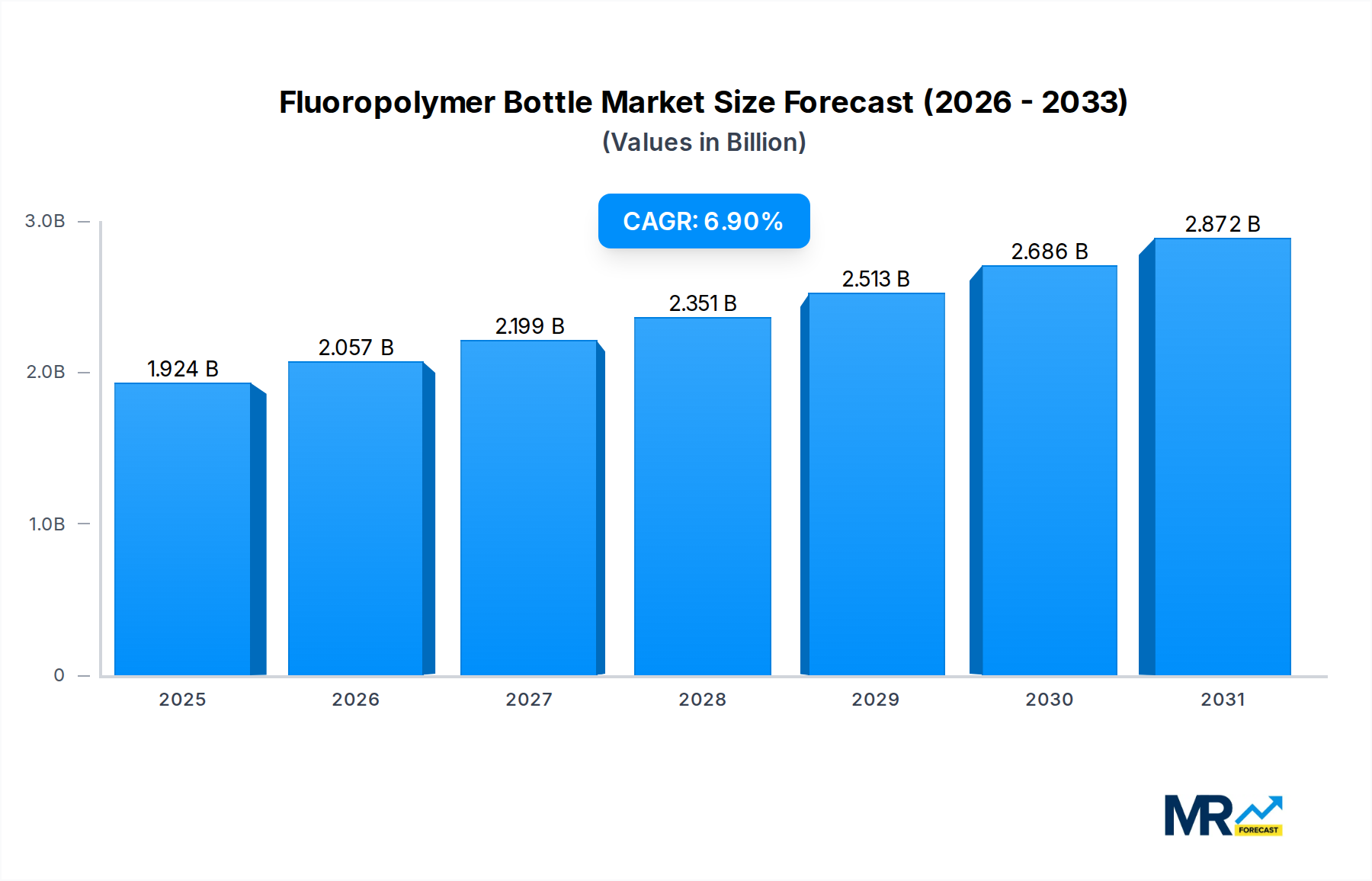

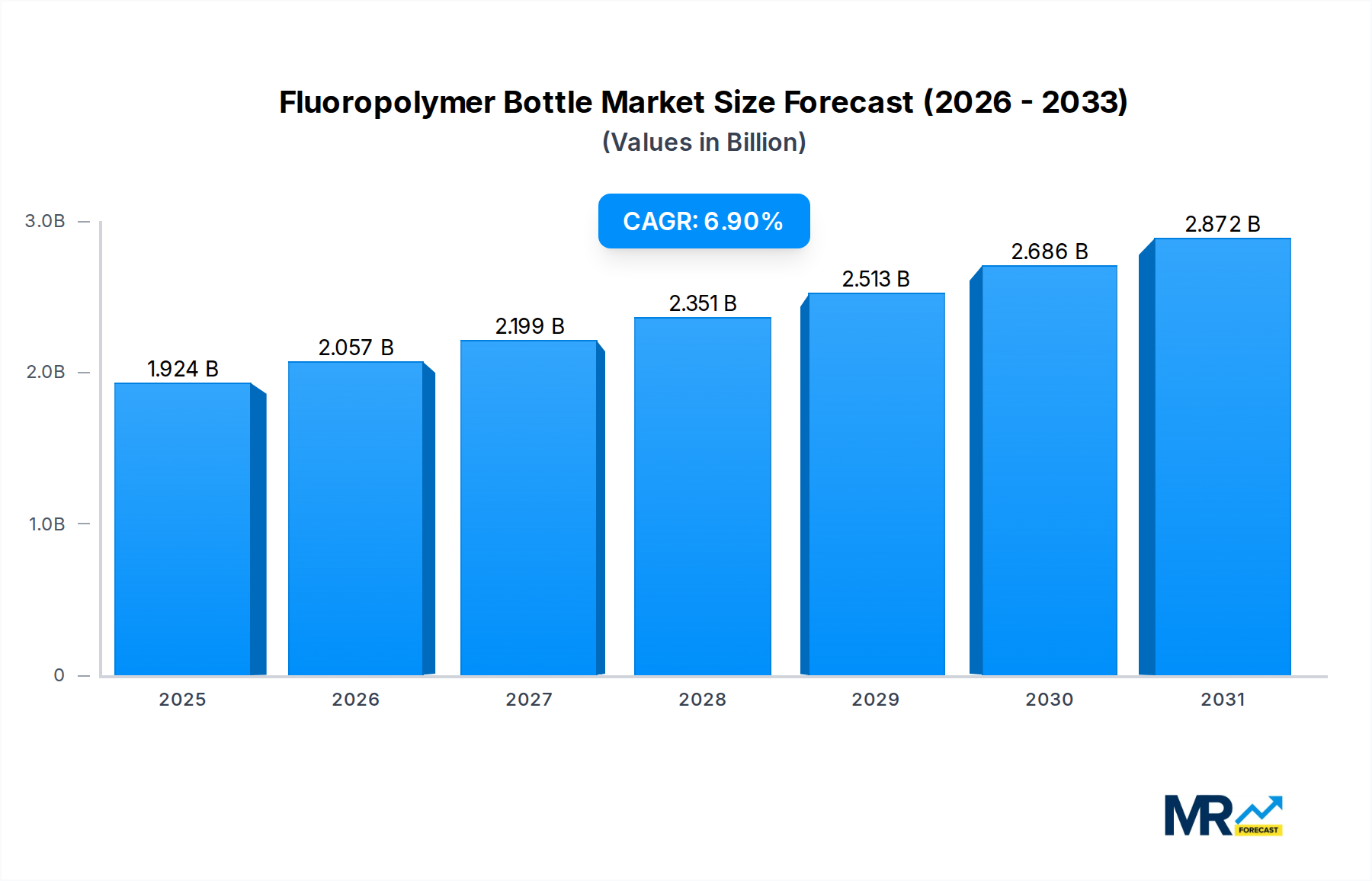

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fluoropolymer Bottle?

The projected CAGR is approximately 6.9%.

Fluoropolymer Bottle

Fluoropolymer BottleFluoropolymer Bottle by Material Type (PTFE (Polytetrafluoroethylene), PFA (Perfluoroalkoxy), FEP (Fluorinated Ethylene Propylene), ETFE (Ethylene Tetrafluoroethylene), PVDF (Polyvinylidene Fluoride), PCTFE (Polychlorotrifluoroethylene), ECTFE (Ethylene Chlorotrifluoroethylene)), by Size (100 ml, 250 ml, 500 ml, 1L, 2L, Others), by End User Industry (Chemical Industry, Pharmaceutical Industry, Biotechnology Companies, Research & Academic Laboratories, Others), by Distribution Channel (Direct Sales, Distributors & Wholesalers, Online), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The Fluoropolymer Bottle Market is demonstrating robust expansion, valued at an estimated $1.8 billion in 2025. Projections indicate a substantial increase, reaching approximately $3.06 billion by 2033, propelled by a Compound Annual Growth Rate (CAGR) of 6.9% during the forecast period. This growth trajectory is primarily underpinned by the increasing demand for ultra-pure and chemically inert containment solutions across critical industries.

