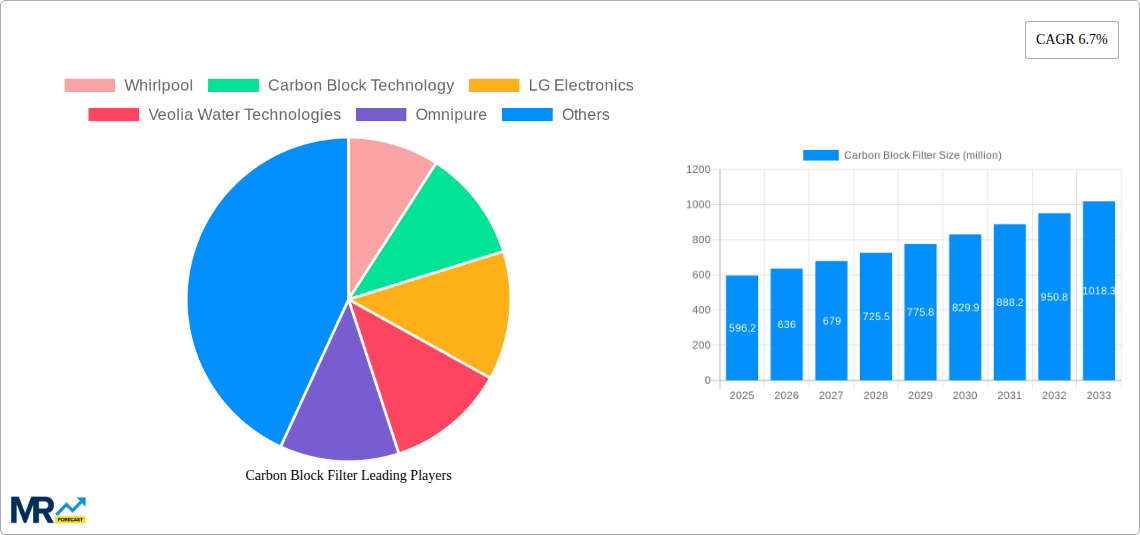

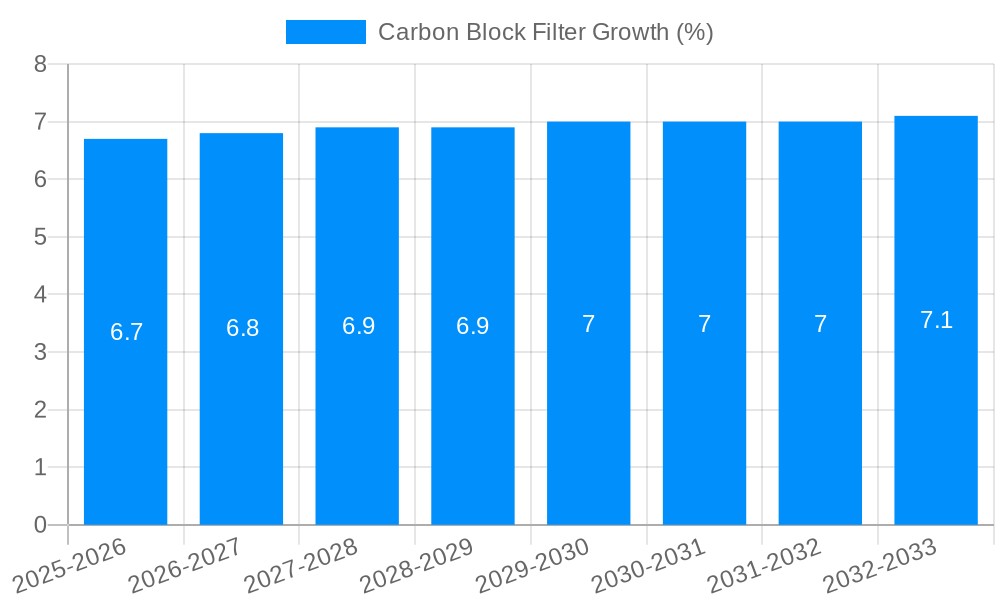

1. What is the projected Compound Annual Growth Rate (CAGR) of the Carbon Block Filter?

The projected CAGR is approximately 6.7%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Carbon Block Filter

