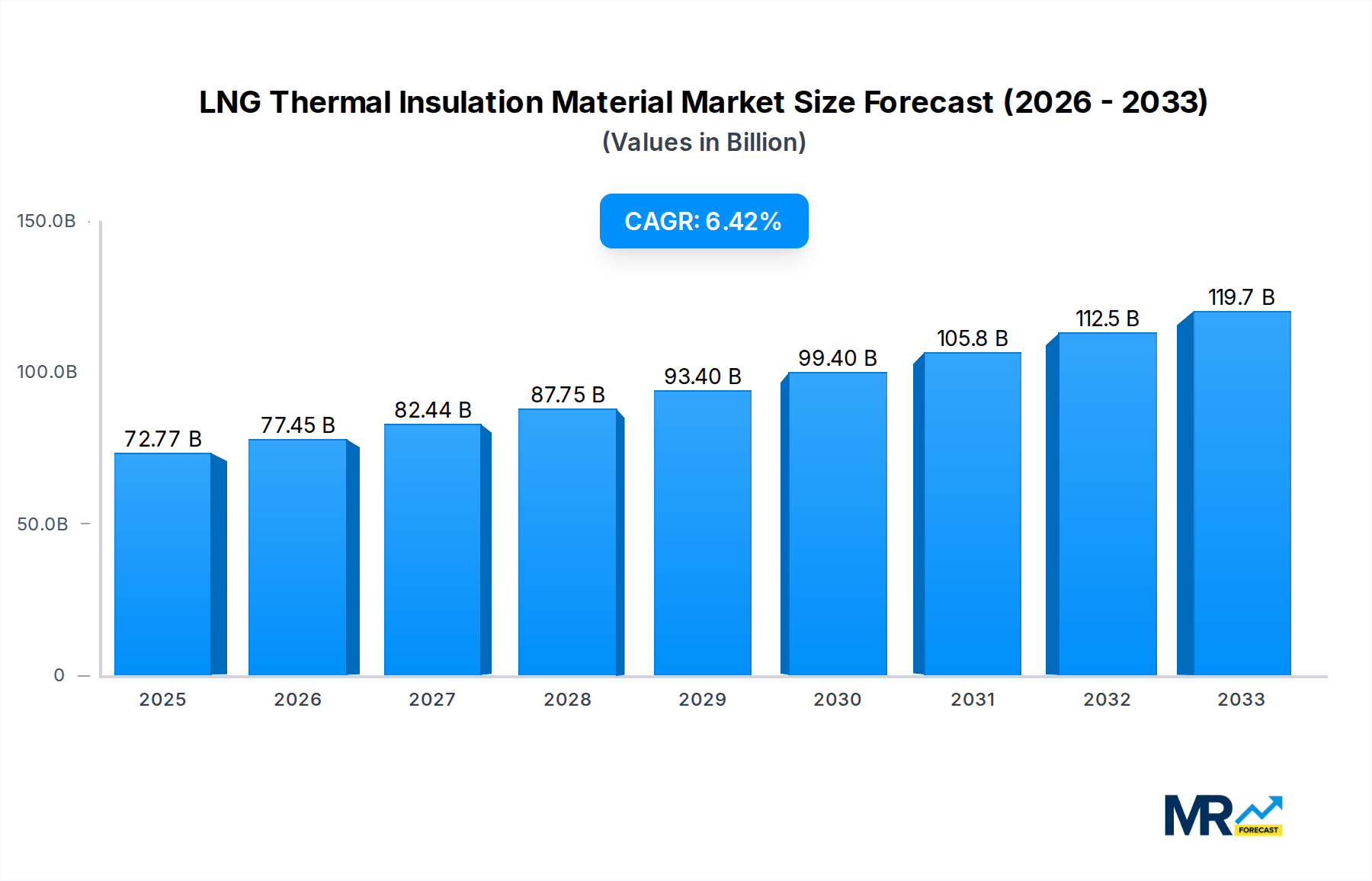

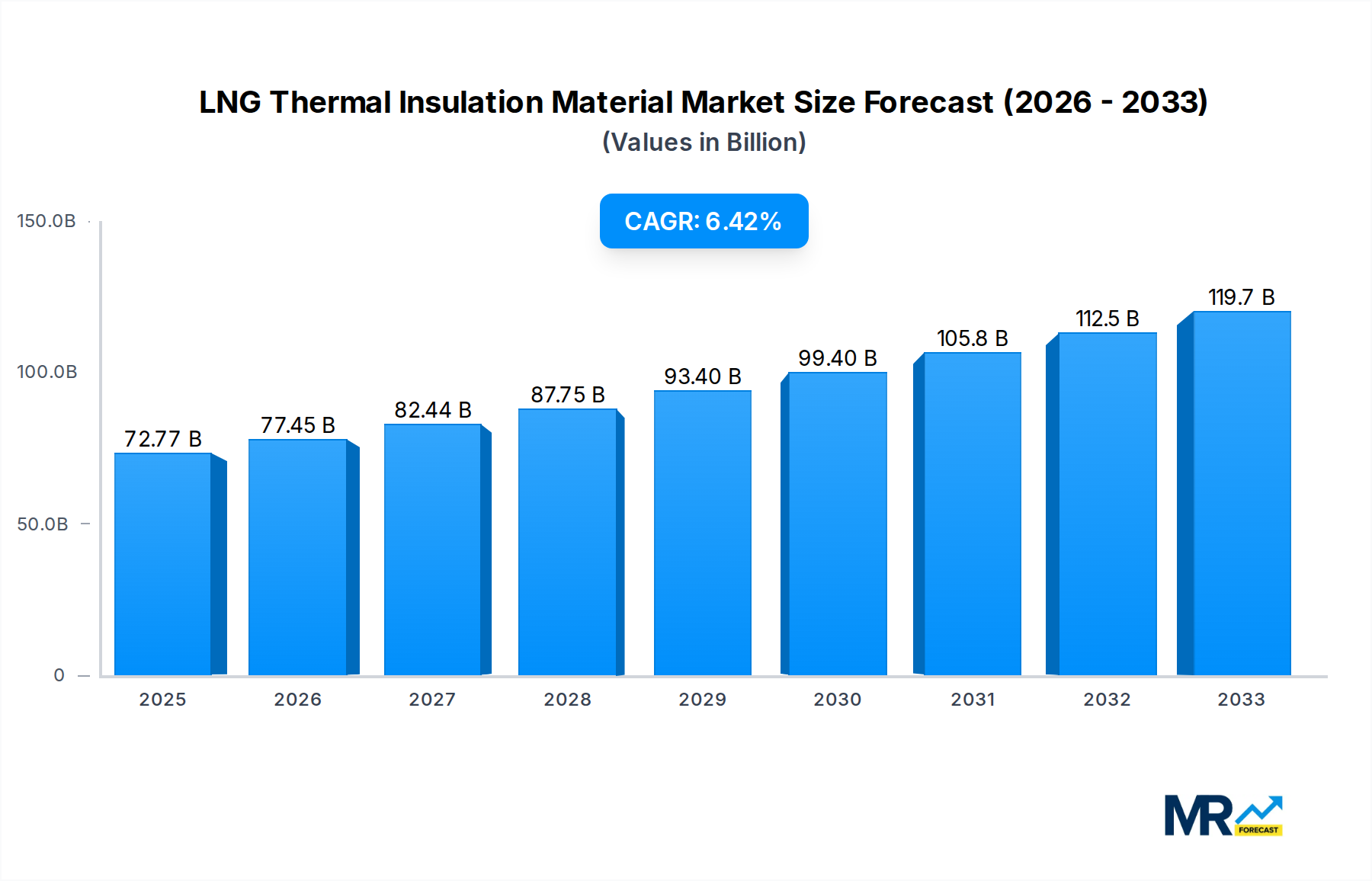

1. What is the projected Compound Annual Growth Rate (CAGR) of the LNG Thermal Insulation Material?

The projected CAGR is approximately 6.4%.

LNG Thermal Insulation Material

LNG Thermal Insulation MaterialLNG Thermal Insulation Material by Application (Pipeline System, Oil Storage Tank, Liquified Natural Gas, Others, World LNG Thermal Insulation Material Production ), by Type (Porous Glass, Polystyrene, Glass Fiber, Perlite, Others, World LNG Thermal Insulation Material Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global LNG thermal insulation material market is poised for robust growth, projected to reach an estimated $72.77 billion by 2025. This expansion is driven by the escalating demand for Liquefied Natural Gas (LNG) as a cleaner alternative to traditional fossil fuels, particularly in power generation and transportation sectors. The increasing investment in LNG infrastructure, including liquefaction plants, regasification terminals, and extensive pipeline networks, directly fuels the need for high-performance thermal insulation materials. These materials are critical for maintaining the cryogenic temperatures required for LNG storage and transportation, thereby minimizing boil-off losses and ensuring operational efficiency and safety. Furthermore, stringent environmental regulations and the global push towards decarbonization are accelerating the adoption of LNG, consequently boosting the market for specialized insulation solutions.

