1. What is the projected Compound Annual Growth Rate (CAGR) of the CO2 Capture and Storage Technology?

The projected CAGR is approximately 15.54%.

CO2 Capture and Storage Technology

CO2 Capture and Storage TechnologyCO2 Capture and Storage Technology by Type (CO2 Capture and Storage (CCS), CO2 Capture and Utilization (CCU)), by Application (Industrial Facilities, Power Plant, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

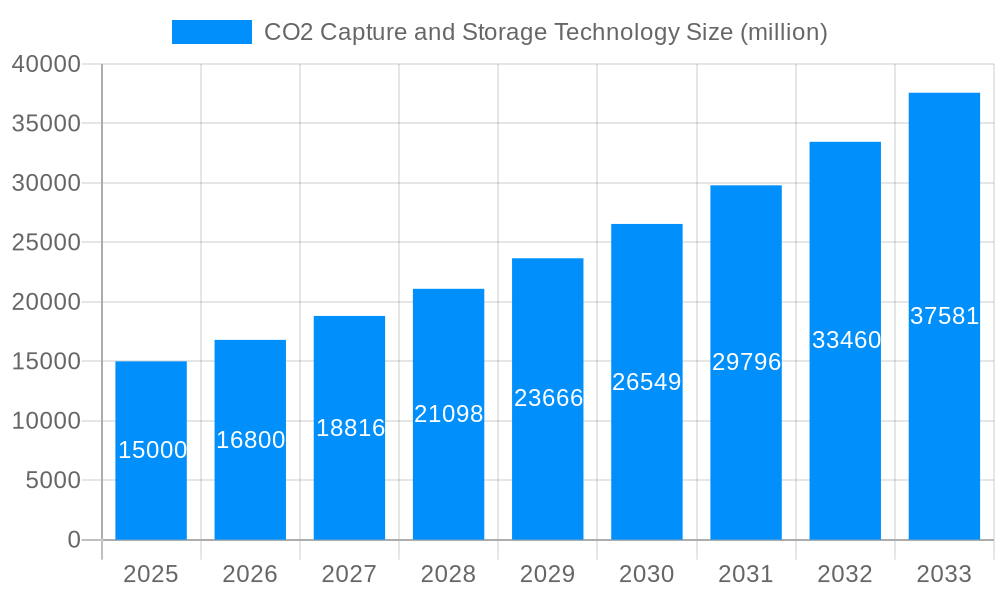

The Carbon Capture and Storage (CCS) technology market is experiencing substantial expansion, propelled by escalating global climate change concerns and rigorous environmental mandates. The market, projected to reach $13.96 billion in the base year of 2025, is anticipated to grow at a Compound Annual Growth Rate (CAGR) of 15.54% through 2033. This upward trend is underpinned by several critical drivers. Foremost is the increasing demand for decarbonized energy solutions from power generation and industrial sectors. Concurrently, technological advancements in CCS are enhancing efficiency and lowering costs, thereby promoting broader implementation. Government incentives, carbon pricing strategies, and corporate sustainability commitments are further stimulating market development. Substantial public and private investments in research, deployment, and infrastructure are accelerating market adoption. Although challenges like high upfront capital expenditure and potential geological storage risks persist, ongoing innovation and supportive policies are effectively addressing these issues.

