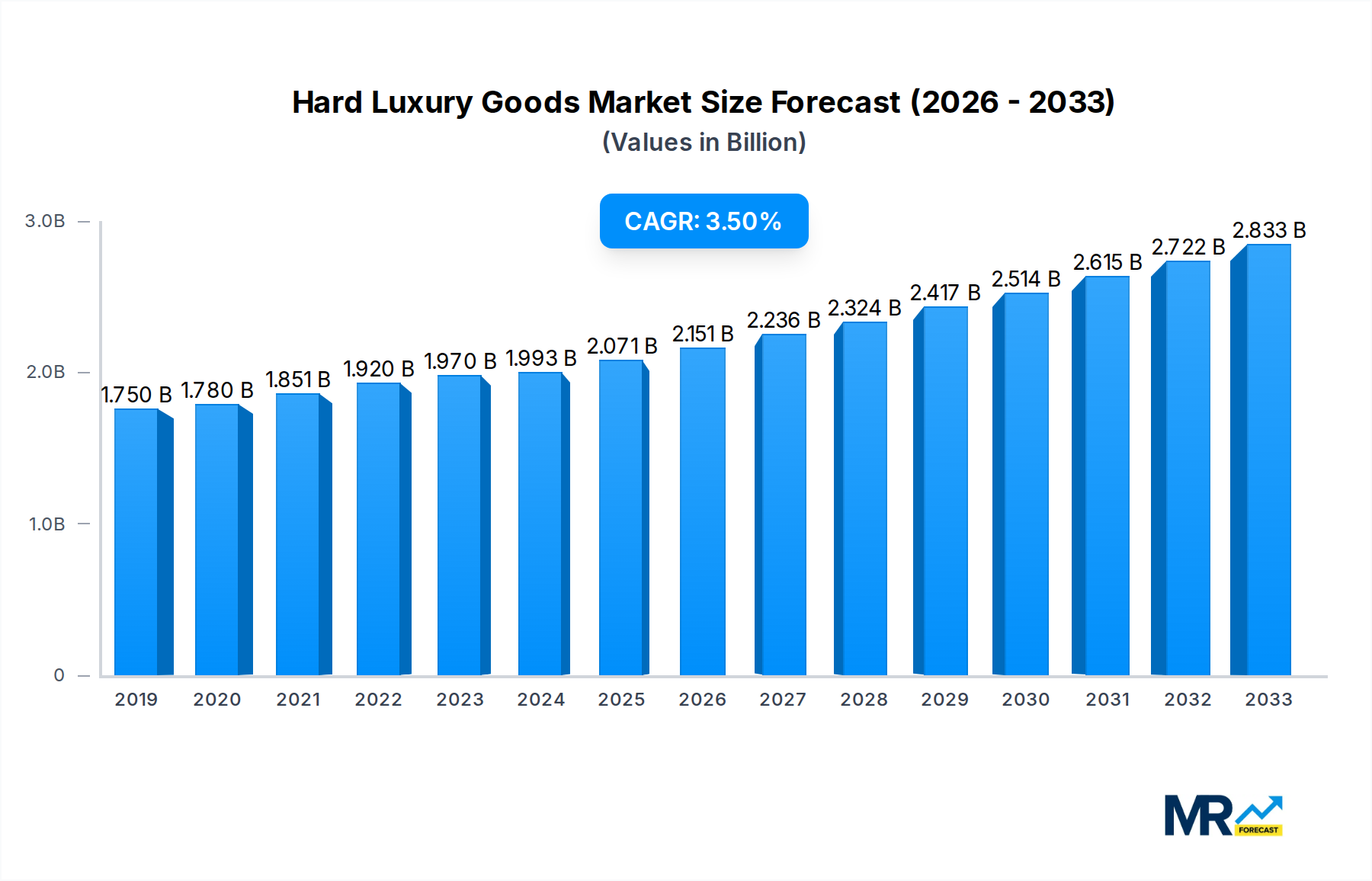

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hard Luxury Goods?

The projected CAGR is approximately XX%.

