1. What is the projected Compound Annual Growth Rate (CAGR) of the High Alumina Refractory Material?

The projected CAGR is approximately 8.0%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

High Alumina Refractory Material

High Alumina Refractory MaterialHigh Alumina Refractory Material by Type (0.4, 0.55, 0.7, 0.8, Other), by Application (Special Road & Construction, Industry Kiln, Sewer Applications, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

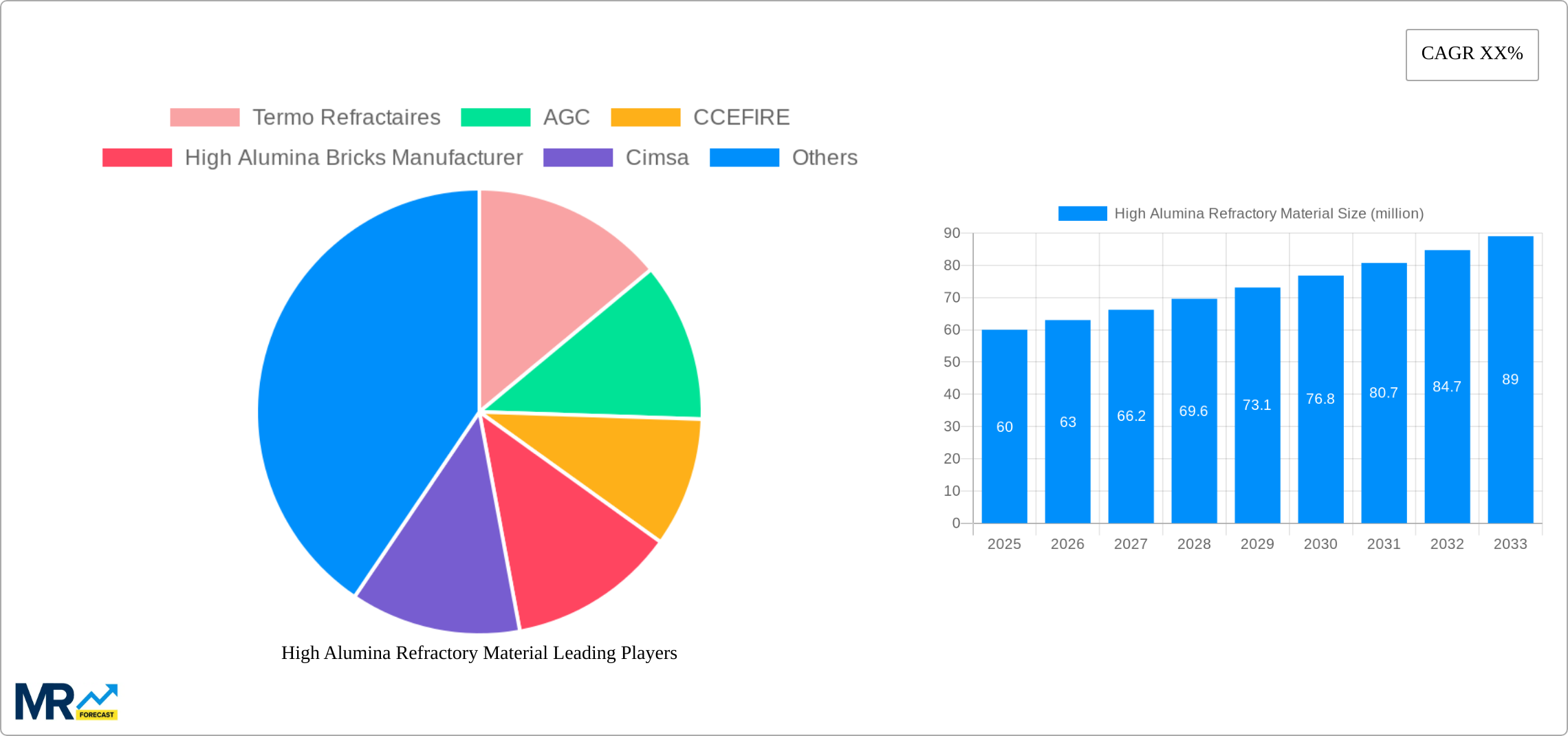

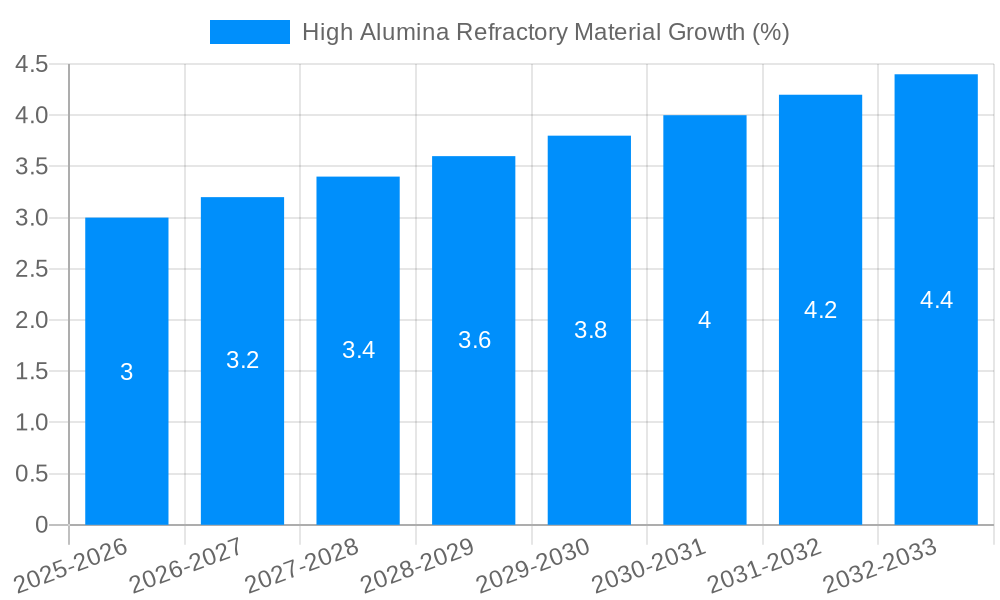

The global High Alumina Refractory Material market is poised for robust growth, with an estimated market size of $35 million and a projected Compound Annual Growth Rate (CAGR) of 8.0% from 2025 to 2033. This expansion is fueled by increasing demand from crucial sectors such as Special Road & Construction and Industry Kiln applications, where the superior heat resistance and durability of high alumina refractories are indispensable. The market's dynamism is further supported by emerging trends in energy efficiency and sustainable industrial practices, which necessitate advanced refractory solutions. For instance, the development of more energy-efficient kilns and the need for longer-lasting materials in construction projects directly contribute to the uptake of high alumina products. The market's trajectory indicates a significant upward trend, with the estimated market size at the end of the forecast period expected to reach approximately $64 million based on the current CAGR.

While the overall outlook is highly positive, certain factors could influence the pace of growth. The "restrains" section, though not explicitly detailed with numerical data, generally points to potential challenges such as the cost of raw materials, the complexity of manufacturing processes, and the availability of substitute materials in specific niche applications. However, the inherent advantages of high alumina refractories, including their high melting point and excellent chemical stability, continue to drive demand, particularly in demanding industrial environments like furnaces and incinerators. The market is segmented by type, with specific alumina content ranges (0.4, 0.55, 0.7, 0.8) indicating a nuanced demand for tailored properties. Key players such as Termo Refractaires, AGC, and CCEFIRE are actively shaping the market landscape through innovation and strategic expansion, ensuring a competitive and evolving industry. The geographic reach of this market is extensive, encompassing major industrial hubs across North America, Europe, and the rapidly developing Asia Pacific region.