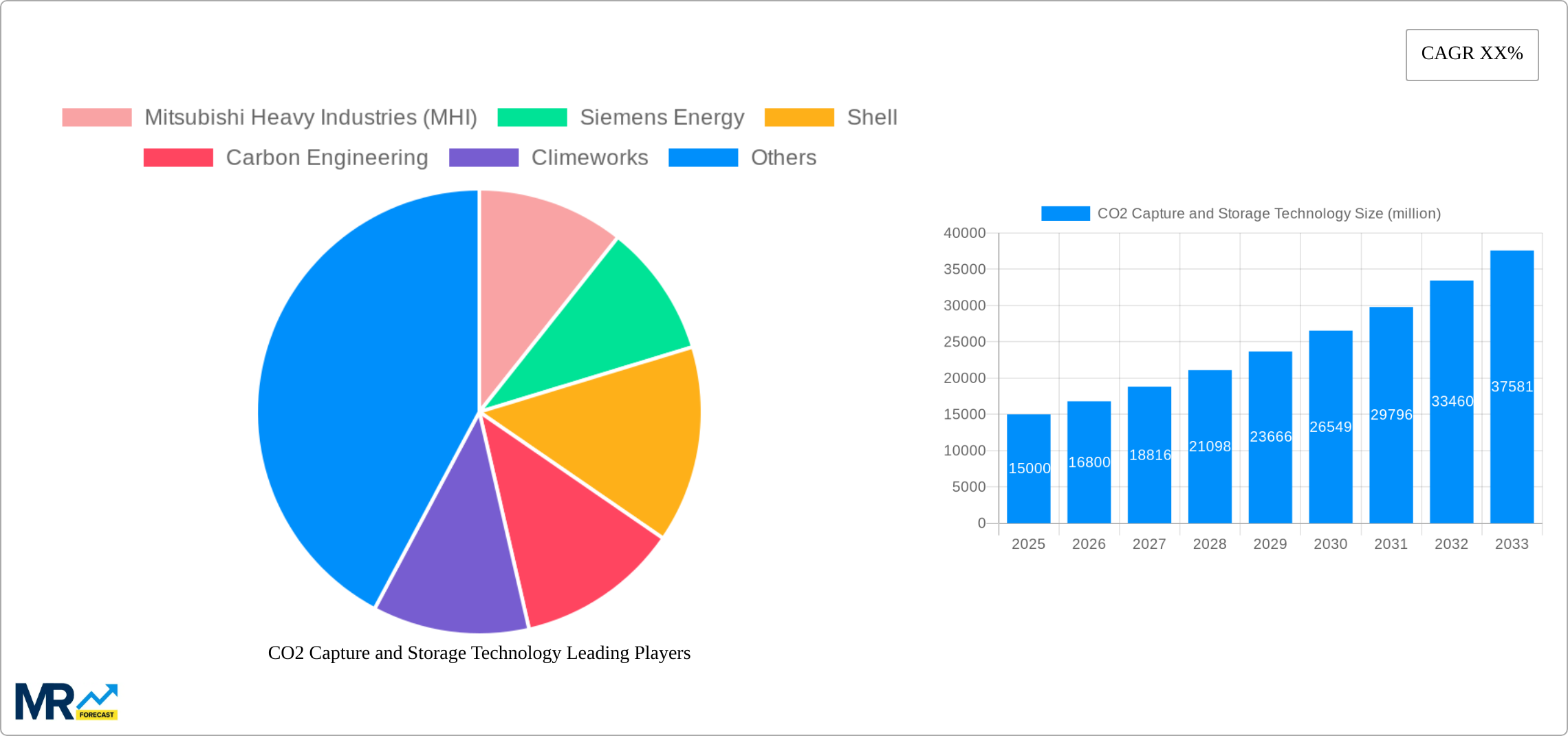

Market segmentation indicates that CCS applications within industrial facilities currently dominate, followed by power plants. The emerging "Others" segment, which includes novel technologies like Direct Air Capture (DAC), is poised for significant future growth. Geographically, North America and Europe lead due to robust infrastructure and established regulatory landscapes. However, the Asia-Pacific region, with key markets like China and India, is projected for rapid advancement, driven by substantial renewable energy investments and heightened emissions reduction pressures. Leading market participants, including Mitsubishi Heavy Industries, Siemens Energy, Shell, and Carbon Engineering, are strategically enhancing their capabilities and forging new alliances to leverage this dynamic market. Continued emphasis on technological innovation, supportive governmental policies, and heightened climate change awareness will continue to define the future trajectory of the CCS market.

The CO2 Capture and Storage (CCS) and CO2 Capture and Utilization (CCU) technology market is experiencing significant growth, driven by escalating concerns about climate change and tightening environmental regulations. The global market, valued at USD 4,500 million in 2025, is projected to reach USD 12,000 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of over 12% during the forecast period (2025-2033). This substantial expansion is fueled by a confluence of factors, including increasing investments in renewable energy, supportive government policies aimed at reducing carbon emissions, and the growing adoption of CCS/CCU technologies across various industrial sectors. The historical period (2019-2024) witnessed steady growth, laying the foundation for the accelerated expansion anticipated in the coming years. Key market insights reveal a strong preference for CCS solutions in power generation and industrial applications, with CCU gaining traction, especially in chemical production and the creation of value-added products from captured CO2. The market is characterized by a diverse range of players, from established energy giants to innovative start-ups, fostering competition and innovation in technology development, deployment, and cost reduction. Technological advancements, such as improved capture efficiency and the development of more cost-effective storage solutions, are pivotal in driving market expansion. Furthermore, the increasing integration of CCS/CCU with other decarbonization strategies enhances its overall appeal and market viability. The ongoing exploration and development of novel capture methods and storage sites are further contributing to the market's dynamic growth trajectory, painting a promising picture for the future of carbon management.

