1. What is the projected Compound Annual Growth Rate (CAGR) of the Fuel Cell Electric Vehicle Passenger Vehicle?

The projected CAGR is approximately 25.4%.

Fuel Cell Electric Vehicle Passenger Vehicle

Fuel Cell Electric Vehicle Passenger VehicleFuel Cell Electric Vehicle Passenger Vehicle by Type (With 2 Hydrogen Tanker, With 3 Hydrogen Tanker, World Fuel Cell Electric Vehicle Passenger Vehicle Production ), by Application (For Sales, For Public Lease, World Fuel Cell Electric Vehicle Passenger Vehicle Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

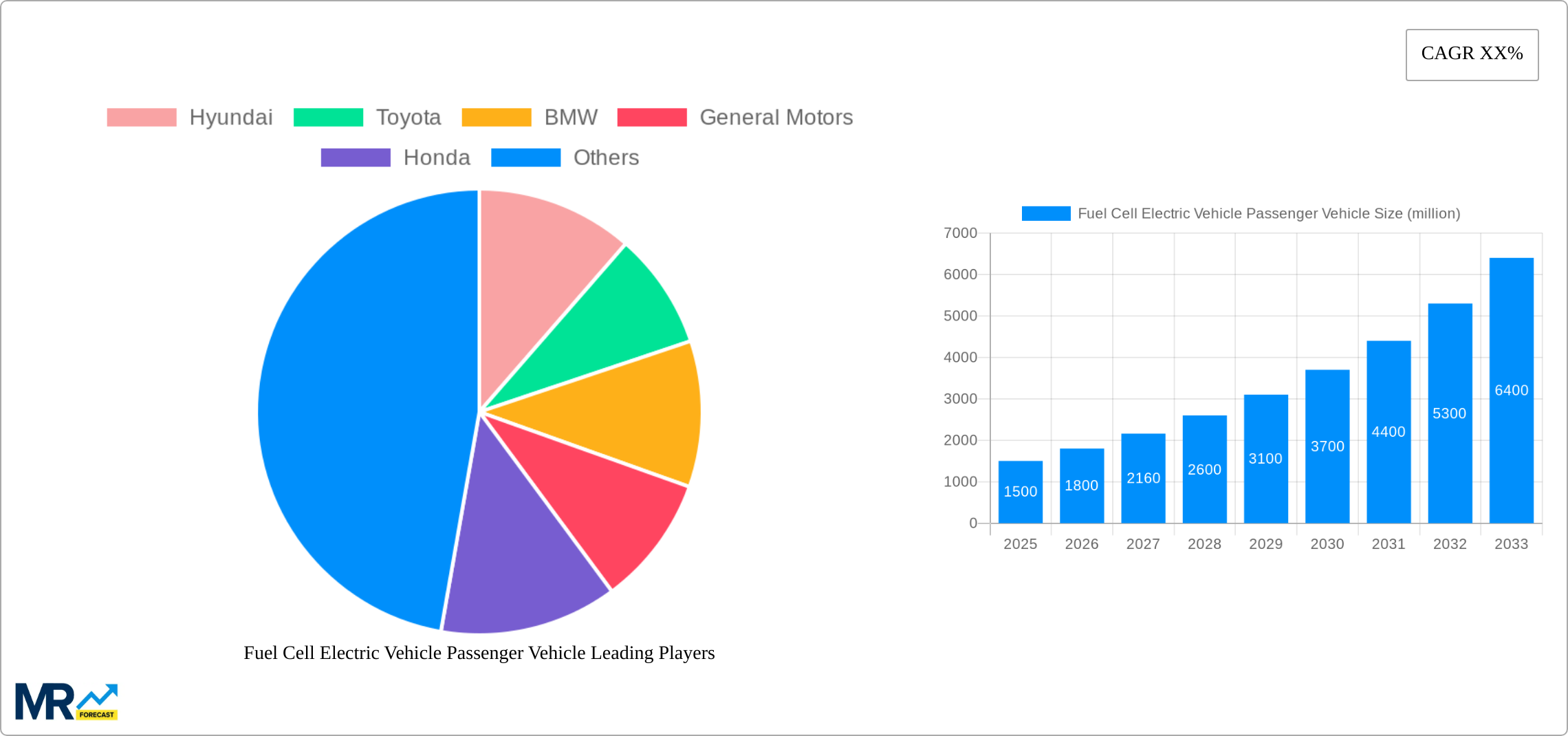

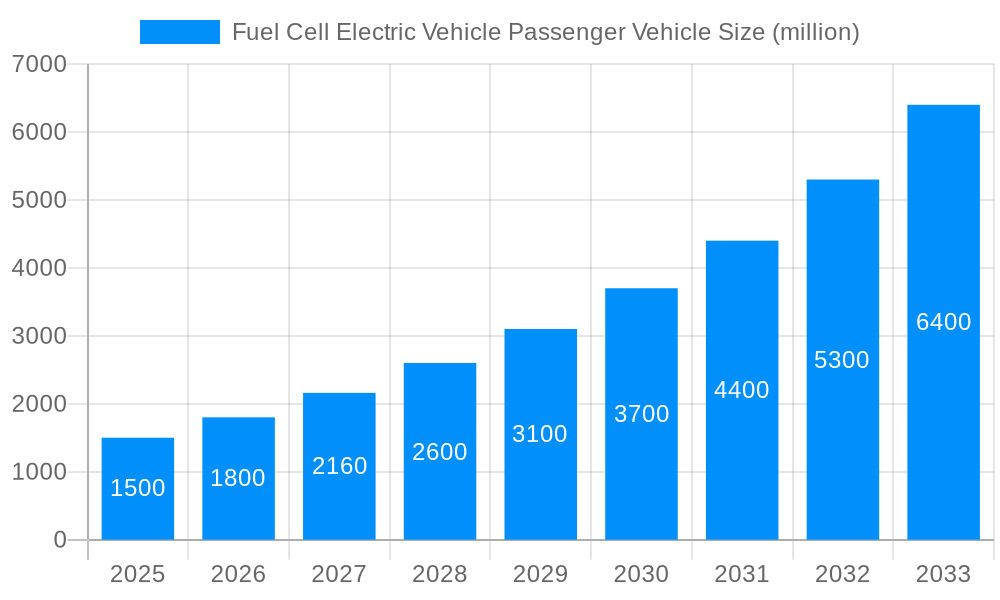

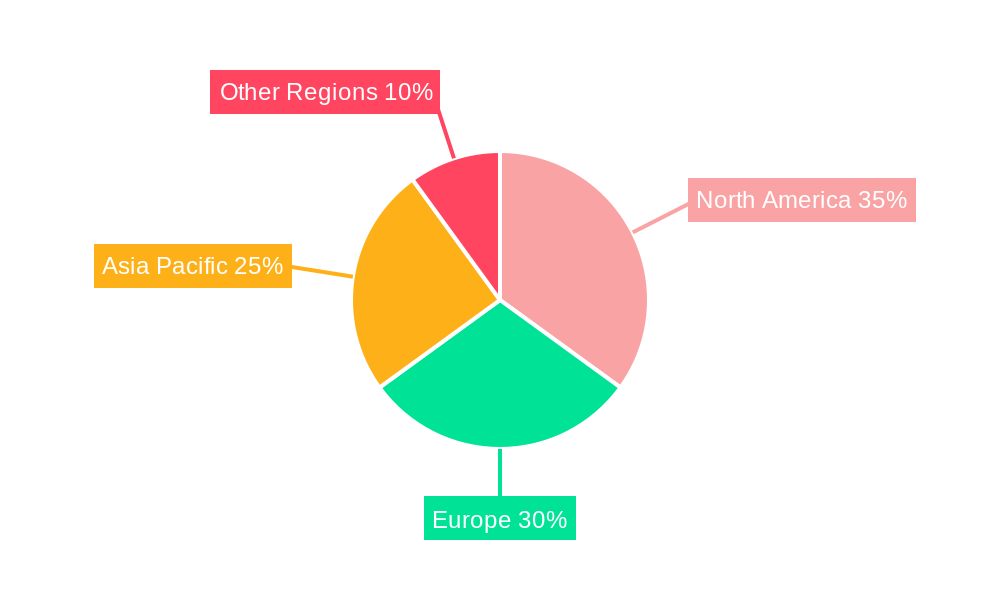

The Fuel Cell Electric Vehicle (FCEV) passenger vehicle market is projected for robust expansion, driven by escalating environmental concerns and stringent global emission regulations. Despite its current niche status, significant investments from leading automotive manufacturers are fostering innovation and accelerating production. Market growth is further supported by advancements in fuel cell technology, leading to enhanced efficiency, extended range, and reduced costs. The segment of FCEVs featuring three hydrogen tanks is anticipated to outpace the two-tank segment, offering extended range capabilities that align with consumer demand for longer travel distances between refueling. The "for sales" application segment currently dominates the market share over "for public lease," indicating early market development and a preference for ownership. However, the expansion of leasing options and subscription models is expected to increase the "for public lease" segment's share in the coming years. Geographically, market concentration is observed in developed regions like North America, Europe, and Asia Pacific, primarily due to substantial governmental support, mature automotive industries, and higher consumer purchasing power. Key challenges include the limited hydrogen refueling infrastructure and the relatively high initial cost of FCEVs compared to Battery Electric Vehicles (BEVs). Nonetheless, continuous technological progress and supportive government policies are poised to address these obstacles, ensuring significant market growth throughout the forecast period (2025-2033). The global Fuel Cell Electric Vehicle (FCEV) passenger vehicle market is estimated to reach 525.2 million by 2024, with a projected Compound Annual Growth Rate (CAGR) of 25.4%.

