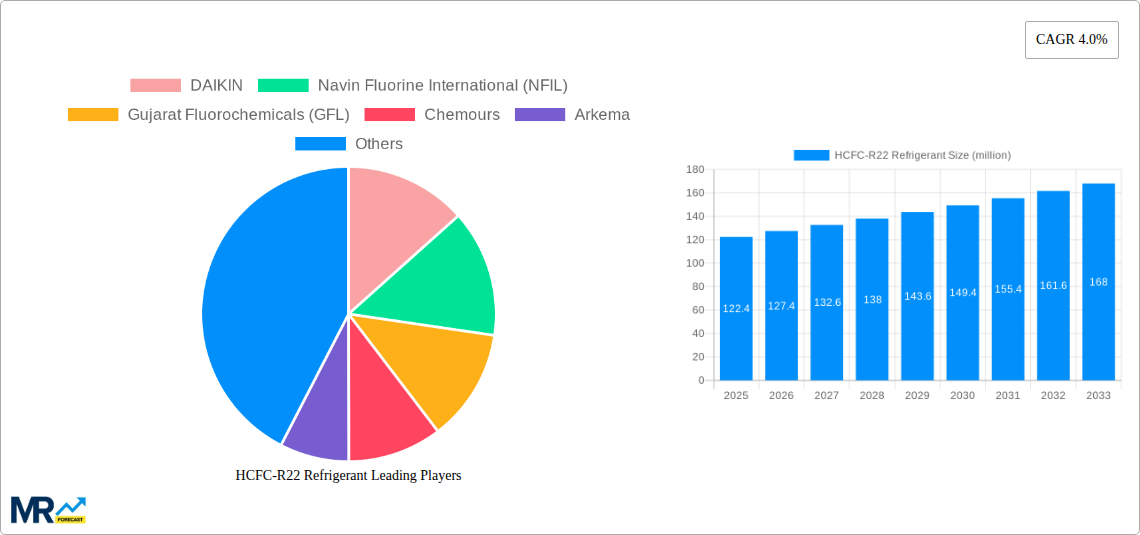

1. What is the projected Compound Annual Growth Rate (CAGR) of the HCFC-R22 Refrigerant?

The projected CAGR is approximately 4.0%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

HCFC-R22 Refrigerant

HCFC-R22 RefrigerantHCFC-R22 Refrigerant by Type (Disposable Steel Cylinders, Refillsble Steel Cylinders), by Application (Air-Condition, Refrigerator, Blowing Agent, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The HCFC-R22 refrigerant market, valued at $122.4 million in 2025, is projected to experience a compound annual growth rate (CAGR) of 4.0% from 2025 to 2033. This growth is driven primarily by its continued use in existing refrigeration systems, particularly in developing economies where replacement with more environmentally friendly alternatives is slower due to cost considerations and limited infrastructure. However, stringent environmental regulations aimed at phasing out HCFC-R22 due to its ozone-depleting potential are acting as a significant restraint. This regulatory pressure is leading to a decline in new installations and a gradual shift towards HFC and natural refrigerants. Key players like Daikin, Navin Fluorine International, and Chemours are navigating this evolving landscape through strategic investments in alternative refrigerant technologies and exploring opportunities in the maintenance and servicing of existing R22 systems. The market segmentation is likely influenced by application (e.g., commercial refrigeration, air conditioning), geographic region, and refrigerant type (pure R22, blends). The regional market share will likely be skewed towards developing nations with a larger base of existing R22 systems and slower adoption rates for replacements. Despite the downward pressure from regulations, the existing installed base ensures a steady, albeit declining, demand for HCFC-R22 in the near to mid-term.

The forecast period of 2025-2033 will see a gradual decrease in the market size for HCFC-R22 as regulatory pressure intensifies and the adoption of alternative refrigerants accelerates. While the initial growth will be driven by existing system maintenance and limited new installations, the overall trend demonstrates a significant decline. This decline will be more pronounced in developed nations where environmental regulations are stricter and the transition to alternatives is well underway. However, developing nations might experience a slightly extended period of R22 usage due to economic factors. Market players will need to adapt by investing in research and development of more sustainable solutions and focusing on services related to the management and responsible disposal of R22. This will help them maintain a market presence even as the overall demand for HCFC-R22 diminishes.

