1. What is the projected Compound Annual Growth Rate (CAGR) of the Central Laboratory Service?

The projected CAGR is approximately 9.16%.

Central Laboratory Service

Central Laboratory ServiceCentral Laboratory Service by Type (Genetic Services, Biomarker Services, Microbiology Services, Pathology Services), by Application (Pharmaceutical Companies, Biotechnological Companies, Academic and Research Institutes), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

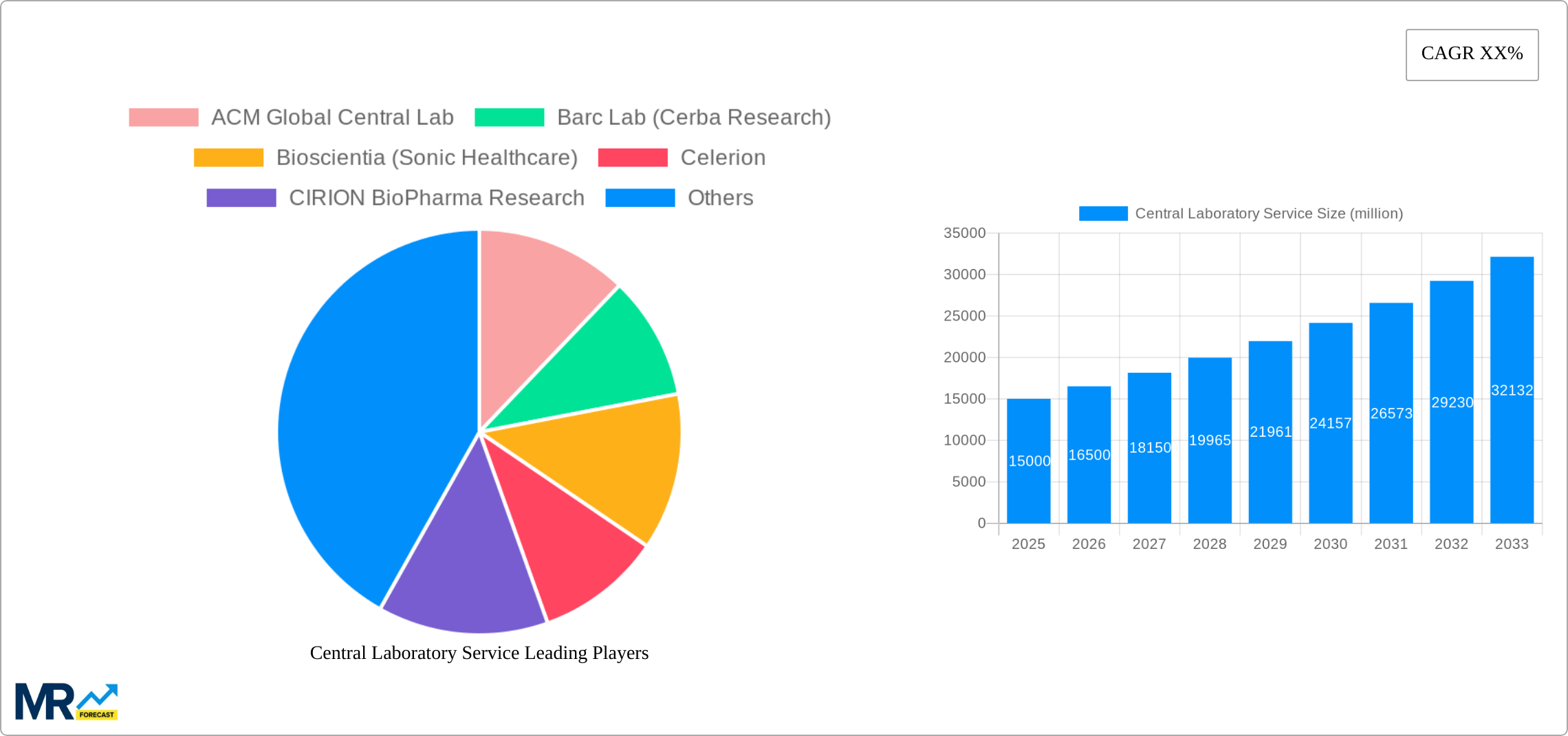

The global central laboratory services market is experiencing robust growth, driven by the increasing outsourcing of laboratory testing by pharmaceutical and biotechnology companies, coupled with the rising demand for high-throughput screening and advanced analytical techniques. The market's expansion is fueled by several key factors, including the accelerating pace of drug discovery and development, the growing prevalence of chronic diseases necessitating extensive diagnostic testing, and the increasing adoption of personalized medicine approaches. This necessitates sophisticated central laboratory services capable of handling complex sample types and delivering fast, accurate results. Technological advancements such as automation, artificial intelligence, and next-generation sequencing are further enhancing efficiency and expanding the scope of services offered, attracting significant investments into the sector. The market is segmented by service type (genetic, biomarker, microbiology, pathology) and application (pharmaceutical, biotechnological companies, academic and research institutes), with pharmaceutical companies representing a substantial portion of the market share due to their high reliance on extensive testing throughout the drug development lifecycle. Geographic variations exist, with North America and Europe currently dominating the market, although the Asia-Pacific region is expected to witness significant growth in the coming years driven by increasing healthcare spending and a growing pharmaceutical industry.

Despite the overall positive market outlook, certain challenges remain. These include stringent regulatory requirements and compliance standards, the high cost associated with advanced technologies and skilled personnel, and potential supply chain disruptions impacting the availability of reagents and consumables. Competition is intensifying among both large multinational corporations and smaller specialized laboratories, leading to price pressures and the need for constant innovation to maintain a competitive edge. However, the continuous rise in demand for advanced testing, coupled with the ongoing development of innovative technologies, suggests that the central laboratory services market will remain a dynamic and lucrative sector, poised for continued expansion throughout the forecast period. Specific growth rates within segments will depend on technological advancements and the changing regulatory landscape.

