1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud Computing in Education Sector?

The projected CAGR is approximately 12.23%.

Cloud Computing in Education Sector

Cloud Computing in Education SectorCloud Computing in Education Sector by Type (Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS)), by Application (K-12 Schools, Higher Education), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

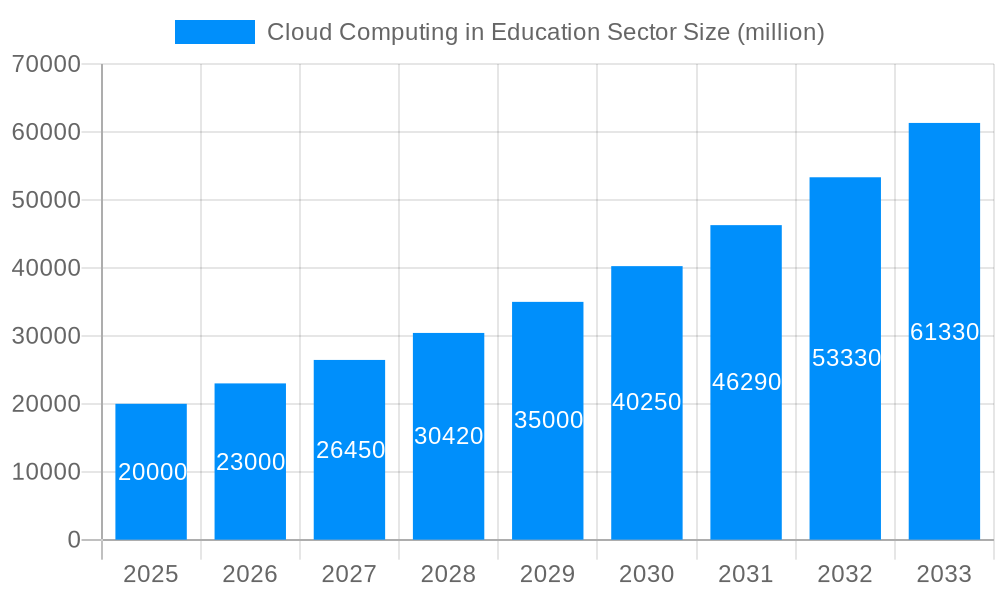

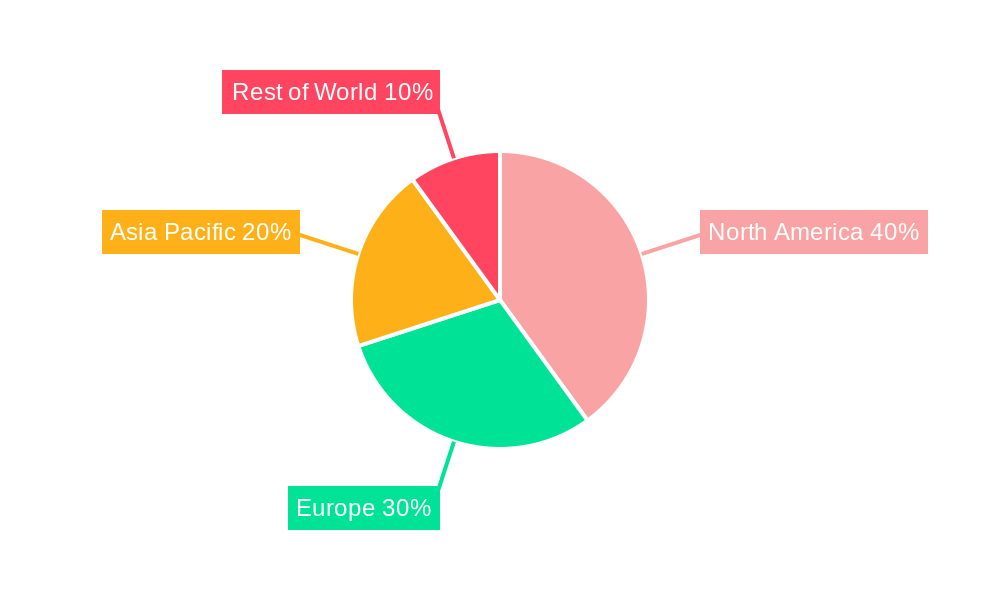

The global cloud computing market within the education sector is experiencing substantial expansion. Key drivers include the escalating adoption of digital learning environments, the imperative for robust data security and accessibility, and the increasing demand for agile and scalable IT infrastructure. The market, currently valued at $10.38 billion in the base year of 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.23% from 2025 to 2033. This trajectory is underpinned by the ongoing digital transformation initiatives in educational institutions, governmental support for technology integration, and the cost efficiencies offered by cloud solutions over traditional on-premise systems. The Software as a Service (SaaS) segment leads, offering accessible learning management systems (LMS), student information systems (SIS), and other educational applications. While higher education currently leads adoption, the K-12 segment is rapidly advancing due to increased funding and a focus on student performance. North America and Europe are primary markets, with significant growth potential in Asia-Pacific and other emerging economies marked by rising digital literacy.

