1. What is the projected Compound Annual Growth Rate (CAGR) of the Catalyst for Diesel Vehicles?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Catalyst for Diesel Vehicles

Catalyst for Diesel VehiclesCatalyst for Diesel Vehicles by Type (Activated Catalyst, Non-Activated Catalyst, World Catalyst for Diesel Vehicles Production ), by Application (Three-Wheel Diesel Vehicle, Four-Wheel Diesel Vehicle, World Catalyst for Diesel Vehicles Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

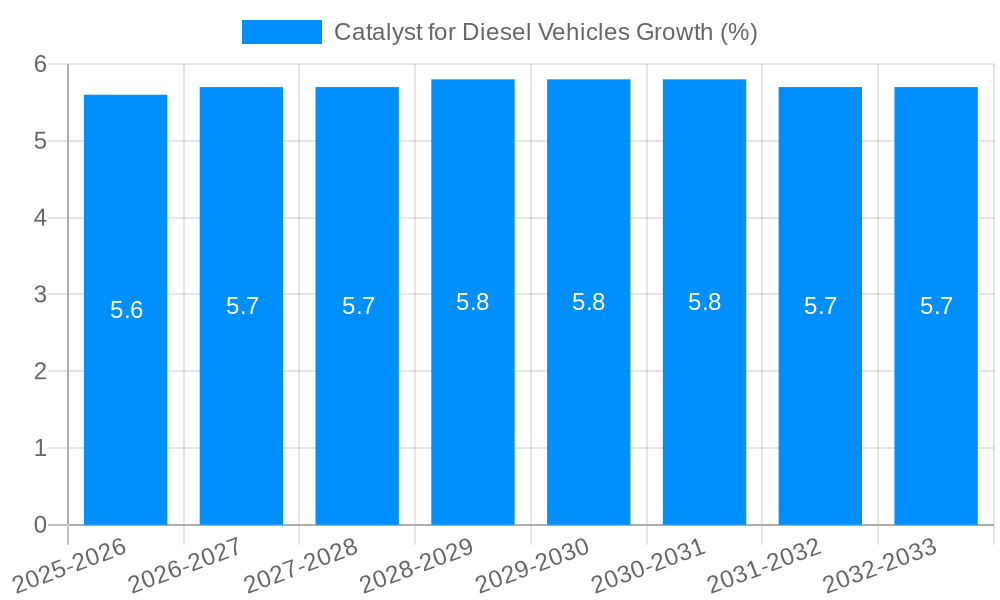

The global market for Catalysts for Diesel Vehicles is poised for significant expansion, driven by increasingly stringent emission regulations worldwide and a sustained demand for diesel powertrains in commercial and heavy-duty applications. The market is projected to reach a substantial size, fueled by a healthy Compound Annual Growth Rate (CAGR) of approximately 5-7% over the forecast period (2025-2033). This growth is underpinned by technological advancements in catalyst formulations, leading to enhanced efficiency in reducing harmful emissions like NOx and particulate matter. Key drivers include government initiatives aimed at improving air quality, particularly in urban centers, and the continued reliance on diesel engines for their fuel efficiency and torque, making them indispensable for freight transportation and industrial machinery. Furthermore, the transition towards cleaner diesel technologies, including selective catalytic reduction (SCR) and diesel oxidation catalysts (DOC), is a major catalyst for market development.

The market segmentation reveals a strong emphasis on Activated Catalysts, reflecting the ongoing innovation and demand for high-performance solutions. In terms of applications, both Three-Wheel and Four-Wheel Diesel Vehicles represent significant end-use segments, with the latter holding a larger share due to the prevalence of diesel in light commercial vehicles and passenger cars in certain regions. Geographically, Asia Pacific, led by China and India, is expected to emerge as a dominant region due to rapid industrialization, increasing vehicle parc, and supportive government policies for emission control. Europe and North America, with their mature automotive markets and stringent environmental standards, will also continue to be crucial markets. However, the market may face certain restraints, such as the rising cost of precious metals used in catalyst production and the growing adoption of alternative powertrains like electric vehicles, which could eventually challenge the long-term dominance of diesel technology. Despite these challenges, the robust demand from the commercial vehicle sector and ongoing regulatory pressures will ensure a dynamic and growing market for diesel vehicle catalysts.

This comprehensive report delves into the dynamic global market for catalysts used in diesel vehicles. Spanning a detailed study period from 2019 to 2033, with a base and estimated year of 2025, the analysis provides an in-depth understanding of historical trends, current market conditions, and future projections. The report meticulously examines the market through various lenses, including production volumes, application segments, technological advancements, and the competitive landscape, offering actionable insights for stakeholders.

