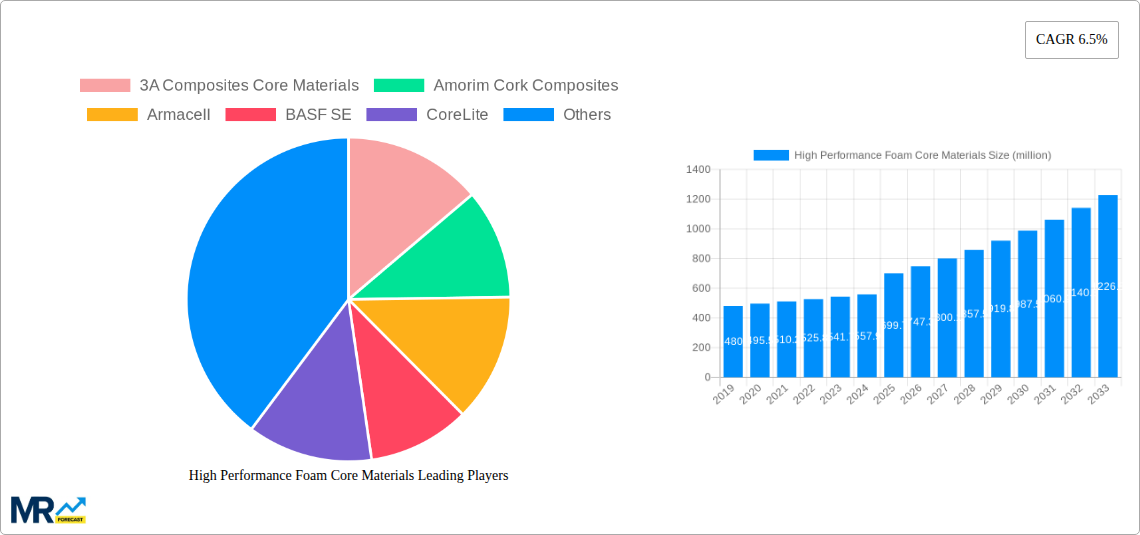

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Performance Foam Core Materials?

The projected CAGR is approximately 6.5%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

High Performance Foam Core Materials

High Performance Foam Core MaterialsHigh Performance Foam Core Materials by Type (PVC Foam Core Materials, Polystyrene Foam Core Materials, Polyurethane Foam Core Materials, PMMA Foam Core Materials, Others), by Application (Wind Energy, Marine, Construction, Transportation, Defense, Aerospace, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The High Performance Foam Core Materials market is poised for substantial growth, projected to reach approximately $699.7 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.5% expected through 2033. This expansion is primarily driven by the increasing demand for lightweight, high-strength, and durable materials across a multitude of industries. Key growth engines include the burgeoning wind energy sector, where large turbine blades benefit immensely from the structural integrity and weight reduction offered by these advanced foam cores, leading to enhanced energy generation efficiency. The marine industry is also a significant contributor, utilizing these materials for boat hulls and superstructures to improve fuel economy and performance. Furthermore, the construction sector's adoption of foam core materials in panels and structural components for insulation and lightweighting purposes is adding considerable momentum to market expansion.

The diverse range of high-performance foam core materials, including PVC, Polystyrene, Polyurethane, and PMMA foam cores, caters to specific application needs, offering tailored solutions for wind energy, marine, construction, transportation, defense, and aerospace industries. While the market is experiencing significant upward trends, certain factors could moderate its pace. The cost of raw materials, particularly for specialized foams, and the complex manufacturing processes involved can present a challenge. Additionally, the development of alternative lightweighting materials and the evolving regulatory landscape concerning material usage and sustainability could influence market dynamics. Nevertheless, the inherent advantages of high-performance foam core materials in terms of weight savings, excellent mechanical properties, and design flexibility are expected to outweigh these restraints, ensuring continued market penetration and innovation.

This comprehensive report provides a detailed examination of the global High Performance Foam Core Materials market, analyzing trends, drivers, challenges, regional dynamics, and key players from 2019 to 2033. The study period encompasses historical data from 2019-2024, a base year of 2025, and a robust forecast period from 2025-2033, with the estimated year also being 2025.