Carbon Block FilterCarbon Block Filter by Type (5-20 Micron, > 20 Micron), by Application (Industrial, Residential, Commercial), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global carbon block filter market is experiencing robust growth, projected to reach a valuation of $596.2 million, expanding at a Compound Annual Growth Rate (CAGR) of 6.7% from 2019 to 2033. This sustained expansion is fueled by increasing consumer awareness regarding water purity and the rising prevalence of waterborne diseases, driving demand for effective filtration solutions in both residential and commercial sectors. The industrial application segment, encompassing food and beverage processing, pharmaceuticals, and chemical manufacturing, represents a significant revenue contributor due to stringent quality control requirements and the need for high-purity water. Furthermore, the growing adoption of point-of-use (POU) and point-of-entry (POE) systems in homes, coupled with a surge in demand for compact and efficient filtration within appliances like refrigerators and water dispensers, are key drivers propelling the market forward. The ongoing development of advanced carbon block technologies, offering superior adsorption capabilities and longer lifespans, is also contributing to market expansion by enhancing product performance and consumer satisfaction.

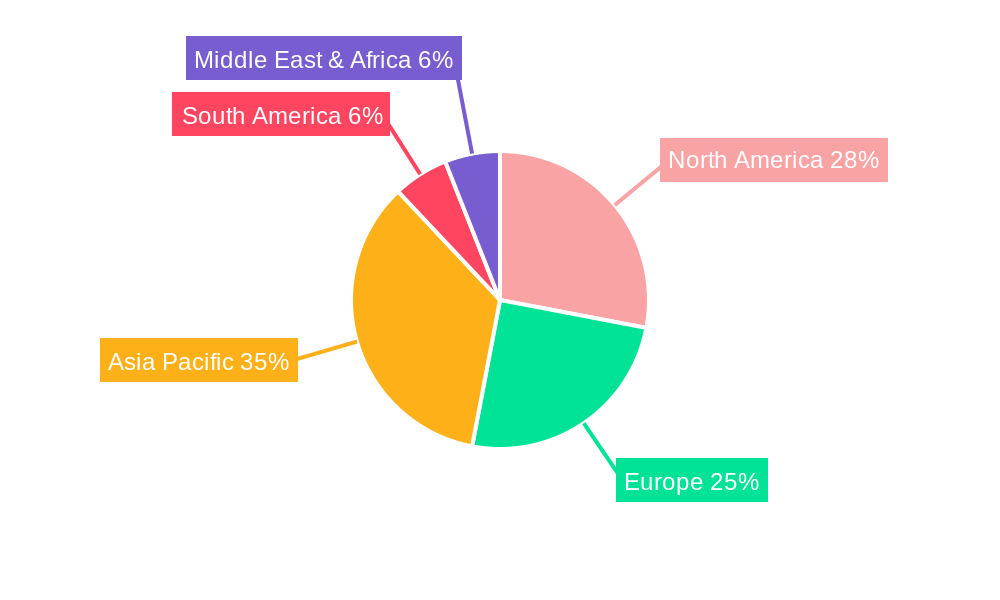

The market is segmented into filter types based on pore size, with the "5-20 Micron" category dominating due to its broad applicability in removing common contaminants, while the "> 20 Micron" segment caters to specific industrial requirements. Geographically, the Asia Pacific region is emerging as a significant growth engine, driven by rapid industrialization, increasing disposable incomes, and a growing middle class with a greater emphasis on health and wellness. North America and Europe remain mature yet substantial markets, characterized by high adoption rates of advanced water purification technologies and stringent regulatory standards. Emerging economies in South America and the Middle East & Africa are also presenting lucrative opportunities as awareness of water quality improves and infrastructure development progresses. Key players in the market are actively engaged in research and development to introduce innovative products, expand their distribution networks, and cater to evolving consumer preferences for sustainable and highly efficient water filtration solutions.