Several compelling forces are accelerating the adoption of CO2 Capture and Storage (CCS) and Utilization (CCU) technologies. Stringent government regulations, aiming to curtail greenhouse gas emissions and meet climate change targets, are significantly driving market growth. These regulations often include carbon pricing mechanisms, emission reduction mandates, and financial incentives for CCS/CCU deployment. The increasing awareness of climate change and its detrimental effects on the environment is fostering a global shift toward cleaner energy sources and sustainable practices, thereby promoting demand for CCS/CCU technologies as vital components of decarbonization strategies. Moreover, advancements in technology have led to enhanced capture efficiency, reduced costs, and the development of more scalable and reliable storage solutions. These improvements are making CCS/CCU more economically viable and attractive to a wider range of industries. The growing participation of major energy companies and industrial players demonstrates a strong commitment to reducing their environmental footprint and embracing sustainable business practices. They are investing heavily in CCS/CCU research, development, and deployment, demonstrating the technology's increasing commercial viability. Furthermore, the potential for CCU to create valuable products from captured CO2 opens up new revenue streams and economic opportunities, further incentivizing its adoption. These combined factors point towards a sustained and accelerated growth trajectory for the CCS/CCU market.

Despite the significant growth potential, several challenges hinder widespread adoption of CO2 Capture and Storage (CCS) and Utilization (CCU) technologies. The high capital costs associated with CCS/CCU deployment remain a major barrier, particularly for smaller companies and developing nations. These costs encompass the installation of capture equipment, construction of pipelines for CO2 transport, and the development of secure storage sites. Furthermore, the energy intensity of some CO2 capture processes can reduce the overall efficiency of power plants and industrial facilities. This trade-off between emission reduction and energy consumption needs careful consideration. The risk of CO2 leakage from storage sites, although mitigated through rigorous geological studies and monitoring, remains a significant environmental concern, requiring ongoing research and robust regulatory frameworks. The lack of a fully developed and interconnected infrastructure for CO2 transport and storage presents another challenge, particularly in regions with limited existing infrastructure. Finally, public perception and acceptance of CCS/CCU technologies, along with potential social and environmental concerns surrounding storage locations, need to be addressed through transparent communication and engagement with local communities. Overcoming these challenges is crucial for unlocking the full potential of CCS/CCU in achieving global decarbonization goals.

The CO2 Capture and Storage (CCS) segment is expected to dominate the market due to its established application in mitigating emissions from large-scale industrial facilities and power plants.