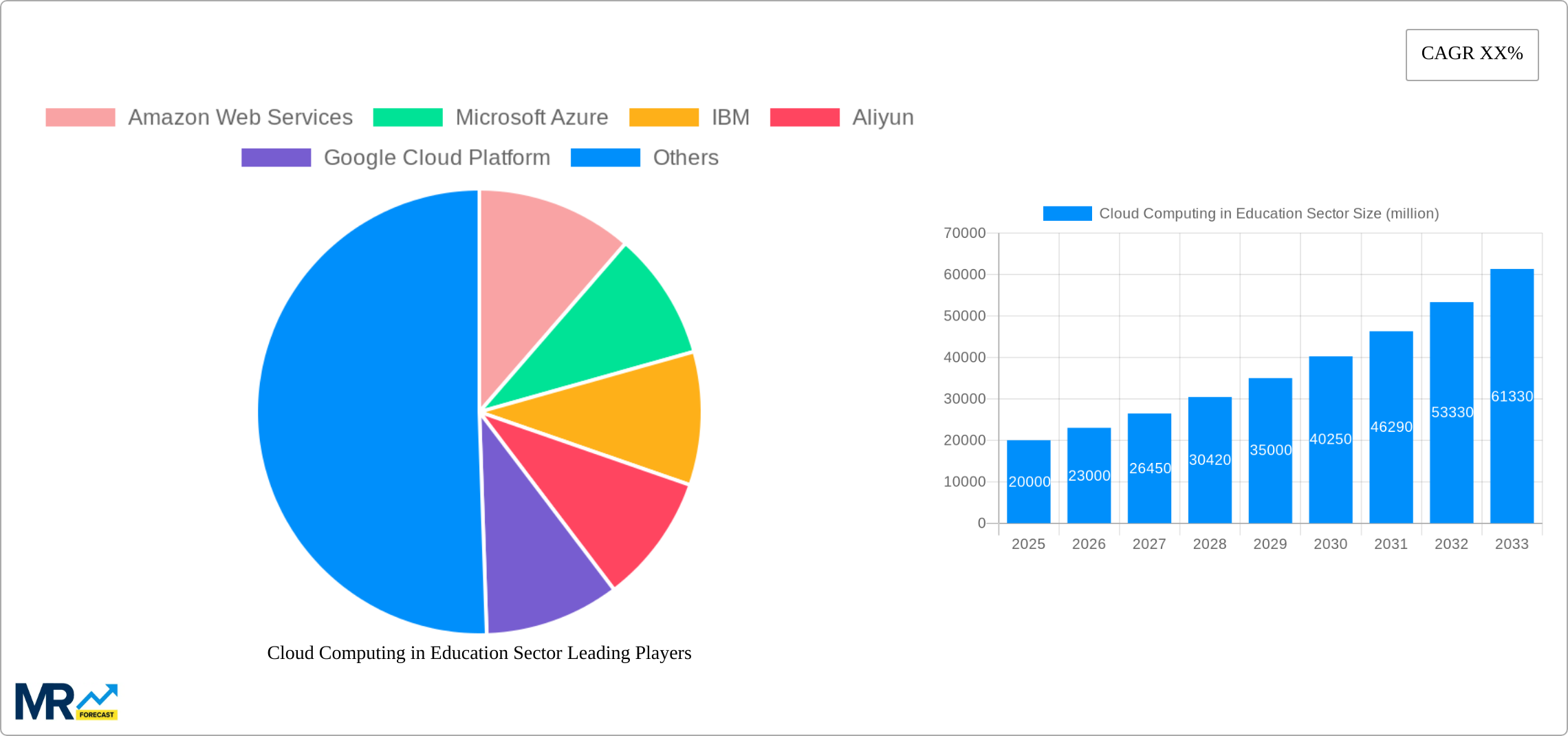

The competitive environment is dynamic, featuring major providers such as Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), and Salesforce. Niche players are also emerging with specialized educational solutions. Advancements in cloud technologies, including Artificial Intelligence (AI) and machine learning, are poised to enhance personalized learning and administrative efficiency. Addressing data privacy and cybersecurity concerns through robust measures and compliance is crucial for sustained adoption. The adoption of hybrid cloud models, blending on-premise and cloud services, is also gaining momentum, offering institutions a balanced approach to data and application management.

The global cloud computing market in the education sector is experiencing explosive growth, projected to reach multi-billion dollar valuations by 2033. Our analysis, covering the period from 2019 to 2033 (with a base year of 2025 and a forecast period of 2025-2033), reveals a significant shift towards cloud-based solutions across K-12 schools and higher education institutions. This transition is driven by the increasing need for flexible, scalable, and cost-effective IT infrastructure to support evolving educational needs. The historical period (2019-2024) showcased a steady rise in cloud adoption, paving the way for the dramatic expansion predicted in the coming years. Key market insights point to a strong preference for Software as a Service (SaaS) solutions, particularly Learning Management Systems (LMS) and collaborative tools. However, the growth is not uniform across all cloud service models. Infrastructure as a Service (IaaS) is gaining traction among institutions seeking greater control over their infrastructure, while Platform as a Service (PaaS) is attracting developers building custom educational applications. The competitive landscape is dynamic, with major players like Amazon Web Services, Microsoft Azure, and Google Cloud Platform vying for market share alongside specialized education technology providers. This competition fuels innovation, leading to the development of increasingly sophisticated and user-friendly cloud-based educational tools. The market's expansion is further fueled