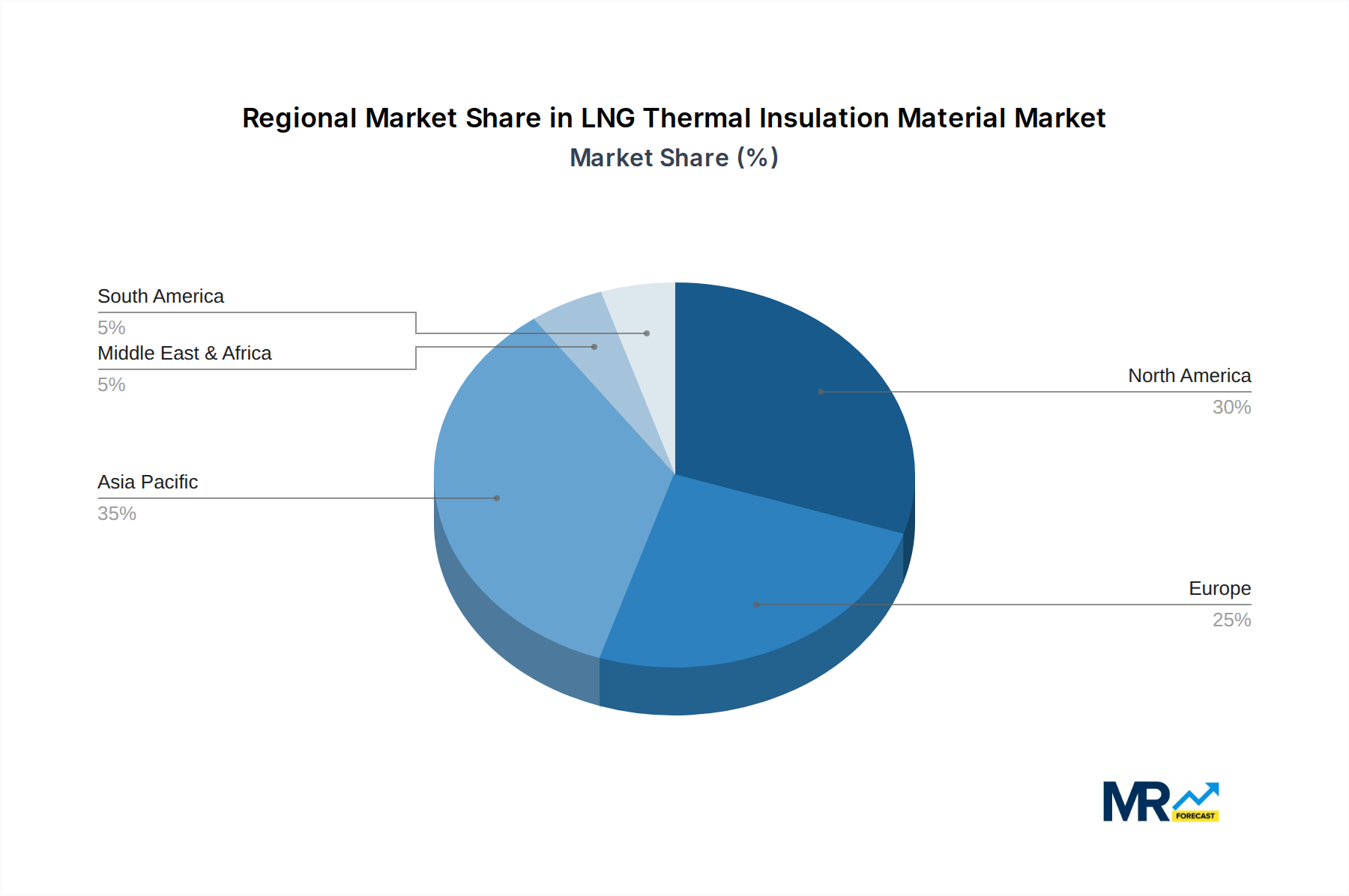

The market segmentation reveals diverse applications and material types contributing to its dynamism. Applications such as pipeline systems, oil storage tanks, and Liquefied Natural Gas (LNG) facilities are primary consumers of these insulation materials. The "Others" category in applications likely encompasses specialized industrial uses. On the materials front, Porous Glass, Polystyrene, Glass Fiber, and Perlite are key types, each offering distinct thermal performance characteristics, cost-effectiveness, and suitability for various operating conditions. Key players like Johns Manville, Saint-Gobain, and BASF are at the forefront, innovating and expanding their product portfolios to meet evolving industry demands. The projected Compound Annual Growth Rate (CAGR) of 6.4% from 2025 to 2033 underscores the market's strong upward trajectory, indicating sustained demand and opportunities for market participants across the globe, with significant activity expected in Asia Pacific and North America due to growing energy needs and infrastructure development.