The HCFC-R22 refrigerant market, while facing significant headwinds due to its ozone-depleting potential, continues to exhibit a complex trajectory. The global market size, estimated at approximately 15 million units in 2025, is projected to witness a modest growth during the forecast period (2025-2033), driven primarily by existing infrastructure and the high cost of transitioning to environmentally friendly alternatives. However, this growth is likely to be uneven, significantly impacted by stringent environmental regulations and the increasing adoption of hydrofluoroolefins (HFOs) and other refrigerants with lower global warming potential (GWP). The historical period (2019-2024) witnessed a decline in R22 consumption in developed nations due to phase-out schedules, but developing economies saw continued, albeit slowing, demand, primarily in the retrofitting of existing refrigeration systems where replacement costs remain a significant barrier. This contrast underscores the geographical disparities in market dynamics. The estimated market value in 2025 suggests a significant slowdown from peak levels, reflecting the global effort to phase down HCFCs. The forecast period will likely see further market contraction as regulations tighten and replacement solutions become increasingly cost-competitive, particularly in the long term. While some niche applications may continue to utilize R22, the overall trend is undeniably towards its eventual replacement. The report provides detailed insights into regional variations, including the continued demand in certain developing regions, alongside projections that account for policy shifts and technological advancements impacting market share and value. The current balance between legacy demand and growing environmental concerns creates a dynamic landscape for stakeholders to navigate.

Despite the phasing out of HCFC-R22, several factors continue to support residual demand. Firstly, the existing infrastructure reliant on R22 represents a significant installed base in older HVAC systems, particularly in developing countries. The high cost of complete system replacements often makes retrofitting with R22, despite its environmental drawbacks, a more economically viable option in the short term for many businesses and individuals. Secondly, the availability of recycled and reclaimed R22 extends its lifespan, albeit temporarily, thus sustaining a small but persistent market. Thirdly, a lack of readily available and affordable alternatives in certain regions continues to prop up demand for R22, especially in applications lacking access to modern refrigeration technologies. Finally, in some specialized industrial applications, R22's unique properties might still provide advantages not easily replicated by current alternatives, maintaining a niche market. However, it is crucial to acknowledge that these driving forces are temporary and subject to significant erosion as environmental regulations tighten and more cost-effective alternatives gain wider adoption.

The primary challenge facing the HCFC-R22 refrigerant market is the global phase-out mandated under the Montreal Protocol. This phase-out, aimed at mitigating ozone depletion, necessitates a continuous reduction in production and consumption, resulting in decreasing market size. Furthermore, the rising awareness of the high global warming potential (GWP) of R22 is putting increasing pressure on its use, even in applications where it remains viable. The increasing cost of compliance with stricter environmental regulations adds to the economic burden on manufacturers and users. Additionally, the development and growing adoption of environmentally friendly alternatives, such as HFOs, are aggressively challenging R22's position. These alternatives, while potentially more expensive upfront, offer long-term cost savings through reduced energy consumption and compliance-related expenses. The limited lifespan of R22, coupled with the increasing difficulty in procuring it, is also a factor hindering market growth. These combined challenges are actively shrinking the market's size and lifespan.

While precise market share data requires proprietary information from the full report, several regions and segments are expected to show continued, albeit declining, relevance within the market:

