1. What is the projected Compound Annual Growth Rate (CAGR) of the Insulin Drugs for Diabetes?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Insulin Drugs for Diabetes

Insulin Drugs for DiabetesInsulin Drugs for Diabetes by Type (Rapid-acting Insulin, Short-acting Insulin, Intermediate-acting Insulin, Long-acting Insulin, Ultra-long-acting Insulin, World Insulin Drugs for Diabetes Production ), by Application (Hospital and Clinic, Retail Pharmacies, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

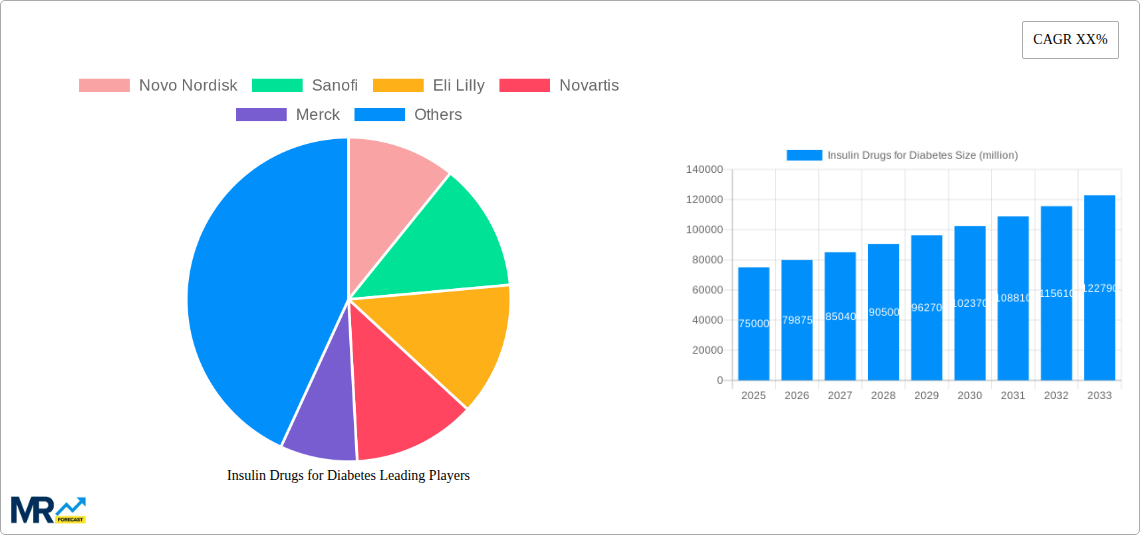

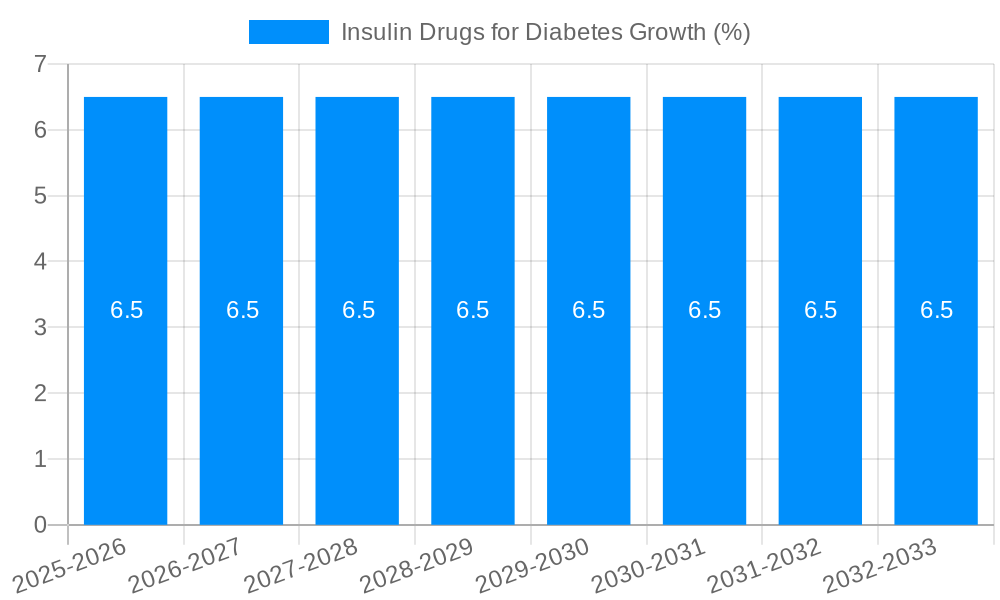

The global Insulin Drugs for Diabetes market is poised for significant expansion, projected to reach approximately USD 75,000 million by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of around 6.5% through 2033. This robust growth is primarily driven by the escalating prevalence of diabetes worldwide, fueled by factors such as increasingly sedentary lifestyles, an aging global population, and rising rates of obesity. The continuous innovation in insulin formulations, including the development of more convenient and effective rapid-acting and ultra-long-acting insulins, further contributes to market expansion. These advancements address unmet patient needs by offering improved glycemic control, reduced dosing frequency, and enhanced patient compliance, thereby solidifying the market's upward trajectory.

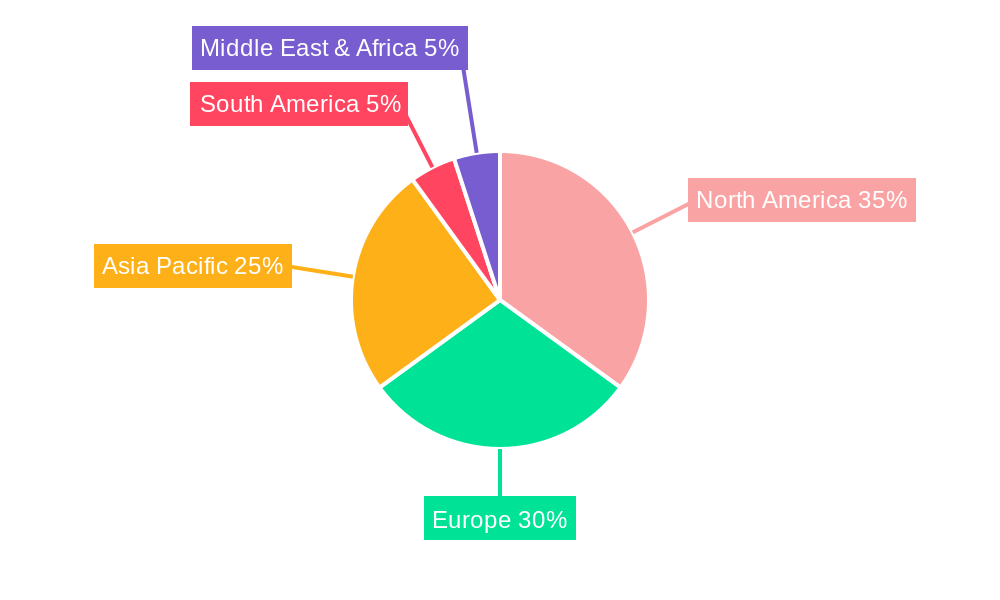

The market segmentation reveals a diverse landscape, with various insulin types catering to specific patient needs and disease progression. Rapid-acting and long-acting insulin segments are expected to witness substantial growth due to their efficacy and patient convenience. The application landscape is dominated by