1. What is the projected Compound Annual Growth Rate (CAGR) of the GaN Semiconductor Device?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

GaN Semiconductor Device

GaN Semiconductor DeviceGaN Semiconductor Device by Type (GaN RF Devices, GaN Power Devices, World GaN Semiconductor Device Production ), by Application (Telecom & Datacom, Consumer Electronics, Industrial, Automotive & Mobility, Military, Defense & Aerospace, Energy, Others, World GaN Semiconductor Device Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

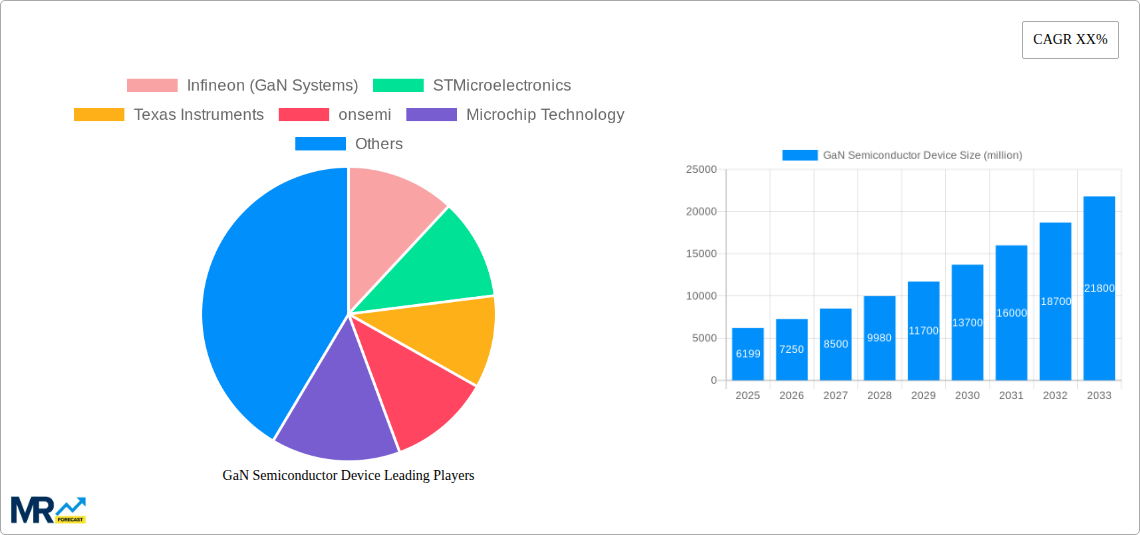

The global Gallium Nitride (GaN) semiconductor device market is poised for significant expansion, projected to reach an estimated market size of $6,199 million by 2025. This robust growth is fueled by the increasing demand for high-performance, energy-efficient electronic components across a multitude of sectors. GaN technology's inherent advantages, such as higher power density, faster switching speeds, and superior thermal performance compared to traditional silicon-based semiconductors, are driving its adoption. Key market drivers include the burgeoning 5G infrastructure rollout, the rapid evolution of consumer electronics like smartphones and laptops, and the growing electrification of the automotive industry, particularly in electric vehicles (EVs) and advanced driver-assistance systems (ADAS). Furthermore, the imperative for energy efficiency in industrial applications and the continued advancements in military and aerospace technology are solidifying GaN's position as a critical enabling technology. The market's trajectory is further supported by ongoing research and development efforts leading to innovative GaN solutions and expanded production capabilities worldwide.

The GaN semiconductor device market is segmented into GaN RF devices and GaN power devices, catering to diverse applications including telecom & datacom, consumer electronics, industrial, automotive & mobility, military, defense & aerospace, and energy. The telecom sector, with its relentless pursuit of higher bandwidth and lower latency for 5G and future wireless generations, represents a major growth avenue. In the consumer electronics space, GaN is revolutionizing power adapters, chargers, and audio amplifiers, offering smaller, lighter, and more efficient solutions. The automotive sector's demand for efficient power management in EVs, alongside the need for advanced radar and communication systems, is a substantial growth catalyst. Despite the promising outlook, the market faces some restraints, including the relatively higher cost of GaN materials and manufacturing processes compared to silicon, as well as the need for specialized design and handling expertise. However, as production scales and technological maturity increases, these challenges are expected to diminish, paving the way for even broader market penetration.