by government initiatives promoting digital learning and the growing adoption of BYOD (Bring Your Own Device) policies in educational settings. Furthermore, the increasing need for data analytics and personalized learning experiences is driving demand for advanced cloud capabilities. By 2033, the market is expected to see a significant increase in the adoption of AI-powered learning platforms and cloud-based cybersecurity solutions, reflecting the evolving needs of a digitally transforming education landscape. The estimated market value for 2025 is in the tens of billions, indicating substantial investment and growth potential.

Several factors are accelerating the adoption of cloud computing in the education sector. Cost savings are a primary driver, as cloud solutions eliminate the need for expensive on-premise hardware and IT infrastructure maintenance. Scalability is another crucial factor; cloud platforms can easily adapt to fluctuating demands, accommodating increasing student populations and peak usage periods without significant upfront investment. The enhanced flexibility offered by cloud solutions allows educational institutions to quickly deploy new applications and services, adapting to changing pedagogical approaches and technological advancements. Improved collaboration is another significant advantage, with cloud-based tools facilitating seamless communication and knowledge sharing among students, teachers, and administrators. Cloud computing also enhances accessibility, enabling students and educators to access learning resources from anywhere with an internet connection, bridging geographical barriers and promoting inclusivity. Furthermore, robust data security features offered by many cloud providers are increasingly vital in protecting sensitive student data. The growing availability of user-friendly, intuitive cloud-based applications specifically designed for educational purposes further reduces the barriers to entry, making the transition to cloud computing smoother for educational institutions of all sizes and technical expertise. Government initiatives promoting digital education and the increasing availability of high-speed internet access are also contributing significantly to this market's growth.