hospital and clinic settings, reflecting the critical role of healthcare professionals in diabetes management and prescription. However, the burgeoning role of retail pharmacies in accessibility and the growing trend of home-based diabetes management will also contribute to their increasing market share. Geographically, North America and Europe currently hold significant market shares, driven by advanced healthcare infrastructure and high diabetes incidence. However, the Asia Pacific region is anticipated to emerge as the fastest-growing market, propelled by increasing awareness, improving healthcare access, and a rapidly growing patient population. Key market players like Novo Nordisk, Sanofi, and Eli Lilly are at the forefront, investing heavily in research and development to introduce next-generation insulin therapies and maintain their competitive edge in this dynamic market.

This comprehensive report offers an in-depth analysis of the global Insulin Drugs for Diabetes market, spanning a study period from 2019 to 2033. The base and estimated year for key projections is 2025, with a detailed forecast period extending from 2025 to 2033, building upon the historical data from 2019-2024. This report aims to provide a nuanced understanding of market dynamics, including production volumes estimated in millions of units, application trends, and the evolving landscape of industry developments. We will explore the intricate interplay of various insulin types, their application across different healthcare channels, and the strategic initiatives undertaken by leading global and regional manufacturers. The report is meticulously crafted to serve as an indispensable resource for stakeholders seeking to navigate this critical segment of the pharmaceutical industry.

