1. What is the projected Compound Annual Growth Rate (CAGR) of the High Barrier Film for Food?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

High Barrier Film for Food

High Barrier Film for FoodHigh Barrier Film for Food by Type (PET, CPP, BOPP, PVA, PLA, Others, World High Barrier Film for Food Production ), by Application (Processed Meat Products Packaging, Pet Food Packaging, Snack Packaging, Jam and Salad Dressing Packaging, Frozen Food Packaging, Others, World High Barrier Film for Food Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

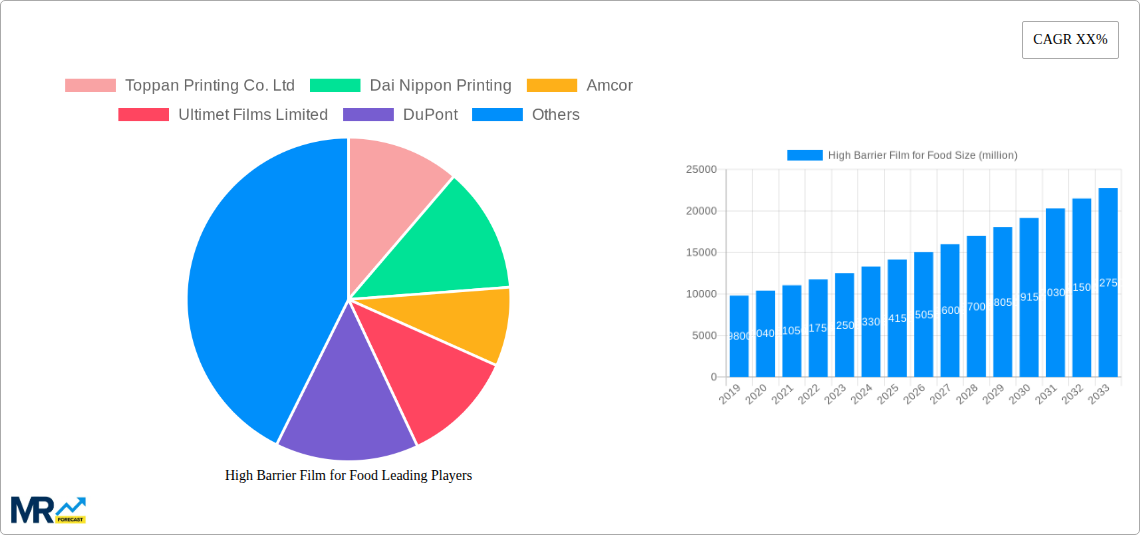

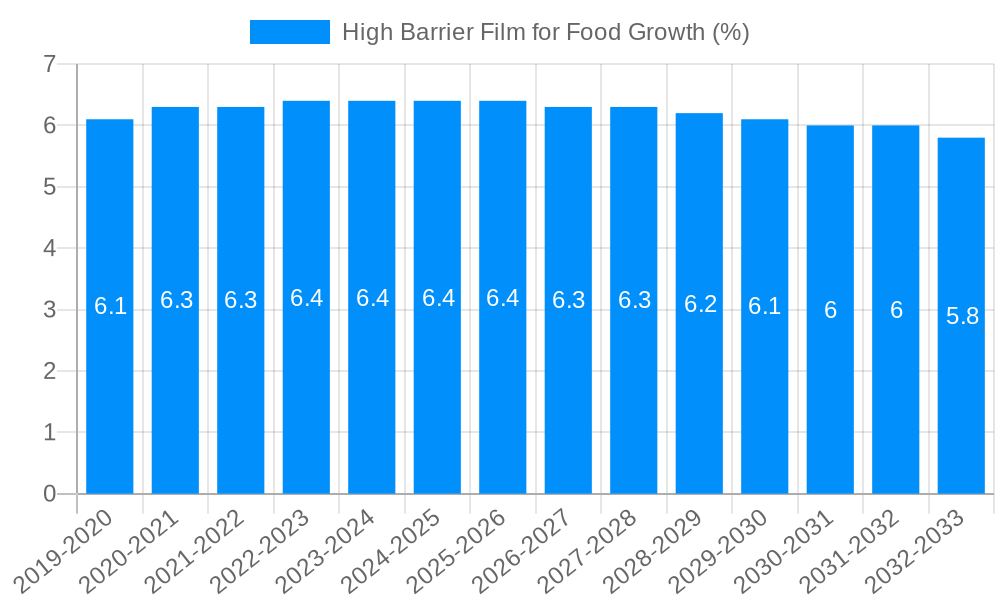

The global High Barrier Film for Food market is poised for significant expansion, projected to reach an estimated USD 15,000 million by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 6.5% throughout the forecast period of 2025-2033. This growth is primarily fueled by the escalating consumer demand for extended shelf-life food products, coupled with a growing awareness of food safety and waste reduction. The increasing preference for convenience foods and the expansion of the processed meat, pet food, and snack segments are key drivers for high barrier film adoption. Manufacturers are actively investing in advanced film technologies that offer superior protection against oxygen, moisture, and aroma transmission, thereby preserving the freshness and quality of packaged foods. Furthermore, the rising disposable incomes in emerging economies are contributing to increased consumption of packaged foods, presenting substantial opportunities for market players.