The forecast period from 2025 to 2033 is expected to witness a transformative shift in the FCEV passenger vehicle sector. Intensified competition among key industry players will stimulate innovative product development and drive price reductions. Strategic alliances between automotive manufacturers and hydrogen infrastructure developers will be critical for accelerating market penetration. Emphasis will increasingly be placed on enhancing the overall user experience, including faster refueling times and greater availability of hydrogen refueling stations. Furthermore, advancements in battery technology and the integration of fuel cell and battery systems (hybrid approaches) are expected to bolster the competitiveness of FCEVs. The emergence of new markets in developing economies, fueled by government incentives and growing environmental consciousness, will contribute to sustained market growth. Regional disparities will persist, influenced by variations in economic development, regulatory frameworks, and hydrogen infrastructure accessibility. A strong focus on sustainable manufacturing processes and the lifecycle management of FCEVs will gain prominence as the market matures.

The global fuel cell electric vehicle (FCEV) passenger vehicle market is poised for significant growth, transitioning from a niche sector to a more prominent player in the broader automotive landscape. The study period (2019-2033), encompassing historical (2019-2024), base (2025), and estimated/forecast periods (2025-2033), reveals a compelling narrative of increasing adoption. While the base year of 2025 shows a relatively modest production volume, projected figures for 2033 indicate a dramatic surge in the millions of units produced and sold, reflecting the growing market acceptance and technological advancements in FCEV technology. This growth is fueled by several factors, including increasing concerns about climate change and air quality, prompting a shift towards cleaner transportation solutions. Governments worldwide are implementing supportive policies such as subsidies, tax breaks, and infrastructure development, further accelerating market expansion. The availability of hydrogen refueling infrastructure, although still limited in many regions, is expanding steadily, addressing a key barrier to FCEV adoption. Moreover, automakers are continuously improving FCEV performance, enhancing range and reducing costs, making these vehicles increasingly competitive with traditional internal combustion engine (ICE) vehicles and even battery electric vehicles (BEVs) in specific applications. Key market players like Toyota, Hyundai, and Honda are spearheading innovation and production, driving competition and technological advancements. However, challenges remain, including the high initial cost of FCEV vehicles, the limited availability of hydrogen refueling stations, and the energy intensity of hydrogen production. Overcoming these obstacles will be crucial to ensuring the sustained and widespread adoption of FCEV passenger vehicles in the coming years. The market is segmented by the number of hydrogen tanks (two or three), application (sales or public lease), and geographic region, each presenting unique growth trajectories influenced by factors like government regulations, consumer preferences, and the cost of hydrogen production and distribution. This report delves into these complexities and projections, offering a nuanced perspective on the FCEV passenger vehicle market's potential. The millions of units produced and sold will likely be significantly impacted by the rate of hydrogen infrastructure deployment and cost reduction strategies for both vehicle manufacturing and hydrogen production.

Several key factors are propelling the growth of the FCEV passenger vehicle market. Firstly, the escalating global concern over climate change and air pollution is pushing governments and consumers towards cleaner transportation alternatives. FCEVs, with their zero tailpipe emissions, offer a compelling solution. Secondly, supportive government policies, including subsidies, tax incentives, and investments in hydrogen refueling infrastructure, are playing a crucial role in stimulating market demand and making FCEVs more financially accessible. Thirdly, continuous technological advancements are leading to improvements in FCEV performance, such as increased range, faster refueling times, and reduced costs. This makes them increasingly competitive with traditional gasoline-powered vehicles and even BEVs, particularly for long-distance travel or heavy-duty applications. Moreover, the growing awareness among consumers about the environmental benefits of FCEVs is driving their adoption. Furthermore, the increasing collaboration between automakers and energy companies is crucial in developing a robust hydrogen infrastructure needed to support the widespread adoption of FCEVs. This collaboration is not only streamlining the refueling process but also ensuring a reliable and sustainable supply of hydrogen fuel. Finally, the strategic investments made by major automotive companies in research and development are pushing technological breakthroughs and accelerating the market's overall growth trajectory. These investments aim to reduce production costs, improve vehicle efficiency, and expand the range of available models.