Hard Luxury Goods

Hard Luxury GoodsHard Luxury Goods by Type (Watches, Jewelry, Other), by Application (Monobrand Store, Department Store, Specialty Store, Online Store, World Hard Luxury Goods Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The hard luxury goods market, encompassing high-end watches, jewelry, and other accessories, presents a lucrative landscape with a 2025 market size estimated at $84.33 billion. While the provided CAGR is missing, considering the consistent growth in the luxury sector fueled by increasing disposable incomes in emerging markets and a growing preference for exclusivity, a conservative estimate of 5-7% annual growth seems reasonable. This translates to a projected market value exceeding $110 billion by 2033. Key drivers include the rising affluent population in Asia-Pacific, particularly China and India, along with a strengthening preference for personalized experiences and sustainable luxury practices. The market is segmented by product type (watches, jewelry, other) and distribution channels (monobrand stores, department stores, specialty stores, online stores). Online channels are experiencing significant growth, driven by enhanced e-commerce platforms and increased digital marketing efforts. However, restraints include economic downturns and geopolitical instability, which can significantly impact consumer spending on luxury goods. The competitive landscape is dominated by established luxury brands like LVMH, Richemont, and Swatch Group, each leveraging its unique brand heritage and product portfolios to cater to a diverse customer base.

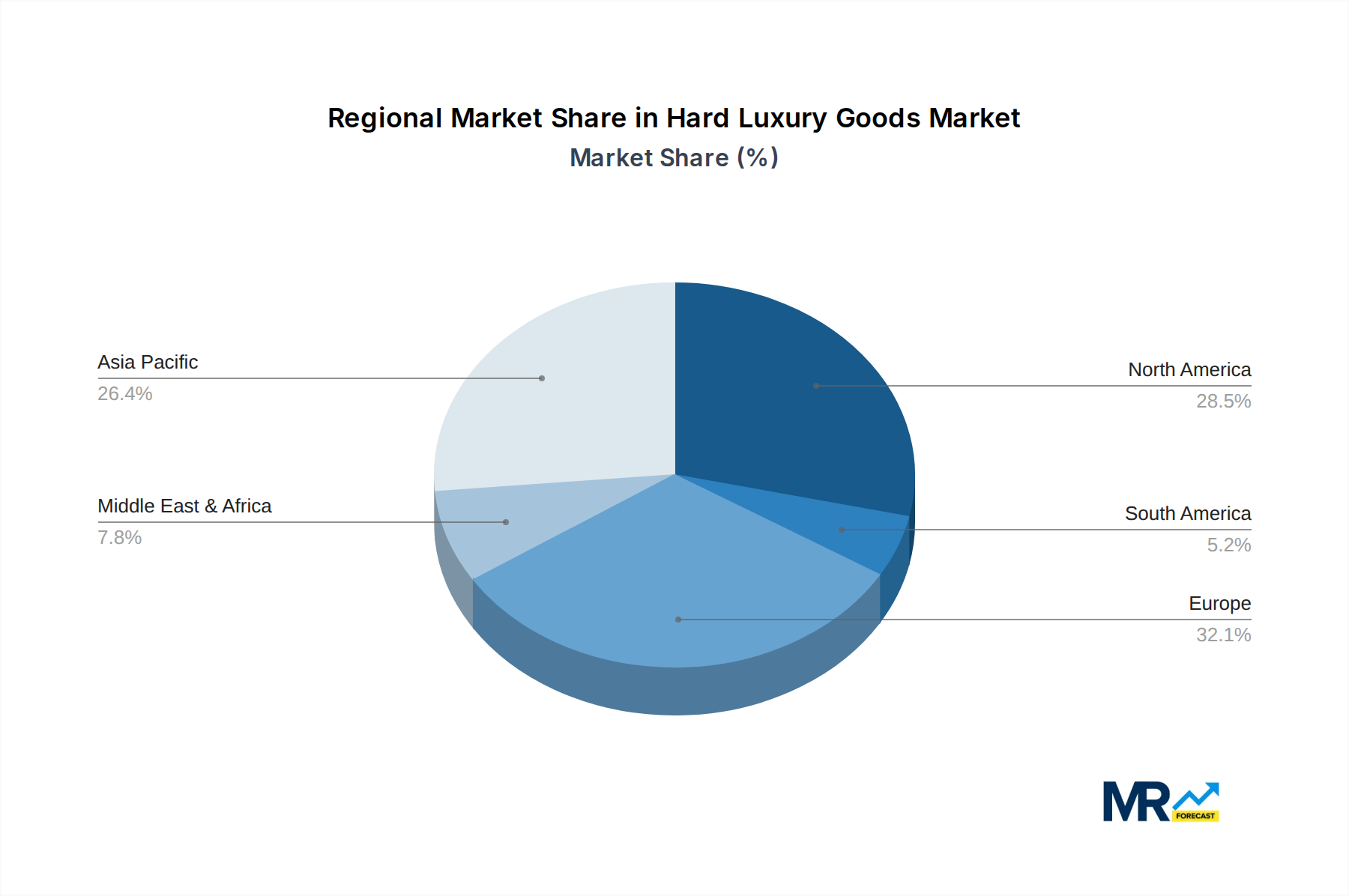

The regional breakdown shows a strong presence across North America, Europe, and Asia-Pacific. North America and Europe, traditional strongholds, maintain substantial market share, but Asia-Pacific is experiencing the most rapid expansion, driven by the aforementioned growth in affluence and luxury consumption. The forecast period (2025-2033) indicates continued growth, though at a potentially moderating rate compared to the initial years. This moderation might be due to market saturation in certain segments or increased competition. Successful players will be those that adapt to changing consumer preferences, embrace digitalization, and maintain a commitment to sustainability and ethical sourcing. This will lead to sustained growth and profitability within the hard luxury goods sector despite potential global economic fluctuations.

The hard luxury goods market, encompassing high-end watches, jewelry, and other luxury accessories, experienced significant fluctuations between 2019 and 2024, mirroring global economic trends and shifting consumer preferences. The historical period (2019-2024) saw a mixed performance, with certain segments, like high-end watches, experiencing a decline due to supply chain disruptions and reduced consumer spending in certain regions impacted by the pandemic. However, the market demonstrated resilience, particularly in the jewelry sector, driven