The global Insulin Drugs for Diabetes market is experiencing a dynamic transformation driven by a confluence of factors that are reshaping both production and consumption patterns. Over the historical period of 2019-2024, we witnessed a steady upward trajectory in the global production of insulin, reaching approximately 950 million units by 2024. This growth was primarily fueled by the increasing prevalence of diabetes worldwide, a chronic condition characterized by elevated blood glucose levels. As of the estimated year 2025, the global production is projected to surpass the 1000 million unit mark, underscoring the sustained demand.

Several key trends are shaping this market. Firstly, there is a pronounced shift towards advanced insulin formulations, including rapid-acting and ultra-long-acting insulins. These newer generations of insulins offer improved glycemic control, enhanced convenience for patients through less frequent dosing, and a reduced risk of hypoglycemia, a significant concern for individuals with diabetes. The demand for these advanced insulins is projected to outpace that of traditional short-acting and intermediate-acting insulins.

Secondly, the application landscape is evolving. While hospitals and clinics continue to be major consumers, driven by diagnosis and initial treatment, the retail pharmacy segment is witnessing substantial growth. This is attributed to the increasing number of individuals managing their diabetes on an outpatient basis and the growing availability of insulin through prescription refills. Furthermore, the emergence of innovative delivery devices, such as pen injectors and insulin pumps, is enhancing patient adherence and comfort, indirectly boosting market demand.

Technological advancements in insulin production are also a significant trend. Manufacturers are investing in optimizing their production processes to improve efficiency, reduce costs, and ensure a consistent supply of high-quality insulin. This includes advancements in recombinant DNA technology and sophisticated purification techniques. The market is also seeing a gradual diversification of players, with both established multinational corporations and emerging regional manufacturers contributing to the global supply chain.

Looking ahead, the trend towards personalized medicine in diabetes management is expected to gain further traction. This involves tailoring insulin therapy based on individual patient characteristics, genetic predispositions, and lifestyle factors. The integration of digital health technologies, such as continuous glucose monitoring (CGM) systems and smart insulin pens, will also play a pivotal role in enhancing treatment outcomes and empowering patients. By 2033, the market is anticipated to witness a significant increase in the penetration of these integrated solutions, further refining the way insulin therapy is administered and monitored. The overall market is characterized by robust growth, driven by unmet medical needs and continuous innovation in both product development and delivery mechanisms.

The global Insulin Drugs for Diabetes market is experiencing robust growth, propelled by a multifaceted array of driving forces. At the forefront is the alarming and escalating global prevalence of diabetes. As populations age and lifestyle patterns shift towards sedentary habits and unhealthy diets, the incidence of both Type 1 and Type 2 diabetes continues to rise unabated. This surge in diabetic patients directly translates into an increased demand for insulin, a life-sustaining medication for millions. By 2025, the estimated number of individuals requiring insulin therapy is projected to cross the 550 million mark globally, underscoring the sheer scale of this public health challenge.

Beyond the sheer volume of patients, advancements in medical understanding and treatment protocols are also significant drivers. The growing awareness among healthcare professionals and patients about the critical role of insulin in managing hyperglycemia and preventing long-term diabetes-related complications, such as cardiovascular disease, nephropathy, and retinopathy, encourages proactive treatment. This heightened awareness translates into earlier diagnosis and initiation of insulin therapy, thereby expanding the market.

Furthermore, the continuous innovation in insulin product development is a major catalyst. The introduction of novel insulin formulations, including ultra-long-acting insulins offering up to 24-hour coverage and rapid-acting insulins that mimic physiological mealtime insulin release, has revolutionized diabetes management. These advanced insulins provide patients with greater flexibility, improved glycemic control, and a reduced burden of frequent injections, leading to enhanced patient adherence and satisfaction. The availability of these improved therapeutic options is actively stimulating market growth as they offer superior clinical benefits. The sustained investment in research and development by leading pharmaceutical companies is ensuring a pipeline of innovative products that address the evolving needs of patients and clinicians alike.