Despite the positive growth trajectory, several challenges hinder the widespread adoption of FCEV passenger vehicles. The high initial purchase price of FCEVs compared to conventional vehicles remains a significant barrier for many consumers. The limited availability of hydrogen refueling infrastructure, particularly outside major metropolitan areas, restricts the practical usage of FCEVs and poses a "range anxiety" similar to that faced by early adopters of BEVs. The energy intensity of hydrogen production is also a concern, particularly if not sourced from renewable energy sources. This can negate some of the environmental benefits of FCEVs if the hydrogen production process itself is carbon-intensive. Furthermore, the technological complexities associated with FCEV production and maintenance contribute to higher manufacturing costs. This complexity also leads to a higher barrier to entry for smaller automotive companies looking to compete in this sector. In addition, consumer awareness and understanding of FCEV technology and its benefits are still limited in many parts of the world, hindering faster market penetration. Finally, competition from battery electric vehicles (BEVs), which are experiencing rapid technological advancements and cost reductions, presents a further challenge to the FCEV sector's growth. Addressing these challenges through government support, technological innovation, and strategic investments in infrastructure is vital for the sustainable growth of the FCEV passenger vehicle market.

The FCEV passenger vehicle market is expected to witness diverse regional growth patterns. While several regions show promising potential, some key areas are anticipated to lead the market:

Japan: Japan has been a pioneer in FCEV technology and enjoys a well-established domestic hydrogen infrastructure, leading to substantial growth in domestic sales and production.

South Korea: Similar to Japan, South Korea has significantly invested in both FCEV technology and hydrogen infrastructure, creating a strong foundation for market dominance within its borders.

Europe: Several European nations are actively promoting the adoption of FCEVs through supportive policies and investments in hydrogen infrastructure, positioning them for substantial growth.

China: China's large automotive market and commitment to reducing emissions positions the country for significant growth in FCEV sales and production, although the timeline for widespread adoption may be slightly longer than in Japan or South Korea.

North America (specifically California): The presence of supportive regulatory environments in areas like California, with their strong focus on zero-emission vehicles, makes the region a potential growth area, though still in the early stages compared to Asia.

Dominating Segment: Application - For Sales: The "For Sales" segment is projected to hold a larger market share than the "For Public Lease" segment. While leasing programs can introduce consumers to the technology, outright sales are anticipated to be the primary driver of volume growth due to wider consumer choice and potential resale value appreciation. However, public lease programs could become increasingly important as a means of expanding FCEV use in public transportation fleets and government-owned vehicles.

Dominating Segment: Type - With 2 Hydrogen Tanker: While both the "With 2 Hydrogen Tanker" and "With 3 Hydrogen Tanker" segments will grow, the "With 2 Hydrogen Tanker" segment is expected to hold a greater market share, mainly due to potentially lower vehicle production costs and reasonable range for many daily-use cases. Three-tank vehicles offer increased range but at a higher manufacturing and operating cost, making them more of a niche segment for very long-distance or heavy-duty applications, at least in the near term.

In summary: While diverse regional growth is expected, Japan and South Korea are likely to lead in early stages of market penetration, driven by mature technology and infrastructure. The "For Sales" application segment will likely outpace "For Public Lease" in the coming decade, and the two-hydrogen-tanker vehicle type is likely to maintain a larger market share than the three-tank version due to cost-effectiveness. However, the balance could shift with technological advancements and changes in hydrogen infrastructure availability across various regions.

Several factors act as catalysts for the growth of the FCEV industry. The development of more efficient and cost-effective hydrogen production methods, utilizing renewable energy sources, is crucial. Simultaneous expansion of hydrogen refueling infrastructure, especially in regions beyond major cities, will encourage greater consumer confidence and adoption. Furthermore, ongoing advancements in FCEV technology, resulting in enhanced vehicle performance, longer ranges, and reduced production costs, are all vital to attracting a broader market. These elements combined will drive greater consumer awareness and acceptance of FCEVs, fostering more rapid market growth and broader acceptance.

This report provides a comprehensive overview of the FCEV passenger vehicle market, encompassing historical data, current market dynamics, and future projections. It details key market trends, driving forces, challenges, and opportunities, providing in-depth analysis of market segmentation by vehicle type, application, and geography. The report also profiles leading players in the industry, analyzing their strategies and competitive landscape, and identifies key growth catalysts driving the market's expansion. The detailed forecast to 2033 offers a valuable resource for businesses, investors, and policymakers seeking insights into this rapidly evolving sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 25.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 25.4%.

Key companies in the market include Hyundai, Toyota, BMW, General Motors, Honda, China FAW Group, Ford, .

The market segments include Type, Application.

The market size is estimated to be USD 525.2 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Fuel Cell Electric Vehicle Passenger Vehicle," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Fuel Cell Electric Vehicle Passenger Vehicle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.