The report quantifies the global catalyst for diesel vehicles production in millions of units, providing a clear picture of market size and growth trajectories. It segments the market by type, distinguishing between Activated Catalyst and Non-Activated Catalyst, and by application, categorizing demand from Three-Wheel Diesel Vehicles and Four-Wheel Diesel Vehicles. This granular segmentation allows for a focused understanding of specific market niches and their respective growth potentials.

Furthermore, the report highlights crucial industry developments that are shaping the future of diesel vehicle catalysts. It identifies key driving forces, challenges, and restraints that influence market dynamics, alongside emerging growth catalysts. The competitive landscape is thoroughly analyzed, featuring leading global players and their significant contributions to the sector. With a focus on providing actionable intelligence, this report is an indispensable resource for manufacturers, suppliers, policymakers, and investors navigating the evolving world of diesel vehicle emission control technology.

The global market for catalysts in diesel vehicles is experiencing a significant transformation, driven by increasingly stringent emission regulations and a growing emphasis on sustainable transportation solutions. Over the historical period of 2019-2024, the market witnessed a steady demand, primarily fueled by the continued prevalence of diesel engines in heavy-duty vehicles, commercial fleets, and specific passenger car segments. The base year of 2025 marks a critical juncture, where the interplay of advanced emission control technologies and evolving regulatory frameworks is expected to define the market's trajectory.

Looking ahead to the forecast period of 2025-2033, the catalyst for diesel vehicles market is poised for notable growth, albeit with regional variations. The increasing adoption of Selective Catalytic Reduction (SCR) and Diesel Particulate Filter (DPF) technologies, which rely on sophisticated catalysts, is a key trend. These systems are crucial for meeting Euro 6/VI and equivalent emission standards worldwide, significantly reducing nitrogen oxides (NOx) and particulate matter (PM) emissions. The report projects a positive CAGR, reflecting the sustained need for effective exhaust after-treatment solutions. A significant trend observed is the shift towards more advanced catalytic materials that offer enhanced durability, higher efficiency at lower temperatures, and improved resistance to poisoning. This innovation is critical as engines are increasingly downsized and equipped with start-stop systems, leading to cooler exhaust gas temperatures where traditional catalysts might be less effective. Furthermore, the integration of catalysts with advanced sensor technologies for real-time monitoring and control is becoming a norm, leading to more optimized emission reduction. The market is also seeing a growing interest in catalysts with lower precious metal loadings without compromising performance, driven by cost optimization efforts. The increasing focus on the circular economy is also influencing the market, with greater emphasis on catalyst regeneration and recycling processes to recover valuable precious metals, thereby reducing the environmental footprint of catalyst production. The demand for catalysts in emerging economies, as they gradually adopt stricter emission norms, is another significant trend that will contribute to overall market expansion during the forecast period.

The catalyst for diesel vehicles market is propelled by a confluence of powerful forces, primarily centered around environmental consciousness and regulatory mandates. The most significant driver is the relentless tightening of global emission standards, such as Euro 6/VI in Europe, EPA Tier 4 in the United States, and similar regulations in other major automotive markets. These stringent norms necessitate advanced exhaust after-treatment systems, with catalysts playing a pivotal role in reducing harmful pollutants like nitrogen oxides (NOx), particulate matter (PM), and carbon monoxide (CO) to meet the legally mandated limits. The increasing global awareness of air quality issues and their adverse impact on public health is further reinforcing the demand for cleaner diesel vehicles, indirectly boosting the catalyst market.

Moreover, the sustained demand for diesel engines, particularly in the commercial vehicle sector (trucks, buses, and agricultural machinery) and for industrial applications, continues to underpin market growth. These sectors often rely on the inherent fuel efficiency and torque characteristics of diesel engines, making them a preferred choice despite the rise of alternative powertrains. The ongoing advancements in catalyst technology, leading to more efficient, durable, and cost-effective solutions, also act as a significant driving force. Manufacturers are investing heavily in research and development to create catalysts that can perform optimally under various operating conditions, including low-temperature starts and stop-start cycles, thereby enhancing their applicability and market penetration. The economic benefits of improved fuel efficiency, often achieved in conjunction with effective emission control systems, also contribute to the sustained interest in diesel powertrains and, consequently, their associated catalysts.

Despite the positive growth trajectory, the catalyst for diesel vehicles market faces several significant challenges and restraints that could impede its full potential. The most prominent challenge is the increasing global shift towards electrification of vehicles, particularly passenger cars. As electric vehicles (EVs) gain market share, the demand for internal combustion engine (ICE) vehicles, including diesel ones, is expected to decline in the long term, especially in developed markets. This transition poses a significant threat to the future market size of diesel catalysts. Another major restraint is the high cost associated with precious metals, such as platinum, palladium, and rhodium, which are crucial components of most diesel catalysts. Fluctuations in the prices of these raw materials can significantly impact the overall cost of catalysts, making them expensive for manufacturers and potentially hindering adoption, especially in price-sensitive markets.

