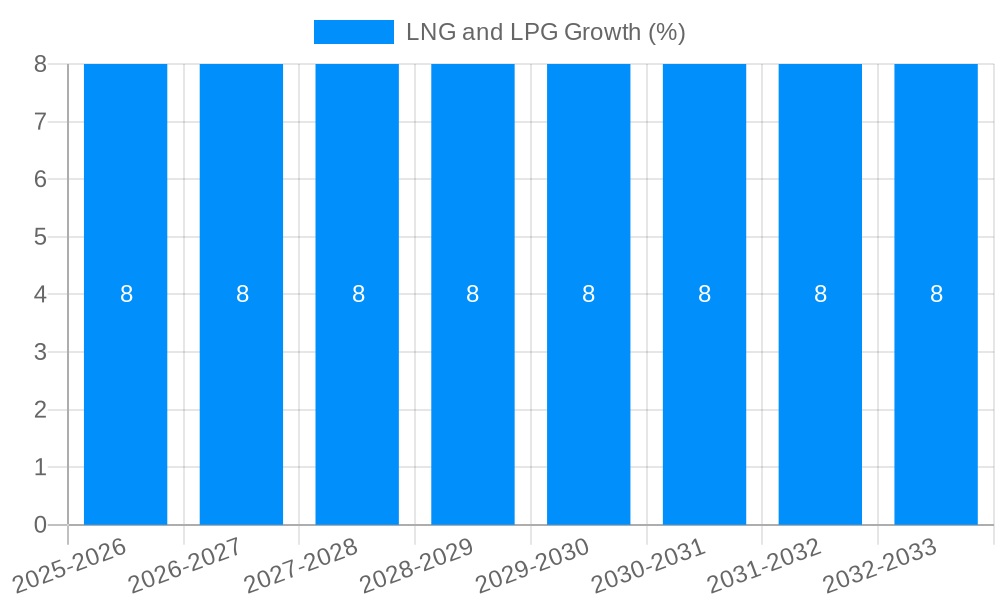

1. What is the projected Compound Annual Growth Rate (CAGR) of the LNG and LPG?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

LNG and LPG

LNG and LPGLNG and LPG by Type (Liquefied Natural Gas (LNG), Liquefied Petroleum Gas (LPG)), by Application (Industrial, Transportation, Residential Heating, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Liquefied Natural Gas (LNG) and Liquefied Petroleum Gas (LPG) market is poised for substantial growth, projected to reach an estimated $XXX billion by 2025, with a Compound Annual Growth Rate (CAGR) of XX% through 2033. This expansion is primarily driven by the increasing global demand for cleaner and more accessible energy sources, especially as countries seek to diversify their energy portfolios and reduce reliance on more polluting fossil fuels. The industrial sector, a significant consumer of both LNG and LPG for power generation, feedstock, and process heating, is a key growth engine. Additionally, the transportation sector is witnessing a surge in the adoption of LNG and LPG as viable alternatives to traditional fuels, spurred by stricter emissions regulations and advancements in vehicle technology. Residential heating also contributes to market expansion, particularly in regions with colder climates where efficient and cost-effective heating solutions are paramount.

