1. What is the projected Compound Annual Growth Rate (CAGR) of the Iron Ore Mining?

The projected CAGR is approximately 2.7%.

Iron Ore Mining

Iron Ore MiningIron Ore Mining by Type (Iron Ore Mining Fines, Iron Ore Mining Pellets, Other), by Application (Construction Industry, Transportation, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global Iron Ore Mining market is projected to reach an estimated value of approximately USD 348,890 million by 2025, exhibiting a steady Compound Annual Growth Rate (CAGR) of 2.7% throughout the study period from 2019 to 2033. This sustained growth is underpinned by a robust demand from key end-use industries, primarily the construction sector, which relies heavily on iron ore for steel production. Infrastructure development initiatives across both developed and emerging economies, coupled with the ongoing urbanization trends, will continue to fuel this demand. Furthermore, the transportation sector, encompassing automotive manufacturing and railway infrastructure, represents another significant consumer of iron ore-derived steel, thereby contributing to market expansion. The market is characterized by a strong presence of major global players, including Vale, Rio Tinto, and BHP, who dominate production and supply chains, influencing market dynamics and technological advancements.

The market's trajectory is shaped by several critical drivers, including increasing government investments in infrastructure projects, particularly in Asia Pacific and developing nations. Innovations in mining technologies, aimed at enhancing efficiency, reducing environmental impact, and optimizing resource extraction, are also playing a crucial role. However, the market faces certain restraints, such as stringent environmental regulations and the fluctuating prices of iron ore on the global commodity market, which can impact profitability and investment decisions. Geopolitical factors and trade policies can also introduce volatility. Despite these challenges, the market is expected to witness diversification within its segments, with a growing emphasis on high-grade iron ore fines and pellets to meet the evolving needs of the steel industry. Regional analysis indicates a significant contribution from Asia Pacific, driven by China's immense industrial output, while North America and Europe remain crucial markets due to their established infrastructure and manufacturing bases.

The global iron ore mining industry is a colossal sector, underpinning the very foundation of modern infrastructure and manufacturing. Over the historical period of 2019-2024, the market has experienced dynamic shifts driven by macroeconomic factors, technological advancements, and evolving demand patterns. For instance, in 2023, global iron ore production was estimated to be around 3,500 million tonnes, a figure that has seen steady growth over the preceding years, barring minor fluctuations. The study period, spanning from 2019 to 2033, with a base and estimated year of 2025, anticipates continued expansion, projecting production to reach approximately 3,800 million tonnes by 2025 and further ascend to 4,200 million tonnes by the end of the forecast period in 2033. This growth trajectory is not merely about volume but also about the increasing sophistication of mining operations. Advanced exploration techniques, utilizing AI and machine learning, are enabling more efficient identification of high-grade ore bodies, thereby optimizing extraction processes. Furthermore, the trend towards higher-quality iron ore, particularly in the form of fines and pellets, is becoming more pronounced. In 2024, fines likely accounted for over 2,500 million tonnes of the total production, while pellets represented a significant, albeit smaller, portion, with an estimated 500 million tonnes produced. The "Other" segment, encompassing various processed iron ore products, also plays a crucial role, contributing an estimated 500 million tonnes in 2024. The market's evolution is also characterized by a heightened focus on sustainability. Companies are investing heavily in reducing their environmental footprint, including carbon emissions reduction strategies and improved water management practices, which are increasingly becoming a prerequisite for market participation. The geographical distribution of production remains concentrated, with Australia and Brazil being the dominant players, collectively accounting for over 60% of global output in recent years. The demand side is equally compelling, with the construction industry remaining the primary consumer, utilizing an estimated 2,000 million tonnes of iron ore in 2024 for everything from rebar to structural steel. Transportation infrastructure development and other industrial applications further bolster this demand, consuming an additional 1,000 million tonnes combined in the same year. The shift towards electric vehicles and the continued growth in global population are expected to further fuel the demand for steel, consequently driving the iron ore market upwards. The report will delve into these intricate trends, providing granular insights into production volumes, product mix, and the underlying economic and environmental forces shaping the industry's future.

The iron ore mining industry's robust growth is propelled by a confluence of powerful economic and developmental forces. Foremost among these is the insatiable global demand for steel, the indispensable material for modern infrastructure and manufacturing. The escalating urbanization rates across developing economies, particularly in Asia, are creating an unprecedented need for residential buildings, commercial complexes, and extensive public works, all of which are steel-intensive. By 2023, the construction industry alone was responsible for a significant portion of global iron ore consumption, estimated at over 55%, showcasing its pivotal role. Beyond construction, the transportation sector is another major propellant. Investments in high-speed rail networks, expanding highway systems, and the burgeoning automotive industry, including the growing demand for electric vehicles that still rely on steel components, all contribute to a sustained appetite for iron ore. For instance, in 2024, the transportation sector likely accounted for approximately 20% of the total demand. Furthermore, the ongoing industrialization of emerging economies signifies a broader demand for machinery, appliances, and various manufactured goods, all of which incorporate steel. This industrial expansion is not confined to traditional sectors; the renewable energy sector, with its vast requirements for wind turbines and solar panel infrastructure, also adds to the steel demand and, consequently, the iron ore market. Technological advancements in mining are also playing a crucial role by improving efficiency and reducing costs. Innovations in extraction techniques, beneficiation processes, and automation are enabling miners to extract more ore with greater precision and at a lower cost per tonne. This increased efficiency makes iron ore mining a more attractive investment and supports higher production volumes. The global economic recovery post-pandemic has also injected renewed confidence into major steel-consuming industries, leading to increased capital expenditure and project development, thereby directly impacting iron ore demand.