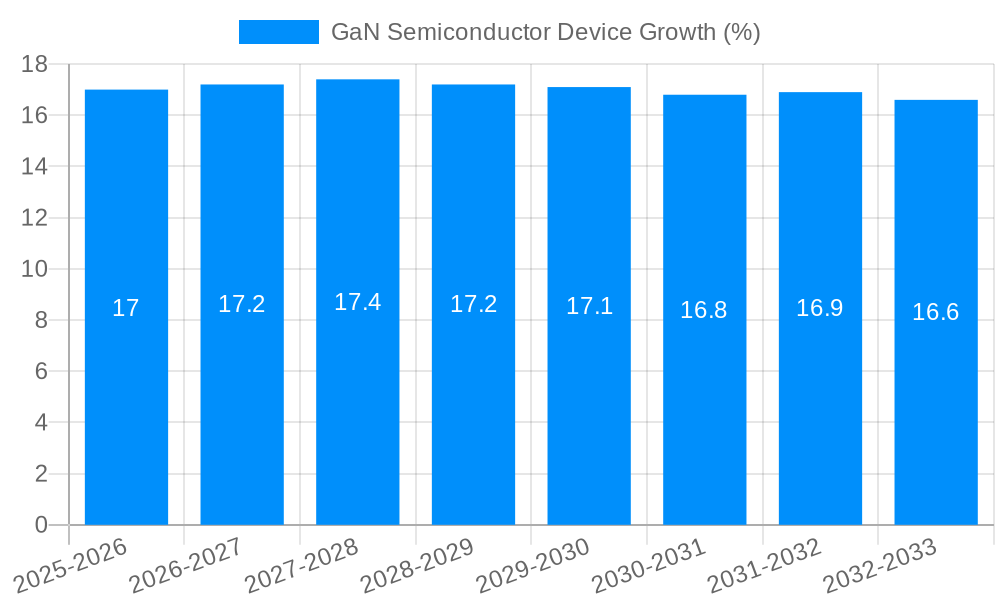

XXX The Gallium Nitride (GaN) semiconductor device market is poised for exponential growth, driven by an insatiable demand for higher efficiency, faster switching speeds, and reduced form factors across a myriad of applications. The historical period from 2019 to 2024 witnessed a foundational phase for GaN adoption, with early innovators paving the way for broader market penetration. As we enter the base year of 2025, the market stands at a critical juncture, with production scaling up to meet escalating demand. The estimated year of 2025 will likely see significant milestones in manufacturing capacity expansion, particularly for GaN Power Devices, which are increasingly supplanting silicon-based solutions in power conversion applications like electric vehicles, renewable energy inverters, and high-efficiency power supplies for consumer electronics and datacenters. The study period extending to 2033, with a forecast period from 2025-2033, suggests a sustained upward trajectory, characterized by rapid technological advancements and the emergence of new application frontiers. The global GaN semiconductor device production, a key indicator of market health, is expected to surge, potentially reaching tens of millions of units annually by the end of the forecast period. This surge will be fueled by both established semiconductor giants and agile startups, all vying for a share of this lucrative market. GaN RF devices, while historically dominant in niche applications like radar and telecommunications, are also experiencing a renaissance, driven by the rollout of 5G and the increasing need for higher frequency operations in advanced wireless systems. The interplay between GaN RF and GaN Power devices will define the market's evolution, with synergistic advancements leading to more integrated and powerful solutions. The increasing focus on energy efficiency and sustainability across all sectors will continue to be a paramount driver, placing GaN at the forefront of next-generation semiconductor technology. The market's segmentation by application is expected to see significant shifts, with Automotive & Mobility and Telecom & Datacom emerging as major growth engines, followed closely by Industrial and Consumer Electronics. The ability of GaN to handle higher power densities and operate at higher frequencies makes it indispensable for these demanding applications. The World GaN Semiconductor Device Production figures will be closely watched as a barometer of market maturity and the successful scaling of manufacturing processes.

The GaN semiconductor device market is propelled by a potent confluence of technological superiority and evolving market demands. Foremost among these is the inherent performance advantage of GaN over traditional silicon. GaN materials possess a significantly higher bandgap, allowing them to operate at higher voltages and frequencies with greater efficiency. This translates directly into smaller, lighter, and more power-efficient electronic devices. The insatiable global appetite for energy efficiency, driven by environmental concerns and rising energy costs, makes GaN an indispensable technology for reducing energy consumption in everything from data centers to electric vehicles. Furthermore, the relentless pursuit of miniaturization across consumer electronics, such as smartphones, laptops, and wearables, necessitates components that can deliver high performance in compact form factors, a niche where GaN excels. The ongoing rollout of 5G and the anticipated advent of 6G technologies are creating unprecedented demand for high-frequency RF components capable of supporting faster data transmission and lower latency, a domain where GaN RF devices are uniquely positioned. The burgeoning electric vehicle market, with its stringent requirements for high-power density and efficient charging systems, is a significant catalyst, as is the expansion of renewable energy infrastructure, which relies heavily on efficient power conversion for solar and wind energy systems. The increasing adoption of GaN in industrial applications, from motor drives to power supplies, further solidifies its growth trajectory.

