1. What is the projected Compound Annual Growth Rate (CAGR) of the Cookware Clad Metal?

The projected CAGR is approximately 3.4%.

Cookware Clad Metal

Cookware Clad MetalCookware Clad Metal by Type (Double-layer Composite Material, Three-layer Composite Material, Multi-layer Composite Material, World Cookware Clad Metal Production ), by Application (Wok, Soup/Milk Pot, Steamer, Pressure Cooker, Frying Pan/Frying Pan, Ceramic Pot/Casserole, World Cookware Clad Metal Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

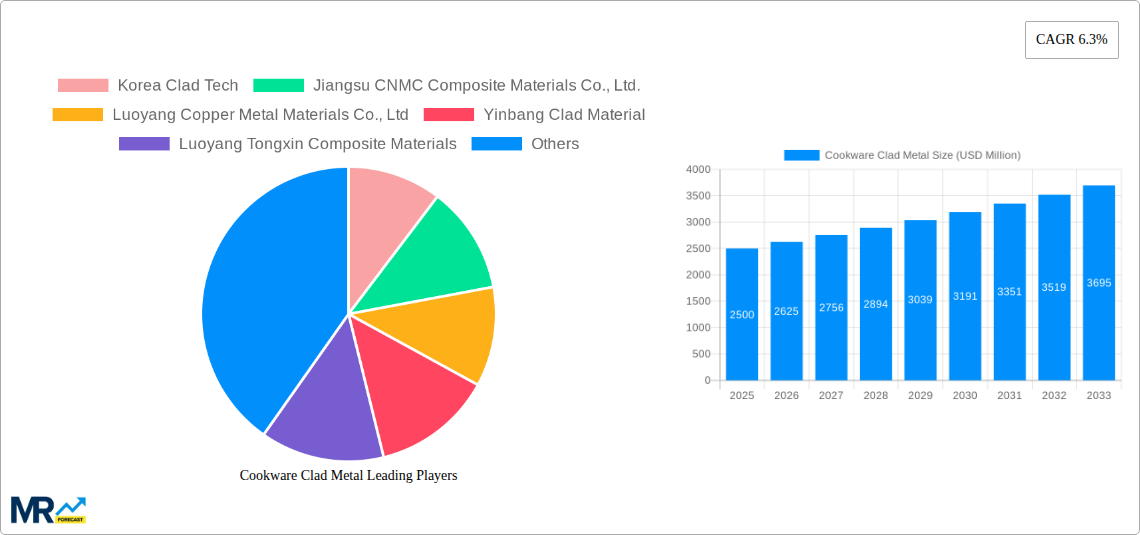

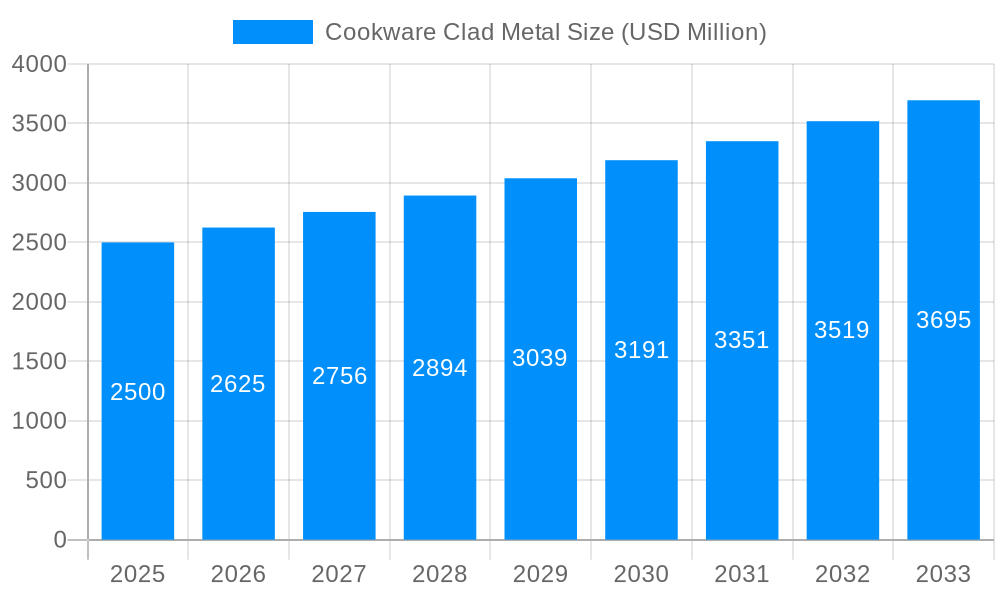

The global Cookware Clad Metal market is poised for substantial growth, projected to reach approximately $2.5 billion in 2025. This expansion is fueled by a Compound Annual Growth Rate (CAGR) of around 5%, indicating a robust and sustained upward trajectory. The demand for high-performance cookware, characterized by superior heat distribution and durability, is a primary driver. Consumers are increasingly prioritizing quality and longevity in their kitchenware, leading to a greater preference for clad metal constructions over traditional materials. The rising disposable incomes in emerging economies further contribute to this demand, as consumers invest in premium kitchen appliances and tools. Key applications driving this growth include frying pans, soup/milk pots, and woks, where the benefits of clad metal are most pronounced. Innovations in material science and manufacturing processes are also contributing to market expansion, offering enhanced performance and aesthetic appeal in clad metal cookware.

The market is segmented by type into Double-layer, Three-layer, and Multi-layer Composite Materials, with multi-layer variants gaining traction due to their advanced performance characteristics. Geographically, the Asia Pacific region, particularly China and India, is emerging as a significant growth engine, owing to a rapidly expanding middle class and increasing adoption of modern kitchen technologies. Europe and North America remain mature yet strong markets, driven by established consumer preferences for high-quality cookware. Restraints such as the higher cost of clad metal compared to some alternative materials and the presence of established traditional cookware manufacturers are present but are increasingly being offset by the perceived value and performance benefits. Key industry players like Korea Clad Tech, Jiangsu CNMC Composite Materials Co., Ltd., and Luoyang Copper Metal Materials Co., Ltd. are actively investing in research and development to cater to evolving consumer needs and technological advancements.