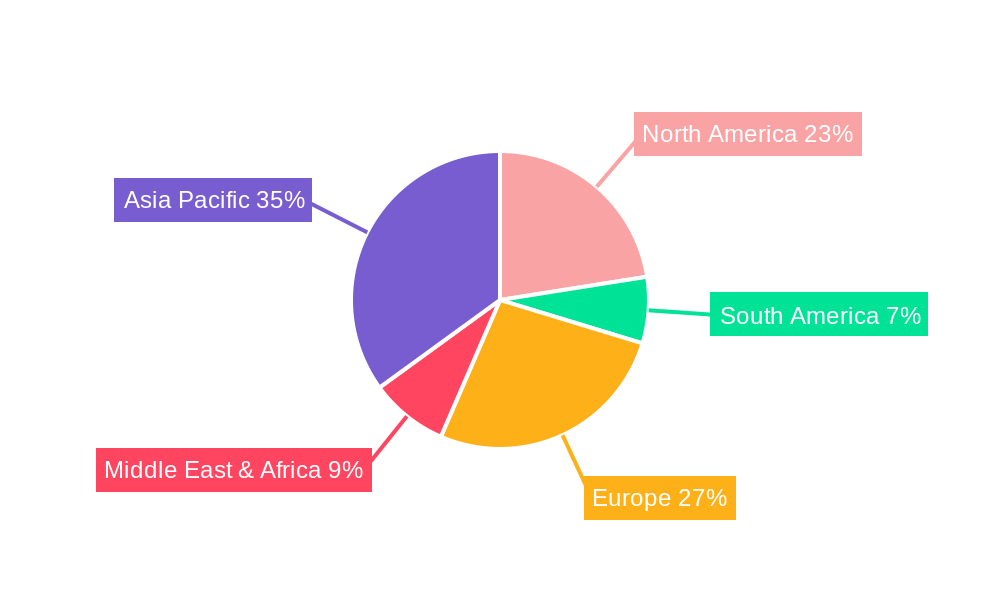

The market landscape for high barrier films is characterized by intense competition and continuous innovation. Key players like Toppan Printing Co. Ltd, Dai Nippon Printing, and Amcor are at the forefront, offering a diverse range of films including PET, CPP, BOPP, and PVA, each tailored to specific food applications. The processed meat products packaging segment is expected to lead the market in terms of application, followed closely by snack packaging and pet food packaging, owing to the inherent need for enhanced shelf-life and product integrity in these categories. Geographically, the Asia Pacific region, led by China and India, is anticipated to witness the highest growth owing to rapid urbanization, a burgeoning middle class, and evolving dietary habits. While the market presents considerable growth potential, stringent regulatory requirements and the fluctuating prices of raw materials pose potential challenges that manufacturers need to navigate strategically.

The global high barrier film market for food packaging is experiencing a significant and dynamic transformation, projected to reach an impressive $15,670.5 million in 2025, with a robust CAGR of 6.2% anticipated throughout the forecast period of 2025-2033. This upward trajectory is underpinned by a confluence of evolving consumer demands, stringent regulatory landscapes, and continuous technological innovation. At the heart of this growth lies the increasing consumer awareness and preference for food products that maintain their freshness, extend shelf life, and preserve their nutritional integrity. The historical period of 2019-2024 has already laid a strong foundation, with the market exhibiting steady expansion. As we move into the base year of 2025, the market stands at a pivotal point, poised for accelerated growth driven by these pervasive trends. Consumers are increasingly seeking convenience without compromising on quality or safety, leading to a heightened demand for packaging solutions that effectively shield food from external contaminants, moisture, oxygen, and light. This necessitates the adoption of advanced barrier technologies that go beyond conventional packaging materials. Furthermore, the food industry's relentless pursuit of reducing food waste is a critical driver, as high barrier films play a vital role in minimizing spoilage during transit, storage, and on retail shelves. The evolving retail landscape, with its emphasis on attractive and informative packaging, also contributes to the adoption of high barrier films that not only protect the product but also enhance its visual appeal and provide essential product information. The study period from 2019 to 2033 provides a comprehensive outlook, encompassing both past performance and future projections, thereby offering a holistic understanding of the market's trajectory and the forces shaping its evolution. The market's resilience and adaptability to changing consumer preferences and industry imperatives are key to its sustained growth.

