1. What is the projected Compound Annual Growth Rate (CAGR) of the Frozen Prepared Foods?

The projected CAGR is approximately 4.12%.

Frozen Prepared Foods

Frozen Prepared FoodsFrozen Prepared Foods by Application (Hypermarkets/Supermarkets, Specialist Retailers, Convenience Stores, Independent Retailers, Online Sales), by Type (Frozen Pizza, Meat Products, Fish and Seafood, Vegetables, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

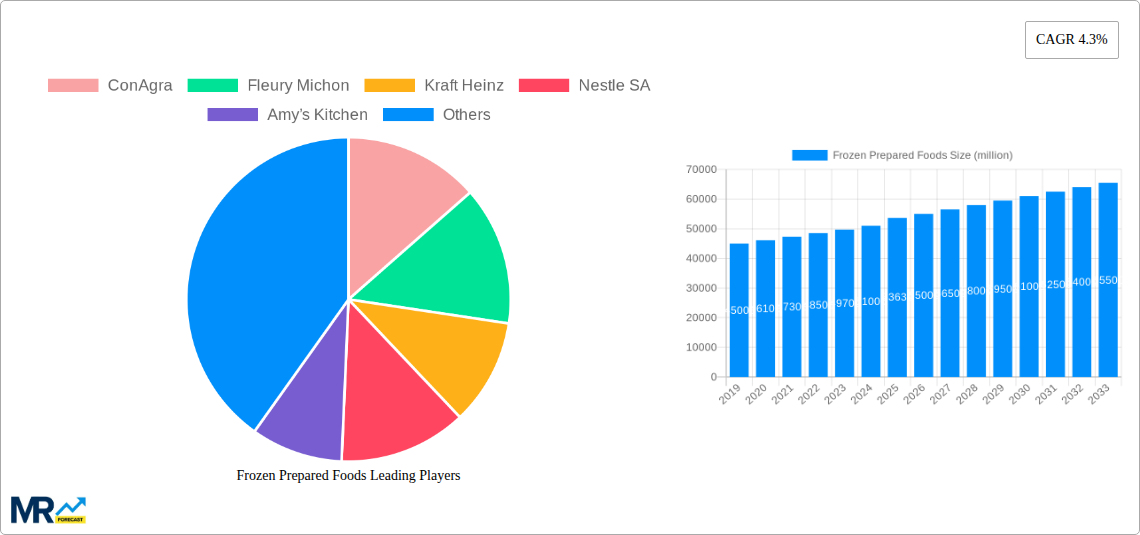

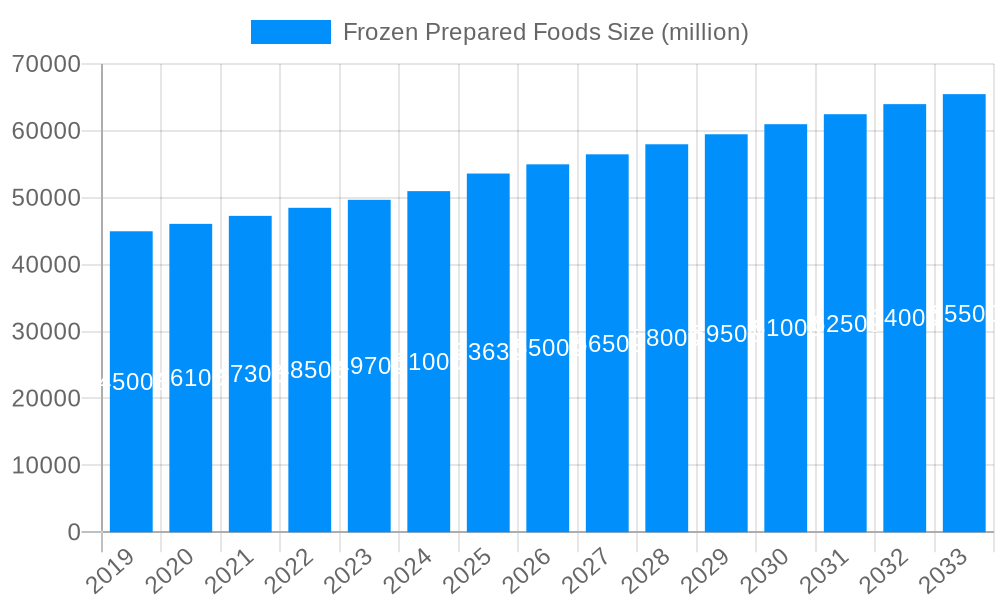

The global Frozen Prepared Foods market is projected to reach $335.58 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.12% from 2025 to 2033. This growth is driven by escalating consumer demand for convenient, ready-to-eat meal solutions, attributed to busy lifestyles, smaller household sizes, and a preference for time-saving options. Advancements in freezing technology, preserving freshness and nutritional value, further enhance consumer confidence and product appeal. Key distribution channels include hypermarkets and supermarkets, alongside the rapidly expanding online sales sector.

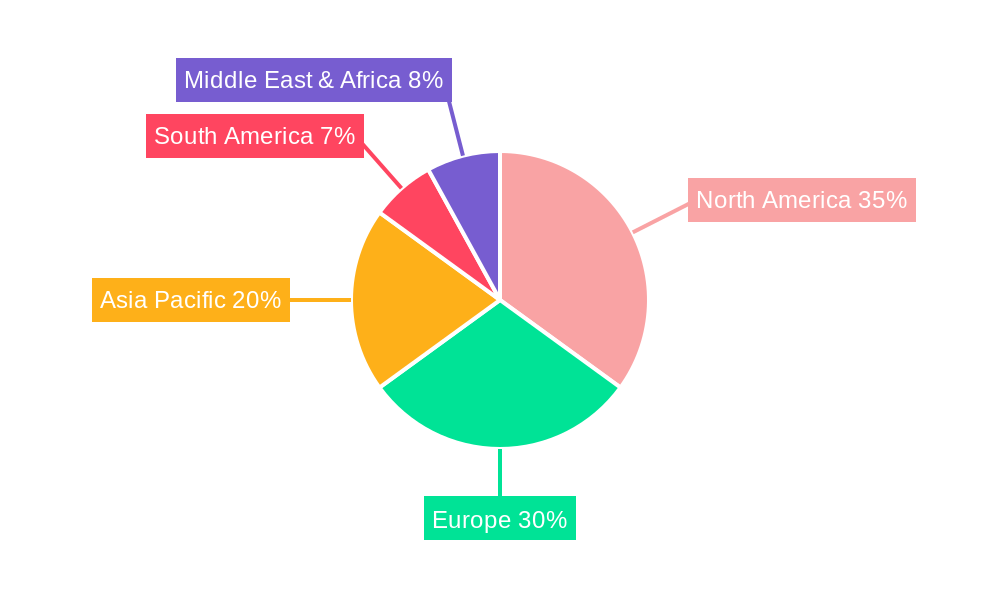

The sector is experiencing a significant demand for healthier options, including lean proteins, reduced sodium, and plant-based ingredients. Consumers are increasingly focused on natural and minimally processed foods, leading to product diversification in frozen seafood, vegetables, and specialized meat products. While demand and innovation are strong, market restraints include fluctuating raw material costs, potential consumer perceptions regarding freshness, and intense competition from major players. North America and Europe currently lead the market, with the Asia Pacific region poised for the fastest growth due to its expanding middle class and adoption of Western dietary habits.

This report provides an in-depth analysis of the global Frozen Prepared Foods market from 2025 to 2033, with a base year of 2025. The study meticulously examines historical trends from 2019-2024. Key industry participants including ConAgra, Fleury Michon, Kraft Heinz, Nestle SA, Amy’s Kitchen, General Mills, McCain Foods Ltd, Tyson Foods, Schwan's Company, Iceland Foods, and Maple Leaf Foods are analyzed. The market is segmented by application (Hypermarkets/Supermarkets, Specialist Retailers, Convenience Stores, Independent Retailers, Online Sales) and by product type (Frozen Pizza, Meat Products, Fish and Seafood, Vegetables, Others). Crucial industry developments are highlighted for a comprehensive market landscape overview.