Furthermore, the complexity of modern emission control systems, which often involve multiple components like Diesel Particulate Filters (DPFs) and Selective Catalytic Reduction (SCR) systems, adds to the overall cost and maintenance requirements of diesel vehicles. This can be a deterrent for consumers, particularly in regions where the infrastructure for maintenance and repair of these advanced systems is not well-developed. The ongoing debate and regulatory scrutiny surrounding diesel emissions, despite technological advancements, also create market uncertainty. Negative public perception regarding diesel pollution, even with advanced catalytic converters, can influence consumer choices and governmental policies, leading to potential restrictions or phase-outs of diesel vehicles in certain urban areas. The development and implementation of alternative emission control technologies, or even outright bans on internal combustion engines, present a continuous challenge for the long-term viability of the diesel catalyst market.

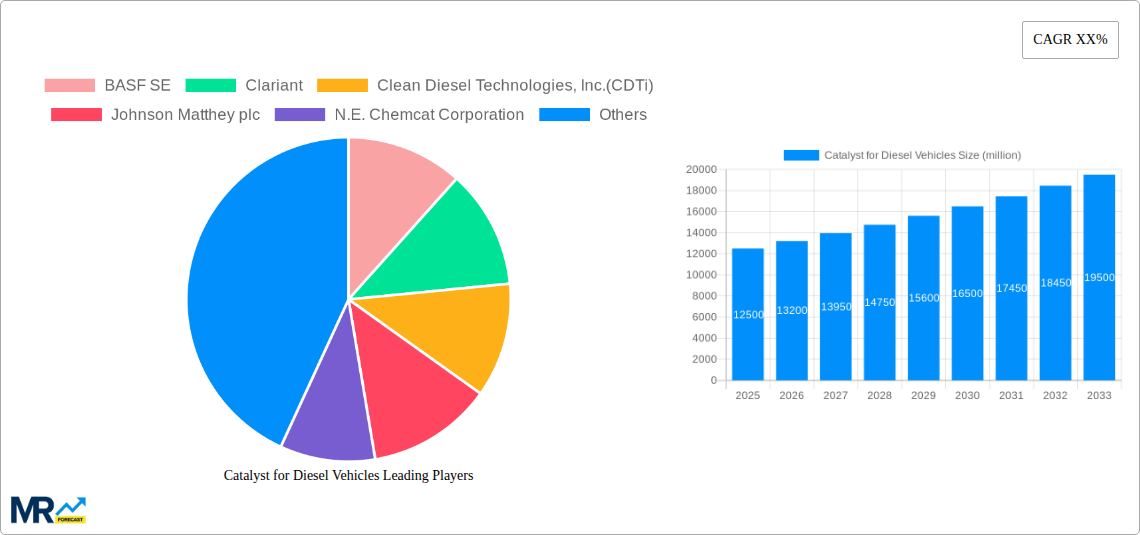

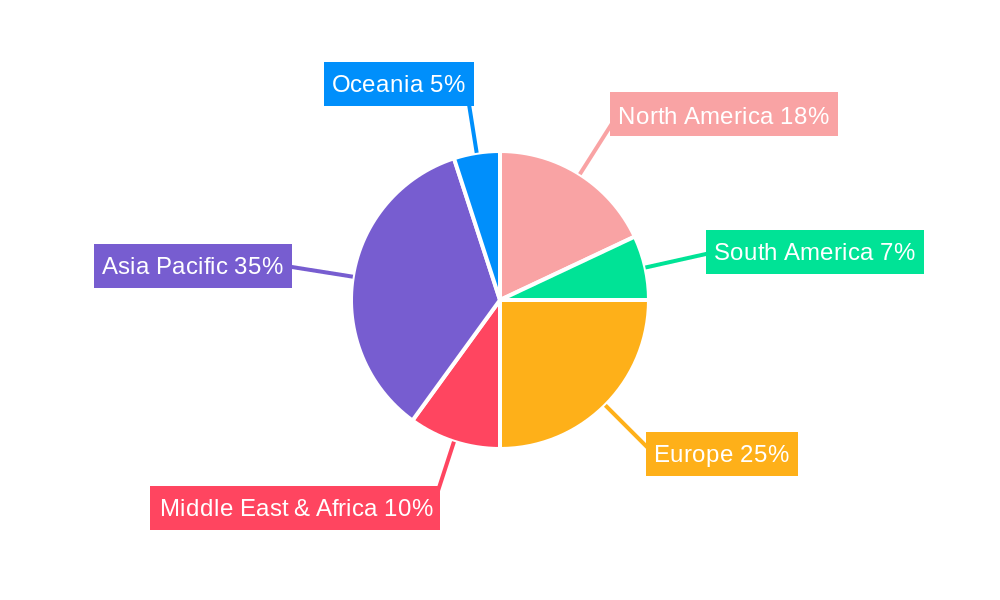

The global Catalyst for Diesel Vehicles market exhibits distinct regional dynamics and segment preferences, with certain areas and product categories poised for significant dominance. Asia Pacific is projected to be a leading region in terms of World Catalyst for Diesel Vehicles Production volume during the forecast period (2025-2033). This dominance is fueled by several factors. Firstly, the region boasts a substantial and growing automotive manufacturing base, with China, India, and Southeast Asian nations being major producers of both diesel engines and vehicles. The sheer volume of production for both Four-Wheel Diesel Vehicles and Three-Wheel Diesel Vehicles in these countries drives a massive demand for catalysts. India, in particular, has a significant market for three-wheelers and commercial vehicles powered by diesel, where emission control is increasingly becoming a regulatory priority.

Secondly, while developed nations are aggressively pursuing electrification, many developing economies in Asia Pacific are still heavily reliant on diesel technology for their transportation needs, especially in commercial fleets and agricultural sectors. The gradual but consistent implementation of stricter emission norms, such as Bharat Stage VI (BS-VI) in India, which are aligned with Euro VI standards, mandates the use of advanced diesel catalysts. This regulatory push, coupled with economic growth and increasing vehicle ownership, creates a robust demand for catalysts to ensure compliance. The robust growth in the Four-Wheel Diesel Vehicle segment, encompassing commercial trucks, buses, and utility vehicles, is a major contributor to this regional dominance. Furthermore, the continued demand for Three-Wheel Diesel Vehicle applications in several Asian countries, used extensively for logistics and public transport, further solidifies the region's leadership in production volume.