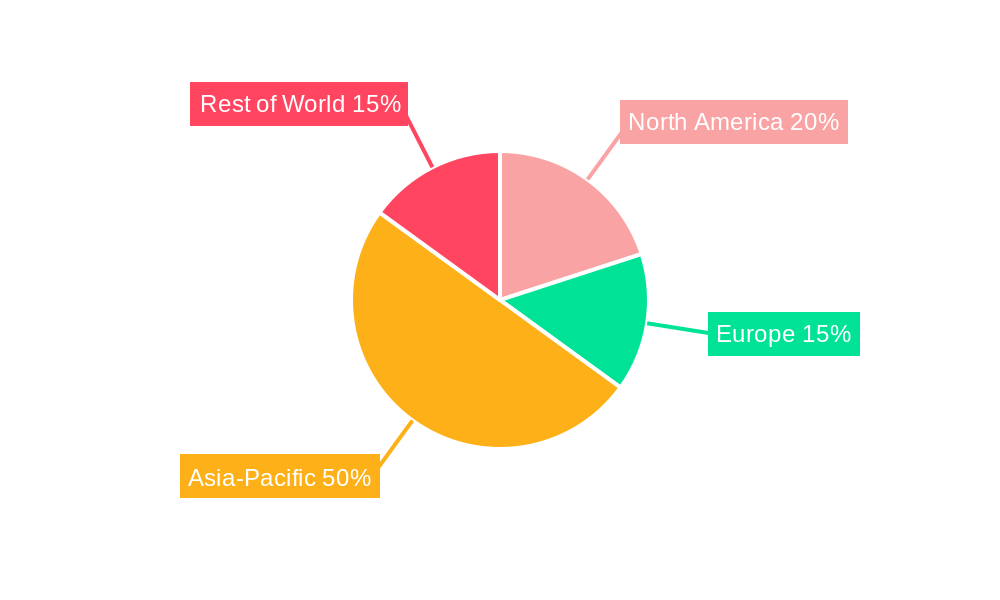

Developing Economies: Regions in Asia, Africa, and parts of South America are predicted to retain a significant, though diminishing, share of the HCFC-R22 market due to existing infrastructure, affordability concerns, and slower adoption of alternative refrigerants. The significant installed base of R-22-based systems in these regions means significant continued demand for refills and servicing, even amidst a global phase-out. The slower pace of technological upgrades also plays a significant role. Policy interventions and financial incentives towards greener technologies are therefore vital to accelerate the transition.

Retrofit and Servicing Segment: The market for R22 is largely dominated by the retrofit and servicing segments. The need for maintenance and repair of existing R22-based systems will sustain a modest demand for the refrigerant during the forecast period, even as new installations dwindle. This segment's dominance reflects the large installed base of equipment globally.

Industrial Refrigeration: While some industrial applications may still utilize R-22 for niche applications where alternatives prove unsuitable or less efficient, the overall trend is towards phasing out this usage as well. However, this segment maintains a specific share in the market due to the high cost of switching to alternative solutions.

The forecast predicts a continued but steadily decreasing importance of these areas in the coming years, as global regulations are enforced and economically viable alternatives are more readily available. The transition is not uniform, with some regions experiencing a faster shift away from R22 than others, highlighting the heterogeneity of the market.

Despite the overall decline, some factors might temporarily catalyze growth. Recycling and reclamation efforts can extend the lifespan of existing R22, thereby prolonging its market presence to some extent. However, this effect is limited and cannot reverse the overall downward trend. Localized production in certain developing countries where regulations are less stringent might temporarily boost local supply, but this remains a short-term phenomenon with limited impact on the global market. The continued servicing of older refrigeration systems will create a persistent, although shrinking, need for R22 refills. Ultimately, these catalysts are limited and unsustainable given the larger trend of the global phase-out.

This report offers a detailed analysis of the HCFC-R22 refrigerant market, considering historical trends (2019-2024), the current market status (Base Year: 2025, Estimated Year: 2025), and providing comprehensive forecasts (2025-2033). It examines market dynamics, including driving forces, challenges, and growth catalysts, and provides insightful market segmentation and regional breakdowns, enabling informed decision-making for stakeholders. The report also identifies key players and analyzes significant developments impacting the industry. The study period (2019-2033) provides a holistic view of the market's evolution, offering critical insights into the ongoing transition towards environmentally friendly alternatives.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.0% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.0%.

Key companies in the market include DAIKIN, Navin Fluorine International (NFIL), Gujarat Fluorochemicals (GFL), Chemours, Arkema, Dongyue Group, Zhejiang Juhua, Jiangsu Meilan Chemical, Sanmei, 3F, Yingpeng Chemicals, Zhejiang Linhai Liming Chemical, Bluestar Green Technology, Shandong Yuean Chemical, Zhengjiang Yonghe Refrigerant, China Fluoro Technology, Zhejiang Lantian Environmental Protection Hi-Tech, Zhejiang Weihua Chemical, .

The market segments include Type, Application.

The market size is estimated to be USD 122.4 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "HCFC-R22 Refrigerant," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the HCFC-R22 Refrigerant, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.