XXX The global Frozen Prepared Foods market is currently experiencing a significant upswing, driven by evolving consumer lifestyles and an increasing demand for convenience without compromising on quality or taste. The historical period from 2019 to 2024 has witnessed a steady growth trajectory, laying a robust foundation for the projected expansion. As of the estimated year 2025, the market is poised for further acceleration, fueled by several key trends. One of the most prominent is the burgeoning interest in plant-based and healthier frozen meal options. Consumers are increasingly seeking out products with perceived health benefits, leading to a surge in demand for frozen meals featuring vegetables, lean proteins, and alternative protein sources like tofu and legumes. This trend is particularly evident in the "Vegetables" and "Others" categories, where innovative formulations are capturing significant market share. Furthermore, the rise of gourmet and premium frozen prepared foods is reshaping consumer perceptions. Gone are the days when frozen meals were synonymous with bland and basic. Today, brands are offering sophisticated flavor profiles, international cuisines, and higher-quality ingredients, appealing to a more discerning palate. This is boosting the "Others" segment, which often encompasses more specialized or international ready-to-eat frozen dishes. Online sales channels have also become a pivotal force, transforming the accessibility and purchase journey of frozen prepared foods. The convenience of ordering frozen meals for home delivery is a major draw, particularly for busy households and individuals. This has led to a substantial increase in the "Online Sales" application segment. The market is also seeing a greater emphasis on sustainable packaging and ethical sourcing, with consumers actively choosing brands that align with their values. This growing awareness is influencing product development and brand positioning across all segments, from "Meat Products" to "Fish and Seafood." The base year of 2025 marks a crucial point, as the market continues to adapt to post-pandemic consumer behaviors, which have solidified a preference for at-home dining solutions and convenient food preparation. The forecast period from 2025 to 2033 anticipates this momentum to continue, with further innovation in product development, broader adoption of healthy and sustainable options, and an expanding reach through diverse sales channels.

The frozen prepared foods market is being propelled by a confluence of powerful drivers that cater to the modern consumer's needs and desires. Foremost among these is the unwavering demand for convenience. The fast-paced nature of contemporary life leaves many individuals with limited time for meal preparation. Frozen prepared foods offer a swift and effortless solution, requiring minimal effort and time to cook, thereby freeing up valuable hours for other activities. This inherent convenience is a consistent and potent driver across all market segments. Complementing this is the evolving perception of frozen foods. Historically, frozen options were often associated with lower quality or less appealing taste. However, advancements in freezing technology and culinary innovation have led to a significant improvement in the quality, flavor, and nutritional profile of frozen prepared meals. Brands are now investing heavily in premium ingredients and sophisticated recipes, transforming frozen meals into desirable and satisfying dining experiences. This evolution is particularly evident in categories like frozen pizza and ready-to-eat meals, which are increasingly mimicking the quality of freshly prepared dishes. Furthermore, the growing awareness and emphasis on healthier eating habits are shaping the market. Consumers are actively seeking out frozen options that align with their health goals, leading to a rise in demand for meals that are lower in sodium, fat, and sugar, and higher in protein and fiber. This has spurred innovation in product development, with manufacturers introducing a wider array of plant-based, gluten-free, and organic frozen prepared foods.