by strong demand from emerging markets and the enduring appeal of heirloom pieces. The estimated year 2025 shows a rebound, indicating a recovery from the pandemic-related setbacks and a renewed interest in luxury goods as a form of investment and self-expression. The forecast period (2025-2033) projects robust growth, fueled by increasing disposable incomes in key markets, a growing affluent middle class, and the continued expansion of e-commerce channels for luxury purchases. Millennials and Gen Z, known for their digitally native lifestyles and appreciation for bespoke experiences, are emerging as a significant driver of market expansion, influencing both design preferences and purchasing behaviors. This younger demographic's preference for unique, ethically sourced, and sustainable luxury products is shaping innovation and brand strategies. The market is also witnessing a strong trend towards personalization and customization, with consumers increasingly demanding unique pieces that reflect their individual styles and tastes. This trend is pushing luxury brands to offer more bespoke services and limited-edition collections. Overall, the hard luxury goods market is poised for considerable expansion in the coming years, driven by a confluence of factors including economic recovery, evolving consumer demographics, and technological advancements. The projected growth is expected to reach several billion units by 2033, surpassing the production levels of the pre-pandemic era. While challenges remain, the inherent value proposition and enduring appeal of hard luxury goods ensure sustained market growth.

Several key factors are propelling the growth of the hard luxury goods market. Firstly, the expanding global affluent population, particularly in emerging markets like Asia and the Middle East, presents a vast pool of potential consumers with increased disposable income to spend on luxury items. Secondly, the increasing popularity of luxury goods as investment assets contributes significantly to market expansion. High-value watches and jewelry are often viewed as stable, appreciating assets, attracting investors seeking alternative investment opportunities. Thirdly, the rise of e-commerce and the increasing sophistication of online luxury retail platforms provide brands with access to a wider global customer base and enhance customer experience through personalized shopping journeys and virtual consultations. Furthermore, strong brand loyalty and the enduring aspirational appeal of hard luxury goods contribute to consistently high demand. Consumers are willing to pay a premium for the craftsmanship, quality, and exclusivity associated with reputable luxury brands. Finally, innovations in materials, design, and technology are constantly pushing the boundaries of luxury, introducing new and exciting products that attract both existing and new customers. This continuous evolution helps maintain the sector's dynamism and appeal, ensuring sustained growth throughout the forecast period.