Despite its robust growth prospects, the iron ore mining sector faces a formidable array of challenges and restraints that can impede its progress. Environmental concerns represent a significant hurdle, with mining operations increasingly scrutinized for their ecological footprint. Issues such as deforestation, water pollution from tailings ponds, and greenhouse gas emissions associated with mining and transportation are under intense pressure from regulatory bodies and the public. The cost of complying with stricter environmental regulations, including investments in sustainable technologies and rehabilitation efforts, can be substantial, impacting profitability. For example, investments in advanced water treatment systems and carbon capture technologies could add several hundred million dollars to operational costs for large-scale mines. Geopolitical instability and trade tensions also pose risks. The concentration of iron ore production in a few key regions makes the market susceptible to disruptions caused by political unrest, trade wars, or export restrictions. Fluctuations in commodity prices, influenced by global economic sentiment and supply-demand imbalances, can also create volatility. A significant drop in iron ore prices, for instance, from an average of $150 per tonne in 2023 to below $100 per tonne, could severely impact the profitability of high-cost producers and deter new investments. Furthermore, the depletion of easily accessible, high-grade ore reserves is becoming a growing concern. As shallow deposits are exhausted, miners are forced to exploit lower-grade ores or delve deeper, which increases extraction costs and requires more sophisticated processing techniques. This necessitates substantial capital investment in new technologies and infrastructure, potentially millions or even billions of dollars for large projects. Labor shortages in skilled mining professions, particularly in remote mining locations, can also create operational bottlenecks. The sheer scale of infrastructure development required for new mines, including roads, railways, and port facilities, can also be a significant barrier, both in terms of cost and time to completion.

