1. What is the projected Compound Annual Growth Rate (CAGR) of the Clinical Research Organization?

The projected CAGR is approximately 6.0%.

Clinical Research Organization

Clinical Research OrganizationClinical Research Organization by Type (Full-Service CRO, Functional Service Provision CRO), by Application (Pre-clinical, Clinical I-Ⅲ, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

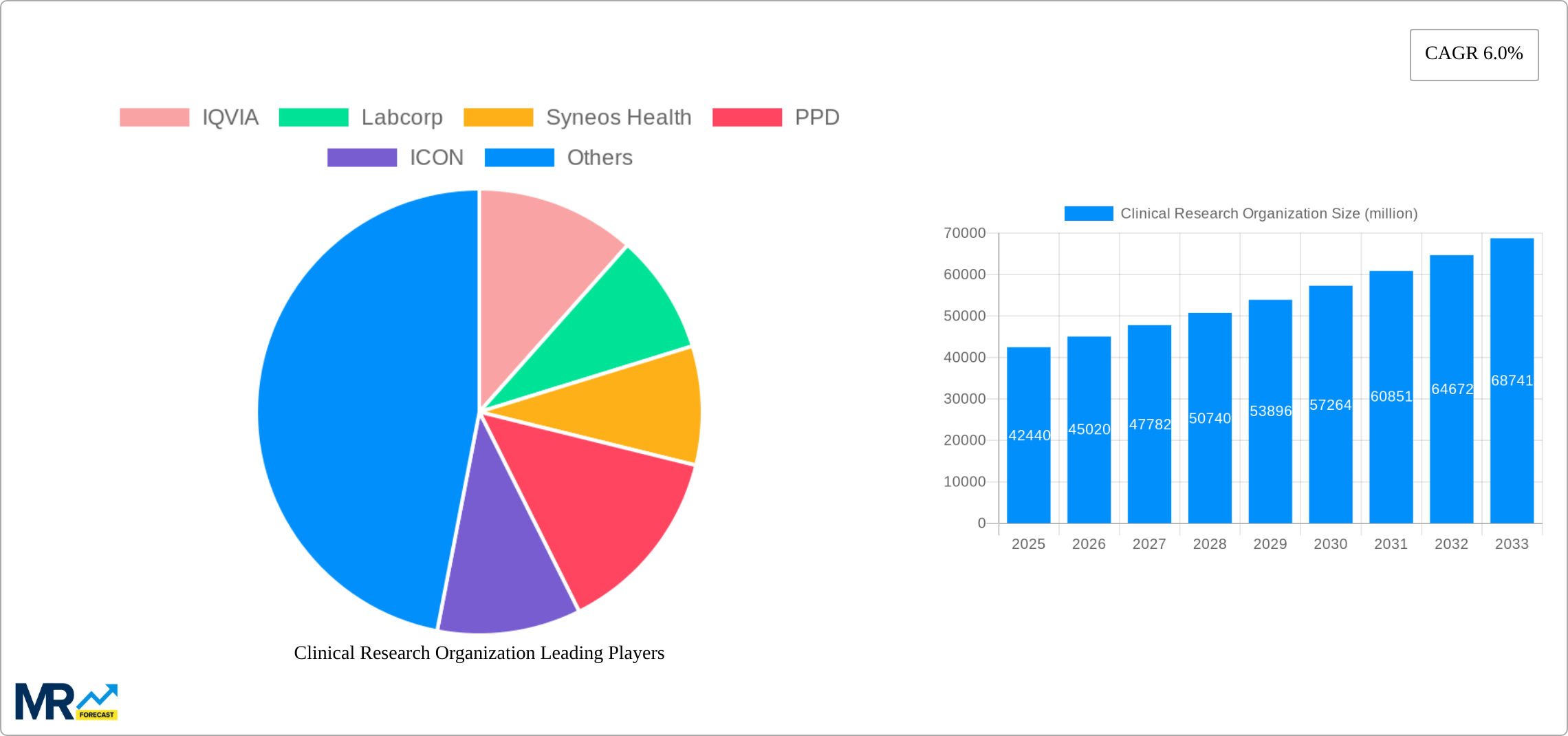

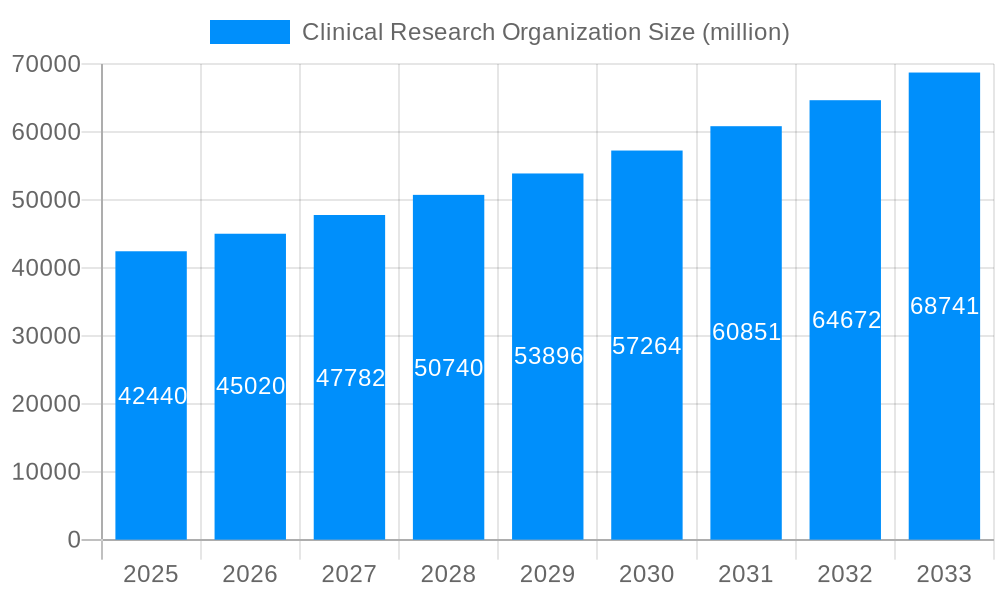

The Clinical Research Organization (CRO) market is experiencing robust growth, projected to reach \$42.44 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 6.0% from 2025 to 2033. This expansion is driven by several key factors. The increasing prevalence of chronic diseases globally fuels the demand for efficient and cost-effective clinical trials. Furthermore, the rising adoption of advanced technologies like artificial intelligence and big data analytics in clinical research is streamlining processes and accelerating drug development. The outsourcing of clinical trials by pharmaceutical and biotechnology companies to specialized CROs continues to be a significant driver, owing to the CROs’ expertise in managing complex regulatory requirements and optimizing trial efficiency. The market's segmentation reveals a strong preference for full-service CROs due to their comprehensive capabilities, though functional service provision CROs are experiencing growth as companies increasingly seek specialized expertise. Pre-clinical and clinical phases I-III represent the most significant application segments, reflecting the extensive involvement of CROs throughout the drug development lifecycle.