Despite the positive outlook, the hard luxury goods market faces several significant challenges. Economic downturns and geopolitical instability can significantly impact consumer spending on luxury goods, making the market susceptible to macroeconomic fluctuations. Counterfeit products represent a major threat, eroding brand value and impacting the authenticity of luxury brands. Stricter regulations and increased scrutiny regarding ethical sourcing of materials and labor practices are putting pressure on brands to enhance their sustainability efforts and transparency. The fluctuating price of precious metals like gold and platinum impacts the pricing and profitability of jewelry and certain types of watches, creating unpredictability in the market. Furthermore, the rise of digitally native brands and direct-to-consumer models are increasing competition within the industry, requiring established luxury brands to adapt and innovate to retain their market share. Lastly, changes in consumer preferences and trends require constant adaptation, demanding creative and agile strategies from luxury brands. Successfully navigating these challenges requires a strategic approach that balances brand heritage with modern consumer expectations and technological advancements.

Key Region: Asia-Pacific, specifically China, is expected to dominate the hard luxury goods market throughout the forecast period (2025-2033). The region's rapidly expanding affluent middle class, coupled with a strong cultural appreciation for luxury goods, fuels significant demand.

Key Segment (Type): Jewelry consistently shows robust performance, driven by the emotional connection consumers have with these items, along with the enduring value of precious metals and gemstones. This segment's share of the overall market is projected to remain substantial throughout the forecast period.

Key Segment (Application): Monobrand stores maintain their dominance in the market due to their focus on delivering an exclusive and immersive brand experience, which resonates particularly strongly with high-net-worth individuals. However, the online segment is expected to experience substantial growth, expanding access to a wider customer base and increasing convenience. Department stores and specialty stores will maintain relevance as crucial channels, providing curated collections and offering specialized customer service.

The Asia-Pacific region's dominance is attributed to several factors: rising disposable incomes, a burgeoning affluent middle class, increasing urbanization, and a cultural affinity for luxury goods. Within this region, China stands out as a key driver of growth due to its massive consumer base and the increasing sophistication of its luxury consumers. Meanwhile, the strong performance of the jewelry segment is rooted in its enduring appeal as a form of investment, self-expression, and cultural significance. The continued importance of monobrand stores reflects the desire for an exclusive and personalized shopping experience, while the growth of online sales demonstrates the evolving retail landscape and increased access to luxury products. The interplay between these regional and segment-specific dynamics will shape the hard luxury goods market's evolution in the coming years. The total production value of jewelry and other segments is expected to reach several billion dollars by 2033.

Several factors are catalyzing growth in the hard luxury goods industry. The rising disposable incomes globally, particularly in emerging markets, fuel demand for luxury items. Simultaneously, the growing awareness of luxury goods as valuable assets encourages investment, further driving market expansion. The increasing prevalence of online luxury retail, coupled with personalized shopping experiences, broadens market access and enhances customer engagement. Finally, brand loyalty, the enduring appeal of exclusivity, and ongoing innovation in design and technology create a robust foundation for sustained growth within the luxury sector.

This report provides a detailed analysis of the hard luxury goods market, encompassing historical data (2019-2024), an estimated year (2025), and a forecast period (2025-2033). It covers key market trends, driving forces, challenges, and growth catalysts, alongside a comprehensive assessment of leading players and significant industry developments. The report offers insights into regional and segmental performance, enabling businesses to make informed strategic decisions within this dynamic market. It provides actionable intelligence for investors, brands, and retailers seeking to understand and capitalize on the opportunities within the luxury sector. The data points presented, including production figures in millions of units, offer a robust quantitative and qualitative foundation for strategic planning.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Graff Diamonds Ltd., LVMH, Giorgio Armani, Swatch Group, Richemont, Bulgari, Chanel S.A., Ralph Lauren Corp., Tiffany & Co., Harry Wintson.

The market segments include Type, Application.

The market size is estimated to be USD 84330 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Hard Luxury Goods," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Hard Luxury Goods, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.