The global high barrier film for food market is experiencing a potent surge in demand, propelled by an intricate interplay of critical factors. Foremost among these is the escalating consumer consciousness regarding food safety and quality. As consumers become more informed, the demand for packaging that guarantees product integrity, extends shelf life, and prevents spoilage is paramount. This directly translates into a greater need for high barrier films that effectively block oxygen, moisture, and other detrimental elements. Furthermore, the global imperative to curb food waste is a significant catalyst. High barrier films are instrumental in reducing spoilage across the entire supply chain, from production and transportation to retail display, thereby contributing to sustainability goals and economic efficiency. The increasing prevalence of processed and convenience foods also fuels demand. These products often require specialized packaging to maintain their palatability and extend their shelf life, making high barrier films an indispensable component. Moreover, the growth of e-commerce and online grocery delivery services has introduced new challenges and opportunities for food packaging. Ensuring product integrity during longer transit times and variable environmental conditions necessitates advanced barrier properties, further boosting the adoption of high barrier films. The expanding middle class in emerging economies, coupled with rising disposable incomes, is also contributing to a growing appetite for packaged food products, thereby expanding the market for high barrier films.

Despite the robust growth prospects, the high barrier film for food market is not without its inherent challenges and restraints. A primary concern revolves around the cost-effectiveness of these advanced packaging solutions. While offering superior protection, high barrier films often come with a higher price tag compared to conventional packaging materials. This can be a significant barrier for smaller food manufacturers or those operating in price-sensitive markets. The complexity of manufacturing and recycling these multi-layered films also presents a hurdle. The intricate structure, often incorporating various polymers and barrier coatings, can make them difficult to recycle using existing infrastructure, raising environmental concerns and potentially leading to increased waste if not managed properly. Regulatory compliance, while a driver for quality, can also act as a restraint. Adhering to evolving food contact regulations and sustainability mandates across different regions requires continuous investment in research and development, as well as potential retooling of manufacturing processes, which can be a significant operational challenge. Consumer perception and awareness regarding the benefits and environmental impact of high barrier films can also be a limiting factor. Misconceptions about recyclability or the perceived over-packaging can lead to resistance from consumers, impacting market adoption. Finally, technical limitations in achieving specific barrier properties for certain highly sensitive food products, or the challenge of maintaining these properties throughout the entire product lifecycle, can also pose challenges for material scientists and manufacturers.

The global high barrier film for food market is characterized by dynamic regional and segmental dominance, with a keen interplay of factors shaping these leadership positions.

Dominant Regions:

Dominant Segments:

The interplay of these regions and segments highlights a global market driven by consumer demand for safe, fresh, and convenient food products, necessitating the continuous innovation and adoption of high barrier film technologies. The economic scale of these segments, often measured in billions of dollars in terms of market value, solidifies their dominance within the overall high barrier film for food landscape.

Several key factors are acting as potent catalysts for the growth of the high barrier film for food industry. The relentless pursuit of reducing food waste globally, driven by both economic and environmental concerns, is a significant driver. High barrier films play a crucial role in extending product shelf life, thereby minimizing spoilage across the supply chain. Furthermore, the increasing consumer demand for convenience and ready-to-eat food options necessitates packaging that maintains freshness and safety for longer periods. The expanding global middle class, particularly in emerging economies, is fueling the demand for processed and packaged foods, consequently increasing the need for advanced barrier packaging solutions.

This report provides an exhaustive analysis of the global high barrier film for food market, spanning the historical period of 2019-2024 and projecting future trends up to 2033, with a base year of 2025. It delves into the intricate market dynamics, examining key drivers such as escalating consumer demand for food safety and extended shelf life, coupled with the growing global imperative to reduce food waste. The report also addresses the significant challenges, including cost considerations and the complexities of recycling advanced barrier materials. A detailed regional analysis identifies Asia Pacific and North America as key growth engines, while dominant segments like BOPP films and applications such as snack and processed meat packaging are thoroughly explored. The report offers a 360-degree view, empowering stakeholders with actionable insights to navigate this evolving market landscape.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Toppan Printing Co. Ltd, Dai Nippon Printing, Amcor, Ultimet Films Limited, DuPont, Toray Advanced Film, Mitsubishi PLASTICS, Toyobo, Schur Flexibles Group, Sealed Air, Mondi, Wipak, 3M, QIKE, Berry Plastics, Taghleef Industries, Fraunhofer POLO.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "High Barrier Film for Food," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the High Barrier Film for Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.