Key demand drivers include the escalating stringency of regulatory standards within the pharmaceutical and biotechnology sectors, necessitating containers with minimal extractables and leachables. The Pharmaceutical Packaging Market and the Biopharmaceutical Packaging Market, in particular, are pivotal end-use segments, driving innovation in fluoropolymer bottle design and material science. Furthermore, the burgeoning semiconductor industry and other advanced materials sectors contribute significantly to the demand for the High Purity Chemical Packaging Market, where contamination control is paramount. The inherent properties of fluoropolymers such as PTFE (Polytetrafluoroethylene), PFA (Perfluoroalkoxy), and FEP (Fluorinated Ethylene Propylene)—including exceptional chemical resistance, thermal stability, and low surface energy—make them indispensable for handling corrosive reagents, sensitive biological samples, and high-purity chemicals.

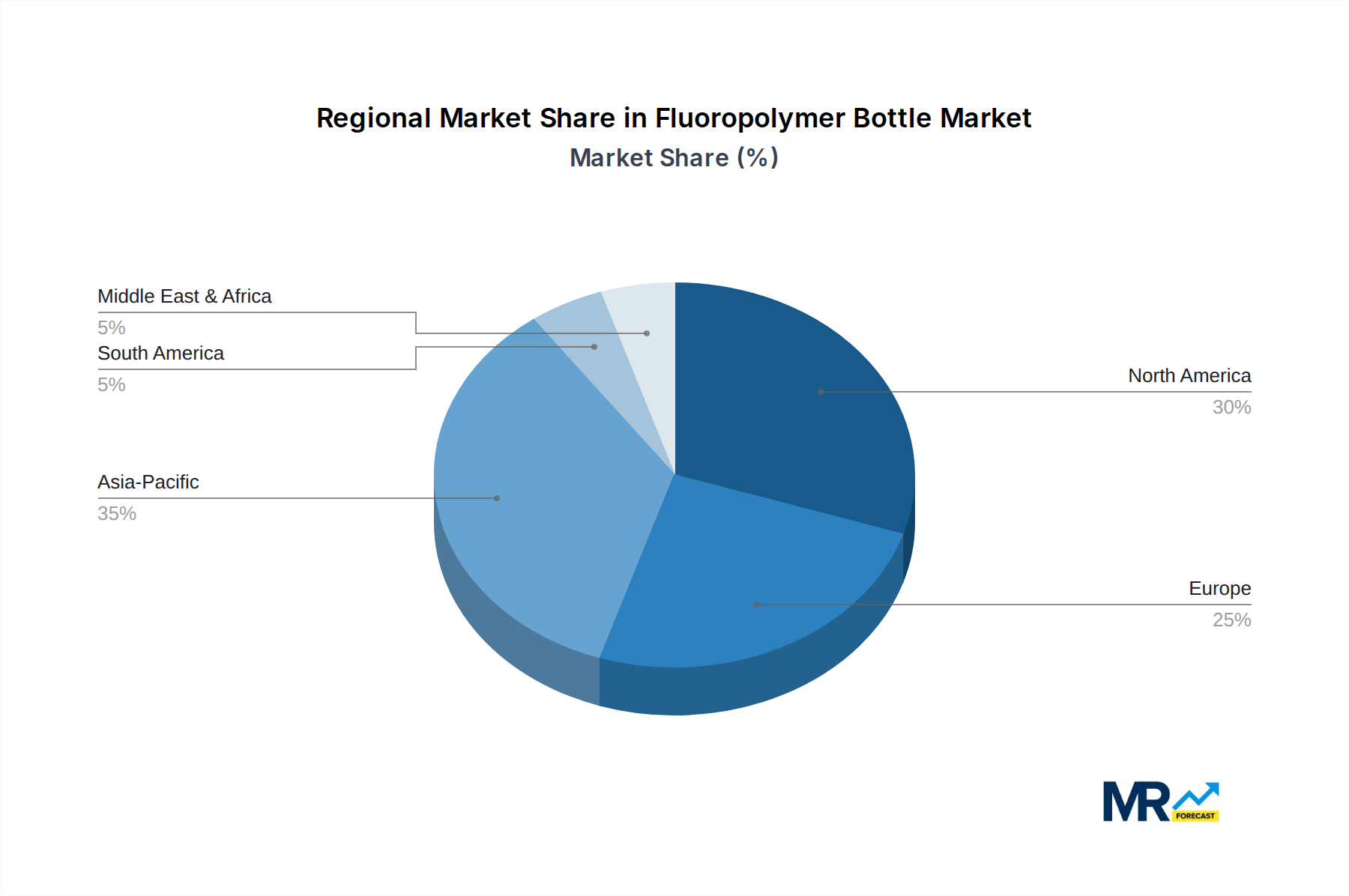

Technological advancements in polymer processing and manufacturing techniques are enhancing the purity and performance characteristics of fluoropolymer bottles, further solidifying their market position. While North America and Europe currently hold significant market shares due to established research infrastructure and strict regulatory frameworks, the Asia Pacific region is anticipated to exhibit the fastest growth, driven by rapid industrialization, expanding healthcare expenditure, and increasing investments in scientific research and manufacturing capabilities. The market also sees opportunities arising from the Laboratory Consumables Market where research institutions and academic laboratories increasingly require reliable and inert storage solutions for their diverse applications. The broader Advanced Polymers Market continues to innovate, leading to enhanced material formulations that offer even greater chemical compatibility and operational longevity for fluoropolymer bottles. The market's resilience against chemical attack positions it strongly within the overall Chemical Storage Market, particularly for hazardous materials.

Within the Fluoropolymer Bottle Market, the 'Material Type' segment stands as a critical differentiator and a primary driver of market dynamics, with PFA (Perfluoroalkoxy) emerging as the dominant sub-segment. PFA fluoropolymer bottles command a significant share due to their superior combination of chemical inertness, high purity, thermal stability, and optical clarity, making them