Here's a unique report description for Cookware Clad Metal, incorporating your specified elements:

The global cookware clad metal market is poised for substantial expansion, demonstrating a robust CAGR during the study period of 2019-2033. This upward trajectory is underpinned by several critical market insights that paint a picture of sustained growth and evolving consumer preferences. In the historical period of 2019-2024, the market witnessed steady adoption, fueled by a growing awareness of the superior heat distribution and durability offered by clad metal cookware. As we move into the base year of 2025 and the subsequent estimated year of 2025, the market is projected to reach a valuation in the billions, reflecting significant investment and consumer demand. The forecast period of 2025-2033 anticipates this momentum to accelerate, driven by both established markets and emerging economies.

Consumer desire for high-performance kitchenware that enhances cooking experiences is a primary trend. Clad metal, with its layered construction, typically comprising stainless steel with a core of aluminum or copper, offers unparalleled heat conductivity, responsiveness, and longevity. This translates to more even cooking, reduced hot spots, and a more enjoyable culinary process. The aesthetic appeal of clad metal cookware, often characterized by its sleek, professional look, also contributes to its desirability, aligning with modern kitchen design trends. Furthermore, the increasing prevalence of home cooking, a trend amplified during and post the pandemic, continues to bolster demand for quality cookware. This has led to a greater appreciation for materials that offer both functionality and a premium feel. The market is also seeing a diversification in product offerings, with manufacturers innovating to meet specific cooking needs across various applications, from everyday frying pans to specialized pots for slow cooking or steaming. The industry is observing a growing emphasis on sustainable manufacturing practices and material sourcing, which will also shape consumer choices and brand loyalty in the years to come. The overall market narrative is one of increasing sophistication in both product development and consumer expectations, leading to a dynamic and growing sector within the broader cookware industry.