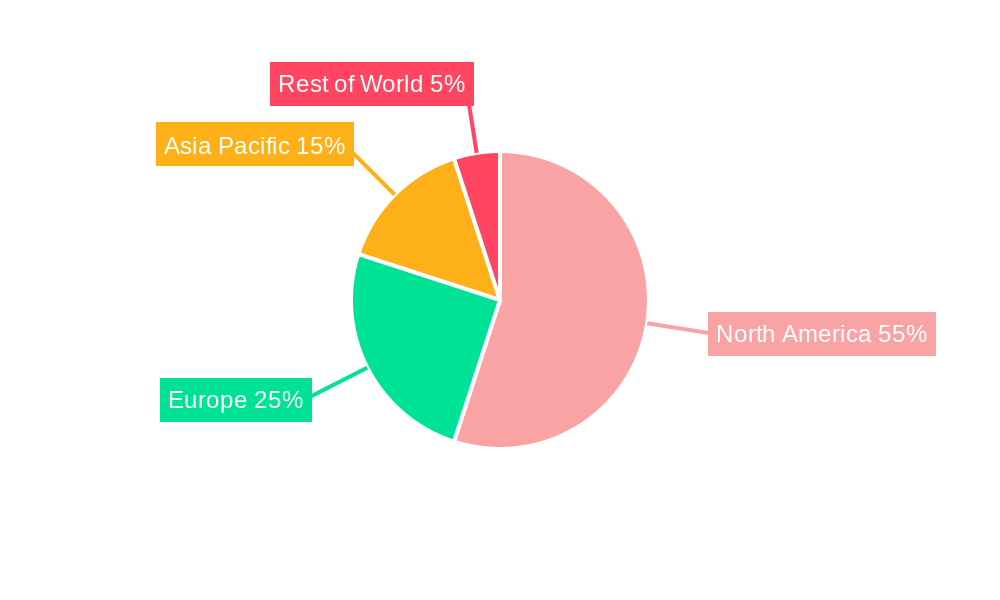

The competitive landscape is marked by both established industry giants like IQVIA, Labcorp, and Syneos Health, and emerging players. Geographical distribution indicates a significant market share held by North America, attributed to the high concentration of pharmaceutical companies and advanced healthcare infrastructure. However, Asia Pacific, driven by growing healthcare expenditure and increasing clinical trial activity in countries like China and India, presents a substantial growth opportunity. Europe remains a significant market, while regions like the Middle East and Africa are emerging as promising but slower-growing areas. The market's future trajectory hinges on regulatory changes, technological advancements, and the overall pace of pharmaceutical innovation. Continued growth is expected, fueled by the ongoing need to accelerate drug development and improve clinical trial efficiency in a complex and evolving global landscape.

The global Clinical Research Organization (CRO) market is experiencing robust growth, projected to reach XXX million by 2033, driven by a confluence of factors. The historical period (2019-2024) witnessed steady expansion, laying the groundwork for the significant acceleration anticipated during the forecast period (2025-2033). This growth is fueled by the increasing complexity of clinical trials, the rising prevalence of chronic diseases necessitating extensive research, and the burgeoning adoption of advanced technologies like AI and big data analytics within the clinical trial process. The market's expansion is further propelled by the outsourcing trend among pharmaceutical and biotechnology companies seeking to streamline operations and reduce costs. This outsourcing leads to increased demand for CRO services across various stages of drug development, from pre-clinical studies to post-market surveillance. Furthermore, the growing number of clinical trials globally, particularly in emerging markets, creates significant opportunities for CROs to expand their geographical footprint and service offerings. The competitive landscape is characterized by both large, multinational CROs offering a full spectrum of services and smaller, specialized firms focusing on niche therapeutic areas. This diversity ensures a wide range of options for sponsors, fostering innovation and driving market growth. However, challenges remain, including stringent regulatory environments, escalating costs associated with clinical trials, and the pressure to deliver faster and more efficient results. The successful CROs will be those that can adapt quickly to these challenges and leverage technological advancements to enhance their service offerings and maintain a competitive edge in this dynamic market. The estimated market size for 2025 is XXX million, representing a significant increase from the base year.

Several key factors are driving the remarkable growth trajectory of the Clinical Research Organization market. The increasing complexity of drug development, particularly in areas like oncology and immunology, necessitates specialized expertise and resources beyond the capabilities of many pharmaceutical companies. This naturally leads to greater reliance on CROs for their expertise in designing, conducting, and managing complex clinical trials. Furthermore, the rising prevalence of chronic diseases worldwide fuels the demand for new treatments and, consequently, the need for extensive clinical research. The cost-effectiveness of outsourcing clinical trial functions is another critical driver. CROs often offer economies of scale and specialized expertise at a lower cost than internal development, making them an attractive option for sponsors facing budgetary constraints. Technological advancements, such as the application of artificial intelligence (AI) and big data analytics, are transforming the clinical research landscape. CROs are at the forefront of adopting these technologies, enabling them to optimize trial design, improve patient recruitment, and accelerate data analysis, thus reducing overall trial timelines and costs. Finally, a growing trend toward globalization in clinical research is expanding market opportunities for CROs. Sponsors are increasingly conducting trials in multiple countries to enhance diversity in their study populations and expedite the drug development process. This creates a significant demand for CROs with global reach and regulatory expertise.