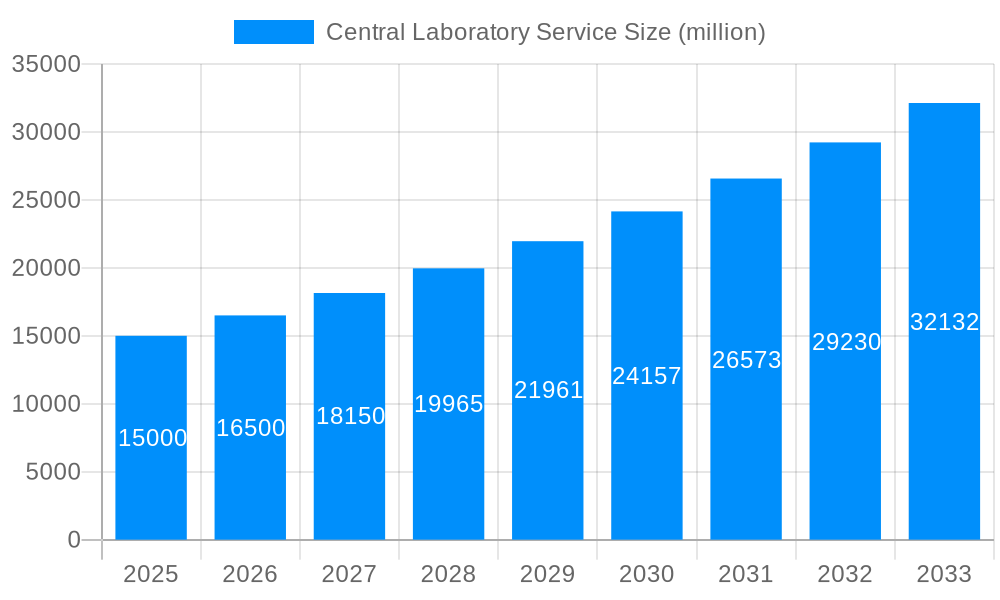

The global central laboratory service market is experiencing robust growth, projected to reach multi-billion dollar valuations by 2033. Driven by increasing outsourcing by pharmaceutical and biotechnological companies, the market witnessed significant expansion during the historical period (2019-2024). This trend is expected to continue throughout the forecast period (2025-2033), fueled by factors such as the rising prevalence of chronic diseases, the growing demand for faster drug development, and the increasing adoption of advanced technologies within the industry. The estimated market value in 2025 is already substantial, representing millions of units in revenue, and projections indicate continued expansion at a healthy CAGR. Key market insights reveal a shift towards integrated services, with companies seeking comprehensive solutions that encompass various testing modalities like genomics, proteomics, and immunology. This integration allows for more efficient and cost-effective drug development processes. Furthermore, the growing adoption of artificial intelligence (AI) and machine learning (ML) in data analysis is improving the accuracy and speed of results, contributing to the overall market expansion. The competitive landscape is dynamic, with both large multinational corporations and smaller specialized laboratories vying for market share. This competition fosters innovation and drives down costs, benefiting clients in the pharmaceutical and biotech sectors. The market's growth is also influenced by stringent regulatory requirements, necessitating high-quality and reliable testing services. This demand for compliance further encourages industry consolidation and the adoption of advanced quality management systems. Finally, the increasing focus on personalized medicine is driving demand for specialized genetic and biomarker testing, further accelerating market growth in specific segments.

Several key factors propel the growth of the central laboratory service market. The pharmaceutical and biotechnology industries are increasingly outsourcing their laboratory testing needs to central labs to reduce operational costs, gain access to advanced technologies, and streamline their drug development processes. This outsourcing trend allows companies to focus on core competencies while leveraging the expertise and infrastructure of specialized central labs. The rising prevalence of chronic diseases, such as cancer, diabetes, and cardiovascular diseases, is another significant driver. The increased need for diagnostic testing and monitoring of these conditions fuels demand for central laboratory services. Furthermore, the growing emphasis on personalized medicine and the development of targeted therapies necessitates comprehensive and precise testing, including genetic and biomarker analysis. This trend is driving the demand for specialized central laboratory services that cater to personalized medicine initiatives. The ongoing technological advancements in laboratory automation, high-throughput screening, and data analytics are also contributing factors. These innovations enhance efficiency, reduce turnaround times, and improve the accuracy of test results, making central laboratories more attractive to clients. Finally, the stringent regulatory environment requiring rigorous quality control and compliance further strengthens the demand for reputable and established central laboratory services that can guarantee accuracy and reliability.

Despite the significant growth potential, the central laboratory service market faces several challenges. Maintaining data security and patient privacy is paramount, and ensuring compliance with evolving data protection regulations is a crucial concern. The industry must invest heavily in cybersecurity measures to mitigate risks associated with data breaches. The high cost of advanced technologies and the need for continuous investment in equipment and personnel training pose a significant financial hurdle for smaller players. Competition among established players and the emergence of new entrants make market penetration challenging. Maintaining consistent quality across multiple testing sites and ensuring standardization of methodologies can be difficult, particularly with a geographically dispersed network of labs. Stringent regulatory requirements, including those related to accreditation and compliance, necessitate significant investment in quality assurance and control systems. Furthermore, managing the complexities of global supply chains, particularly regarding reagent availability and logistics, presents logistical and operational challenges. Finally, fluctuating healthcare reimbursement policies and pricing pressures from payers can impact the profitability of central laboratories.