The global cookware clad metal market is experiencing significant growth, propelled by a confluence of powerful driving forces. At the forefront is the escalating demand for premium and high-performance kitchenware. Consumers are increasingly prioritizing quality, durability, and superior cooking functionality, recognizing that clad metal cookware offers distinct advantages over single-material alternatives. The excellent heat conductivity and even distribution provided by the layered construction, typically featuring stainless steel with an aluminum or copper core, translate to more precise cooking control and better culinary results, thus enhancing the user experience. This pursuit of culinary excellence is a major impetus for the market's expansion.

Furthermore, the growing global middle class and rising disposable incomes, particularly in emerging economies, are enabling more consumers to invest in higher-quality kitchen appliances and cookware. This demographic shift translates into a larger addressable market for clad metal products. The increasing popularity of home cooking, often inspired by culinary shows and social media, has also amplified the desire for professional-grade equipment, further benefiting the clad metal segment. Manufacturers are also playing a crucial role by investing in research and development to innovate and offer a wider range of clad metal products tailored to specific cooking applications and consumer needs, thereby broadening the market's appeal and accessibility. The inherent longevity and resilience of clad metal cookware also contribute to its value proposition, appealing to consumers seeking durable investments rather than frequent replacements.

Despite its promising growth trajectory, the global cookware clad metal market faces several challenges and restraints that could potentially impede its full expansion. A primary hurdle is the higher price point associated with clad metal cookware compared to its aluminum or stainless steel counterparts. This premium pricing can be a deterrent for budget-conscious consumers, limiting market penetration in price-sensitive regions or segments. The manufacturing process for clad metals is also more complex, requiring specialized techniques and equipment, which contributes to the elevated costs.

Another significant restraint is the availability of substitute materials and cookware types. While clad metal offers superior performance, other materials like cast iron, ceramic, and advanced non-stick coatings provide viable alternatives that cater to different consumer preferences and price points. The market must continually emphasize the unique benefits of clad metal to justify its cost against these competitors. Furthermore, consumer education and awareness remain crucial. While awareness is growing, a segment of consumers may not fully comprehend the technical advantages of clad metal or its long-term value proposition, potentially opting for more familiar or cheaper options.

The volatile raw material prices, particularly for metals like aluminum and copper, can also impact the cost-effectiveness of clad metal production, leading to fluctuations in end-product pricing and potentially affecting profit margins for manufacturers. Finally, intense competition within the broader cookware market, with numerous established and emerging brands vying for market share, adds another layer of challenge. Companies must continuously innovate and differentiate their offerings to stand out in this crowded landscape.

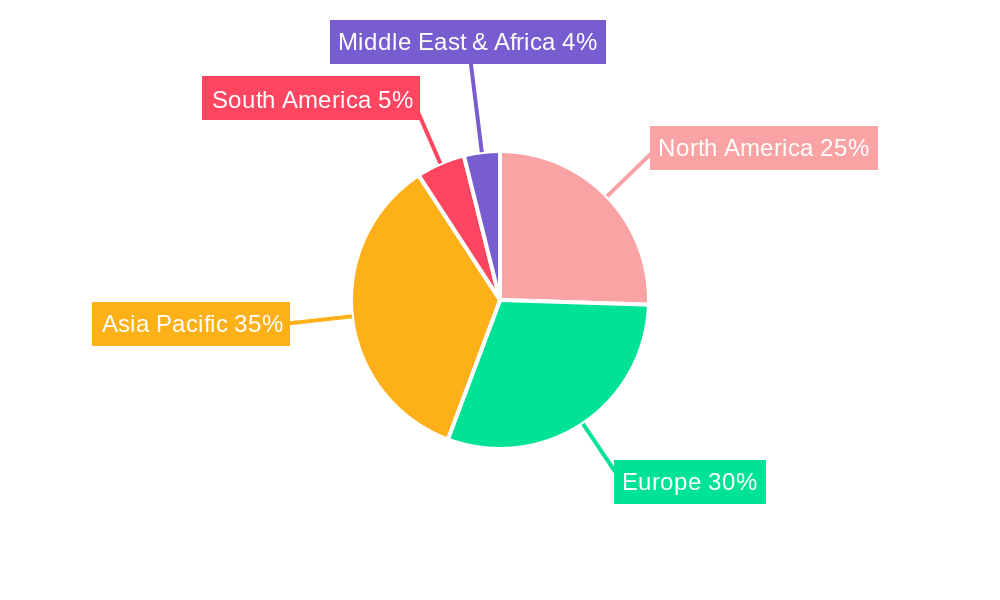

The global cookware clad metal market exhibits significant regional and segmental dominance, driven by a combination of economic factors, consumer preferences, and manufacturing capabilities.