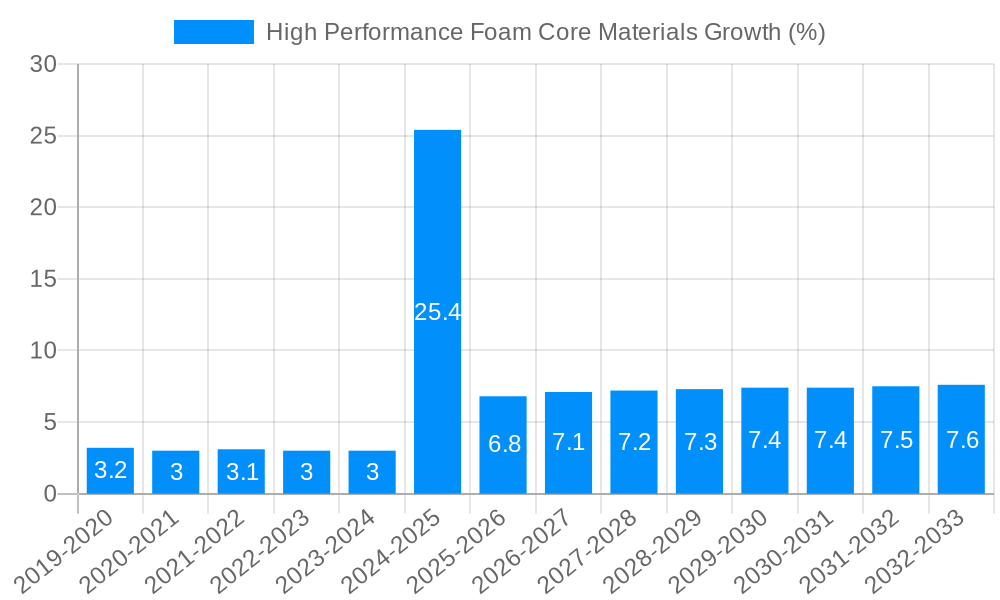

The global High Performance Foam Core Materials market is poised for significant expansion, driven by an insatiable demand for lightweight, durable, and sustainable solutions across a multitude of industries. XXX indicates that the market is witnessing a transformative shift, moving beyond traditional materials to embrace advanced foam core technologies that offer superior mechanical properties and performance characteristics. The increasing adoption of composite materials in sectors like wind energy and aerospace, where weight reduction directly translates to enhanced efficiency and reduced operational costs, is a primary catalyst. For instance, in the wind energy sector, the quest for larger and more efficient wind turbine blades necessitates the use of lightweight yet incredibly strong core materials. This has led to a surge in the demand for advanced PVC and PET foam cores, which offer excellent stiffness-to-weight ratios and fatigue resistance. Similarly, the aerospace industry's continuous pursuit of fuel efficiency and payload optimization is fueling the adoption of high-performance foam cores in aircraft structures, from fuselage components to interior panels. The marine industry, with its focus on fuel economy and enhanced buoyancy, is also a significant contributor to market growth, utilizing these materials in boat hulls and superstructures. Furthermore, the construction sector is increasingly recognizing the benefits of foam core materials in prefabricated building components, offering improved insulation, structural integrity, and faster construction times. The "Others" segment, encompassing applications in sporting goods, automotive interiors, and industrial equipment, also presents substantial growth potential as manufacturers seek to innovate and improve product performance. Overall, the market is characterized by a strong emphasis on material innovation, with a continuous development of new foam chemistries and manufacturing processes aimed at achieving even higher performance benchmarks. This includes the exploration of bio-based and recycled foam core materials, aligning with global sustainability initiatives and catering to environmentally conscious consumers and industries. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period, with market volume expected to reach over 700 million units by 2033.