Another segment expected to exhibit strong performance and contribute significantly to market dominance is the Activated Catalyst type. Activated catalysts, which undergo a specific activation process to enhance their performance and longevity, are essential for meeting the stringent emission standards. As regulations become more rigorous, the demand for highly efficient and durable activated catalysts will continue to grow. These catalysts are integral to advanced after-treatment systems like SCR and DPF, which are becoming standard in modern diesel vehicles to curb NOx and particulate matter emissions effectively. The technological advancements in developing more effective and cost-efficient activated catalysts are also a key factor driving their market share. The continuous research and development efforts by leading players to improve the catalytic activity, thermal stability, and poisoning resistance of activated catalysts will ensure their sustained relevance and market leadership throughout the forecast period. The interplay of robust production volumes in Asia Pacific and the increasing adoption of advanced activated catalyst technologies across various diesel vehicle applications positions these regions and segments at the forefront of the global market.

Several key factors are acting as significant growth catalysts for the catalyst for diesel vehicles industry. The primary catalyst is the ongoing global tightening of emission regulations for diesel engines, compelling manufacturers to adopt advanced emission control technologies that rely on sophisticated catalysts. Furthermore, the robust demand for commercial vehicles, including trucks and buses, which continue to utilize diesel engines for their power and efficiency, provides a steady market base. Technological advancements in catalyst design, leading to improved efficiency, durability, and cost-effectiveness, are also spurring growth by making these solutions more accessible and attractive. The increasing focus on sustainable logistics and the reduction of greenhouse gas emissions from transportation fleets further reinforces the need for effective emission control systems.

This comprehensive report offers an exhaustive analysis of the global catalyst for diesel vehicles market, providing stakeholders with a deep understanding of its multifaceted dynamics. The report meticulously covers the market's historical trajectory from 2019 to 2024, establishes a detailed outlook for the forecast period of 2025 to 2033 with 2025 as the base and estimated year, and quantifies production volumes in millions of units. It dissects the market by segmentation, including Type (Activated Catalyst, Non-Activated Catalyst) and Application (Three-Wheel Diesel Vehicle, Four-Wheel Diesel Vehicle), offering granular insights into segment-specific performance and growth potential. The report also provides a thorough examination of industry developments, identifying key trends, driving forces, challenges, and restraints that shape the market landscape. Furthermore, it highlights dominant regions and countries, as well as high-performing market segments, alongside a comprehensive list of leading global players. This detailed coverage ensures that all critical aspects of the catalyst for diesel vehicles market are addressed, empowering informed strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include BASF SE, Clariant, Clean Diesel Technologies, Inc.(CDTi), Johnson Matthey plc, N.E. Chemcat Corporation, Umicore N.V., Evonik, Vineeth Chemicals, Johnson Matthey, Haldor Topsoe A/S, W.R.Grace, Axens, Kailong High Technology, Ningbo Kesen Exhaust Gas Cleaner Manufacturing, Luoyang JALON Micro-nano New Materials, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Catalyst for Diesel Vehicles," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Catalyst for Diesel Vehicles, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.