Dominant Segments:

Multi-layer Composite Material: This segment is poised to lead the market, particularly during the forecast period of 2025-2033. Multi-layer clad metals, often featuring three or more distinct metal layers (e.g., stainless steel-aluminum-stainless steel, or stainless steel-copper-stainless steel), offer the most optimized blend of heat conductivity, responsiveness, and durability. This superior performance makes them the preferred choice for premium cookware lines, appealing to both professional chefs and discerning home cooks. The increasing emphasis on culinary precision and the desire for professional-grade equipment further bolster the demand for multi-layer constructions. Manufacturers are investing heavily in refining multi-layer technologies to achieve even better heat distribution and weight balance, making them increasingly attractive.

Frying Pan/Frying Pan: This application segment is expected to maintain its dominant position. Frying pans are quintessential kitchen tools, used daily for a wide array of cooking tasks. The superior heat control and even cooking offered by clad metal frying pans are highly valued by consumers for achieving perfect searing, sautéing, and frying results. The demand is driven by the need for versatile cookware that can handle high heat and prevent sticking when used with proper techniques. The aesthetic appeal and durability of clad metal frying pans also contribute to their market leadership.

Dominant Regions/Countries:

North America: This region, particularly the United States, is a significant driver of the clad metal cookware market.

Europe: Similar to North America, Europe represents a substantial market for cookware clad metal.

Asia-Pacific (Emerging Dominance): While currently a significant market, the Asia-Pacific region, particularly China, is rapidly emerging as a dominant force, driven by both production and burgeoning consumer demand.

The interplay of these dominant segments and regions, driven by economic growth, evolving consumer aspirations, and technological advancements in materials science, will shape the future landscape of the global cookware clad metal market.

The growth of the cookware clad metal industry is significantly propelled by several key catalysts. A primary driver is the escalating consumer demand for high-performance, durable, and aesthetically pleasing kitchenware. As culinary trends evolve and home cooking gains prominence, individuals are seeking cookware that offers superior heat distribution, responsiveness, and longevity, all hallmarks of clad metal. The continuous innovation in material science and manufacturing techniques by companies like Korea Clad Tech and others is leading to improved product quality and a wider range of applications, further stimulating market growth. Moreover, the increasing disposable incomes in emerging economies are enabling a larger segment of the population to invest in premium kitchen products, thus expanding the market's reach.

This comprehensive report offers an in-depth analysis of the global cookware clad metal market, covering the period from 2019 to 2033. It delves into the intricate trends shaping the industry, exploring the driving forces behind its expansion, such as the growing consumer preference for premium kitchenware and the rising disposable incomes. The report also critically examines the challenges and restraints that the market navigates, including the impact of substitute materials and pricing sensitivities. A significant portion of the report is dedicated to identifying the key regions and segments poised for dominance, providing detailed insights into their market dynamics. Furthermore, it highlights the pivotal growth catalysts and lists the leading players, offering a holistic view of the competitive landscape. The report concludes with a detailed overview of significant developments and an outlook for the future, making it an indispensable resource for stakeholders seeking to understand and capitalize on opportunities within the evolving cookware clad metal sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.4%.

Key companies in the market include Korea Clad Tech, Jiangsu CNMC Composite Materials Co., Ltd., Luoyang Copper Metal Materials Co., Ltd, Yinbang Clad Material, Luoyang Tongxin Composite Materials, Zhejiang Jinnuo Composite Materials, Zhengzhou Yuguang Composite Materials, Shanghai Huayuan Composite Materials, Zhejiang Aibo Composite Materials, Hunan Fangheng Composite Materials.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Cookware Clad Metal," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cookware Clad Metal, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.