Here's a comprehensive report description for High Alumina Refractory Material, incorporating your specified details:

The High Alumina Refractory Material market is poised for significant expansion, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.8% from the historical period of 2019-2024 to the forecast period of 2025-2033. The base and estimated year of 2025 signifies a crucial inflection point, with the market expected to reach a valuation in the hundreds of millions, potentially exceeding $700 million in global revenue by 2025 and charting a course towards over $1 billion by 2033. This upward trajectory is underpinned by a confluence of factors, including the relentless demand from burgeoning industrial sectors and the inherent superior properties of high alumina refractories. Their exceptional resistance to high temperatures, chemical inertness, and superior mechanical strength make them indispensable in applications where conventional refractories falter. The market is witnessing a discernible shift towards specialized, high-performance grades, driven by industries seeking to optimize operational efficiency, extend equipment lifespan, and reduce downtime. For instance, the growing emphasis on energy efficiency and stringent environmental regulations is pushing industries to invest in refractories that can withstand more aggressive operating conditions, thereby enabling higher processing temperatures and reduced energy consumption. Furthermore, advancements in manufacturing processes and material science are leading to the development of novel high alumina refractory formulations with enhanced properties, catering to increasingly complex industrial demands. The study period of 2019-2033 provides a holistic view, encompassing the recovery and growth phases post-pandemic and forecasting robust future expansion. The market's inherent cyclical nature, tied closely to industrial output and capital expenditure cycles, is evident in the historical data, which showcases steady but sometimes fluctuating growth patterns. However, the overarching trend indicates sustained demand and a commitment to innovation within the sector, solidifying its importance in the global industrial landscape.