indispensable for the most demanding applications. Unlike PTFE, which is opaque, PFA offers translucency, allowing for visual inspection of contents, a crucial advantage in many laboratory and industrial settings. This characteristic, combined with its resistance to nearly all chemicals, including strong acids, bases, and organic solvents, positions PFA as the material of choice for the High Purity Chemical Packaging Market.

The widespread adoption of PFA bottles stems from their extremely low levels of extractable and leachable compounds, ensuring the integrity of stored reagents, sensitive pharmaceuticals, and biological samples. This property is particularly vital for segments like the Pharmaceutical Packaging Market and Biopharmaceutical Packaging Market, where regulatory compliance (e.g., USP <665>) mandates minimal interaction between the container and its contents. Manufacturers such as Savillex Corporation and Entegris, Inc. are prominent players leveraging PFA's attributes to produce ultra-high purity bottles designed for these critical applications. The smooth, non-porous surface of PFA also minimizes particle shedding and microbial adhesion, further enhancing its appeal for sterile and contamination-sensitive environments within the Laboratory Consumables Market.

While other fluoropolymers like PTFE, FEP (Fluorinated Ethylene Propylene), PVDF (Polyvinylidene Fluoride), and ETFE (Ethylene Tetrafluoroethylene) also serve specific niches within the Fluoropolymer Bottle Market, PFA consistently outranks them in applications requiring the highest level of chemical purity and thermal performance. FEP, for instance, offers good chemical resistance and translucency but generally has a lower maximum operating temperature than PFA. PTFE boasts excellent chemical resistance but its opaque nature and more challenging processing often limit its use for bottles requiring visual content monitoring. PVDF, while cost-effective and chemically resistant, does not match PFA's ultra-high purity profile or temperature tolerance. The ongoing trend towards miniaturization in research and diagnostics, coupled with the increasing complexity of chemical and biological formulations, continues to solidify PFA's dominant position, driving its share growth within the overall Specialty Packaging Market. The sustained demand for high-performance fluoropolymer bottles ensures PFA remains a cornerstone of the market's material landscape, with its properties proving crucial for advanced scientific and industrial applications.