This comprehensive report provides an in-depth analysis of the global LNG thermal insulation material market, spanning the historical period of 2019-2024, with a base year of 2025 and a forecast extending to 2033. Leveraging extensive research and industry data, this report offers invaluable insights for stakeholders seeking to understand the dynamic landscape of this critical sector. The estimated market size for LNG thermal insulation materials is projected to reach over $20 billion by 2025, with significant growth anticipated in the coming years.

XXX The global LNG thermal insulation material market is experiencing a profound transformation driven by an escalating demand for efficient and reliable insulation solutions across the entire LNG value chain. A pivotal trend is the increasing adoption of advanced materials that offer superior thermal performance at cryogenic temperatures, thereby minimizing boil-off gas and ensuring the integrity of LNG storage and transportation. The Liquified Natural Gas segment, encompassing storage tanks, liquefaction plants, and regasification terminals, is at the forefront of this material innovation. Companies are increasingly investing in research and development to create materials with lower thermal conductivity, enhanced durability, and improved fire resistance. The growing emphasis on safety and environmental regulations is further propelling the demand for high-performance insulation, making it a non-negotiable aspect of LNG infrastructure projects. Looking ahead, the market will likely witness a surge in demand for bespoke insulation solutions tailored to specific project requirements and geographical conditions. The Oil Storage Tank segment, while not exclusively focused on LNG, is also seeing a shift towards more sophisticated thermal insulation to optimize energy efficiency, indirectly benefiting the broader understanding and application of cryogenic insulation technologies. The Pipeline System application, crucial for the transportation of LNG from production sites to end-users, is also experiencing innovation in insulation materials, particularly for offshore and long-distance terrestrial pipelines. The overarching trend is a move away from conventional, lower-performance materials towards cutting-edge composites and aerogels, which offer significant advantages in weight reduction and thermal efficiency. The market is also influenced by the evolving global energy landscape, with a growing reliance on natural gas as a cleaner alternative to fossil fuels, which directly translates into increased investment in LNG infrastructure and, consequently, the demand for its essential components like thermal insulation. The World LNG Thermal Insulation Material Production is not only expanding in volume but also in the sophistication of its output, reflecting a mature market that is continuously seeking improvements.

The LNG thermal insulation material market is experiencing robust growth, propelled by a confluence of powerful factors. The most significant driver is the burgeoning global demand for Liquefied Natural Gas (LNG). As nations worldwide increasingly pivot towards cleaner energy sources to combat climate change and enhance energy security, the role of natural gas, and by extension LNG, becomes paramount. This surge in LNG consumption necessitates the expansion of liquefaction plants, import/export terminals, and extensive transportation networks, all of which rely heavily on advanced thermal insulation to maintain cryogenic temperatures and minimize gas loss. Furthermore, stringent government regulations and international standards emphasizing energy efficiency and environmental protection are compelling players across the LNG value chain to invest in high-performance insulation materials. These regulations mandate reduced boil-off rates, thereby translating into significant economic savings and a minimized environmental footprint. Technological advancements in insulation materials themselves are also playing a crucial role. Innovations such as aerogels, advanced composite materials, and enhanced vacuum insulation systems offer superior thermal performance, lighter weight, and greater durability compared to traditional materials. These advancements make them increasingly attractive for demanding LNG applications. The increasing investment in floating liquefaction, storage, and regasification units (FLNG/FSRU) for offshore operations presents another significant growth catalyst, as these complex structures require specialized, space-efficient, and robust insulation solutions. The World LNG Thermal Insulation Material Production is therefore under pressure to innovate and scale up to meet these expanding needs. The interplay of these drivers creates a dynamic and promising market environment for LNG thermal insulation materials.

Despite the promising growth trajectory, the LNG thermal insulation material market faces several significant challenges and restraints that could impede its full potential. A primary concern is the high initial cost associated with advanced, high-performance insulation materials. While these materials offer long-term benefits in terms of energy savings and reduced boil-off, their upfront price can be a deterrent for some projects, particularly in price-sensitive markets or for smaller-scale operations. The complex and specialized nature of cryogenic insulation installation also presents a challenge. It requires highly skilled labor and adherence to rigorous quality control standards to ensure optimal performance and safety. Shortages of skilled installers can lead to project delays and cost overruns. Moreover, the development and scaling up of novel insulation technologies, while promising, can be hindered by lengthy research and development cycles, significant capital investment requirements, and the need for extensive testing and certification to gain industry acceptance. Supply chain disruptions, exacerbated by global geopolitical events and economic volatility, can also impact the availability and pricing of raw materials essential for the production of these specialized insulation materials, potentially leading to production bottlenecks and increased costs. The inherent complexity of LNG infrastructure, encompassing vast storage tanks and extensive pipeline networks, means that retrofitting existing facilities with advanced insulation can be a technically challenging and economically unviable proposition for some older plants. The World LNG Thermal Insulation Material Production must constantly navigate these complexities.