The growth trajectory of the High Performance Foam Core Materials market is being propelled by a confluence of powerful factors. Foremost among these is the relentless global push for lightweighting across diverse industries. The inherent strength-to-weight ratio of these foam cores makes them indispensable in applications where reducing mass is paramount for enhancing efficiency, improving fuel economy, and reducing operational costs. This is particularly evident in the transportation sector, where lighter vehicles translate to significant fuel savings and reduced emissions, aligning with stringent environmental regulations. Furthermore, the increasing focus on sustainability and the circular economy is acting as a significant driver. Manufacturers are actively seeking materials that offer a reduced environmental footprint throughout their lifecycle, from production to disposal. This has spurred innovation in developing foam cores from recycled materials and bio-based feedstocks, appealing to a growing segment of environmentally conscious consumers and corporate clients. The expanding renewable energy sector, especially wind energy, represents another critical growth driver. The demand for larger and more efficient wind turbine blades necessitates the use of advanced composite materials, with high-performance foam cores forming the structural backbone. Advancements in composite manufacturing techniques, such as vacuum infusion and resin transfer molding, are also enabling the wider adoption of foam core materials in complex structural applications. Finally, the ongoing technological advancements in material science are continuously improving the properties of foam cores, leading to the development of materials with enhanced thermal insulation, acoustic dampening, and fire resistance, thereby expanding their application scope and attractiveness across various industries.

Despite the promising growth, the High Performance Foam Core Materials market is not without its hurdles. A primary challenge lies in the cost of raw materials and manufacturing processes. The production of specialized high-performance foams, particularly those with advanced chemistries or intricate cell structures, can be capital-intensive. This can sometimes make these materials a more expensive option compared to traditional core materials, especially in cost-sensitive applications where margins are tight. Another significant restraint is the need for specialized processing and handling techniques. While advancements are being made, some high-performance foam cores still require specific curing temperatures, pressures, or bonding agents, necessitating specialized equipment and skilled labor. This can create a barrier to entry for smaller manufacturers or those looking to quickly integrate these materials into existing production lines. The perception of durability and long-term performance in certain niche applications can also be a concern. While these materials are engineered for high performance, anecdotal evidence or specific failure cases, even if rare, can create hesitation in adopting them for critical structural components. Furthermore, the complexity of recycling and end-of-life management for certain composite structures incorporating foam cores presents an environmental challenge. While efforts are underway to develop more effective recycling processes, the current infrastructure and technology for dealing with end-of-life composite waste can be a restraint for widespread adoption, particularly in regions with less developed waste management systems. Finally, the inherent technical limitations of certain foam types for specific extreme environments or demanding applications can also act as a restraint, requiring careful material selection and design considerations.