Despite the robust growth, the frozen prepared foods market is not without its hurdles. A significant challenge lies in overcoming the lingering negative perceptions associated with frozen foods, particularly regarding taste, texture, and nutritional value. While advancements have been made, some consumers still harbor reservations, viewing frozen options as inferior to fresh alternatives. This requires continuous marketing efforts and product innovation to educate consumers and build trust. Another prominent restraint is the intense competition within the market. The presence of numerous established players and the continuous entry of new brands create a highly saturated landscape. This necessitates substantial investment in branding, marketing, and product differentiation to capture and retain consumer attention and market share. The fluctuating costs of raw materials, such as meat, poultry, seafood, and vegetables, also pose a considerable challenge. These price volatilities can impact production costs, leading to potential price increases for consumers and affecting profit margins for manufacturers. Furthermore, the cold chain logistics required for frozen prepared foods are complex and costly. Maintaining the integrity of the cold chain from production to consumption is paramount to ensure product quality and safety. Any breakdown in this chain can lead to spoilage and financial losses, making efficient and reliable logistics a critical operational challenge. Finally, regulatory scrutiny concerning food safety, labeling, and ingredients can also act as a restraint. Manufacturers must adhere to stringent regulations, which can add to production complexity and costs, particularly when introducing new product formulations or expanding into new geographical markets.

The Hypermarkets/Supermarkets application segment is poised to dominate the global Frozen Prepared Foods market throughout the forecast period, driven by their extensive reach, diverse product offerings, and established consumer trust. These large retail formats provide a one-stop shop for consumers, allowing them to conveniently purchase a wide array of frozen prepared meals alongside their regular groceries. The sheer volume of foot traffic and the strategic placement of frozen food aisles within these stores ensure consistent visibility and accessibility for a broad consumer base. For instance, in the estimated year 2025, hypermarkets and supermarkets are projected to account for over 45% of the total sales volume in millions of units.

Within the Type segment, Frozen Pizza is expected to remain a dominant force. Its universal appeal, versatility in toppings and crusts, and the continued innovation in gourmet and healthier alternatives have solidified its position. The ability to cater to diverse dietary preferences, such as gluten-free or vegan options, further amplifies its market appeal. In 2025, the Frozen Pizza segment alone is estimated to contribute approximately 20% of the total market value in millions of units, reflecting its consistent popularity.

Geographically, North America is anticipated to lead the market in terms of both value and volume. This dominance is attributed to several factors:

Furthermore, Europe is expected to be another significant contributor to the market. Factors driving growth in this region include:

The Online Sales application segment, while smaller in the historical period, is projected for substantial growth. The increasing adoption of e-commerce platforms for grocery shopping, particularly in the wake of recent global events, has made online purchasing of frozen foods more mainstream. This segment is expected to witness a compound annual growth rate (CAGR) significantly higher than traditional brick-and-mortar channels over the forecast period.

In summary, the synergy between established retail giants like hypermarkets/supermarkets, the enduring popularity of staples like frozen pizza, the strong purchasing power and lifestyle trends in North America and Europe, and the rapidly expanding online sales channels will collectively define the dominant forces shaping the Frozen Prepared Foods market.

The frozen prepared foods industry is experiencing accelerated growth due to several key catalysts. The persistent demand for convenience, driven by increasingly busy consumer lifestyles, remains a primary propellant. Furthermore, a heightened consumer focus on health and wellness is spurring innovation in the development of nutritious and wholesome frozen meal options, including plant-based and low-calorie alternatives. The expansion of online grocery shopping and efficient cold chain logistics are making frozen prepared foods more accessible than ever. Finally, advancements in freezing technology are enhancing the quality, taste, and texture of frozen products, effectively dismantling historical negative perceptions.

This report delves into the intricate dynamics of the global Frozen Prepared Foods market, meticulously analyzing trends, driving forces, and challenges from 2019 to 2033. It provides a forward-looking perspective based on a base year of 2025, with estimations and forecasts designed to equip stakeholders with critical market intelligence. The report's comprehensive scope encompasses key industry players, detailed segmentation by application and product type, and an in-depth examination of significant industry developments, offering a holistic view for strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.12% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.12%.

Key companies in the market include ConAgra, Fleury Michon, Kraft Heinz, Nestle SA, Amy’s Kitchen, General Mills, McCain Foods Ltd, Tyson Foods, Schwan's Company, Iceland Foods, Maple Leaf Foods, .

The market segments include Application, Type.

The market size is estimated to be USD 335.58 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Frozen Prepared Foods," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Frozen Prepared Foods, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.