Despite its immense promise, the GaN semiconductor device market faces several hurdles that could temper its growth. The primary challenge remains the higher manufacturing cost associated with GaN compared to mature silicon-based technologies. While production volumes are increasing, the complex fabrication processes and specialized equipment required for GaN epitaxy and device manufacturing contribute to elevated costs, making it a premium option in some price-sensitive applications. Supply chain complexities and capacity constraints also pose a significant restraint. As demand outpaces current production capabilities, lead times can extend, and ensuring a stable and robust supply chain for critical raw materials and substrates is crucial. Design and integration challenges for engineers accustomed to silicon-based designs can also slow adoption. Implementing GaN devices often requires a deeper understanding of their unique characteristics and the development of new circuit topologies and thermal management strategies. Reliability and long-term performance concerns, though diminishing with technological advancements and increased field experience, can still be a factor for some critical applications where extreme robustness is paramount. Furthermore, the lack of standardization in certain areas of GaN device packaging and testing can create interoperability issues and add to design complexity. Finally, while GaN's performance advantages are clear, the inertia of established silicon-based ecosystems and the significant investment already made in silicon infrastructure can create resistance to rapid widespread adoption in some segments.

The global GaN semiconductor device market is characterized by a dynamic interplay of regional manufacturing strengths and segment-specific demand. GaN Power Devices are poised to dominate the market landscape, both in terms of production volume and revenue, across the study period of 2019-2033. This dominance is intrinsically linked to the burgeoning applications in Automotive & Mobility and Industrial sectors. The escalating demand for electric vehicles (EVs) is a prime driver, with GaN power devices enabling more efficient onboard chargers, DC-DC converters, and motor drives, thereby increasing EV range and reducing charging times. The industrial sector's continuous drive for energy efficiency in motor control systems, power supplies for automation equipment, and renewable energy integration further bolsters the demand for GaN power solutions.

Key Regions & Countries:

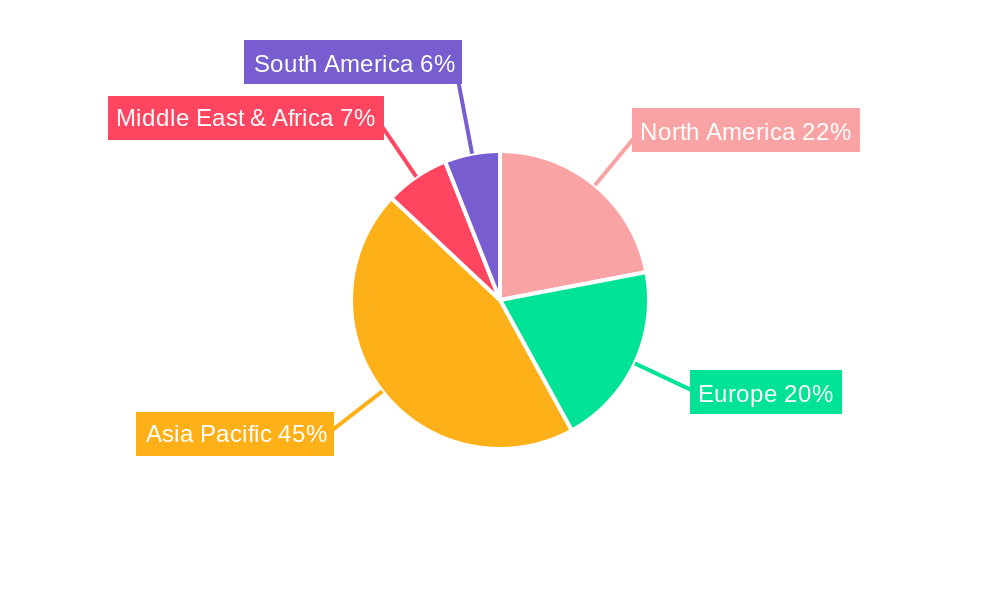

Asia Pacific: This region is expected to emerge as the dominant force in both production and consumption of GaN semiconductor devices. China, in particular, is rapidly scaling its GaN manufacturing capabilities, driven by significant government support and a burgeoning domestic demand across various sectors. South Korea and Japan are also key players, with established semiconductor giants investing heavily in GaN technology and its applications, especially in consumer electronics and advanced communications. The region's robust manufacturing ecosystem and its pivotal role in global electronics supply chains position it for sustained leadership.