The Fluoropolymer Bottle Market is primarily driven by an confluence of stringent regulatory requirements and the escalating need for high-performance containment solutions across critical industries. A significant driver is the increasing demand from the Pharmaceutical Packaging Market and Biopharmaceutical Packaging Market. These sectors face rigorous global standards, such as those from the FDA and EMA, regarding the inertness and non-reactivity of packaging materials. Fluoropolymer bottles, particularly those made from PFA or PTFE, offer unparalleled chemical resistance and extremely low extractables, directly addressing concerns about drug stability and patient safety. For example, recent updates to pharmacopeial guidelines, like USP <665> on plastic components and systems used in pharmaceutical manufacturing, underscore the necessity for materials that do not leach harmful substances, thereby driving adoption in this high-value segment.

Another crucial impetus comes from the High Purity Chemical Packaging Market, especially in the semiconductor and electronics industries. The production of microchips and other advanced electronic components requires ultra-pure chemicals, acids, and solvents that must be stored without any contamination. Fluoropolymer bottles prevent ion leaching and particle generation, which are common issues with traditional glass or polyethylene containers. The growth of the global semiconductor industry, projected to expand by an estimated 7-9% annually in terms of sales, directly translates to increased demand for specialized packaging solutions that maintain chemical purity throughout the supply chain.

The expanding scope of research and development activities globally also fuels the Laboratory Consumables Market. Academic institutions, government research labs, and private R&D centers rely on fluoropolymer bottles for storing sensitive reagents, corrosive samples, and precious compounds. Their inertness ensures experimental integrity and prevents degradation of valuable materials. This growing scientific endeavor necessitates reliable, contamination-free storage, which fluoropolymer bottles uniquely provide. Furthermore, the inherent superior chemical resistance positions these bottles as critical components in the broader Chemical Storage Market, particularly for hazardous and highly reactive industrial chemicals, reducing risks of container degradation and leakage. The ongoing innovation in the Fluoropolymer Resins Market also ensures a steady supply of advanced materials, directly supporting the expansion and diversification of fluoropolymer bottle applications.

The Fluoropolymer Bottle Market is characterized by the presence of several specialized manufacturers offering high-performance solutions for demanding applications. These companies differentiate themselves through material expertise, product innovation, and adherence to stringent industry standards:

The Fluoropolymer Bottle Market exhibits distinct regional dynamics driven by varying industrial landscapes, regulatory frameworks, and research expenditures. Globally, North America and Europe currently represent significant revenue shares due to their mature pharmaceutical, biotechnology, and semiconductor industries, coupled with stringent quality control standards. North America, characterized by its robust research and development infrastructure and a large base of pharmaceutical and biopharmaceutical companies, shows consistent demand for high-purity fluoropolymer bottles. The primary demand driver here is the sustained investment in drug discovery and manufacturing, coupled with strict regulatory oversight, particularly for the Biopharmaceutical Packaging Market.

Europe, another established market, benefits from a strong chemical industry and advanced scientific research. Countries like Germany, France, and the UK are at the forefront of chemical and pharmaceutical innovation, propelling the need for inert packaging. The demand in Europe is largely driven by its strong emphasis on environmental and health regulations, which favor chemically resistant and stable containers for hazardous substances and pharmaceutical products. The Chemical Storage Market for various industrial and specialty chemicals remains a core application.

However, the Asia Pacific region is projected to be the fastest-growing market for fluoropolymer bottles during the forecast period. This growth is attributable to rapid industrialization, escalating healthcare expenditure, burgeoning electronics manufacturing, and increasing foreign direct investment in research and development centers across countries like China, India, Japan, and South Korea. The expansion of the High Purity Chemical Packaging Market in the semiconductor and electronics sectors, alongside the burgeoning Pharmaceutical Packaging Market due to a large patient pool and growing contract manufacturing, are the key demand drivers. The region's increasing focus on advanced materials and specialty chemicals also fuels the demand for these high-performance bottles.

The Middle East & Africa and South America regions also present growth opportunities, albeit at a slower pace compared to Asia Pacific. In these regions, the primary demand stems from the expanding chemical and oil & gas sectors (for corrosive fluid handling) and developing pharmaceutical industries. While these regions currently hold smaller market shares, investments in industrial infrastructure and healthcare modernization are expected to gradually increase the adoption of fluoropolymer bottles, contributing to the global Specialty Packaging Market landscape.