Despite the significant growth and positive outlook, the Insulin Drugs for Diabetes market is not without its hurdles. One of the most prominent challenges is the high cost of insulin. For many patients, particularly in low- and middle-income countries, the exorbitant price of insulin, especially newer and more advanced formulations, poses a significant barrier to access. This financial strain can lead to inadequate dosing, missed injections, and ultimately, poorer health outcomes, creating a critical issue of affordability and accessibility that impacts global market penetration.

Another substantial restraint is the complex regulatory landscape. The approval process for new insulin drugs and advanced delivery devices is often lengthy, rigorous, and expensive. Navigating these stringent regulatory requirements across different geographies can be a daunting task for manufacturers, potentially delaying the market entry of life-saving innovations. This can slow down the pace at which patients gain access to novel treatments.

Patient adherence and education remain ongoing challenges. While modern insulin formulations and delivery devices offer convenience, ensuring consistent and correct usage requires ongoing patient education and support. Factors such as fear of needles, misperceptions about insulin therapy, and the complexities of dose titration can lead to suboptimal adherence. Bridging this gap requires sustained efforts in patient empowerment and healthcare provider training.

Furthermore, the potential for hypoglycemia associated with insulin therapy, while mitigated by newer formulations, remains a concern. The risk of dangerously low blood sugar levels necessitates careful monitoring and adjustments, which can be challenging for some patients and their caregivers. This inherent risk, though decreasing with advancements, continues to be a consideration in treatment decisions. Finally, the development of biosimilars, while offering potential cost savings, also introduces market complexities and requires careful evaluation of bioequivalence and therapeutic efficacy to ensure patient safety.

The global Insulin Drugs for Diabetes market is characterized by distinct regional dynamics and segment dominance, with North America and Asia Pacific emerging as key players in terms of both production and consumption.

North America, particularly the United States, has historically been a dominant force in the Insulin Drugs for Diabetes market. This dominance stems from several factors:

Asia Pacific is rapidly emerging as a crucial growth engine for the Insulin Drugs for Diabetes market. This region is characterized by:

Segmentation Dominance:

Within the Type of insulin, Long-acting Insulin and Ultra-long-acting Insulin are projected to dominate the market. As of the base year 2025, these advanced insulins are estimated to constitute over 40% of the global insulin market by value and are expected to witness the highest growth rates.

In terms of Application, the Hospital and Clinic segment is expected to remain a significant contributor, given the critical role of these settings in diagnosis, initiation of treatment, and management of complex cases. However, the Retail Pharmacies segment is poised for substantial growth, driven by the increasing number of patients managing their diabetes in outpatient settings and the trend towards home-based care.

The Insulin Drugs for Diabetes industry is experiencing robust growth, fueled by several key catalysts. Foremost is the escalating global prevalence of diabetes, a chronic condition that necessitates lifelong insulin therapy for many individuals. This rising patient population directly translates into sustained demand for insulin products. Furthermore, continuous innovation in insulin formulations, such as the development of ultra-long-acting insulins and novel delivery devices, enhances patient convenience and therapeutic outcomes, driving market adoption. Increased healthcare expenditure, particularly in emerging economies, coupled with government initiatives aimed at improving diabetes management, further accelerates market expansion. The growing awareness and education surrounding diabetes management also empower patients to seek and adhere to insulin therapy, acting as a significant growth stimulant.

This report provides a comprehensive and in-depth analysis of the global Insulin Drugs for Diabetes market, covering a detailed study period from 2019 to 2033. The report meticulously examines market trends, including production volumes in millions of units, and forecasts future growth trajectories. It delves into the driving forces propelling the market, such as the rising global diabetes prevalence and continuous product innovation, as well as the challenges and restraints that influence market dynamics, including cost and regulatory complexities. The analysis highlights key regions and segments expected to dominate the market, providing insights into their growth drivers and potential. Furthermore, it identifies significant growth catalysts and lists the leading players in the industry, along with their significant developments over the study period. This report is designed to equip stakeholders with the essential knowledge to navigate and capitalize on opportunities within this vital segment of the pharmaceutical landscape.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Novo Nordisk, Sanofi, Eli Lilly, Novartis, Merck, AstraZeneca, Bayer, Takeda, Johnson & Johnson, Tonghua Dongbao Pharmaceutical, Wanbang Biopharmaceuticals, HTBT, Gan & Lee Pharmaceuticals, Kamp Pharmaceuticals.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Insulin Drugs for Diabetes," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Insulin Drugs for Diabetes, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.