Despite the significant growth potential, the CRO industry faces several challenges and restraints that could impede its progress. Stringent regulatory requirements and increasing scrutiny from regulatory bodies worldwide pose significant hurdles for CROs. Maintaining compliance with evolving guidelines and regulations necessitates substantial investment in infrastructure, training, and quality control measures. The high cost of clinical trials is another major challenge. The cost of conducting clinical trials continues to rise due to factors such as increased complexity, stringent regulatory requirements, and the growing need for specialized personnel. This can make it difficult for smaller CROs to compete effectively and can limit the number of trials that can be conducted. Competition is fierce within the CRO industry. The market is characterized by a large number of players, ranging from multinational giants to smaller niche players. This intense competition leads to price pressures and the need for CROs to constantly differentiate their services and capabilities. Patient recruitment and retention continue to be significant challenges. Finding and retaining suitable patients for clinical trials can be time-consuming and expensive, often leading to delays and increased costs. Finally, data management and security are of paramount importance in the CRO industry. The large volumes of sensitive patient data generated during clinical trials necessitate robust data management systems and stringent security measures to comply with regulations and protect patient privacy.

The North American region is expected to dominate the market throughout the study period (2019-2033), followed by Europe. This dominance is primarily attributed to the high concentration of pharmaceutical and biotechnology companies, robust regulatory frameworks, and advanced healthcare infrastructure within these regions. Within these regions, the Full-Service CRO segment holds a significant market share.

Full-Service CROs: These companies offer a comprehensive range of services, covering all aspects of clinical trial management, from pre-clinical development to post-market surveillance. This end-to-end approach is highly attractive to pharmaceutical and biotechnology sponsors seeking a simplified and streamlined process. Their comprehensive services command higher fees compared to functional service providers, driving market revenue growth. Major players in this segment include IQVIA, Labcorp, Syneos Health, and PPD, contributing substantially to the segment's dominance. The increased adoption of technology and the need for streamlined operations continue to fuel the demand for full-service solutions.

Geographic Dominance: North America’s advanced healthcare infrastructure, high concentration of pharmaceutical and biotech companies, and robust regulatory frameworks make it the leading market. Europe's strong regulatory environment and presence of major pharma players also contribute significantly to its strong market position. Asia-Pacific demonstrates significant growth potential, fueled by increasing government investments in healthcare and a rise in chronic disease prevalence.

Application Dominance: The Clinical I-III segment commands a significant portion of the market due to the intense research and development efforts focused on advancing drug candidates through various phases of clinical trials. Pre-clinical stages also contribute substantially, as pharmaceutical companies increasingly outsource this initial crucial stage to CROs.

The paragraph above further details the reasons behind the dominance of full-service CROs and the specific geographic regions.

Several factors are accelerating growth in the CRO industry. The increasing outsourcing of clinical trials by pharmaceutical and biotechnology companies, driven by cost optimization and access to specialized expertise, is a major catalyst. Technological advancements, including AI and big data analytics, are improving trial efficiency and speed, attracting more sponsors to utilize CRO services. Furthermore, the growing prevalence of chronic diseases globally, necessitating extensive clinical research, fuels the industry’s expansion. Finally, the expansion of clinical trials into emerging markets presents significant opportunities for CROs to broaden their reach and operations.

This report provides a comprehensive analysis of the Clinical Research Organization market, covering market size and trends, driving forces, challenges, and key players. It offers insights into the major segments – Full-Service CROs, Functional Service Provision CROs, and application segments such as Pre-clinical, Clinical I-III – providing a granular understanding of market dynamics and future growth potential across different regions. The report also highlights significant industry developments and provides detailed company profiles of leading CROs, offering valuable insights for stakeholders in the pharmaceutical, biotechnology, and clinical research industries.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.0% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.0%.

Key companies in the market include IQVIA, Labcorp, Syneos Health, PPD, ICON, PRA, Parexel, Medpace, Wuxi Apptec, EPS International, Worldwide Clinical Trials, CMIC, Premier Research, Courante Oncology, PROMETRIKA, Charles River Laboratories International Inc (CRL), Hangzhou Tigermed, Clinipace, PSI CRO, Pierrel Research, .

The market segments include Type, Application.

The market size is estimated to be USD 42440 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Clinical Research Organization," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Clinical Research Organization, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.