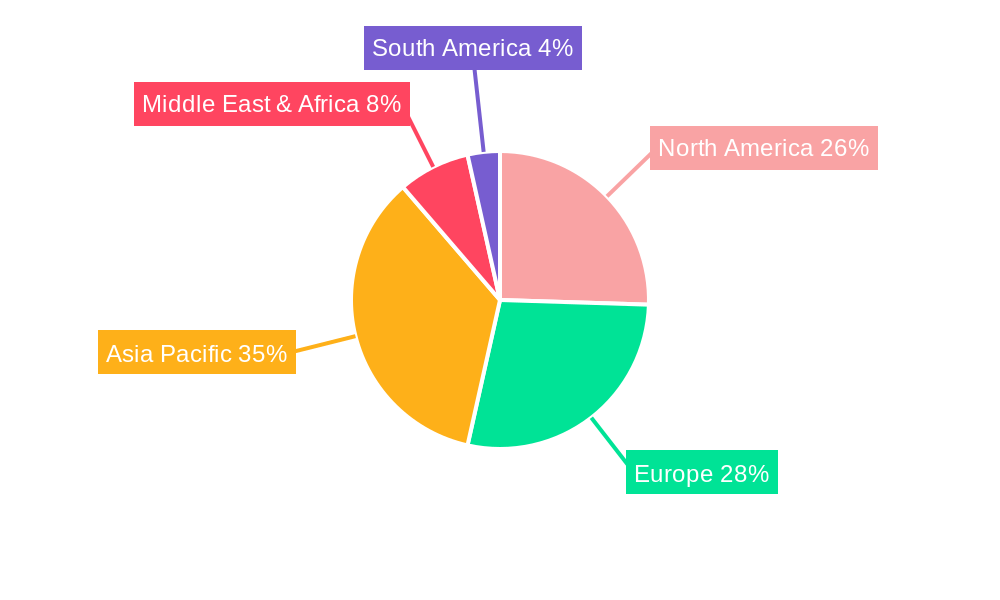

The global High Performance Foam Core Materials market is experiencing a significant concentration of demand and innovation within specific regions and application segments. Europe stands out as a dominant force, particularly in the Wind Energy application segment. This dominance is largely attributable to the region's strong commitment to renewable energy targets, coupled with substantial investments in wind power infrastructure. Countries like Germany, Denmark, and the United Kingdom are at the forefront of wind turbine manufacturing, driving substantial demand for high-performance foam core materials, primarily PVC and PET foam cores, which are crucial for the structural integrity and efficiency of large wind turbine blades. The Aerospace segment, while smaller in volume compared to wind energy, is another critical area where high-performance foam cores are gaining traction, with North America leading the charge. The region's robust aerospace manufacturing industry, home to major players like Boeing and Lockheed Martin, is consistently seeking advanced materials to reduce aircraft weight and improve fuel efficiency. Here, materials like honeycomb cores and specialized PMI (Polyoxymethylene) foams are being increasingly adopted for interior components, fuselage structures, and wing elements.

The Asia-Pacific region is emerging as a rapidly growing market, with Construction and Marine applications showing considerable promise. China, with its massive construction industry and ambitious infrastructure projects, is a significant consumer of foam core materials for insulation, lightweight building panels, and structural components. Similarly, the burgeoning maritime industry in countries like South Korea and Japan, renowned for shipbuilding, is contributing to the demand for lightweight and durable foam cores in boat construction and offshore structures.

Among the Type segments, PVC Foam Core Materials are expected to continue their dominance throughout the forecast period. Their excellent balance of properties, including good mechanical strength, excellent moisture resistance, and ease of processing, makes them a versatile choice across multiple industries. However, Polyurethane Foam Core Materials are anticipated to witness the highest growth rate. Their ability to be tailored for specific properties, such as enhanced fire retardancy and superior adhesion, is driving their adoption in demanding applications, particularly in the defense and transportation sectors. The "Others" segment, which includes innovative materials and niche applications, is also projected to grow steadily as research and development continue to yield new and improved foam core solutions.

The synergy between these dominant regions and key application segments, driven by technological advancements and evolving market demands, will shape the future landscape of the High Performance Foam Core Materials market. The consistent demand from established sectors like wind energy in Europe and aerospace in North America, coupled with the rapid growth in construction and marine in Asia-Pacific, ensures a diversified and robust market outlook.

The High Performance Foam Core Materials industry is fueled by several key growth catalysts. The global imperative for lightweighting across all transportation sectors, including automotive, aerospace, and marine, is a primary driver. Reduced weight directly translates to improved fuel efficiency and lower emissions, aligning with stringent environmental regulations and consumer demand for sustainable solutions. Furthermore, the significant growth in renewable energy infrastructure, particularly in wind energy, necessitates larger and more efficient turbine blades, where advanced foam cores are indispensable for structural integrity and performance. Continued technological advancements in material science are enabling the development of foam cores with superior properties like enhanced stiffness, thermal insulation, and fire resistance, expanding their application scope into more demanding sectors. Lastly, the increasing global focus on sustainability and the circular economy is spurring innovation in bio-based and recycled foam core materials, appealing to environmentally conscious industries and consumers.

This report offers a comprehensive and granular analysis of the High Performance Foam Core Materials market, providing invaluable insights for stakeholders. It delves into market dynamics, exploring the intricate interplay of trends, driving forces, and challenges that shape the industry landscape. With a detailed segmentation of the market by type of foam (PVC, Polystyrene, Polyurethane, PMMA, Others) and application (Wind Energy, Marine, Construction, Transportation, Defense, Aerospace, Others), the report offers a clear understanding of the market's structure and growth potential. Furthermore, it provides an in-depth regional analysis, highlighting key markets and their specific contributions. The report is underpinned by robust market sizing and forecasting, utilizing data from 2019-2024 for the historical period, 2025 as the base and estimated year, and projecting forward to 2033. This rigorous analytical framework equips businesses with the strategic intelligence needed to make informed decisions, identify emerging opportunities, and navigate the complexities of this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.5% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.5%.

Key companies in the market include 3A Composites Core Materials, Amorim Cork Composites, Armacell, BASF SE, CoreLite, Diab, Evonik, General Plastics, Gurit, Hexcel Corporation, Polyumac, The Gill Corporation, Toray Industries.

The market segments include Type, Application.

The market size is estimated to be USD 699.7 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "High Performance Foam Core Materials," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the High Performance Foam Core Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.