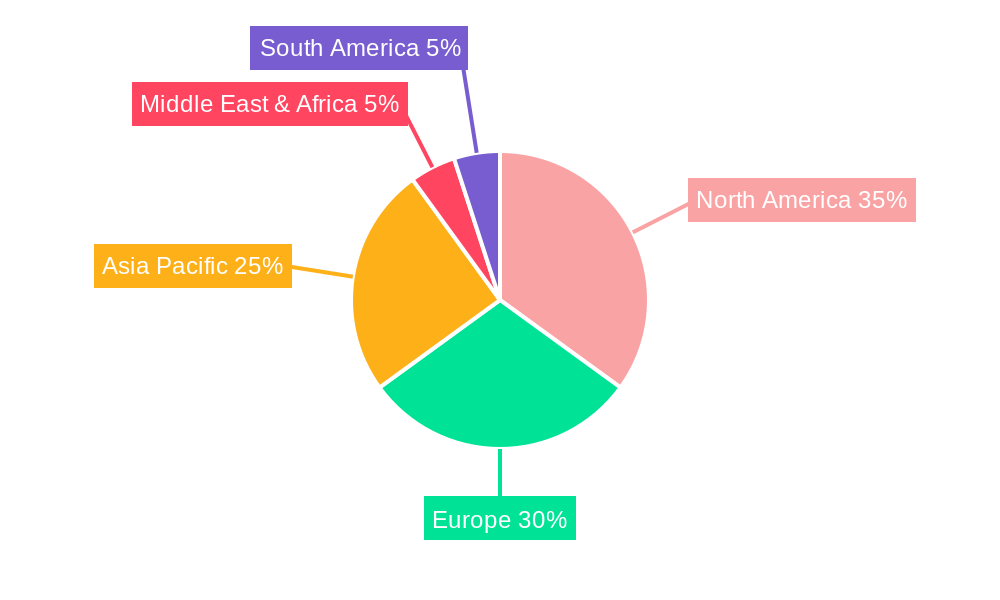

North America: This region is projected to hold a significant market share, driven by substantial investments in CCS projects, supportive government policies, and the presence of major energy companies with extensive CCS experience. The United States, in particular, is investing heavily in CCS infrastructure and research. The presence of mature oil and gas fields offers suitable geological formations for CO2 storage, bolstering the region's competitiveness.

Europe: Stringent environmental regulations and ambitious climate change targets are driving strong growth in the European CCS market. Several large-scale CCS projects are underway or planned, particularly in countries with advanced energy and industrial sectors. Significant funding and policy support for CCS initiatives are contributing to market expansion. The EU’s focus on achieving carbon neutrality further strengthens this region's potential.

Asia Pacific: This region is poised for rapid growth, driven by increasing industrialization, expanding power generation capacity, and growing awareness of environmental issues. China and India, with their large carbon footprints, are investing heavily in CCS technology to reduce emissions from their power plants and industrial facilities. However, the region also faces challenges related to infrastructure development and technology adoption.

Dominant Application Segment: The Power Plant application segment will dominate due to the substantial CO2 emissions generated by power generation and the crucial need for effective carbon capture and storage solutions to meet climate goals.

Detailed Segment Analysis:

CO2 Capture and Storage (CCS): This segment is expected to dominate the market due to its more established technology and proven ability to reduce emissions. The maturity of the technology and substantial investment from both the public and private sectors have led to widespread deployment across industrial facilities and power plants.

CO2 Capture and Utilization (CCU): While currently smaller, CCU is showing strong growth potential as the technology advances and becomes more cost-effective. The ability to convert captured CO2 into valuable products creates economic incentives, driving investment in the segment.

Industrial Facilities: This application segment will see significant growth owing to stringent emissions regulations targeting heavy industries such as cement, steel, and chemicals. These industries are major CO2 emitters, making CCS/CCU essential for environmental compliance.

Power Plants: The power generation sector is a key driver of CCS market growth, as power plants are major sources of CO2 emissions. The incorporation of CCS technology into new and existing power plants is a crucial aspect of mitigating climate change.

Several factors contribute to the accelerated growth of the CO2 Capture and Storage technology industry. Government incentives, including tax credits and grants, significantly reduce the financial burden of deploying CCS/CCU systems. Technological advancements, such as the development of more efficient and cost-effective capture technologies, are making CCS/CCU economically more attractive. The increasing awareness of climate change and the growing pressure to reduce carbon emissions are driving the demand for CCS/CCU technologies globally. Furthermore, the development of robust and secure CO2 storage infrastructure, enabling large-scale deployment of CCS projects, is playing a pivotal role in the market’s expansion. The exploration of carbon capture utilization (CCU) processes that convert captured CO2 into valuable products further drives innovation and market expansion.

This report provides a comprehensive analysis of the CO2 Capture and Storage (CCS) and Utilization (CCU) technology market, covering historical data (2019-2024), current estimates (2025), and future projections (2025-2033). The report delves into market drivers, challenges, and growth catalysts, offering a detailed segmentation analysis by type (CCS, CCU), application (industrial facilities, power plants, others), and key geographical regions. It also profiles leading players in the industry, providing valuable insights into their strategies, technologies, and market positions. This report serves as a valuable resource for companies, investors, and policymakers seeking to understand and navigate the evolving landscape of carbon capture technologies.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.54% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 15.54%.

Key companies in the market include Mitsubishi Heavy Industries (MHI), Siemens Energy, Shell, Carbon Engineering, Climeworks, Occidental Petroleum Oxy, Aker Solutions, Carbon Clean Solutions, Global Thermostat, C-Capture, Schlumberger (SLB), Bechtel, ION Clean Energy, Chevron, Svante Technologies, NET Power, LanzaTech, .

The market segments include Type, Application.

The market size is estimated to be USD 13.96 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "CO2 Capture and Storage Technology," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the CO2 Capture and Storage Technology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.