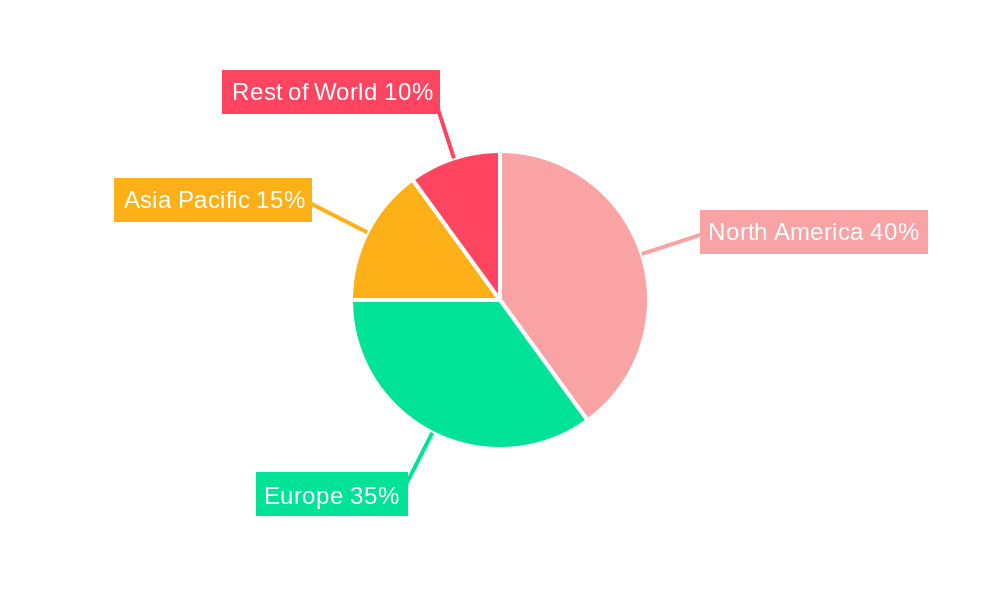

The North American region, particularly the United States, is anticipated to dominate the central laboratory service market throughout the forecast period. This dominance is primarily attributable to the high concentration of pharmaceutical and biotechnology companies, coupled with substantial funding for research and development activities. Furthermore, the advanced healthcare infrastructure and the early adoption of cutting-edge technologies in the US contribute to the region’s leading position.

Pharmaceutical Companies: This segment constitutes the largest application segment within the market. Pharmaceutical companies rely heavily on central laboratory services for drug development, clinical trials, and quality control testing throughout the drug lifecycle. The demand for sophisticated testing and analytics within this segment is substantially higher than other application segments, driving overall market expansion. Their need for large-scale testing capacity, stringent quality control measures, and rapid turnaround times has significantly contributed to the growth of central laboratory services tailored to their needs.

Biomarker Services: The increasing understanding of biomarkers' role in disease diagnosis, prognosis, and treatment monitoring is a significant driving force behind the growth of the biomarker services segment. The segment's expansion is attributable to the growing need for accurate and reliable biomarker testing to support personalized medicine initiatives and accelerate drug discovery. Biomarker testing is fundamental to developing targeted therapies and stratifying patients for clinical trials, making it an essential aspect of modern pharmaceutical and clinical research.

Genetic Services: The rapid advances in genomic technologies have spurred significant growth in the genetic services segment. The growing demand for genetic testing for disease diagnosis, predisposition assessment, and pharmacogenomics is pushing the market forward. This demand is driven by increased awareness among healthcare professionals and patients, as well as the increasing availability of cost-effective genetic testing technologies.

In summary, the convergence of factors like the dominance of large pharmaceutical companies in North America, coupled with the high demand for advanced biomarker and genetic testing within pharmaceutical applications, points to a continued dominant position for the North American region and its associated sectors within the central laboratory service market.

Several factors are catalyzing growth in the central laboratory service industry. The rising prevalence of chronic diseases worldwide increases the need for diagnostic testing and disease monitoring. Simultaneously, advancements in technologies, like automation and AI-powered analytics, enhance efficiency and accuracy, making central labs increasingly attractive. Stringent regulatory requirements necessitate high-quality testing, further boosting the demand for reliable and compliant central labs.

This report provides a comprehensive overview of the Central Laboratory Service market, encompassing historical data, current market trends, and future projections. It offers deep insights into key market segments, leading players, growth drivers, and challenges, making it a valuable resource for stakeholders seeking to understand and navigate this evolving landscape. The report analyzes the market's competitive landscape, identifies opportunities, and offers strategic recommendations for businesses operating within this sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.16% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.16%.

Key companies in the market include ACM Global Central Lab, Barc Lab (Cerba Research), Bioscientia (Sonic Healthcare), Celerion, CIRION BioPharma Research, Clinical Reference Laboratory, Eurofins Central Laboratory, Frontage Laboratories, Inc, Icon central labs, Metropolis Healthcare Ltd., .

The market segments include Type, Application.

The market size is estimated to be USD 6.51 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Central Laboratory Service," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Central Laboratory Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.