Here is a report description on Carbon Block Filters, incorporating your specific requirements:

The global carbon block filter market is poised for significant expansion, projected to reach an estimated 2.5 billion USD by the end of the study period in 2033. This upward trajectory is underpinned by a confluence of factors, including escalating consumer awareness regarding water purity and the growing imperative for robust industrial water treatment solutions. The historical period from 2019 to 2024 saw steady growth, driven by increasing adoption in residential applications and a burgeoning demand from commercial establishments seeking to enhance the quality of their water supply. The base year, 2025, stands as a pivotal point, with an estimated market valuation of 1.8 billion USD, setting the stage for an impressive compound annual growth rate (CAGR) of approximately 7% during the forecast period of 2025-2033. Key market insights reveal a distinct shift towards higher-performance filters, with a growing preference for carbon block technologies over traditional granular activated carbon (GAC) filters due to their superior contaminant removal capabilities, reduced channeling, and extended lifespan. The market is also witnessing a diversification of applications, extending beyond traditional drinking water purification to encompass specialized industrial processes requiring high levels of chemical and particulate filtration. Furthermore, advancements in material science and manufacturing processes are continuously contributing to the development of more efficient and cost-effective carbon block filter solutions, making them increasingly accessible across a broader spectrum of end-users. The increasing regulatory focus on water quality standards, both for potable and industrial use, further bolsters the market's growth prospects. As global water scarcity concerns intensify, the demand for effective water treatment and recycling solutions will only amplify, with carbon block filters playing a crucial role in meeting these challenges. Innovations in activated carbon sourcing and block manufacturing are expected to drive down production costs while simultaneously enhancing filtration efficiency, further solidifying the market's expansion. The study’s extensive coverage aims to provide a granular understanding of these evolving trends, offering valuable insights for stakeholders across the entire value chain.

The accelerating demand for clean and safe water across residential, commercial, and industrial sectors is the primary catalyst for the growth of the carbon block filter market. Consumers are increasingly health-conscious and proactive in seeking solutions to remove a wide array of contaminants from their tap water, including chlorine, lead, volatile organic compounds (VOCs), and microplastics. This heightened awareness is directly translating into higher sales of point-of-use (POU) and point-of-entry (POE) filtration systems, where carbon block filters are a dominant technology. In the commercial sphere, establishments such as restaurants, hotels, and healthcare facilities are investing in advanced water purification to ensure product quality, customer satisfaction, and compliance with stringent health regulations. The industrial segment, in particular, presents a significant growth avenue. Industries ranging from pharmaceuticals and electronics manufacturing to food and beverage processing rely heavily on ultrapure water for their operations. Carbon block filters are instrumental in meeting these demanding purity requirements, safeguarding sensitive equipment, and ensuring the integrity of manufactured goods. Furthermore, the growing concern about emerging contaminants, such as PFAS (per- and polyfluoroalkyl substances), is driving innovation and adoption of specialized carbon block filters capable of effectively removing these persistent pollutants, further fueling market expansion.

Despite the promising growth trajectory, the carbon block filter market encounters several challenges. One of the primary restraints is the higher initial cost associated with carbon block filters compared to their granular activated carbon (GAC) counterparts. This cost differential can deter some price-sensitive consumers and smaller businesses from investing in these advanced filtration solutions. Another significant challenge is the limited lifespan and the need for regular replacement of carbon block filters. Once saturated, these filters lose their efficacy and require periodic replacement, which incurs ongoing maintenance costs for the end-user. This necessitates robust aftermarket support and a clear communication strategy from manufacturers regarding filter replacement schedules. The availability of alternative filtration technologies also poses a competitive threat. While carbon block filters excel in many areas, other technologies like reverse osmosis (RO) and ultrafiltration (UF) offer different levels of purification and may be preferred for specific applications or contaminants. Furthermore, consumer education and awareness regarding the specific benefits and maintenance requirements of carbon block filters remain an ongoing challenge. Misconceptions about their capabilities or the importance of timely replacement can hinder market penetration. Finally, fluctuations in raw material prices, particularly for activated carbon, can impact manufacturing costs and subsequently affect the final price of carbon block filters, creating potential pricing volatility for the market.