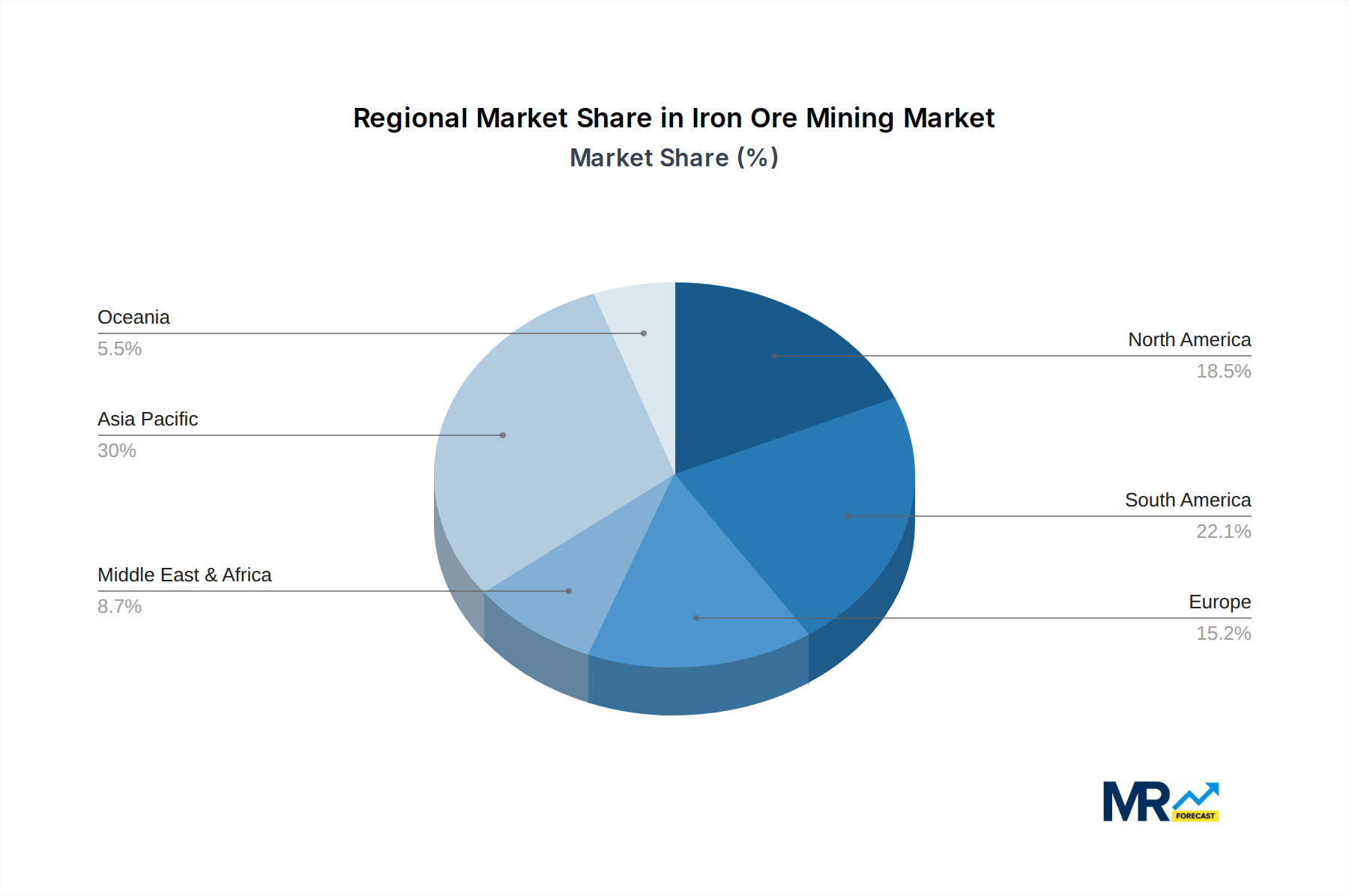

The global iron ore mining market's dominance is intricately linked to both key geographical regions and specific product segments.

Dominant Regions:

Dominant Segments:

Iron Ore Mining Fines: This segment is unequivocally the largest and most dominant within the iron ore market. In 2024, iron ore fines are estimated to have constituted over 70% of the total global iron ore production, translating to approximately 2,500 million tonnes. Fines are the direct output from many crushing and grinding processes and are the most commonly traded form of iron ore globally due to their suitability for direct use in blast furnaces. The ease of transportation and handling, coupled with their high iron content when sourced from high-grade deposits, makes them the workhorse of the steelmaking industry. The sheer volume of construction and infrastructure projects worldwide, particularly in Asia, fuels this consistent and substantial demand for fines.

Iron Ore Pellets: While smaller in volume compared to fines, iron ore pellets represent a significant and growing segment, accounting for an estimated 500 million tonnes in 2024. Pellets are produced from iron ore fines through agglomeration and hardening processes, resulting in a more uniform, dense, and easily handled product. They are highly valued for their consistent size and composition, which leads to improved efficiency and lower emissions in the direct reduction ironmaking process. The increasing adoption of direct reduced iron (DRI) technology, especially for producing high-quality steel for specialized applications like automotive manufacturing, is a key driver for the growth of the pellet segment. As steelmakers strive for greater operational efficiency and reduced environmental impact, the demand for premium products like pellets is expected to rise.

Other: This segment, encompassing a variety of processed iron ore products and concentrates, contributes an estimated 500 million tonnes to the global market in 2024. This category includes products like sinter, lump ore, and iron ore concentrates that may not fit neatly into the "fines" or "pellets" categories. While not as dominant as fines, the "Other" segment plays a crucial role in catering to specific industrial needs and processing requirements of different steelmaking technologies.

The interplay between these regions and segments is crucial. Australia and Brazil primarily export large volumes of iron ore fines, catering to the global demand for blast furnace feedstock. China, while importing significant quantities of fines, also has a considerable domestic fine ore production and is investing in pelletizing technologies to enhance its steel quality. India's domestic mining efforts are also heavily focused on fines to meet its burgeoning construction and manufacturing needs. The growing preference for higher-quality steel and cleaner production methods is gradually shifting the market's focus, favoring segments like pellets, and driving investments in technologies that can produce and utilize them more effectively.

Several key factors are acting as significant catalysts for the iron ore mining industry. The relentless pace of global urbanization and infrastructure development, particularly in emerging economies, is a primary driver, creating sustained demand for steel. The ongoing transition towards cleaner energy sources, such as wind and solar, also necessitates significant steel for their construction. Furthermore, technological advancements in mining, including automation and digital solutions, are enhancing operational efficiency and reducing costs, making extraction more viable. Increased investment in infrastructure upgrades and expansion projects worldwide further bolsters demand.

This report offers an exhaustive examination of the global iron ore mining industry, providing in-depth insights into its current state and future trajectory. Covering the study period from 2019 to 2033, with a base and estimated year of 2025, it meticulously analyzes key market trends, driving forces, and prevailing challenges. The report details the dominance of specific regions and segments, such as Iron Ore Mining Fines and Pellets, and their critical applications in sectors like the Construction Industry and Transportation. It also identifies the leading players and their strategic initiatives, alongside a timeline of significant industry developments. This comprehensive coverage aims to equip stakeholders with the knowledge necessary to navigate the complexities and capitalize on the opportunities within this vital global market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.7%.

Key companies in the market include Vale, Rio Tinto, BHP, Fortescue Metals, Anmining, ArcelorMittal, Anglo American, HBIS Group, Beijing Huaxia Jianlong Mining, Evrazholding Group, Metalloinvest, LKAB Group, Cleveland-Cliff, .

The market segments include Type, Application.

The market size is estimated to be USD 348890 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Iron Ore Mining," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Iron Ore Mining, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.