The global LNG thermal insulation material market is characterized by a dynamic interplay of dominant regions and segments, with several key players poised to capture significant market share. In terms of regional dominance, Asia-Pacific is expected to emerge as a powerhouse, driven by robust growth in LNG demand from countries like China, India, and Southeast Asian nations. These regions are heavily investing in new LNG import terminals, regasification facilities, and associated infrastructure to meet their expanding energy needs, creating a substantial demand for thermal insulation materials. The ongoing expansion of liquefaction capacity in countries like Australia and potential future developments in other Asian nations further solidify this region's leading position. Europe also represents a significant market, fueled by efforts to diversify energy sources away from traditional suppliers and a strong emphasis on energy efficiency and decarbonization. The development of new LNG import terminals and the expansion of existing ones in countries like Germany, the Netherlands, and the UK are key contributors. North America, with its substantial domestic natural gas production and growing export capabilities, also commands a considerable share of the market, particularly in the United States and Canada, driven by ongoing investments in liquefaction plants and export terminals.

Within the segments, the Liquified Natural Gas application will unequivocally dominate the market. This segment encompasses the entire LNG lifecycle, from liquefaction plants and LNG carriers to storage tanks at import/export terminals and regasification facilities. The critical need for precise temperature control and the prevention of boil-off gas loss during these processes make advanced thermal insulation an indispensable component. The sheer scale of LNG infrastructure development and expansion globally directly translates into a sustained and growing demand for insulation materials within this application.

Furthermore, the Type of material also plays a crucial role in market dominance. While various insulation types exist, Porous Glass and advanced Others, such as aerogels and specialized composite materials, are projected to see the most significant growth. Porous glass offers excellent thermal performance, non-combustibility, and resistance to moisture, making it suitable for cryogenic applications. The emergence of high-performance aerogels, with their exceptionally low thermal conductivity and lightweight properties, is revolutionizing cryogenic insulation, offering significant advantages in space-constrained applications like LNG carriers and floating facilities. The continuous innovation and development in these "Others" categories are expected to drive their market share upwards. The World LNG Thermal Insulation Material Production is therefore concentrated in regions and focused on segments that demand the highest performance and innovation.

The LNG thermal insulation material industry is experiencing robust growth fueled by several key catalysts. The accelerating global shift towards cleaner energy sources, with natural gas positioned as a crucial transitional fuel, is driving unprecedented investment in LNG infrastructure worldwide. This includes the construction of new liquefaction plants, import/export terminals, and an expanding fleet of LNG carriers, all of which require substantial quantities of high-performance thermal insulation. Furthermore, increasingly stringent environmental regulations and a heightened focus on energy efficiency are compelling operators to adopt superior insulation solutions to minimize boil-off gas and reduce operational costs. Technological advancements in insulation materials, such as the development of advanced aerogels and composite materials with superior thermal conductivity and durability, are also acting as significant growth drivers, offering innovative solutions for challenging cryogenic applications.

This report provides an exhaustive examination of the LNG thermal insulation material market, offering unparalleled depth and breadth of analysis. It delves into the intricate details of market dynamics, including historical trends from 2019-2024, current market conditions in the base year of 2025, and a comprehensive forecast spanning through 2033. The report meticulously analyzes key growth catalysts, such as the increasing global demand for LNG as a transitional fuel, stringent environmental regulations, and continuous technological innovation in insulation materials like aerogels. It also addresses the significant challenges, including the high cost of advanced materials and the need for specialized installation expertise. Detailed segment-wise and region-wise market projections are presented, highlighting the dominant applications like Liquified Natural Gas and leading geographical markets such as the Asia-Pacific. The report also offers a curated list of leading players and significant industry developments, providing stakeholders with a holistic understanding of this critical and rapidly evolving sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.4%.

Key companies in the market include Johns Manville, Saint Gobain, Cabot Corporation, Hertel, BASF, Armacell International Holding, Lydall, Dunmore Corporation, Imerys Minerals, Aspen Aerogels, Roechling Group, Jiangsu Yoke Technology, Dehe Technology Group, .

The market segments include Application, Type.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "LNG Thermal Insulation Material," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the LNG Thermal Insulation Material, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.