North America: While not always the primary manufacturing hub, North America is a significant consumption market, particularly for high-end applications in Telecom & Datacom and Military, Defense & Aerospace. The presence of leading technology companies and research institutions fosters innovation and adoption of cutting-edge GaN solutions for 5G infrastructure, advanced radar systems, and satellite communications. Wolfspeed, Inc., a major GaN wafer and device manufacturer, is headquartered in the US, underscoring the region's importance in the supply chain.

Europe: Europe is also a critical market, with strong emphasis on sustainable energy solutions and automotive advancements. The region is a significant consumer of GaN power devices for EVs, renewable energy inverters, and industrial automation. Germany, with its strong automotive and industrial base, is a key contributor to European demand.

Dominant Segments:

GaN Power Devices: As highlighted, these devices will lead the market. Their superior efficiency, higher power density, and faster switching capabilities make them ideal for:

Telecom & Datacom: This segment will also witness substantial growth, primarily driven by GaN RF devices:

World GaN Semiconductor Device Production: The overall production volume will be a testament to the market's maturity. By 2025, we anticipate production in the tens of millions of units, with a significant portion dedicated to power applications. The forecast period to 2033 suggests a compound annual growth rate that will push this figure into the hundreds of millions. This scaling will be crucial for meeting the demand across all application segments.

The synergistic growth of GaN Power Devices and the increasing demand in the Automotive & Mobility and Industrial sectors, coupled with the robust manufacturing capabilities in the Asia Pacific region, will collectively define the dominant forces shaping the GaN semiconductor device market in the coming years.

The GaN semiconductor device industry is fueled by powerful catalysts. The increasing global demand for energy efficiency, driven by environmental regulations and rising energy costs, makes GaN's superior performance a compelling choice. The rapid expansion of electric vehicle adoption and the need for faster charging and longer ranges directly translate into a surging demand for GaN power components. Furthermore, the ongoing rollout of 5G and the development of future wireless technologies are creating a significant need for high-frequency, high-power GaN RF devices. Continued investment in R&D by leading players, coupled with advancements in manufacturing techniques, is steadily reducing costs and improving reliability, further accelerating market adoption across diverse applications.

This comprehensive report provides an in-depth analysis of the global GaN semiconductor device market, spanning the study period of 2019-2033, with a base year of 2025 and a forecast period from 2025-2033. It delves into the intricate trends, driving forces, and challenges shaping the industry. The report meticulously examines key regions and segments expected to dominate the market, offering detailed insights into the World GaN Semiconductor Device Production figures and industry developments. It identifies growth catalysts and presents a comprehensive overview of the leading players. This report is an essential resource for stakeholders seeking to understand the transformative impact of GaN technology on various industries and to capitalize on the immense growth opportunities within this rapidly evolving market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Infineon (GaN Systems), STMicroelectronics, Texas Instruments, onsemi, Microchip Technology, Rohm, NXP Semiconductors, Toshiba, Innoscience, Wolfspeed, Inc, Renesas Electronics (Transphorm), Sumitomo Electric Device Innovations (SEDI) (SCIOCS), Alpha and Omega Semiconductor Limited (AOS), Nexperia, Epistar Corp., Qorvo, Navitas Semiconductor, Power Integrations, Inc., Efficient Power Conversion Corporation (EPC), MACOM, VisIC Technologies, Cambridge GaN Devices (CGD), Wise Integration, RFHIC Corporation, Ampleon, GaNext, Chengdu DanXi Technology, Southchip Semiconductor Technology, Panasonic, Toyoda Gosei, China Resources Microelectronics Limited, CorEnergy, Dynax Semiconductor, Sanan Optoelectronics, Hangzhou Silan Microelectronics, Guangdong ZIENER Technology, CETC 13, CETC 55, Qingdao Cohenius Microelectronics, Youjia Technology (Suzhou) Co., Ltd, Nanjing Xinkansen Technology, GaNPower, CloudSemi, Shenzhen Taigao Technology.

The market segments include Type, Application.

The market size is estimated to be USD 6199 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "GaN Semiconductor Device," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the GaN Semiconductor Device, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.