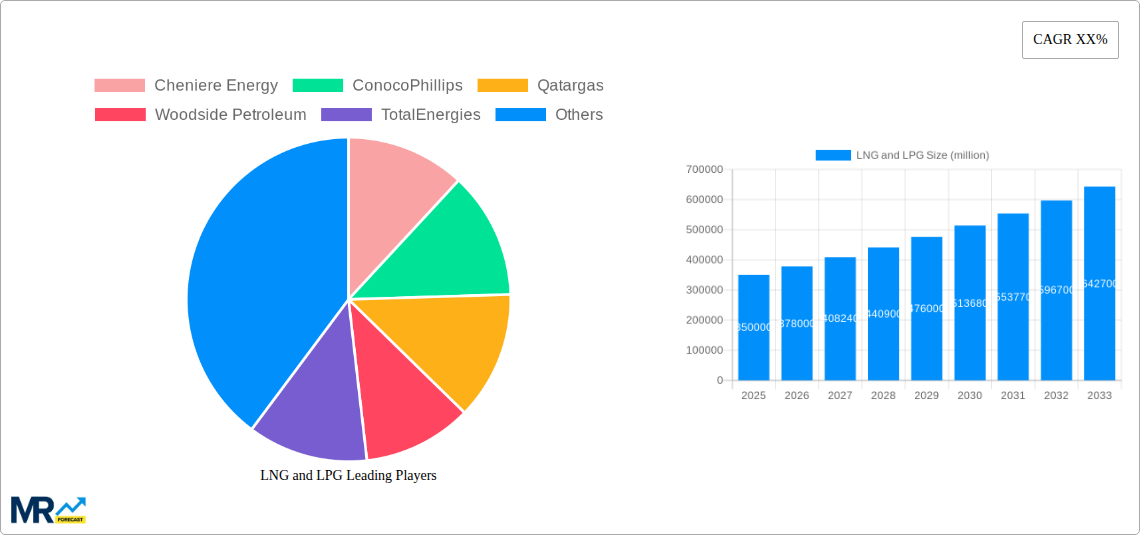

However, the market faces certain restraints that could temper its growth trajectory. Volatility in crude oil prices can impact the pricing of LNG and LPG, creating uncertainty for consumers and investors. Furthermore, the significant infrastructure requirements for liquefaction, transportation, and regasification of LNG, as well as storage and distribution networks for LPG, represent substantial capital investments and potential bottlenecks. Environmental concerns related to methane emissions during the production and transportation of natural gas, and the flammability of LPG, also present ongoing challenges that the industry must address through technological advancements and stringent safety protocols. Despite these challenges, the overarching trend towards energy transition, coupled with strategic investments by major players like Cheniere Energy, ConocoPhillips, Qatargas, Woodside Petroleum, TotalEnergies, Shell, ExxonMobil, BP, Chevron, Bharat Petroleum, and Repsol, will continue to fuel market expansion across key regions such as North America, Asia Pacific, and Europe.

This comprehensive report offers an in-depth analysis of the global Liquefied Natural Gas (LNG) and Liquefied Petroleum Gas (LPG) markets, providing critical insights for stakeholders navigating this dynamic sector. The study encompasses a significant timeframe, covering the historical period from 2019 to 2024, with a base year set in 2025 and extending through an extensive forecast period from 2025 to 2033. This allows for a robust understanding of past trends, current market dynamics, and future trajectory. The report delves into the intricate workings of both LNG and LPG, examining their distinct characteristics, applications, and the overarching industry developments shaping their global footprint. With projected market values in the million unit, this report provides a quantifiable perspective on the economic significance and growth potential of these vital energy sources.

XXX The global LNG and LPG markets are poised for substantial expansion, driven by a confluence of factors including evolving energy demands, environmental considerations, and technological advancements. Over the study period (2019-2033), a discernible upward trend in both LNG and LPG consumption is projected. The base year of 2025 serves as a crucial reference point for understanding the current market equilibrium, from which the forecast period (2025-2033) anticipates significant shifts and growth. A key trend observed is the increasing diversification of supply sources for LNG, moving beyond traditional exporters to unlock new reserves and infrastructure development, particularly in regions with burgeoning demand. Similarly, LPG, known for its versatility and relative affordability, continues to solidify its position as a crucial fuel for a wide array of applications.

The historical period (2019-2024) has witnessed volatility, influenced by geopolitical events, supply disruptions, and fluctuating energy prices. However, the overarching narrative has been one of resilience and adaptation. The increasing focus on decarbonization has spurred innovation in both LNG and LPG. For LNG, this translates to investments in more efficient liquefaction and regasification terminals, as well as the exploration of lower-carbon LNG options. LPG, already considered a cleaner alternative to traditional fossil fuels in many applications, is seeing its role amplified in residential heating and cooking in developing economies, while also finding new applications in industrial processes and as a component in autogas. The estimated year of 2025 highlights a market that is recovering from recent global challenges and is on the cusp of accelerated growth, fueled by a renewed emphasis on energy security and accessibility. The interplay between these two liquefied gases, their respective market shares, and their synergistic or competitive roles across various applications will be a central theme explored in this report. Understanding these evolving trends is paramount for strategic decision-making in the energy sector.