The High Alumina Refractory Material market is experiencing robust growth, driven primarily by the insatiable appetite of key industrial sectors for materials capable of withstanding extreme temperatures and harsh chemical environments. The Industry Kiln segment, in particular, stands as a significant demand generator. As industries like cement, steel, and non-ferrous metals continue to expand, especially in emerging economies, the need for durable and efficient kilns and furnaces intensifies. High alumina refractories, with their superior refractoriness and resistance to slag and molten metal, are the material of choice for lining these critical pieces of equipment. Their ability to maintain structural integrity at temperatures often exceeding 1500°C directly translates into extended operational lifespans for kilns, leading to reduced maintenance costs and increased productivity. Furthermore, the ongoing global infrastructure development projects, including the construction of advanced manufacturing facilities and power plants, further bolster the demand for high alumina refractories. The inherent strength and thermal stability of these materials are crucial for the construction and operation of these large-scale industrial complexes. This persistent need for durable, high-performance refractory solutions across a wide spectrum of heavy industries forms the bedrock of the current market expansion.

Despite the promising growth trajectory, the High Alumina Refractory Material market is not without its hurdles. One of the primary challenges lies in the volatility of raw material prices. The extraction and processing of alumina-rich ores, the foundational component of these refractories, can be subject to geopolitical factors, supply chain disruptions, and fluctuating market demand for related minerals. Significant price swings in bauxite and other key raw materials can directly impact the production costs for refractory manufacturers, potentially squeezing profit margins or necessitating price increases that could dampen demand, especially in cost-sensitive applications. Moreover, the increasingly stringent environmental regulations concerning mining operations and the disposal of industrial waste pose another significant challenge. Manufacturers are compelled to invest in cleaner production technologies and sustainable practices, which can incur substantial upfront costs. The energy-intensive nature of refractory production also adds to the operational expenditure and the environmental footprint, necessitating a continuous search for energy-efficient manufacturing processes. Furthermore, while high alumina refractories offer superior performance, their higher initial cost compared to some conventional refractories can be a deterrent for certain industries or applications where extreme thermal resistance is not an absolute necessity. This price sensitivity, particularly in less demanding segments, can limit the market penetration of high alumina refractories.