The Residential segment, particularly within the 5-20 Micron filtration type, is poised to dominate the global carbon block filter market, with a significant contribution expected from North America and Asia Pacific. These regions are characterized by a rapidly growing middle class with increasing disposable incomes and a heightened awareness of health and wellness. The demand for safe and purified drinking water at home is paramount, driving the adoption of various water filtration systems, with carbon block filters emerging as a preferred choice due to their superior performance in removing common impurities like chlorine, sediment, and unpleasant tastes and odors.

Residential Segment Dominance: In North America, established markets like the United States and Canada have a long-standing appreciation for water quality, leading to widespread adoption of home filtration systems. The increasing prevalence of aging water infrastructure in some areas further fuels this demand. In Asia Pacific, countries such as China, India, and Southeast Asian nations are experiencing rapid urbanization and industrialization, leading to a corresponding rise in water pollution concerns. As disposable incomes grow in these regions, consumers are increasingly investing in household appliances that enhance their quality of life, including advanced water purifiers that commonly utilize carbon block filters. The trend towards healthy living and the growing concern over the presence of microplastics and other emerging contaminants in tap water are significant drivers for this segment. The ease of installation and maintenance of POU systems featuring carbon block filters makes them particularly attractive to homeowners.

5-20 Micron Type: The 5-20 Micron filtration range is expected to capture a substantial market share. This micron rating strikes an optimal balance between effective sediment removal and maintaining sufficient water flow rates. It is highly effective in capturing common impurities such as rust, sand, silt, and larger suspended solids, which are prevalent in many municipal and well water sources. This level of filtration is crucial for protecting downstream appliances and ensuring palatable drinking water. While larger micron filters (> 20 Micron) serve as pre-filters for gross sediment, and finer micron filters (e.g., sub-micron) are used for specialized applications, the 5-20 Micron range offers a versatile and cost-effective solution for a broad spectrum of residential and many commercial applications. The technology behind achieving consistent pore structures within this range allows for reliable performance and predictable contaminant capture, making it a cornerstone of many standard water filtration cartridges. Companies are investing in R&D to optimize the density and composition of carbon block filters within this micron range to maximize adsorption capacity and filtration efficiency.

Several key factors are acting as powerful catalysts for the carbon block filter industry. The increasing global emphasis on public health and water safety regulations mandates stricter water quality standards, driving demand for effective filtration solutions. Furthermore, the rising consumer awareness and concern about emerging contaminants like PFAS and microplastics are spurring innovation and the development of specialized carbon block filters capable of tackling these challenges. The expanding industrial sector, particularly in manufacturing and food processing, where water purity is critical, is a significant growth driver. Moreover, the ongoing technological advancements in activated carbon production and extrusion techniques are leading to more efficient, durable, and cost-effective carbon block filters.

This comprehensive report delves into the multifaceted global carbon block filter market, offering an in-depth analysis of trends, drivers, and challenges from 2019 to 2033. The study provides granular insights into market segmentation by type and application, with a particular focus on the dominant 5-20 Micron category and its significant impact on Residential and Commercial sectors. It meticulously examines growth catalysts, including rising health consciousness and stringent regulations, while also addressing restraints such as cost sensitivities and the need for regular maintenance. The report features a detailed competitive landscape, profiling leading players and their strategic developments, alongside a thorough exploration of key regional market dynamics. The comprehensive nature of this analysis ensures that stakeholders gain a profound understanding of the market's current state and future potential, equipping them with the knowledge to make informed business decisions in this dynamic and evolving industry.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.7% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.7%.

Key companies in the market include Whirlpool, Carbon Block Technology, LG Electronics, Veolia Water Technologies, Omnipure, Samsung, Pentair, KX Technologies, Paragon Water Systems, WaterCare, Donaldson, Culligan, Multipure, Watts, Davey Microlene, Atlas Filtri, Puretec, Ningbo Dukang Ceramics, Hatenboer, Stefani, Pure-Pro Water Corporation, .

The market segments include Type, Application.

The market size is estimated to be USD 596.2 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Carbon Block Filter," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Carbon Block Filter, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.