The ascent of the LNG and LPG markets is underpinned by a robust set of driving forces that are reshaping the global energy landscape. Foremost among these is the ever-growing global energy demand, particularly in emerging economies, which necessitates a reliable and accessible supply of energy. Both LNG and LPG, with their relatively cleaner burning profiles compared to coal and heavy fuel oil, are increasingly viewed as critical transitional fuels in the journey towards a low-carbon future. The push for improved air quality and adherence to stringent environmental regulations worldwide is a significant propellant, encouraging the adoption of these cleaner alternatives in sectors like transportation and industrial processes. Furthermore, the strategic importance of energy security has been amplified, leading nations to diversify their energy portfolios and secure stable supply chains. LNG, in particular, offers a highly flexible solution for energy importers, allowing for rapid deployment and adaptation to changing geopolitical dynamics. The development of extensive liquefaction and regasification infrastructure, coupled with advancements in transportation and storage technologies, has made LNG more accessible and economically viable than ever before. Similarly, the widespread availability and cost-effectiveness of LPG continue to drive its demand, especially in regions where access to natural gas pipelines is limited. The growing awareness of LPG's domestic and industrial applications, from cooking and heating to automotive fuel and feedstock for the petrochemical industry, further fuels its market expansion.

Despite the promising growth trajectory, the LNG and LPG markets are not without their inherent challenges and restraints that can impede their full potential. A primary concern for LNG is the significant capital investment required for the development of liquefaction plants, regasification terminals, and specialized shipping infrastructure. These projects are often subject to lengthy approval processes and can face substantial cost overruns, leading to delays and increased project risk. Furthermore, the global LNG market remains susceptible to price volatility, influenced by fluctuating crude oil prices, geopolitical tensions, and the delicate balance of supply and demand. Extreme weather events can also disrupt production and transportation, leading to temporary supply shortages and price spikes. For LPG, while generally more accessible, concerns regarding safety in storage and handling persist. Leaks and improper usage can pose significant fire and explosion hazards, necessitating strict adherence to safety regulations and ongoing public awareness campaigns. The availability and affordability of alternative energy sources, such as renewable energy technologies (solar, wind), also present a competitive restraint, particularly in developed markets with strong policy support for these cleaner alternatives. Moreover, the development of extensive natural gas pipeline networks in certain regions can diminish the demand for both LNG and LPG for some applications. The capital intensity of infrastructure development, coupled with regulatory hurdles and environmental concerns associated with the fossil fuel industry, collectively pose significant restraints that market players must adeptly navigate.

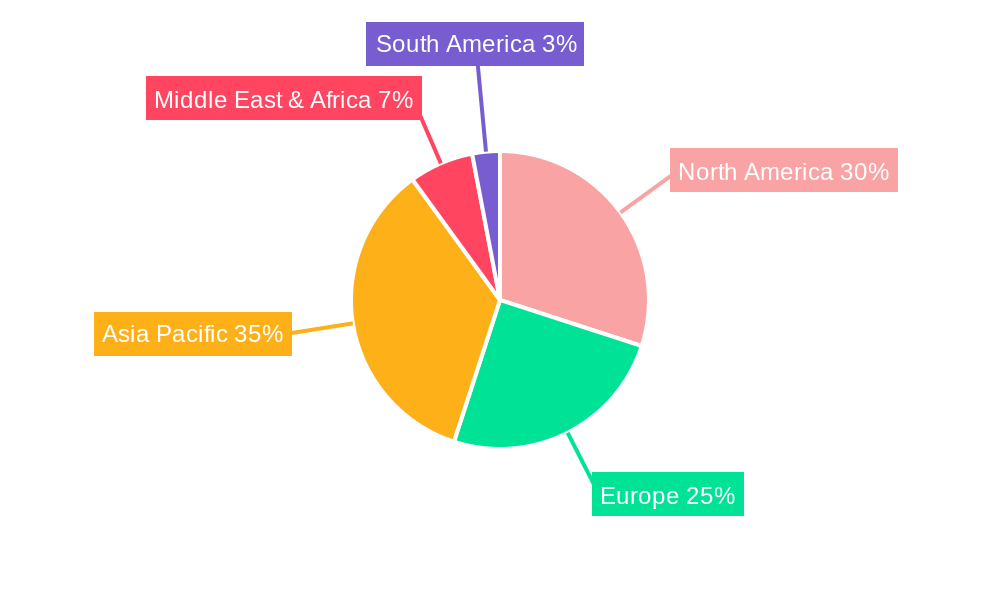

The global LNG and LPG markets are characterized by distinct regional dominance and segment leadership, driven by unique economic, infrastructural, and demographic factors.