The Fluoropolymer Bottle Market is highly dependent on a specialized and complex upstream supply chain, primarily centered around the availability and pricing of specific fluoropolymer resins. Key raw materials include PTFE (Polytetrafluoroethylene), PFA (Perfluoroalkoxy), FEP (Fluorinated Ethylene Propylene), and PVDF (Polyvinylidene Fluoride). The production of these resins begins with the mining of fluorspar, a critical mineral, which is then processed into hydrofluoric acid (HF). HF serves as a foundational building block for various fluoromonomers (such as tetrafluoroethylene, hexafluoropropylene, and vinylidene fluoride), which are subsequently polymerized into the final fluoropolymer resins.

Upstream dependencies create inherent sourcing risks. The global supply of fluorspar is concentrated, with China being the dominant producer, making the market susceptible to geopolitical shifts, trade policies, and export restrictions. This concentration can lead to price volatility, directly impacting the cost structure of fluoropolymer bottle manufacturers. Energy costs for polymerization processes are also a significant factor, as these are energy-intensive operations. Historically, fluctuations in global energy prices have directly translated into elevated costs within the Fluoropolymer Resins Market, subsequently affecting the pricing of finished bottles.

Supply chain disruptions, such as those experienced during the global pandemic or due to natural disasters affecting key production regions, have demonstrated the market's vulnerability. Lead times for specialized resins can extend significantly, impacting manufacturing schedules and the ability to meet demand from critical end-user industries like the Pharmaceutical Packaging Market and the semiconductor sector. Manufacturers often maintain strategic inventories or diversify their resin suppliers to mitigate these risks. The general trend for fluoropolymer resin prices has been upward over the past few years, driven by increasing global demand for high-performance materials in diverse applications, coupled with rising raw material and energy costs, and growing environmental compliance expenses for fluorochemical production. This upward pressure on raw material costs necessitates continuous optimization in manufacturing processes and strategic sourcing for players in the Fluoropolymer Bottle Market.

The Fluoropolymer Bottle Market is increasingly under scrutiny from sustainability and Environmental, Social, and Governance (ESG) perspectives, prompting manufacturers to re-evaluate product lifecycle and operational practices. The core challenge stems from the broader fluorochemical industry's association with PFAS (per- and polyfluoroalkyl substances), often dubbed "forever chemicals." Although solid fluoropolymers like PTFE and PFA used in bottles are stable and largely non-leaching, the manufacturing processes for their precursors can involve PFAS compounds, leading to regulatory pressures and public perception issues. Regulatory bodies in regions like Europe and North America are actively developing and implementing restrictions on certain PFAS substances, which could influence future raw material sourcing for the Fluoropolymer Resins Market.

In response, manufacturers are focusing on mitigating environmental footprints. This includes efforts to reduce energy consumption during production, minimize waste generation, and ensure responsible management of any byproduct streams. Carbon footprint reduction targets are becoming integral to corporate strategies, pushing for greater efficiency and potentially the adoption of renewable energy sources in manufacturing facilities. While recycling fluoropolymers can be challenging due to their high performance characteristics and specialized compositions, the emphasis in the Fluoropolymer Bottle Market is shifting towards promoting extended product longevity and reusability, particularly in Laboratory Consumables Market and industrial settings. This "circular economy" approach aims to maximize the value and lifespan of existing materials rather than frequent disposal.

ESG investor criteria are also playing a pivotal role, compelling companies to demonstrate transparency in their supply chains and environmental performance. Companies are investing in cleaner production technologies and exploring alternatives or improved processes for fluoromonomer synthesis to minimize environmental impact. The drive towards more sustainable packaging solutions, even within high-performance segments, is undeniable. For instance, developing bottles with higher recycled content (where feasible and without compromising purity), or designing products for easier re-processing at end-of-life, represents areas of future innovation. These pressures are reshaping procurement decisions, fostering a preference for suppliers who can demonstrate clear commitments to sustainability and responsible manufacturing within the Advanced Polymers Market and the broader Plastics Packaging Market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.9%.

Key companies in the market include Savillex Corporation, Saint-Gobain Performance Plastics, Thermo Fisher Scientific, DWK Life Sciences, Nalgene (Thermo Fisher Scientific), AMETEK Fluoropolymer Products, Entegris, Inc., NICHIAS Corporation, Zeus Industrial Products, Inc., Fluorotherm Polymers, Inc., Chang Zhou Feng Di Plastic Technology, AGC Chemicals Americas, Daikin Industries Ltd., Others.

The market segments include Material Type, Size, End User Industry, Distribution Channel.

The market size is estimated to be USD 1.8 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Fluoropolymer Bottle," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Fluoropolymer Bottle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.