Despite the numerous benefits, several challenges and restraints hinder widespread cloud adoption in the education sector. Data security and privacy concerns remain a major obstacle, particularly regarding the protection of sensitive student information. Institutions are concerned about potential data breaches and compliance with relevant regulations like FERPA (Family Educational Rights and Privacy Act) in the US and GDPR (General Data Protection Regulation) in Europe. The digital divide, with unequal access to high-speed internet and computing devices, presents another significant challenge, hindering cloud adoption in under-resourced areas and among underserved student populations. Concerns about vendor lock-in, the dependence on a specific cloud provider, and the potential for increased costs in the long run also discourage some institutions from fully embracing cloud solutions. The need for robust training and support for educators and administrators in effectively utilizing cloud-based technologies is also a considerable challenge. Resistance to change among some educators and administrators who are accustomed to traditional IT infrastructure can also slow down the adoption process. Finally, the integration of cloud solutions with existing legacy systems can be complex and time-consuming, requiring significant investment in technical expertise and resources. Addressing these challenges through robust security measures, bridging the digital divide, providing adequate training and support, and offering flexible and adaptable solutions will be crucial for driving further adoption of cloud technologies within the education sector.

The North American region, particularly the United States, is expected to dominate the cloud computing market in education throughout the forecast period (2025-2033). This dominance stems from factors such as:

Within the market segments, Software as a Service (SaaS) is projected to hold the largest market share. This is because:

While the North American region leads, other regions, particularly Western Europe and parts of Asia-Pacific, are witnessing significant growth in cloud adoption within the education sector. These regions are expected to demonstrate strong growth rates in the coming years, albeit starting from a smaller base than North America. The growth is fueled by similar factors, such as increasing government investments in digital education and improving internet infrastructure.

The convergence of factors is propelling the growth of cloud computing in education. Increasing government support for digital learning initiatives and the growing need for flexible, scalable, and cost-effective IT solutions are key drivers. The rising adoption of BYOD (Bring Your Own Device) policies and the increasing demand for personalized learning experiences are also contributing to this growth. The development of innovative cloud-based educational applications, along with the integration of Artificial Intelligence and Machine Learning into learning platforms, promises further expansion in the years to come. These catalysts are expected to drive significant market expansion, making cloud computing an integral part of the modern education landscape.

This report provides a detailed analysis of the cloud computing market in the education sector, covering market trends, drivers, challenges, and key players. It offers insights into the various cloud service models (IaaS, PaaS, SaaS) and their application across different educational segments (K-12, Higher Education). The report also highlights regional variations in cloud adoption and provides growth forecasts for the period 2025-2033, projecting significant market expansion driven by technological advancements, increasing government support, and the evolving needs of the educational landscape. This comprehensive analysis is intended to inform stakeholders, including educational institutions, technology providers, and investors, about the opportunities and challenges in this rapidly growing market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.23% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12.23%.

Key companies in the market include Amazon Web Services, Microsoft Azure, IBM, Aliyun, Google Cloud Platform, Salesforce, Rackspace, SAP, Oracle, Dell EMC, Adobe Systems, Verizon Cloud, NetApp, Baidu Yun, Tencent Cloud, Blackboard, .

The market segments include Type, Application.

The market size is estimated to be USD 10.38 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Cloud Computing in Education Sector," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cloud Computing in Education Sector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.