Dominant Segments:

Liquefied Natural Gas (LNG): The Industrial segment stands out as a primary consumer of LNG. Across the forecast period (2025-2033), industries requiring a reliable and abundant energy source for manufacturing processes, power generation for industrial facilities, and as a feedstock for petrochemical production will continue to drive significant LNG demand. This includes sectors such as chemicals, manufacturing, cement, and metals. The shift towards cleaner fuels in industrial operations, driven by regulatory pressures and corporate sustainability goals, further bolsters LNG's position. Additionally, the Transportation segment, particularly for heavy-duty trucking and maritime shipping, is witnessing a gradual but significant uptake of LNG. As stricter emissions standards are implemented, LNG offers a viable solution for reducing sulfur oxides (SOx) and nitrogen oxides (NOx) emissions.

Liquefied Petroleum Gas (LPG): The Residential Heating segment remains a cornerstone for LPG demand, especially in developing nations where it serves as a crucial cooking fuel and for heating purposes, offering a cleaner alternative to biomass and kerosene. The sheer volume of households relying on LPG for basic energy needs makes this segment a consistent driver of growth. The Industrial segment also presents considerable opportunities for LPG, particularly in sectors that require localized heating or specialized processes, and as a feedstock in the petrochemical industry. The Others segment, which encompasses applications like autogas (LPG for vehicles), portable stoves, and various industrial uses, is also poised for significant growth. The increasing adoption of autogas in regions with government incentives and established refueling infrastructure highlights its expanding role in the transportation sector.

Dominant Regions/Countries:

Asia-Pacific: This region is a powerhouse for both LNG and LPG markets.

North America:

Middle East: This region is a major producer and exporter of both LNG and LPG, with countries like Qatar and Saudi Arabia playing pivotal roles in global supply. Domestic demand for industrial and residential uses is also significant.

Europe:

The interplay between these dominant regions and segments creates a complex global market where localized demand, supply capabilities, and governmental policies significantly influence the growth and adoption rates of LNG and LPG.

The LNG and LPG industries are propelled by several key growth catalysts. The ongoing global energy transition, with its emphasis on cleaner alternatives to traditional fossil fuels, positions both LNG and LPG as vital transitional fuels. Growing energy demand in developing economies, coupled with the pursuit of energy security and diversification of supply by many nations, further fuels market expansion. Technological advancements in liquefaction, transportation, and storage are enhancing efficiency and reducing costs, making these fuels more accessible. Additionally, favorable government policies, including subsidies for LPG adoption and incentives for using LNG in industrial and transportation sectors, act as significant catalysts.

The global LNG and LPG markets are characterized by the presence of major integrated energy companies and specialized players. Key companies influencing these sectors include:

This report offers an unparalleled and exhaustive coverage of the global LNG and LPG markets. It provides a granular breakdown of market segmentation, encompassing type (LNG, LPG), application (Industrial, Transportation, Residential Heating, Others), and regional analysis. The report meticulously details historical trends from 2019-2024, establishes a clear base year in 2025, and projects future market trajectories through 2033. It delves into the intricate dynamics of demand and supply, analyzes the impact of technological advancements, and explores the evolving regulatory landscape. Furthermore, it identifies key growth catalysts and challenges, providing a balanced perspective on the opportunities and risks within these vital energy sectors.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Cheniere Energy, ConocoPhillips, Qatargas, Woodside Petroleum, TotalEnergies, Shell, ExxonMobil, BP, Chevron, Bharat Petroleum, Repsol.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "LNG and LPG," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the LNG and LPG, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.