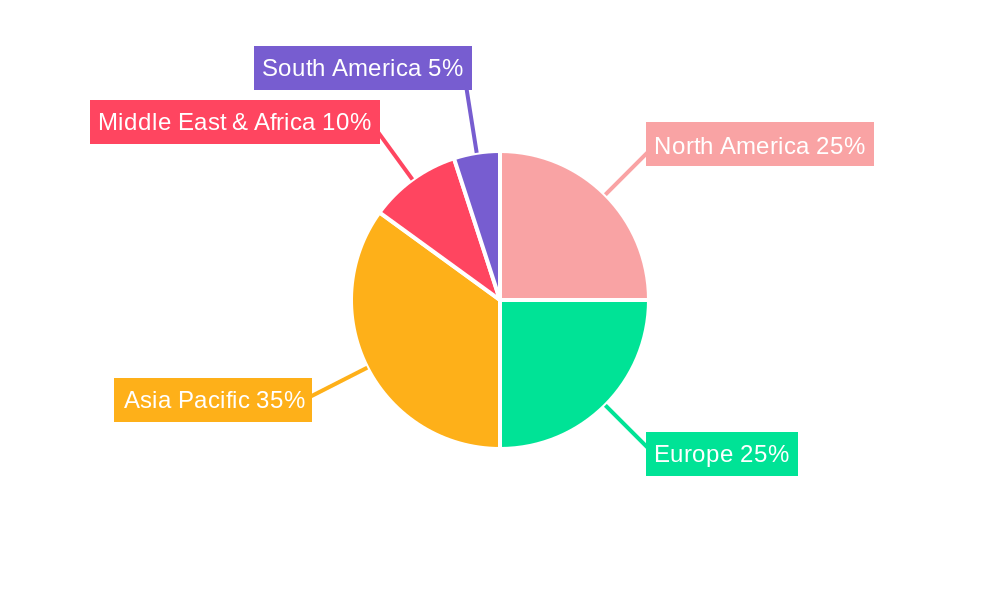

The High Alumina Refractory Material market is poised for significant dominance by the Asia Pacific region, driven by its robust industrial growth and substantial investments in infrastructure and manufacturing. Within this dynamic region, China stands out as a paramount market, accounting for a substantial portion of both production and consumption. The country's vast manufacturing base, encompassing sectors like steel, cement, and ceramics, necessitates a continuous and high volume of refractory materials. Furthermore, China's ongoing urbanization and infrastructure development projects, including the construction of high-speed rail networks and advanced industrial complexes, are creating a sustained demand for high-performance refractory solutions.

The Industry Kiln application segment is projected to be a leading driver of market growth across all regions, but its dominance is particularly pronounced in the Asia Pacific. The sheer scale of industrial operations in countries like China, India, and Southeast Asian nations necessitates the widespread use of high-performance refractories in their extensive network of kilns and furnaces. These kilns are critical for processes such as cement production, where temperatures can routinely exceed 1400°C, as well as in the smelting and refining of metals. The need for refractories that can withstand prolonged exposure to extreme heat, corrosive gases, and abrasive materials makes high alumina types indispensable. The superior mechanical strength and thermal shock resistance of high alumina refractories contribute to longer kiln lifespans and reduced operational downtime, translating into significant cost savings for these energy-intensive industries.

In terms of product types, the 0.7 and 0.8 alumina content grades are expected to witness substantial market share. These grades offer an optimal balance of performance and cost-effectiveness for a wide range of demanding industrial applications. The 0.7 Alumina content refractories provide excellent thermal stability and good resistance to chemical attack, making them suitable for many general industrial kiln applications. The 0.8 Alumina content refractories, on the other hand, push the performance envelope further, offering enhanced resistance to higher temperatures and more aggressive chemical environments. This makes them ideal for specialized applications within the steel industry, such as in ladles and tundishes, and in advanced ceramic firing processes. While other types like 0.4 and 0.55 alumina content refractories will continue to serve specific niche markets or less demanding applications, the trend towards higher performance and increased operational efficiency is likely to favor the higher alumina content grades, driving their market dominance.

The presence of major refractory manufacturers and raw material suppliers in the Asia Pacific region, coupled with a cost-competitive manufacturing environment, further solidifies its position as the dominant market. Companies like CCEFIRE and HeNan JunSheng Refractories Limited are significant players contributing to this regional dominance. Their ability to produce high-quality, high-alumina refractory materials at scale, coupled with a deep understanding of the specific needs of the regional industries, positions them favorably to capture a significant share of this growing market. The continuous investment in research and development by these players to improve material properties and manufacturing processes will further propel the market forward.

The High Alumina Refractory Material industry is propelled by several key growth catalysts. The ongoing industrialization and infrastructure development in emerging economies are creating a sustained demand for high-temperature materials in sectors like cement, steel, and power generation. Furthermore, the increasing focus on energy efficiency and sustainability is driving the adoption of advanced refractories that can withstand higher operating temperatures and improve thermal performance, leading to reduced energy consumption. Technological advancements in refractory manufacturing are also enabling the development of specialized high-alumina grades with enhanced properties, catering to evolving industry needs and niche applications.

This report provides an in-depth and comprehensive analysis of the global High Alumina Refractory Material market, spanning the historical period of 2019-2024 and projecting growth through 2033, with a base year of 2025. It meticulously details market trends, driving forces, challenges, and regional dynamics. The report offers detailed segmentation by type (0.4, 0.55, 0.7, 0.8, Other) and application (Special Road & Construction, Industry Kiln, Sewer Applications, Other). It also includes an exhaustive list of leading market players and their recent significant developments, providing invaluable insights for stakeholders seeking to understand the market's current state and future potential.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.0% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.0%.

Key companies in the market include Termo Refractaires, AGC, CCEFIRE, High Alumina Bricks Manufacturer, Cimsa, P-D Refractories GmbH, Imerys Group, Caltra Nederland, U.S. Electrofused Minerals, Shree Harikrushna Industries, HeNan JunSheng Refractories Limited, Zhengzhou Dengfeng Smelting Materials, .

The market segments include Type, Application.

The market size is estimated to be USD 35 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "High Alumina Refractory Material," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the High Alumina Refractory Material, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.